No Fee Credit Card Processing: How It Works, What to Know, and Whether It’s Right for You

No Fee Credit Card Processing: How It Works, What to Know, and Whether It’s Right for You

EBizCharge is a 100% compliant surcharging solution and is rated 5-stars on G2.

As the common phrase goes, nothing in life is free, and the same can be said about no-fee credit card payment processing.

While some fees are inevitable regarding credit card processing, no-fee payment processing can be a great way to catch a merchant’s attention. Despite it not actually being free, small businesses still gravitate toward the promise of zero processing fees.

Before committing to no-fee credit card processing, there are a few things merchants should know first…

What is no-fee credit card processing?

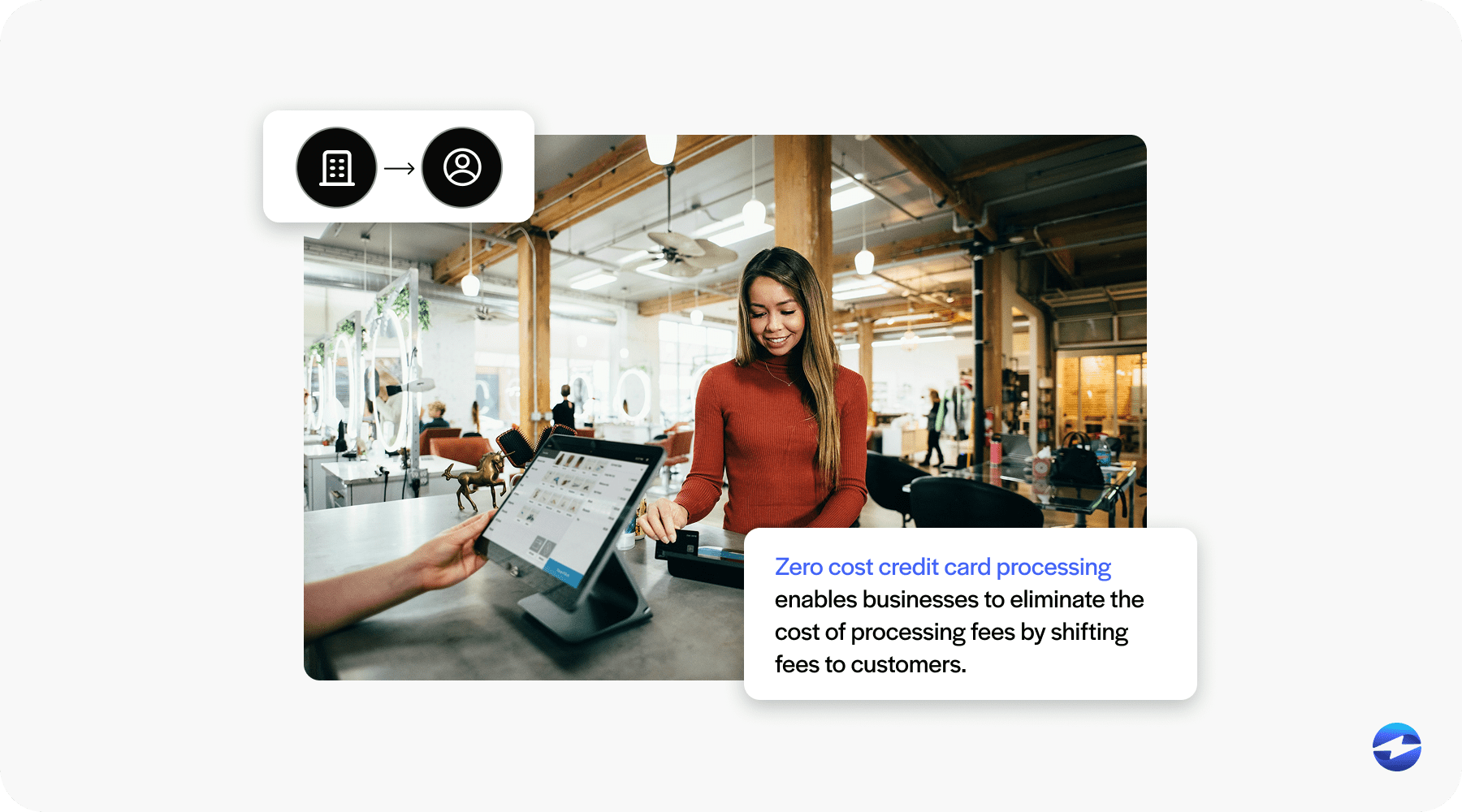

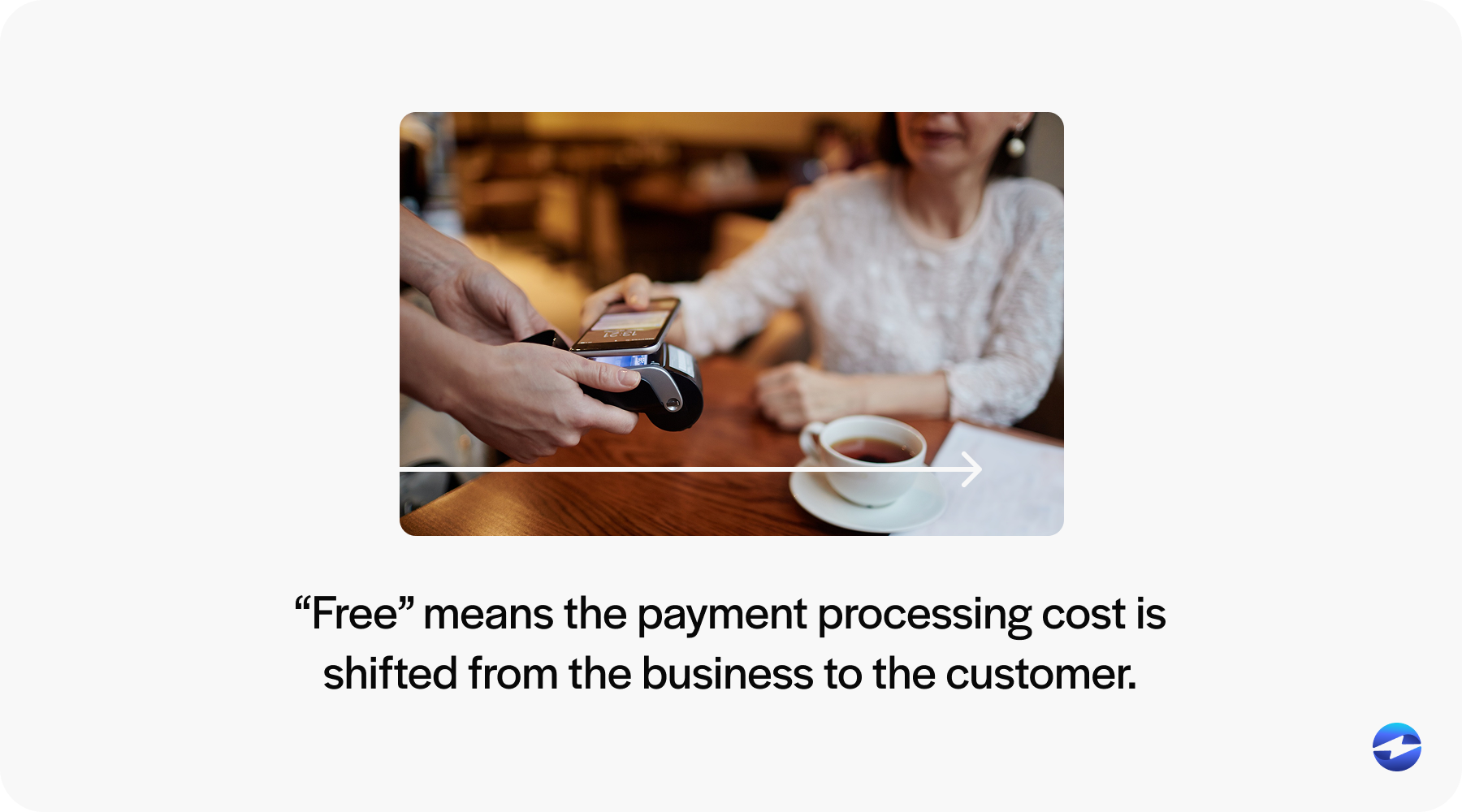

No-fee credit card processing, also called zero-cost processing, free credit card processing, zero-fee processing, or no-cost processing, all refer to the same thing. They all refer to a payment model where merchants stop paying credit card processing fees by passing those costs to customers through a surcharge at checkout.

Despite what the name implies, the fees do not disappear. They shift. Some processors market this as “free” to catch a merchant’s attention, but a more accurate term is surcharging. Surcharges are additional fees used to cover the costs of services that allow merchants to accept credit card payments. Surcharges are common for major credit card processors and are often advertised as no-fee solutions since they’re used by merchants to pass processing fees onto their customers.

What are credit card processing fees?

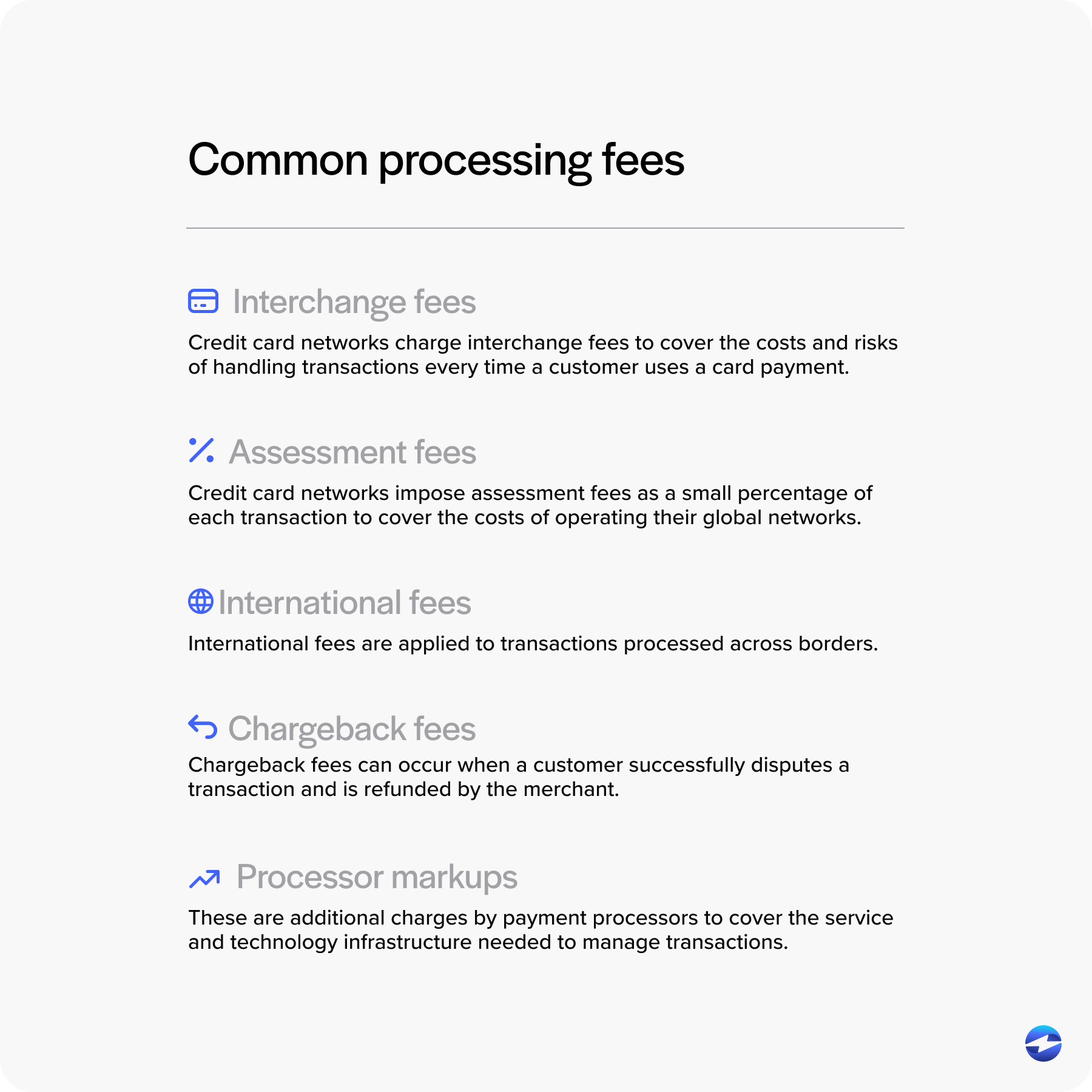

Before exploring no-fee processing, it helps to understand what fees merchants are actually trying to avoid. Every time a customer pays by card, the merchant pays a combination of three core fees:

- Interchange fees are paid to the card-issuing bank and typically consist of a percentage of the transaction plus a small fixed charge. These vary by card type and are usually the largest component of processing costs.

- Assessment fees are charged by the card networks (Visa, Mastercard, etc.) to cover operating costs. These are typically a small percentage of total sales volume.

- Merchant service fees are charged by the payment processor for managing and facilitating transactions. These can include per-transaction charges, monthly service fees, or bundled pricing models and vary significantly by provider.

Additional charges like chargeback fees, PCI non-compliance fees, and gateway fees can stack on top of these. For small businesses processing high volumes, these costs add up quickly, which is exactly why no-fee processing models have gained traction.

What’s the difference between no-fee credit card processing and surcharging?

There’s essentially no difference between surcharging and no-fee credit card processing but some companies will disguise their business as a no-fee processing program to entice merchants. These companies will typically advertise no-fee processing or free credit card processing as a package that consists of surcharging options.

No fee processing vs. cash discounting: what’s the difference?

No fee credit card processing and cash discounting are both ways to avoid absorbing processing fees, but they work differently and have different compliance requirements.

With surcharge-based no fee processing, the standard price is the base price and a fee is added at checkout for customers who pay by credit card. With cash discounting, the posted price already includes the processing fee built in, and customers who pay with cash or debit receive a discount off that price. The end result for the customer looks similar, but the structure is reversed — and that distinction matters for compliance.

Cash discounting is permitted in all 50 states, including states that restrict or limit surcharging. If you’re operating in a restricted state, cash discounting is often the compliant alternative. Dual pricing is a third variation that displays both the cash price and the card price side by side at the point of sale, letting customers choose before committing to a payment method.

The right approach depends on your state, your customer base, and how your terminals are programmed.

Zero Fee vs. No Cost vs. Low Cost vs. Free Credit Card Processing

These terms get used interchangeably in payment processing marketing and they all refer to the same basic concept: a program that reduces or eliminates what the merchant pays out of pocket for credit card processing. The cost doesn’t disappear. It shifts.

Zero cost processing and no cost processing mean the merchant pays nothing directly toward transaction fees because those fees are passed to the customer as a surcharge. Zero fee processing and free credit card processing are the same thing with different branding. Low cost credit card processing is a broader term that sometimes refers to surcharging programs and sometimes refers to processors offering reduced interchange rates or flat monthly pricing without full cost elimination.

If a provider is advertising any of these options, the first question to ask is whether they mean surcharging, a cash discount program, or simply a cheaper pricing model. The answer changes what the program looks like for your customers and what compliance requirements apply.

How does no-fee credit card processing work?

When a merchant sets up a credit card processing solution, physical and online terminals need to be programmed to process these payments. No-fee payment processing requires these terminals to be programmed to add a markup on the purchase which covers the credit card processing fees for that particular transaction.

However, there’s a limit to how much the surcharge markup can consist of which typically varies by state — most states will set a limit of roughly 4%. Merchants should first check local laws to verify if no-fee payment processing is permitted in their state before implementing.

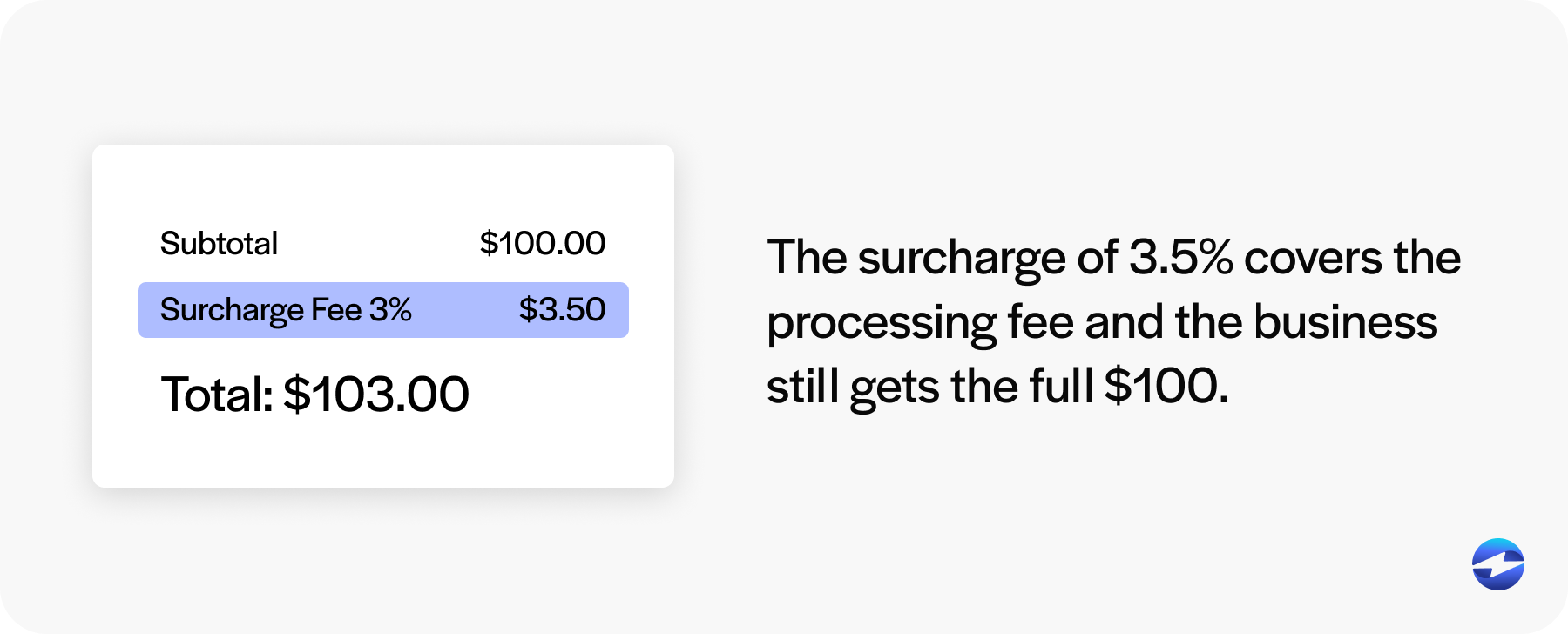

Here’s an example to show you how this all works…

Let’s say a customer is buying a $100 snow jacket from a retailer using a credit card. The cashier inputs the payment type as a credit card purchase which adds an additional fee to the overall transaction to cover the credit card processing fees. If the markup to cover the processing fee is 4%, then an extra $4 would be added to the transaction.

While no-fee credit card processing may sound simple, it can come with its own set of complications.

What about ACH payments?

ACH and eCheck payments offer a parallel cost-saving alternative worth knowing about. Unlike credit card transactions, ACH payments transfer funds directly between bank accounts through the ACH network, bypassing card networks entirely. This means no interchange fees and no surcharge complications — just a flat rate or small percentage per transaction, typically far lower than credit card processing costs.

For businesses looking to minimize fees without passing costs to customers, promoting ACH as a payment option alongside a no-fee credit card program gives customers a genuinely low-cost path and reduces the merchant’s overall processing burden.

The legality of no-fee processing

Businesses can charge a fee for paying with a credit card, but no-fee payment processing can be a controversial topic, depending on which party you ask. Banks typically don’t agree with the idea of passing processing fees onto customers and as a result, multiple legal cases have arisen regarding the matter.

Banks are typically against no-cost credit card processing because of the implications it has for credit card payments. If merchants add additional fees to customers’ credit card transactions, they’ll be less inclined to pay with a card. In fact, in a 2025 survey of 650 businesses, we found that when companies do charge fees, 62% see customers switch to cheaper payment methods.

Although banks want to promote the use of credit cards, merchants often want the opposite to avoid high credit card processing fees. This dispute has even led to the prohibition of no-fee payment processing in some states. Make sure to check the credit card surcharge laws by state before implementing no-fee merchant services. As of 2026, Connecticut, Maine, and Massachusetts prohibit credit card surcharging entirely. Oklahoma limits surcharges to 3%. Several other states have disclosure and cap requirements that vary. Checking your specific state’s rules before enabling no-fee credit card processing is essential; non-compliance can result in fines or loss of card acceptance privileges.

Card network guidelines

Beyond state laws, Visa, Mastercard, American Express, and Discover all have their own policies governing surcharging that merchants must follow. Violating these rules can result in penalties, card acceptance restrictions, or termination of your merchant account.

Key requirements to be aware of:

- Fee caps. You generally cannot charge more than 3% as a surcharge, even if your actual processing costs are higher. In some cases card networks may limit you to your exact cost of acceptance.

- Brand parity. If you apply a surcharge, it must be applied equally across all credit card brands. You cannot selectively charge a fee on Visa transactions while exempting Mastercard or American Express.

- Advance notice. Most card networks require merchants to provide formal notice at least 30 days before starting a surcharging program. This includes completing an online registration form and submitting specific business details. This step is mandatory and cannot be skipped.

These are not optional guidelines — they are contractual obligations with your payment processor. Make sure your processing solution includes built-in tools to help you stay current with network rules.

No-fee credit card processors

No-fee payment processing is a great option for businesses with lower sales volumes. Credit card processing fees can add up quickly, so saving money is crucial, especially for smaller businesses.

No-fee credit card processors are also a great option because they automate various processes that would otherwise be left to the merchant. All the merchant needs to do is notify their customers of the surcharge for credit card transactions. Solutions like EBizCharge make this even easier by offering credit card processing for QuickBooks and Epicor payment processing, so surcharges are applied automatically and every transaction syncs directly to your accounting system.

How to implement no-fee credit card processing

Once you’ve decided no-fee processing is right for your business, here’s how to roll it out:

- Verify compliance. Surcharging is regulated at the state level and governed by card network rules. Connecticut, Maine, and Massachusetts prohibit it entirely. Oklahoma caps it at 3%. Research your state’s laws and card brand policies before proceeding. Cash discounting is legal in all 50 states and is often the simpler compliant alternative.

- Choose a trusted provider. Look for a processor that offers built-in surcharging or cash discounting with automated compliance safeguards, transparent pricing, and no hidden fees. The right provider will handle configuration, signage requirements, and disclosure needs so you’re not managing compliance manually.

- Update your POS system. Your terminals need to be programmed to identify credit vs. debit cards, apply the surcharge only to credit transactions, itemize it on receipts, and stay within your state’s cap. For cash discounting, the system should display the card-inclusive price and deduct the discount at cash checkout.

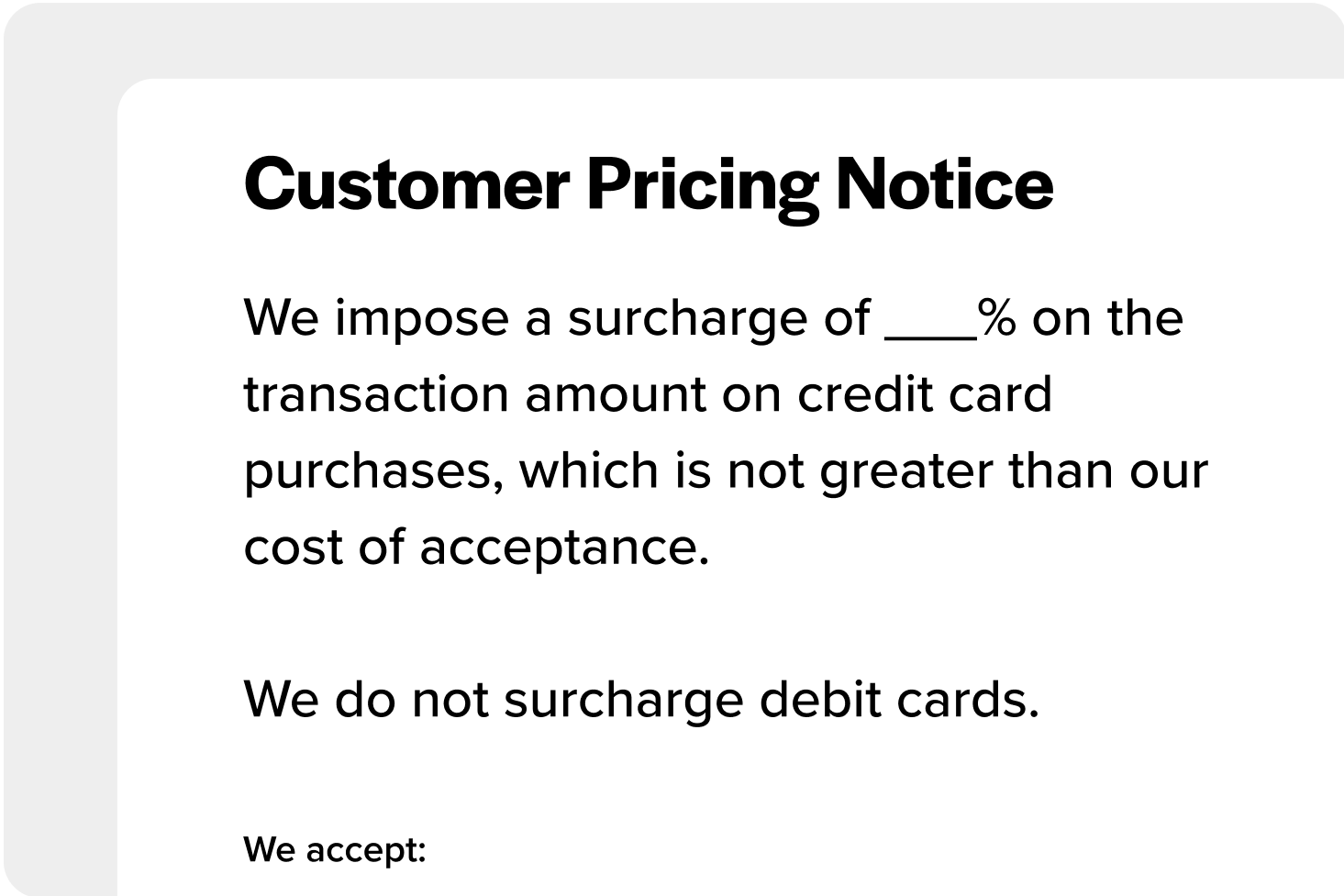

- Notify your customers. Post signage at your storefront entrance, POS terminal, and online checkout. Receipts must itemize the surcharge separately. When framed as a way to keep base prices lower for everyone, most customers are receptive.

What About No Monthly Fee Credit Card Processing?

Some merchants searching for zero cost processing are actually trying to solve a different problem: avoiding the flat monthly fees that many processors charge regardless of transaction volume. These are two separate issues worth distinguishing.

No monthly fee processing refers to payment processing contracts that don’t charge a recurring subscription regardless of whether you process any transactions. Processors that offer this model typically charge slightly higher per-transaction rates instead. For low-volume businesses, this can work out cheaper. For high-volume businesses, a monthly fee with lower per-transaction rates usually makes more sense.

Surcharge-based zero cost programs are separate from this. They address transaction fees specifically. Some processors offering surcharging programs still charge monthly platform or software fees on top. Checking the contract for both fee types before signing is worth the time.

Despite saving merchants money, there are still some costs involved with no-fee payment processing.

The reality of no-fee processing fees

There’s no denying that no-fee credit card processing allows merchants to reduce their operational costs by passing processing fees to their customers, but there are other fees they may not be able to avoid.

It’s important to check the fine print to verify which fees are included in your credit card processing contract. Some of the most common fees to look out for include:

Equipment fees example: Point of sale (POS)

In addition to extra fees, no-fee payment processing services often require hardware like Point of Sale (POS) systems to be installed and set up. Some payment processors may even require merchants to lease this equipment.

Some service providers will offer preprogrammed POS equipment but may not require leasing this equipment to use their services. Although reprogramming your current POS equipment can be a hassle, it’s far more convenient in the long run.

Leasing pre-programmed equipment could result in a long-term contract which can be problematic if a merchant decides to switch providers. A long-term contract could prevent merchants from switching providers and even land the merchant in a lawsuit should they try to make the switch.

Setting up credit card surcharging

To set up surcharging, merchants can work with their credit card processors to update their payment terminals with the necessary software.

Virtual terminals must be programmed to list surcharges on a separate item line on the customer’s receipt. The terminal must also be programmed to charge no more than the state’s maximum surcharge amount which varies by state.

The terminal will also need to be able to differentiate between debit and credit cards to ensure surcharges are only added for credit card transactions.

What does surcharge-free mean?

Surcharge free refers to transactions or programs where no surcharge is added to the customer’s payment. From a merchant perspective, a surcharge-free transaction means the business is absorbing the processing cost rather than passing it to the customer. Some processors market themselves as offering a “surcharge-free guarantee” for customers, meaning their cardholders won’t see extra fees at the point of sale regardless of where they shop.

For merchants, surcharge free is also sometimes used to describe debit card transactions specifically since surcharges on debit are prohibited. A transaction being surcharge free doesn’t mean it’s free to process, it just means the cost stays with the merchant.

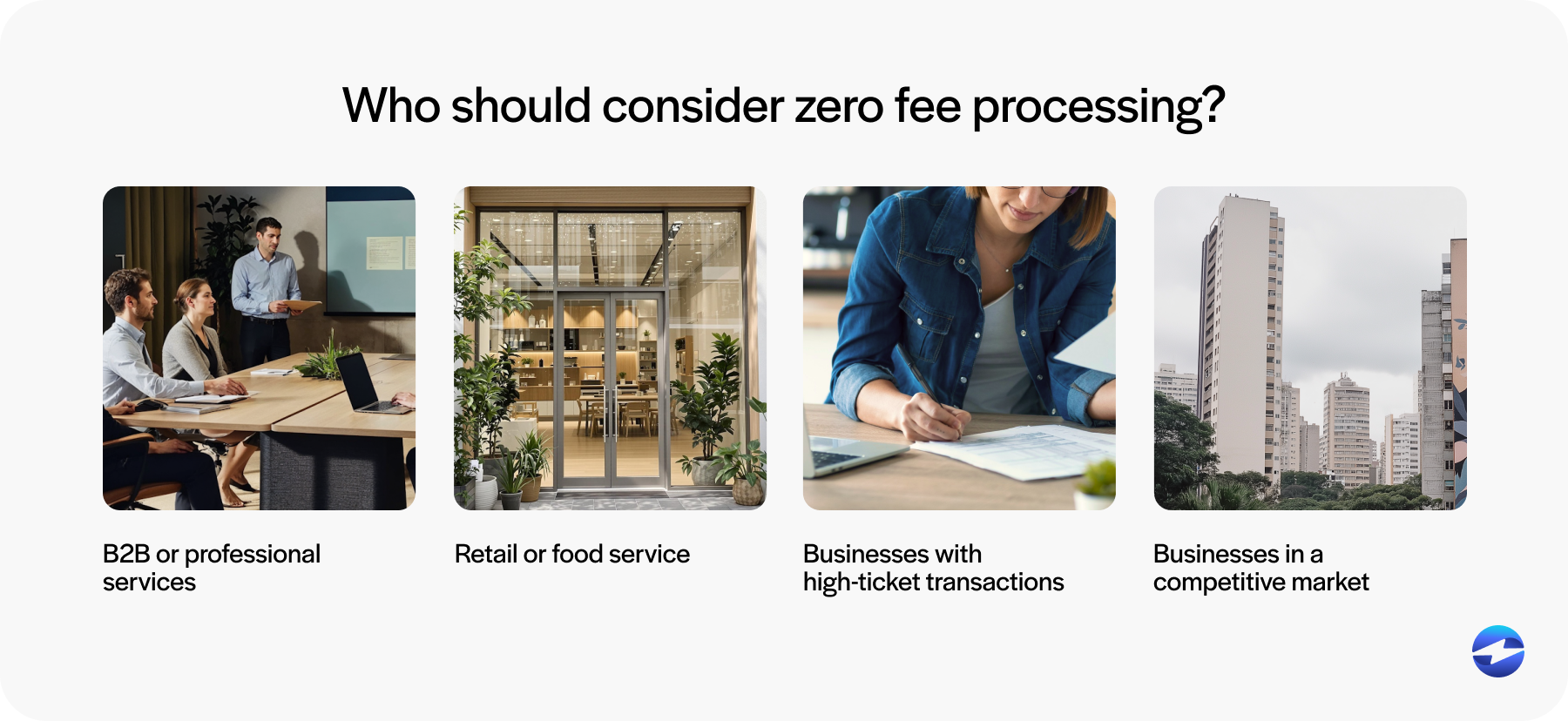

Which businesses can use no-fee processing?

No fee credit card processing works best for businesses where processing fees are cutting meaningfully into margins.

- Small businesses with lower transaction volumes benefit because every dollar saved on fees matters more when revenue is thin.

- High-risk merchants who already face elevated processing rates can offset those costs by passing them to customers rather than absorbing them.

- Enterprise-level businesses with high monthly volumes benefit simply from the math — even a 2–3% fee on millions of dollars in transactions adds up fast.

That said, no fee credit card processing isn’t the right fit for every situation. Take advantage of no-fee processing to reduce operational costs. Businesses in highly price-sensitive markets, or those where customer experience is a differentiator, should weigh the potential impact on customer satisfaction before implementing surcharging.

Is no-fee processing the right fit for your business?

Choosing to add a surcharge is not just a pricing decision — it is a business strategy that has to align with how your customers think and how your business operates.

If you are in B2B or professional services. Clients in these sectors are generally accustomed to administrative or convenience fees. A 3% card fee on a $2,000 invoice is unlikely to raise eyebrows, and clients often care more about net terms than the checkout experience.

If you run a retail store or food service business. Things get trickier. A customer paying for a $3 coffee may feel nickel-and-dimed by a surcharge appearing at checkout. If your brand depends on loyalty and regular foot traffic, the customer experience impact is worth weighing carefully before implementing.

If your average transaction size is high. The savings become more meaningful at higher ticket sizes. A 3.5% surcharge on a $500 transaction is $17.50 you no longer owe the processor. Businesses with infrequent but high-value transactions tend to see the clearest benefit.

If you operate in a competitive market. Think about what your competitors are doing. If they are absorbing processing costs and you are not, you will need to clearly communicate your fee structure and make the case for why customers should stay.

You know your customers better than anyone. The right choice balances your margins with their expectations and your competitive position in the market.

Pros and cons of no-fee credit card processing

Before committing, it’s worth weighing the benefits and trade-offs honestly.

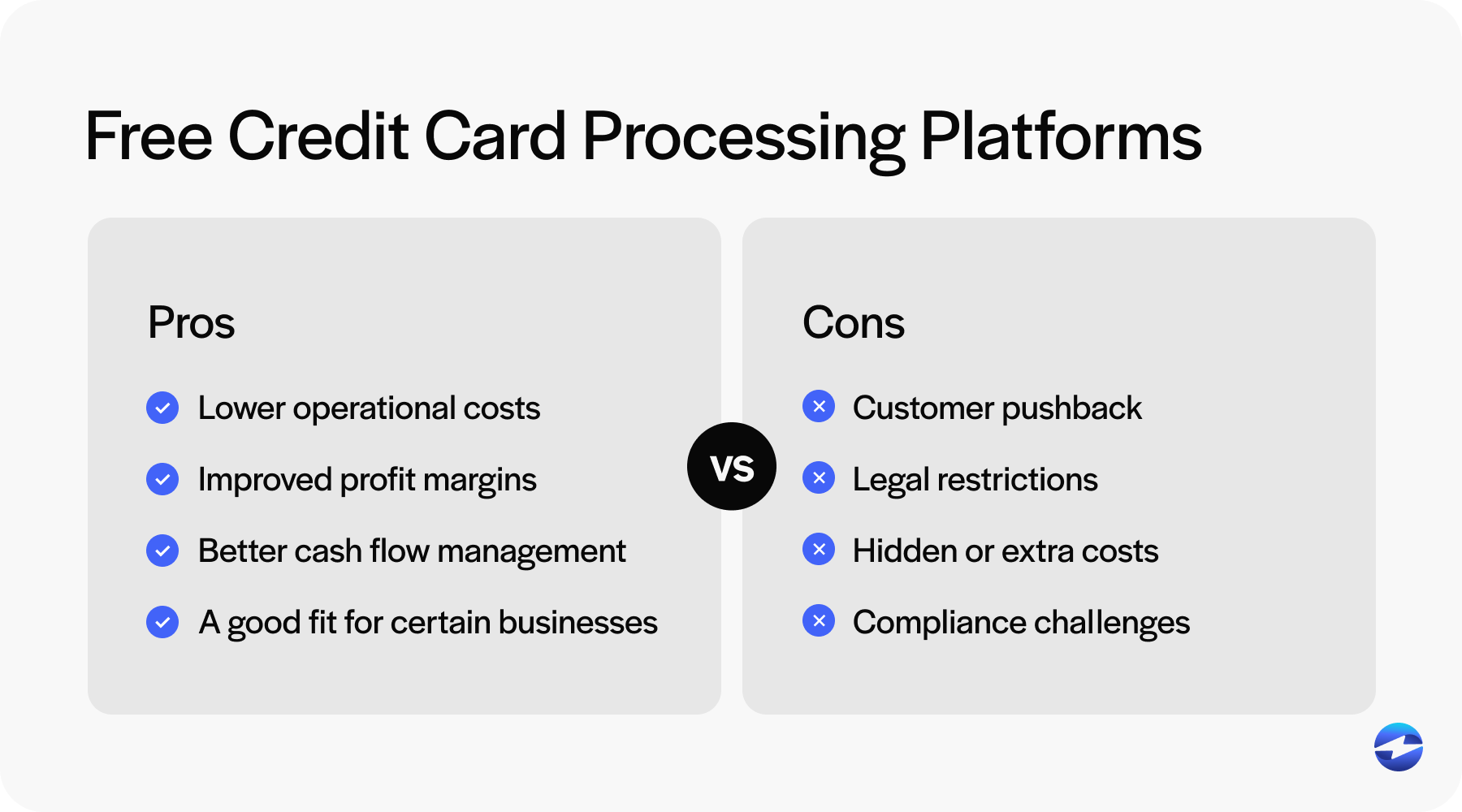

Pros:

- Reduces or eliminates the cost of credit card processing for your business

- Allows you to maintain profit margins without inflating base prices

- Gives customers a choice — pay the surcharge or switch to a non-credit method like debit, ACH, or cash

- Creates transparency around payment costs rather than burying them in pricing

Cons:

- Some customers push back against added fees, particularly if they weren’t expecting them

- Unclear or late disclosure of fees risks non-compliance and damages customer trust

- Not all processors handle surcharging correctly, which can create technical or legal issues

- Businesses in price-sensitive markets may see customers switch payment methods or abandon transactions altogether

Customer perception plays a major role in how well this model works. When communicated clearly and implemented correctly, no-fee processing is a sustainable way to reduce overhead. When it’s poorly presented, it can backfire.

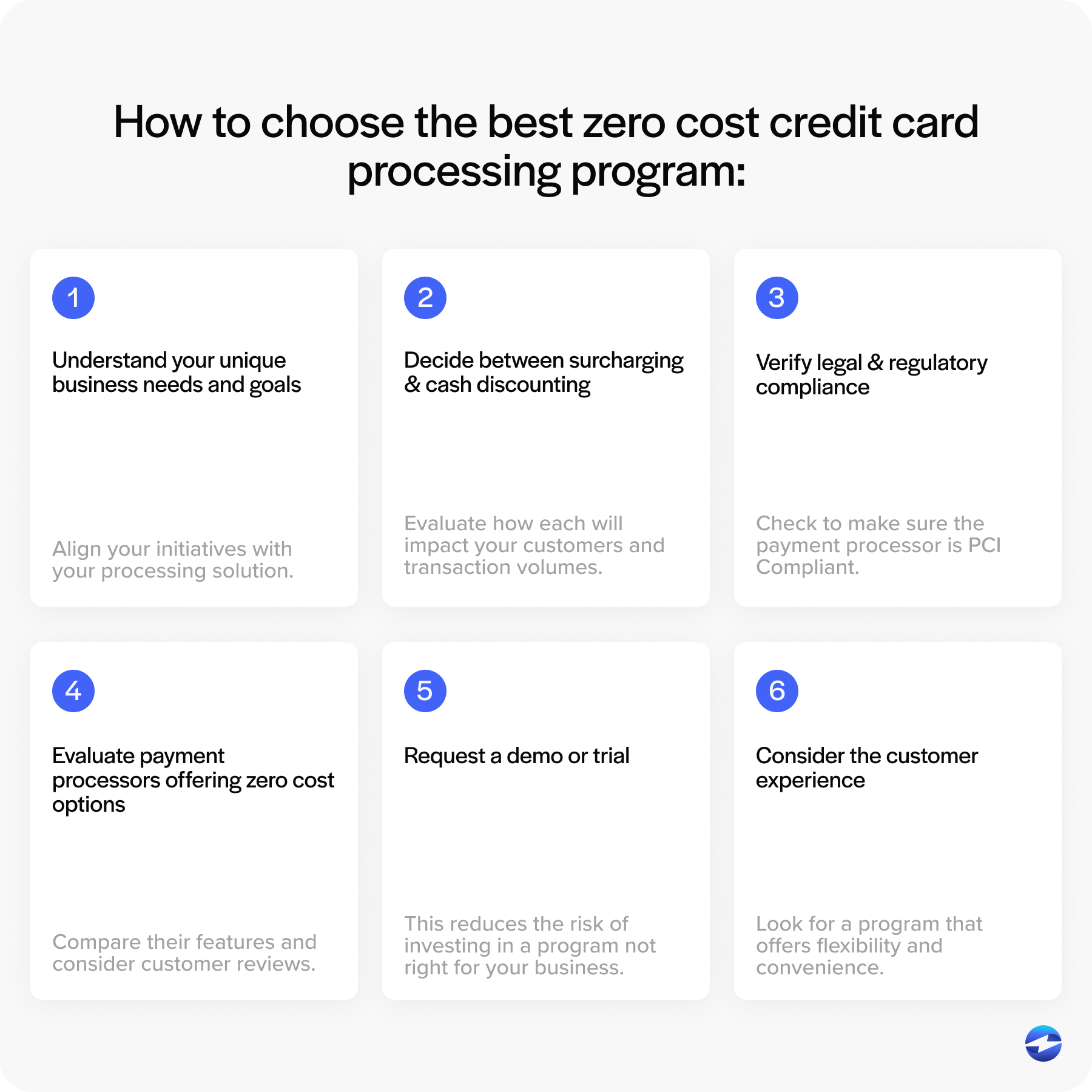

How to choose the right no-fee processing program and provider

Not all no-fee programs are built the same. Here are the key factors to evaluate before committing:

- Understand your business needs. Consider your average transaction size, volume, and whether you primarily process in-person or online. These factors determine which program type fits best and where savings will be most meaningful.

- Decide between surcharging and cash discounting. Surcharging adds a fee for credit card use; cash discounting rewards customers who pay with cash. Surcharging can recover more fees but may deter some card users. Cash discounting is universally legal and often smoother for customer experience.

- Verify compliance for your state. Non-compliance can result in fines or loss of card acceptance privileges. Confirm your program meets both state law and card network rules.

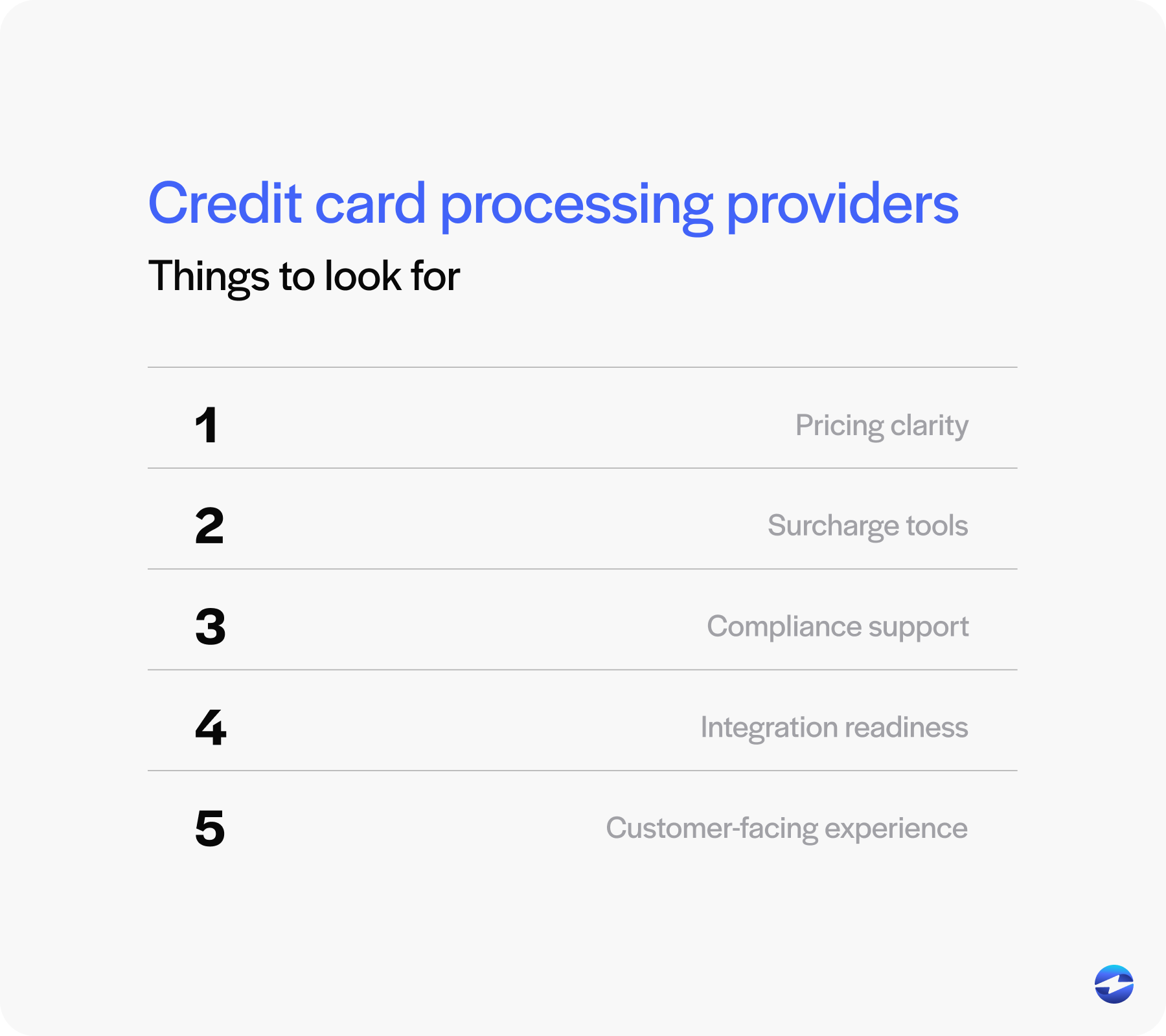

- Evaluate processors carefully. Look for transparent pricing, no long-term contracts, positive reviews, and built-in compliance support. Watch for monthly platform fees that may exist alongside the no-fee program itself.

- Check integration readiness. Will it work with what you already use? Look for direct compatibility with your POS system, eCommerce platform, accounting software, and invoicing tools. A surcharging solution that does not connect to your existing systems creates more work, not less.

- Request a demo or trial. Test the system before committing. This lets you evaluate ease of use, compatibility with your current equipment, and customer support responsiveness.

- Consider the customer experience. A program that’s confusing or feels punitive can hurt retention. Choose a setup that’s transparent, easy to explain, and gives customers genuine payment flexibility.

With the right program selected and your evaluation complete, the next step is putting it to work.

Hidden fees to watch out for

Just because a platform calls itself free does not mean the service is. Many no-fee processing platforms still build in costs elsewhere that can quietly add up. Before signing with any provider, ask for a complete cost breakdown and watch specifically for:

Monthly platform or software fees. Some providers charge a recurring subscription regardless of how many transactions you process. This is separate from the no-fee surcharging program and can offset your savings at lower volumes.

PCI compliance charges. PCI compliance fees are sometimes bundled in and sometimes billed separately. Confirm upfront whether compliance support is included or an add-on.

Terminal rental or leasing costs. Some providers require you to lease pre-programmed equipment rather than own it. A long-term equipment lease can become a problem if you decide to switch providers, potentially locking you into a contract or exposing you to early termination fees.

Early termination fees. Always check whether the agreement includes a long-term contract with penalties for leaving early. A provider confident in their service should not need to lock you in.

Interchange markups under pass-through pricing. Even under so-called pass-through or interchange-plus pricing, some providers add their own markup on top of the actual interchange rate. Always ask what the processor’s margin is, not just the interchange rate.

The total cost of a no-fee program is rarely just the surcharge. Reading the fine print before signing protects you from surprises later.

Take advantage of no-fee processing to reduce operational costs

After learning about all the components involved in zero-cost credit card processing, merchants can make more informed decisions when deciding if surcharging options are right for their business.

While no fee credit card processing still comes with some costs (PCI fees, equipment, and platform charges depending on your contract), it remains one of the most effective ways for merchants to reduce what they pay out of pocket on every transaction. EBizCharge offers a built-in credit card surcharge program that automates the entire process and connects through 100+ software integrations, so surcharge calculations and payments post directly to your accounting software without any manual work.

Frequently Asked Questions

How to get free credit card processing for my small business?

To get free credit card processing for your small business, you can use a no-fee model that passes the costs to customers through surcharges or cash discounts. Just make sure you’re following local laws and think about how it might impact your customer experience.

What is zero cost credit card processing?

Zero cost credit card processing is a payment model where merchants pass credit card transaction fees to customers as a surcharge rather than absorbing them. The merchant pays little to nothing in processing fees per transaction. It goes by many names including no-fee, no-cost, and zero-fee processing, but they all refer to the same surcharging-based model.

Is zero cost credit card processing actually free?

Not entirely. Transaction fees are shifted to the customer rather than eliminated. Merchants may still pay PCI compliance fees, equipment fees, monthly platform fees, and service charges depending on the processor and contract. Reviewing the fine print before signing is worth the time.

Is zero cost credit card processing legal?

Yes, zero cost credit card processing is legal at the federal level, but legality varies by state. Connecticut, Maine, and Massachusetts prohibit surcharging entirely, Oklahoma caps it at 3%, and several other states have specific disclosure and fee requirements. Merchants must also follow card network rules around fee caps, brand parity, and advance notice. Cash discounting is legal in all 50 states and is often the simpler compliant alternative for businesses in restricted states.

What does surcharge free mean?

Surcharge free means no surcharge is added to the customer’s transaction. From a merchant perspective, it means absorbing the processing cost rather than passing it to the customer. Debit card transactions are always surcharge free since surcharges on debit are prohibited under card network rules.

What is the difference between zero cost processing and low cost credit card processing?

Zero cost processing eliminates what the merchant pays per transaction by passing fees to the customer through a surcharge. Low cost credit card processing refers more broadly to processing arrangements with reduced rates, which may include surcharging programs, interchange-plus pricing, or flat-rate pricing structures. Not all low cost programs pass fees to customers.

How do I set up zero cost credit card processing?

Setting up zero cost processing involves working with your payment processor to program terminals to add a surcharge to credit card transactions, registering with Visa and Mastercard at least 30 days in advance, and ensuring disclosure requirements are met at the point of sale and on receipts. The surcharge cannot be applied to debit or prepaid cards.

Which businesses work best with no-fee credit card processing?

Small businesses with thin margins, high-risk merchants facing elevated processing rates, and enterprise-level businesses with high transaction volumes tend to benefit most from no-fee processing programs. The model works best in industries where customers are accustomed to or accepting of surcharges.