Passing Credit Card Fees to Customers: 4 Legal Methods Explained

Passing Credit Card Fees to Customers: 4 Legal Methods Explained

EBizCharge is a 100% compliant surcharge solution and is rated 5 stars on G2.

When accepting credit card payments from customers, merchants are expected to pay fees to various parties — card issuers, card networks, and payment processors — which can add up over time.

Luckily, businesses can alleviate these costs by directly or indirectly passing credit card fees to customers using several methods.

Can businesses charge a credit card fee?

Yes, in most states. Businesses can legally charge customers a fee for paying with a credit card, but the rules depend on which type of fee you’re charging, which state you operate in, and which card networks you accept.

- Surcharging is permitted in most states but banned in a few.

- Convenience fees are legal in all states when structured correctly.

- Cash discounting is legal everywhere.

- Minimum purchase requirements are federally permitted up to $10 for credit card transactions.

Charging a credit card fee is legal for most U.S. merchants, provided you choose the right method for your state and follow card network disclosure requirements. The sections below break down each option.

4 ways to pass credit card fees to customers

A common question merchants have is it illegal to charge a credit card fee? The short answer is no, in most states it is permitted, provided you follow card network rules and state regulations.

Merchants can pass cc fees to customers using four main methods:

- Credit card surcharging

- Minimum purchase requirements

- Convenience fees

- Cash discounting

| Method | How It Works | Legal in All States | Applied To | Customer Pays More |

|---|---|---|---|---|

| Surcharging | Adds a fee to credit card transactions | No | Credit cards only | Yes |

| Cash discounting | Lowers price for cash payments | Yes | All payment types | No |

| Convenience fee | Adds fee for alternative payment channels | Yes (varies by network) | Specific channels | Yes |

| Minimum purchase | Sets a $10 minimum for card use | Yes | Credit cards only | Indirectly |

1. Credit card surcharging

With surcharging, merchants are able to automatically pass credit card fees to their customers when a credit card is used at checkout.

Credit card surcharging allows businesses to pass on the financial burden of credit card processing fees by attaching an extra fee to each customer’s credit card transaction. Surcharges are regulated by credit card brands and state governments and can range from 1.5% to 4%, depending on a merchant’s preference.

It’s important to note that merchants can only use surcharging to offset processing costs — they cannot profit off of these charges — and must disclose any charges to their customers with credit card surcharge signage.

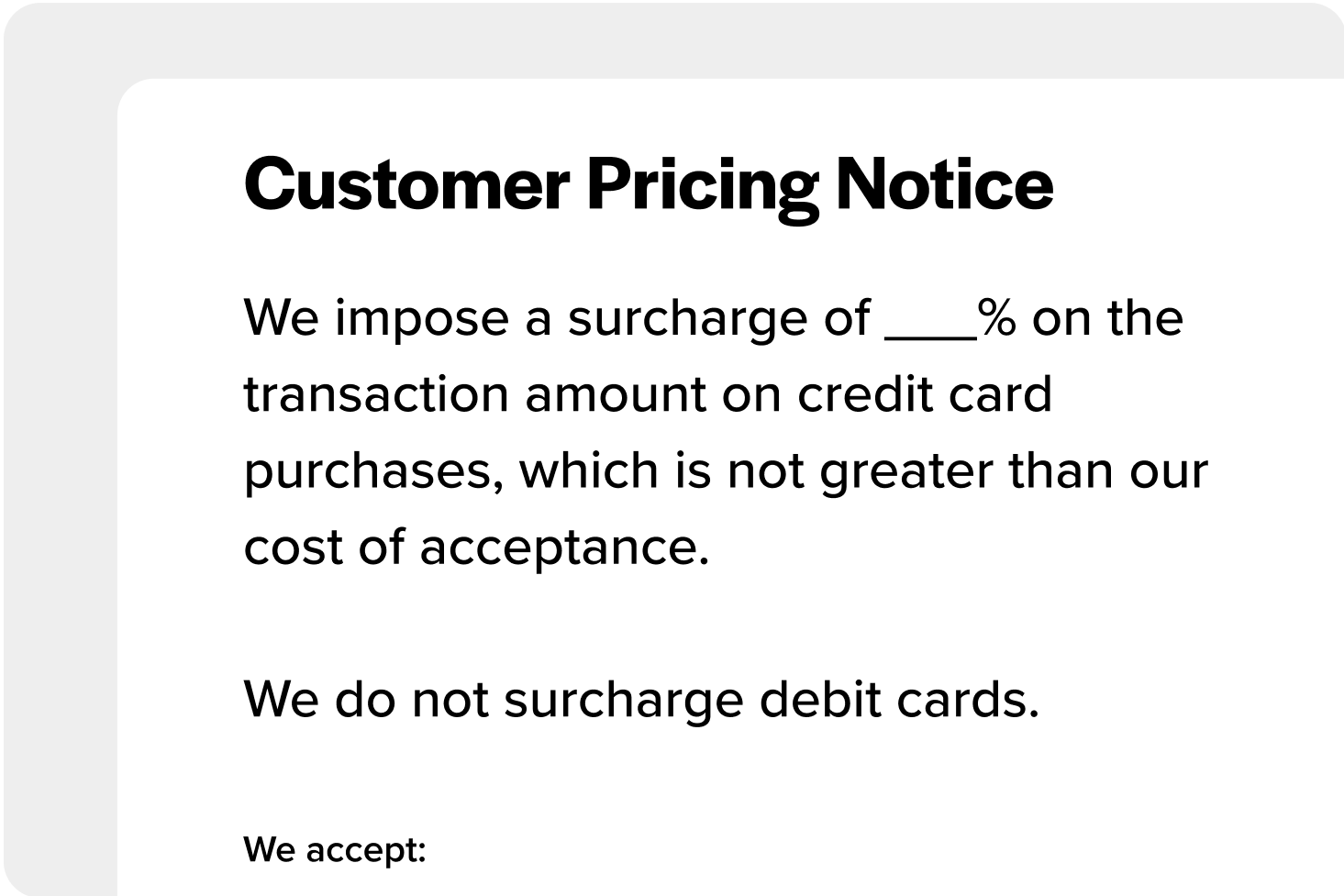

Credit card surcharge sign requirements

Before you start surcharging, signage is not optional. Both Visa and Mastercard require merchants to post a notice at the point of entry and at the point of sale.

Here is what those signs must include and where they need to go:

What the sign must say:

- That a surcharge applies to credit card transactions

- The surcharge percentage or dollar amount

- That the surcharge does not exceed your cost of acceptance

- That the fee applies to credit cards only, not debit cards or prepaid cards

Where to post it:

- At the point of entry: store entrance, website homepage, or the first page of a checkout flow

- At the point of sale: the register, payment terminal screen, or the payment step of an online checkout

Visa and Mastercard rules: Visa requires merchants to notify Visa and their acquirer at least 30 days before implementing a surcharge. Mastercard has the same 30-day notification requirement. Both networks require that signage be posted at entry and at the point of sale before any surcharge is collected. Failing to post proper notice can result in fines or losing the right to accept those cards.

Businesses need to review and stay up-to-date on their state laws since surcharging is illegal in some states.

2. Minimum purchase requirements

Businesses that process many small-ticket purchases can still be subject to high processing costs. Thankfully, minimum purchase requirements provide a legal way to pass credit card fees to customers to mitigate these charges.

With minimum purchase requirements, merchants can enforce a credit card minimum purchase amount — no more than $10 — which helps them avoid and minimize processing fees on smaller tickets. Customers unable to meet this threshold will be directed to use cash to complete their transactions.

Minimum purchase requirements tend to favor smaller businesses like convenience stores since they typically handle low-ticket items and can use this method to offset the associated processing costs.

While merchants are not required to disclose minimum purchase requirements, signs and verbal communication with customers can encourage a more transparent transaction process.

3. Convenience fees

While convenience fees offer another effective option for merchants passing credit card fees to customers, they can’t be applied to every credit card purchase and may vary by the card issuer.

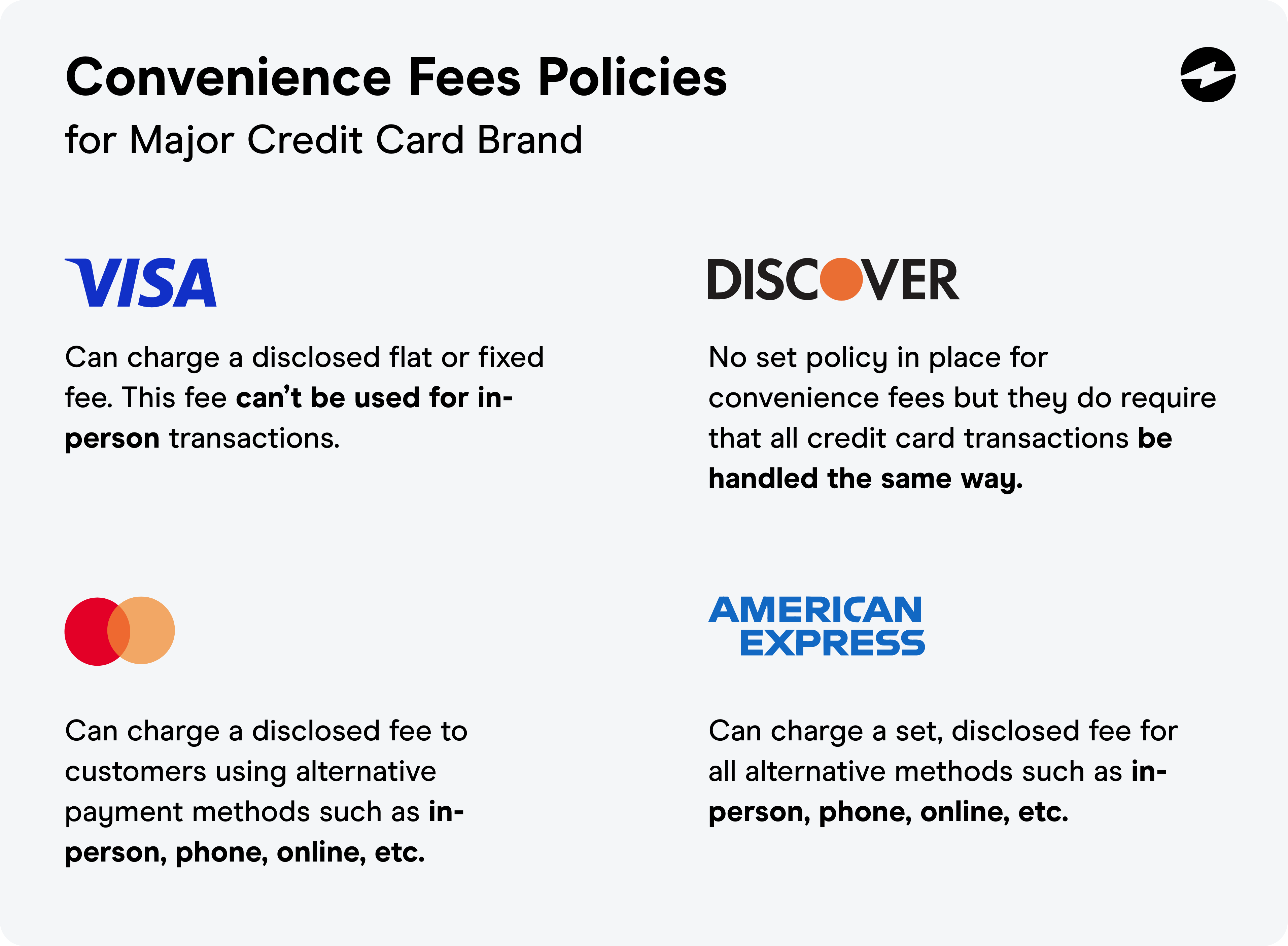

Convenience fees are typically implemented when products or services are purchased using alternative or unconventional payment methods, or if there’s another preferred form of payment. Each major credit card network has its own set of policies for convenience fees:

- Visa: Merchants can charge a disclosed flat or fixed fee for the convenience of using a Visa credit card as an alternative payment method. This fee can’t be used for in-person transactions.

- Mastercard: Merchants can charge a disclosed credit card convenience fee to customers using alternative payment methods such as in-person, phone, online, mailed-in payments, etc.

- American Express: Merchants can charge a set, disclosed fee for all alternative payment methods which include in-person transactions, recurring payments, subscriptions, etc.

- Discover: Discover has no set policy in place for convenience fees but they do require that all credit cards are handled the same way. This means merchants can’t limit convenience fees to one network — these charges must be added for all networks.

For transparency purposes, merchants can also send a credit card convenience fee letter to customers if they decide to add this extra charge on transactions.

Credit card convenience fee wording

When adding a convenience fee, you must disclose it before the transaction is completed. The exact wording will vary by context, but it needs to state the fee amount or percentage, when it applies, and how customers can avoid it. Here are three ready-to-use templates:

- Invoice or billing statement: “A convenience fee of [X]% has been applied to this invoice for payment by credit card. To avoid this fee, please remit payment by check or ACH bank transfer.”

- Point-of-sale or receipt: “A [X]% convenience fee applies to all credit card payments. Cash and check are accepted with no additional charge.”

- Online checkout: “Credit card payments are subject to a [X]% convenience fee. Select ACH or eCheck at checkout to pay with no added fee.”

Convenience fee notification letter template

If you are adding a convenience fee to credit card transactions, notifying customers in writing before the change takes effect helps maintain trust and keeps you compliant with card network disclosure requirements. Here is a template to adapt:

Adjust the fee amount, effective date, and accepted payment alternatives to match your setup. If customers have a payment portal or specific remittance instructions, include those details in place of the general contact line.

Convenience fee vs surcharge

It’s important to not confuse convenience fees with surcharges. Merchants can add surcharges to any credit card transaction with the intent to offset processing costs. Whereas, convenience fees can only be added to transactions that use an unusual or alternative form of payment.

4. Cash discounting

Merchants that want to avoid charging their customers extra can also look into cash discounting to incentivize a different payment method instead of penalizing their customers.

Rather than passing credit card fees to customers, businesses can use cash discounting to offer a discounted rate to customers who purchase with cash. This discount can encourage more people to pay with cash which helps merchants minimize or avoid processing fees altogether.

Cash discounting is most common for businesses like gas stations, convenience stores, and service-related businesses such as automotive shops. Cash discounting can be a great option for merchants in states where surcharging is illegal or has limitations.

Can you pass credit card fees to customers paying with a debit card?

No, merchants generally cannot surcharge debit card transactions the way they can credit card transactions. The Durbin Amendment, part of the Dodd-Frank Act, placed restrictions on debit card interchange fees and related practices. The card network rules mirror that separation. Debit cards are treated differently than credit cards under both card network rules and federal law.

Minimum purchase requirements are also off the table for debit cards. Federal law prohibits merchants from setting a minimum transaction amount for debit card purchases, even though a $10 minimum is permitted for credit cards.

Cash discounting is the most practical option when your goal is reducing costs on both card types. Since you are offering a lower price for cash rather than penalizing any specific payment method, it applies across the board without running into the restrictions that surcharging and minimums carry.

What you can do: passing on debit card fees to customers

Convenience fees on debit cards are also restricted in most cases. Visa prohibits convenience fees on debit card transactions in most merchant contexts, and Mastercard has similar limitations. If your setup includes convenience fees, confirm with your processor whether debit cards are covered under your specific agreement before applying the fee.

For merchants where debit card volume is high, cash discounting tends to be the most cost-effective path forward. Debit card customers pay the standard posted price; customers who pay with cash receive a discounted rate. No surcharge, no convenience fee, no compliance gap.

Is it legal to charge credit card fees?

Yes, in most states. The legality depends on which method you use and where you operate.

Surcharging is legal in most states but prohibited in a few, including Connecticut and Massachusetts. Convenience fees are legal in all 50 states when structured correctly. Cash discounting is legal everywhere. Minimum purchase requirements are federally permitted up to $10 for credit cards but cannot be applied to debit cards.

Each method carries its own disclosure requirements and card network notification steps, so getting the details right before implementing is essential.

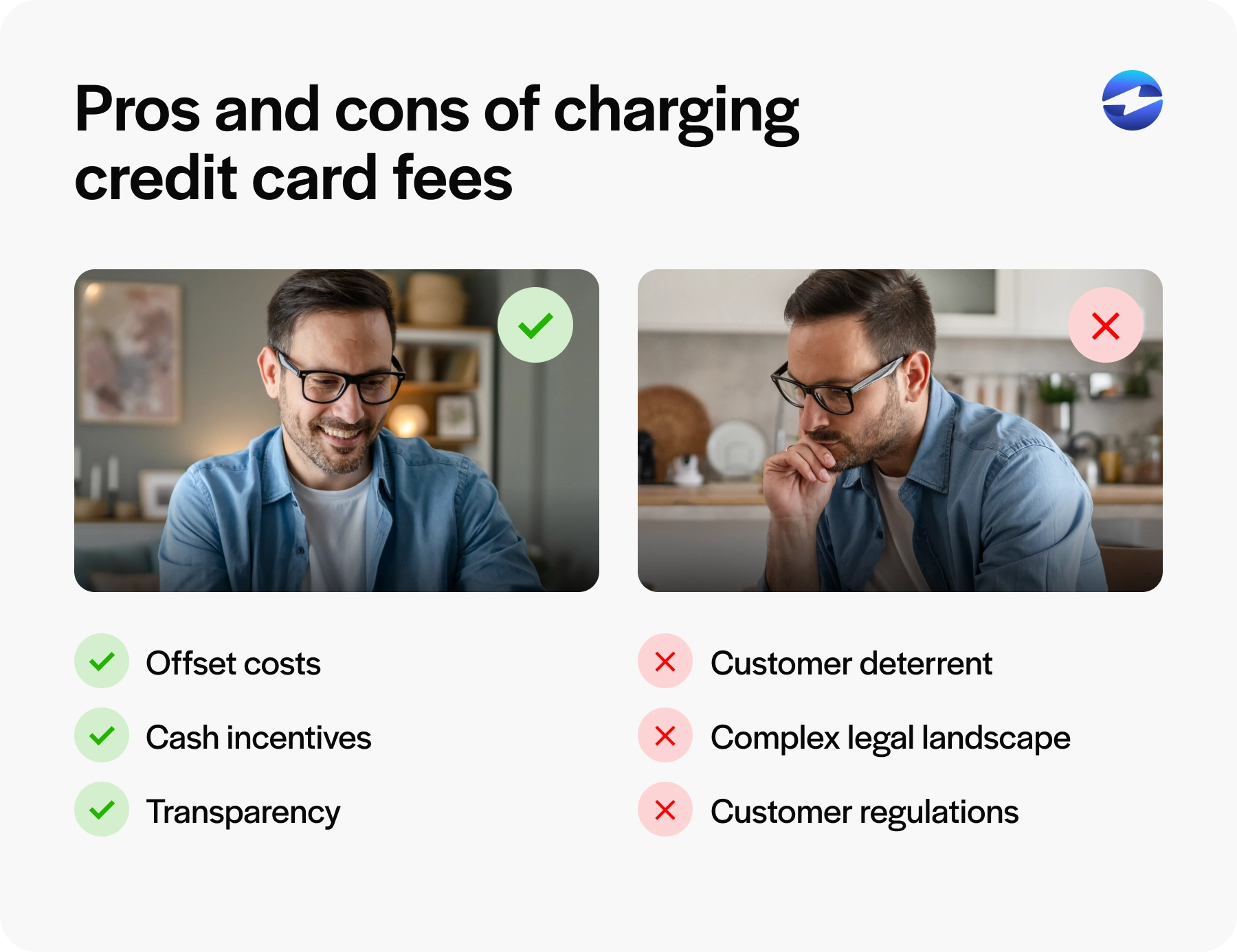

Pros and cons of passing credit card fees to customers

Passing credit card fees to customers has its share of pros and cons for both merchants and customers. Therefore, you should review each method to determine if it’s beneficial for your business.

Pros

Cost savings is the most obvious advantage for merchants that pass credit card fees to customers, as it’s the main objective behind these methods. When merchants opt for zero processing fees by passing along processing costs, they can offset, reduce, and avoid these fees altogether.

More specifically, surcharging benefits merchants by allowing them to automatically pass charges to customers paying with credit cards for a more streamlined approach, and also give customers the option to pay with cash or debit cards instead.

Cash discounting can benefit both merchants and customers since it incentivizes customers to pay with cash to receive a discounted rate while simultaneously allowing merchants to avoid processing fees.

Other processing costs reduction methods like minimum purchase requirements, cash discounting, and convenience fees may allow for more flexibility for some merchants.

Cons

Passing credit card fees to customers also comes with its share of disadvantages that can be damaging for some businesses.

Passing credit card fees to customers can be great for merchants but puts the financial burden onto your customers which may result in fewer sales, fewer return purchases, and a weakened brand image.

Implementing surcharging or convenience fees means staying up to date on evolving state laws, card network regulations, etc. Failing to do so may result in your business going against guidelines or conducting illegal business practices.

Strategies for minimizing credit card fees

Passing fees to customers is one approach to managing processing costs, but it is not the only option. Before implementing surcharging or convenience fees, it is worth considering whether there are ways to reduce the fees your business pays in the first place. Three strategies worth evaluating:

Offer cash transaction discounts. Rather than adding a fee for card use, incentivize customers to pay with cash by offering a small discount. This reduces the volume of credit card transactions and the associated fees without penalizing card users. Customers tend to respond more positively to discounts than to surcharges, making this a smoother approach for businesses where customer experience is a priority.

Choose a provider with transparent pricing. Many businesses overpay on processing fees simply because their pricing model is not well suited to their transaction profile. Look for a processor that clearly outlines interchange fees, transaction fees, monthly fees, and any other potential costs. Flat-rate, interchange-plus, and subscription-based models each work better in different situations. If a provider cannot give you a clear, itemized breakdown of every charge, that is a red flag.

Minimize fraud risk. Fraudulent transactions lead to chargebacks, which carry their own fees and penalties on top of the lost revenue. Reducing fraud exposure directly reduces these costs. Key measures include encryption and tokenization, adherence to PCI DSS standards, enabling address verification service (AVS), and requiring CVV verification on card-not-present transactions.

With these reduction strategies in mind, the next step is understanding what questions to ask before deciding which approach is right for your business.

Before you implement: four questions to ask

Deciding whether to charge credit card fees is not just a compliance question. It’s a business decision that affects your customers, your pricing, and your competitive position.

- Will it drive away customers? If your competitors aren’t charging fees and you start, some customers will notice, and some will leave. Understanding your customer base and what they’ll tolerate matters before you flip the switch.

- How will you communicate the change? Card networks require disclosure before the transaction, and some states mandate specific signage. Merchants also need to notify their card association, acquirer, and processor at least 30 days in advance before implementing surcharges or convenience fees. Planning the communication ahead of time avoids compliance gaps and customer complaints.

- Can you incentivize cash instead? Rather than penalizing card users, a cash discount program rewards customers who pay with cash or check. For merchants in states where surcharging is restricted, or for businesses where customer relationships are particularly sensitive to fee changes, this is often a smoother approach.

- Is the real problem your processor? If processing fees are high enough that surcharging feels necessary, it may be worth reviewing your current rates first. Negotiating lower rates or switching to a processor with more transparent pricing sometimes solves the problem without adding fees to customer transactions at all.

Best practices for charging credit card fees

Knowing the rules around credit card fees is one thing; implementing them in a way that protects your business and maintains customer trust is another. Three practices that separate compliant, customer-friendly fee programs from ones that create friction:

Transparent disclosure. Any credit card fee must be clearly disclosed before the transaction is completed. This means stating the fee explicitly at the point of entry, at the point of sale, and on receipts. Transparency is not just a compliance requirement; it builds customer trust and reduces disputes. Customers who understand the fee before they pay are far less likely to contest it afterward. Customers who see that their credit cards have been charged a “cc fees” line item after the payment may feel upset and create problems.

Consistency across transactions. The same fee should apply to the same type of transaction regardless of the customer, the card brand (where card network rules permit), or the purchase amount. Inconsistent fee application creates confusion, perceived unfairness, and compliance risk. A standardized approach also simplifies accounting and reduces the chance of errors in your processing records.

Adherence to card network guidelines. Visa, Mastercard, American Express, and Discover each have specific rules governing how fees can be applied, disclosed, and capped. Staying current with these guidelines protects your ability to accept those cards. Merchants who fall out of compliance risk fines, card acceptance restrictions, or termination of their merchant account. When in doubt, confirm requirements directly with your processor before making any changes.

Following these best practices will help ensure your fee program runs smoothly and holds up if your practices are ever reviewed or questioned. If you need to notify customers of an upcoming fee change, the template below provides a straightforward starting point.

Tips for properly passing credit card fees to customers

Merchants that want to effectively pass credit card fees while also avoiding turmoil from their customers can look to these three tips:

- Be upfront and transparent with customers about extra charges

- Follow state legislation and card issuer policies

- Offer additional payment methods besides credit cards to help customers avoid fees

If you are adding a surcharge or updating your fee policy, notifying customers in advance protects the relationship and keeps you compliant with disclosure requirements.

Sample letter to customers about credit card fees

Here is a straightforward template to adapt:

Adjust the fee percentage, effective date, and payment alternatives to match your setup. If you are using a cash discount model rather than a surcharge, the framing shifts: you are not adding a fee, you are offering a discount for non-card payments, which is worth making explicit in the letter.

If done right, merchants can successfully pass off credit card fees, conduct legal business operations, and maintain good rapport with customers.

EBizCharge helps merchants reduce credit card fees and optimize this process

Lastly, merchants can look to an all-in-one payment processor like EBizCharge to significantly reduce credit card processing fees by offering zero hidden fees, no setup costs, no cancellation charges, and more.

In addition to a seamless payment experience, EBizCharge allows merchants to surcharge customers to further minimize processing fees and save more money.

Merchants can maximize these savings by connecting their payment solution directly to the software they already use. With credit card processing for QuickBooks, surcharges and fees are automatically calculated and recorded in your accounting software. Manufacturers and distributors can do the same with Epicor payment processing or Acumatica payment processing, both of which sync every transaction to your ERP so you can track exactly how much you’re saving by passing fees to customers. When your payments and accounting are connected, managing surcharges and compliance becomes much simpler.

Frequently Asked Questions

Can stores charge a minimum for debit cards?

No, businesses are generally not permitted to set a minimum purchase amount for consumers paying with a debit card.

Can you pass credit card fees to consumers

Yes. Businesses can pass credit card fees to customers through surcharging, cash discounting, convenience fees, or minimum purchase requirements. Each method has its own rules around disclosure, state legality, and which card types it applies to. The right choice depends on your state, your customer base, and how your processor is configured.

What is standard credit card processing fee wording?

Convenience fee wording should state the fee amount, when it applies, and how customers can avoid it. A common example: “A [X]% convenience fee applies to credit card payments. Pay by check or ACH to avoid this fee.” Adjust the amount and payment alternatives to match your setup. See the convenience fee wording section above for additional templates.

What does standard credit card convenience fee wording look like?

The standard credit card convenience fee wording typically includes a clear and concise explanation of the additional fee charged for the convenience of using a credit card for payment. A standard wording could be:

“A credit card convenience fee of [percentage or flat amount] will be applied to all transactions. This fee is charged to cover the processing costs associated with credit card payments. Please note that this fee does not apply to other payment forms such as cash or debit cards.”

It will vary by merchant.

Is it legal to charge customers a credit card fee?

In most states, yes. Surcharging is legal in the majority of U.S. states but prohibited in a few, including Connecticut and Massachusetts. Cash discounting is legal in all 50 states. Convenience fees are generally permitted as long as they follow card network guidelines. Working with a processor that manages compliance on your behalf removes most of the operational burden.