Blog > What are Convenience Fees? The Pros and Cons for Merchants

What are Convenience Fees? The Pros and Cons for Merchants

Is charging a credit card convenience fee the right choice for your business?

If your business wants to offer customers new avenues of credit card payment—like paying over the phone or online—you’ll have to decide if you also want to charge a convenience fee. However, there are a few things you should consider before making this important choice.

What is a credit card convenience fee?

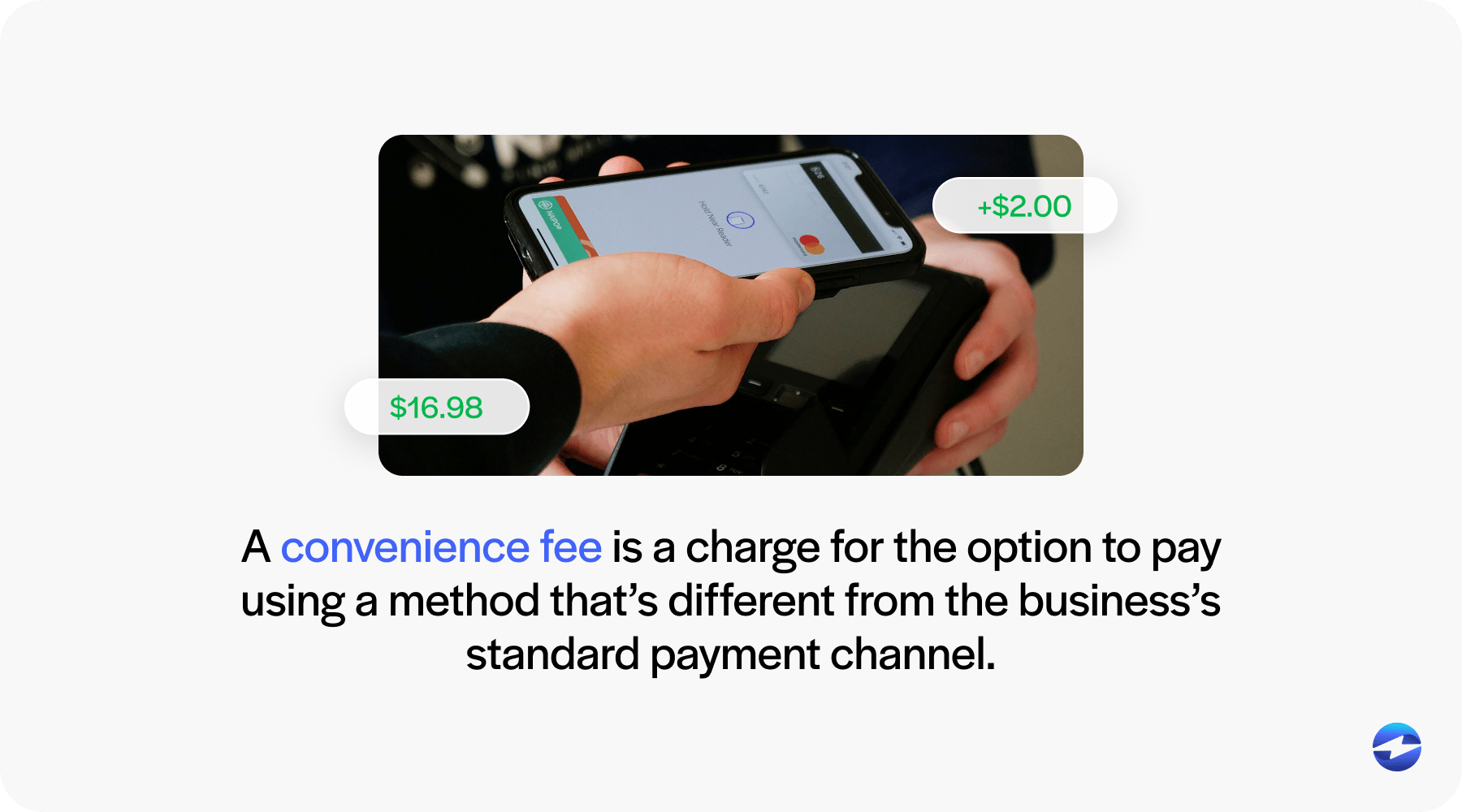

A convenience fee is an additional cost tacked on to credit card payments made using a non-standard method. The credit card convenience fee is a charge imposed by a business or merchant on a customer for the convenience of using a credit card for payment. Convenience fees help merchants account for the varying costs of accepting credit cards. This fee covers the cost of processing the credit card payment and is typically a percentage of the transaction amount, ranging from 1% to 3%. The cost of processing a credit card depends on many factors, but one of the most important is risk level. If a transaction is considered riskier, it will cost more to process.

Sometimes, a convenience charge may be worth paying if the benefits of using a credit card outweigh the additional cost. This can include earning rewards points, enjoying purchase protections, or having access to a line of credit. Convenience fees must be disclosed to customers before the transaction and apply to all alternative payment types equally. These fees are typically a percentage of the transaction amount or a flat fee. The disclosure process ensures that customers are fully informed about the convenience fees and can weigh the pros and cons before using a non-standard payment method.

What is a Non-standard payment method?

Merchants may charge convenience fees when they want to recover the costs of processing credit card transactions. These fees may be applied for non-standard transactions such as online or over-the-phone purchases. Non-standard payment channels can be identified and addressed by referring to Visa, Discover, MasterCard, and American Express guidelines. Each card brand has specific criteria for when convenience fees are permissible. Visa, for example, allows convenience fees for payments made through non-standard channels such as telephone payments, while MasterCard permits convenience fees for government and education payments. American Express and Discover also have their own guidelines for when convenience fees are acceptable.

Understanding each card brand’s specific guidelines can help consumers and merchants navigate non-standard payment channels and the associated fees.

Why Do Businesses Charge Convenience Fees?

The short answer is cost recovery. When a customer pays through a non-standard channel like a website or over the phone, the transaction typically costs more to process than an in-person card swipe. There’s a higher risk of fraud, different processing infrastructure, and sometimes third-party platforms involved. The convenience fee shifts some of that cost to the customer choosing that payment method rather than the merchant absorbing it across the board.

It’s also worth understanding what a convenience fee is not. It isn’t a penalty for paying by card. It’s specifically tied to the channel used, not the payment type. A customer paying in person with the same credit card would not be charged the fee, because the merchant’s costs for that transaction are lower.

Convenience fee examples

Encountering a convenience fee has become a common experience during online transactions, notably in sectors like restaurants and movie theaters. These fees are often attached to the convenience of digital transactions, adding an extra layer of cost to services for the sake of ease.

What is a convenience fee at a Restaurant?

A restaurant convenience fee is typically applied when customers pay with a credit card for transactions not traditionally associated with credit card payments. For example, some restaurants may apply a convenience fee for large party reservations or catering orders paid with a credit card. Convenience fees may also cover merchant fees associated with peer-to-peer payment platforms like Venmo or PayPal. These fees help offset restaurants’ costs when processing nontraditional forms of payment.

It’s important to note that convenience fees are not applied to standard dine-in or takeout orders paid with a credit card. Instead, they are typically reserved for larger or non-standard transactions. This helps businesses cover the additional costs associated with processing these types of payments while still providing customers the convenience of using their preferred payment method.

One thing worth noting: restaurants in some states have started adding what they call a “non-tipper fee” or automatic service charge to online orders. These are separate from convenience fees and structured differently, though customers often encounter them in the same checkout flow. Colorado has seen legislation and public attention around these charges in particular. If you’re a restaurant operator, understanding which type of fee you’re applying matters for compliance.

Overall, convenience fees at restaurants are designed to help businesses cover the costs of credit card processing for nontraditional transactions, ensuring that they can continue offering various payment options to their customers. Another common business that uses convenience fees is movie theaters.

Do you have to pay a convenience fee at the movie theater?

The example most people are familiar with is movie tickets. When you go to a movie theater, you pay for your tickets in person at the box office. That’s the standard payment method most customers use. However, many theaters now offer the option to pay for tickets online. Because this is considered a non-standard payment method, theaters often charge a convenience fee.

The theater pays less to process a credit card accepted at the box office because that’s an in-person transaction, which is considered less risky. However, the theater will pay more to process credit cards used to purchase tickets online because there’s a greater potential for fraud. The convenience fee helps offset the extra cost caused by the increased risk of the alternative payment method. In part, customers pay this fee for the privilege of paying in an alternative, more convenient way. Convenience fees are not to be mistaken for surcharges.

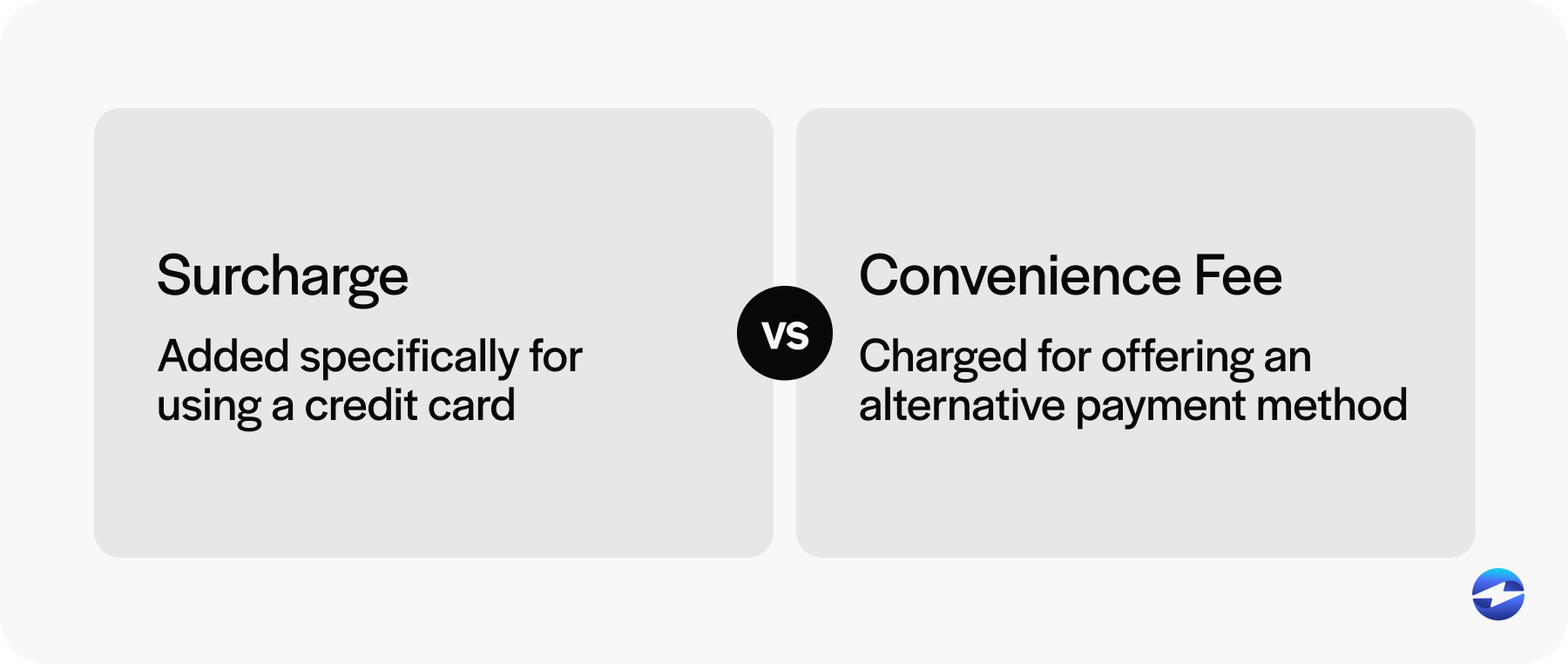

Credit card convenience fee vs. surcharge

Convenience fees can be confused with surcharges. But they’re very different fees with very different sets of rules.

A convenience fee only applies to alternative payment methods, like in the movie theater example. A surcharge, on the other hand, is a fee applied to every single credit card transaction, regardless of method. The purpose of a convenience fee is to compensate the merchant for the added trouble and cost of accepting payment through a non-standard method, while the purpose of a surcharge is to offset at least some of the costs of processing credit card payments in general.

Convenience fees are legal in all states, but a surcharge is not. Before adopting an added fee for credit cards, make sure you know the difference between the two and which one your business is charging. And of course, if you choose to surcharge on transactions, make sure it’s legal in your state.

For more information, watch this podcast episode where we compare convenience fees vs. surcharges:

Pros of convenience fees:

Choosing to implement a convenience fee can enable merchants to add new, more convenient ways for their customers to pay. For example, they could add the option to pay over the phone or online. The more convenient it is to purchase, the more likely it is that a customer will pay, which could increase sales volume and boost a merchant’s bottom line.

These days, most customers expect easy payment options. We’re used to online payments, mobile payments, even contactless payments. So if a convenience fee gives your business the ability to offer these more streamlined payment experiences, they can add legitimacy to your business and satisfy customer expectations.

If you’re looking for a convenient way to add a credit card convenience fee to your transactions, use automated software like EBizCharge to seamlessly include a convenience fee with each payment. Pairing convenience fees with a payment solution that connects to your accounting software can make the process even smoother. With QuickBooks payment processing, small businesses can automatically apply and track convenience fees while keeping their books accurate. For mid-market finance teams, a Sage Intacct credit card processing integration offers the same level of automation within a more robust ERP environment. Both options help merchants recover processing costs without adding manual work to their workflow.

Cons of convenience fees:

Unfortunately, there are some downsides to implementing convenience fees.

Merchants who use convenience fees have to abide by strict regulations imposed by the card brands and associations. For example, merchants must disclose the convenience fee to the customer at the point of sale. If merchants don’t give ample notice, customers can lodge complaints with credit card networks, which could have serious consequences for your business. If you choose to use a convenience fee, do your research with each card brand to ensure you’re following all necessary rules and regulations.

Convenience fees may also be a deterrent for customers who bridle at the idea of paying more just for added convenience. Not all customers are willing to pay more for a smoother experience. In fact, they may choose to take their business elsewhere. When thinking about adopting convenience fees, take a look at your competition. Are they also charging convenience fees? If not, then it may be more difficult for your business to start suddenly charging more for certain credit card transactions. Make sure to study the current landscape and determine if convenience fees could hurt your competitive edge.

How to avoid paying a convenience fee

Convenience fees for online or phone payments can easily be avoided by utilizing alternative payment methods. One option is to use cash, check, or an ACH transfer. These methods typically do not incur convenience fees, making them a cost-effective alternative. Another option is to make payments by mail if a business charges a convenience fee for online or phone payments. This traditional method allows you to bypass any additional fees associated with electronic or phone transactions.

It’s wise to ask businesses about convenience fees before making a purchase. By being informed upfront, you can decide if you want to proceed with the transaction. Also, consider using ATMs that belong to your bank to avoid additional fees. Using out-of-network ATMs often leads to surcharges, so it’s best to utilize ATMs associated with your bank to avoid these extra costs.

By being mindful of alternative payment methods and staying informed about convenience fees, you can avoid unnecessary charges and keep more money in your pocket.

Conclusion

If your business is considering a convenience fee, there are a number of pros and cons to weigh and important questions to answer before choosing to implement them. Convenience fees may not be right for every business. If you believe extra fees could deter business or upset customers, or if you don’t want to deal with all the regulation, then maybe it’s not the best option. But if adding a credit card convenience fee enables your business to offer additional, more convenient payment methods for your customers, it could be a win-win for customers willing to pay more for easier payment options.

If you’d rather offset processing costs without the complexity of convenience fees, EBizCharge’s credit card surcharge program handles the compliance and calculation automatically so you’re not managing it manually.

Frequently Asked Questions

Why are convenience fees legal?

Convenience fees are legal because they’re tied to a specific, optional payment channel rather than the payment type itself. Card networks including Visa and Mastercard permit them when structured correctly: flat fee, non-standard channel, disclosed before the transaction. Most states don’t restrict them the way some restrict credit card surcharges, which apply broadly to all credit card transactions regardless of channel.

Why do movie theaters charge a convenience fee?

Movie theaters charge a convenience fee for online ticket purchases because their standard payment method is in-person at the box office. Online transactions cost more to process due to higher fraud risk and platform infrastructure. The fee covers that added cost. You generally won’t see it if you buy tickets at the window on the day of the show.

What is the difference between a convenience fee and a surcharge?

A convenience fee is a flat charge for using a non-standard payment channel. A surcharge is a percentage-based fee applied to credit card transactions broadly. Convenience fees are legal in all U.S. states. Surcharges are banned in some states. Surcharges cannot be applied to debit cards. Convenience fees can apply to debit transactions when the channel qualifies.