Blog > B2B Merchant Services: What Growing Companies Need to Know

B2B Merchant Services: What Growing Companies Need to Know

As a business grows, payments become more complicated. At first, a basic payment processor might seem good enough. You can accept credit cards, send invoices, and collect payments online without much trouble. But once your company starts handling larger transactions, extending payment terms, or managing hundreds of invoices every month, the cracks begin to show.

That’s especially true for B2B companies. Business-to-business payments work differently than retail or ecommerce payments. The timelines are longer, the transaction sizes are larger, and customers expect more flexibility. Accounting teams also need accurate reconciliation, while processing costs can quietly eat away at margins if systems aren’t built correctly.

Many companies discover this after outgrowing a generic payment processor that was never designed for B2B operations in the first place. If your business sells to other businesses, choosing the right B2B merchant services setup can make a major difference in cash flow, efficiency, and long-term scalability.

What Are B2B Merchant Services?

B2B merchant services refer to the payment tools and infrastructure businesses use to accept and manage payments from other businesses. That includes far more than simply processing a credit card transaction.

A modern payment processing solution may include credit card processing, ACH and eCheck payments, invoice payment portals, virtual terminals, automated reminders, ERP integration, and accounts receivable automation tools. These systems are designed to support the realities of B2B payments rather than the instant checkout experiences common in retail.

The biggest difference between B2B and consumer payments comes down to workflow. In retail, customers usually pay immediately at checkout. In B2B, payments often happen days or weeks later after invoices are issued. Many businesses operate on Net 30, Net 60, or Net 90 terms, while customers may pay using ACH, purchasing cards, or corporate credit cards.

For finance teams, the goal isn’t only to collect payments. It’s also to streamline reconciliation, reduce merchant services fees, and improve cash flow without adding more administrative work.

Why Generic Payment Processors Fall Short

Most payment processors are designed with consumer transactions in mind. Their systems are optimized for online stores, restaurants, retail counters, and subscription checkouts where speed and simplicity matter most. B2B businesses operate differently, and that difference becomes more obvious as transaction volume increases.

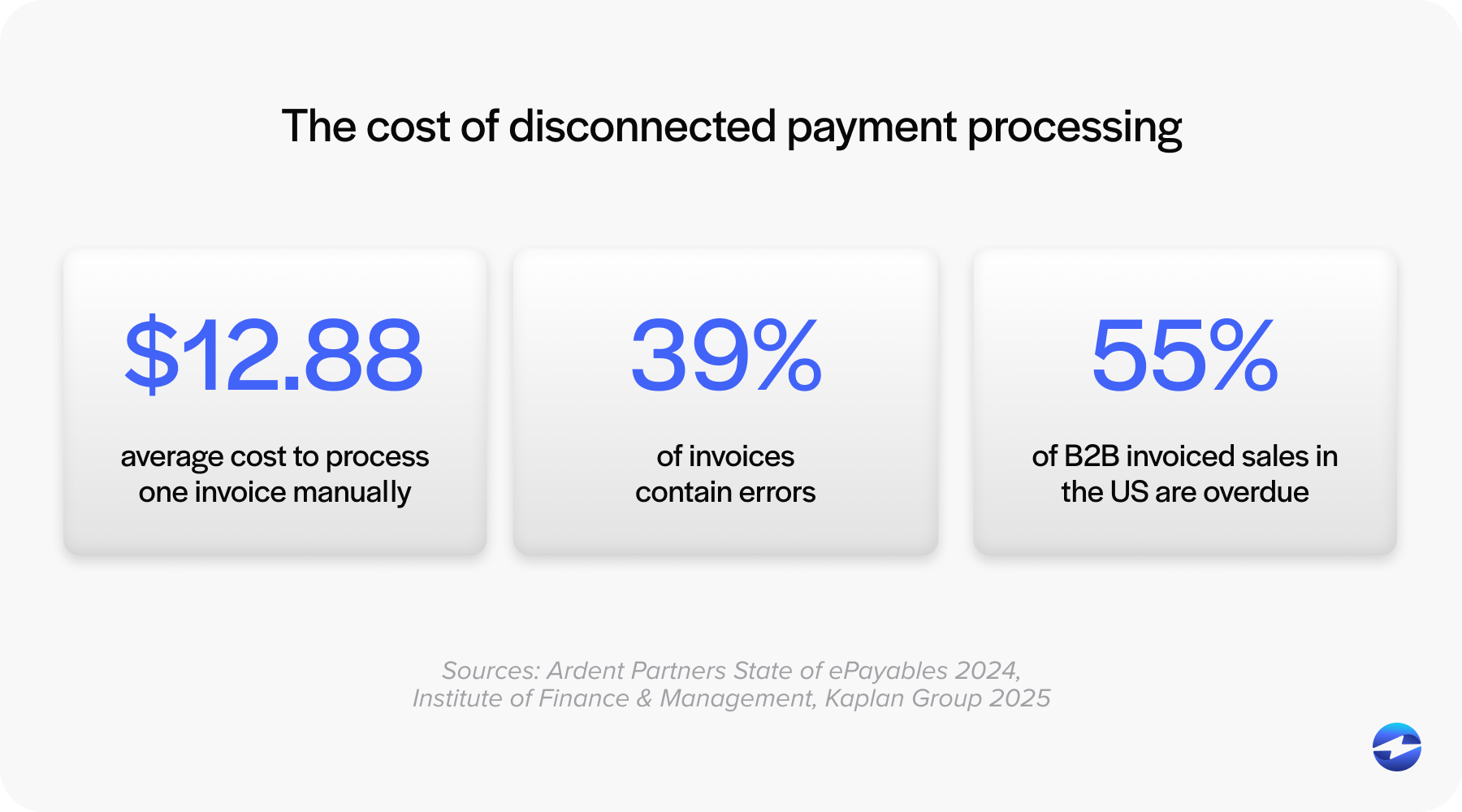

For example, many generic merchant services platforms struggle with invoice-based payments because they assume the customer pays immediately rather than after receiving an invoice. Once accounting teams begin manually tracking payments across dozens or hundreds of open invoices, inefficiencies start piling up.

Weak ERP integration is another common issue. Without proper ERP integration, accounting teams often reconcile payments manually by matching invoices, updating records, and correcting errors by hand. That creates delays, increases the risk of mistakes, and consumes valuable time that could be spent on higher-level financial work.

The same problem applies to merchant services credit card processing fees. Many B2B businesses process large payments using commercial cards or purchasing cards. If your payment processor doesn’t support Level 2 and Level 3 processing, you could be paying unnecessarily high interchange rates on those transactions. Over time, those higher merchant services fees can significantly affect margins.

ACH support is another area where generic systems often fall behind. In B2B environments, ACH is commonly preferred for large invoice payments because it’s more cost-effective than credit cards. However, many consumer-focused platforms treat ACH as secondary instead of making it a core part of the payment workflow.

What works for a smaller company may no longer work once transaction volume increases and financial processes become more demanding. That’s why many growing businesses eventually start looking for a more specialized payment solution.

What to Look For in a Merchant Services Provider

Not all merchant services providers are built for B2B companies. The right platform should simplify operations rather than create more administrative work. It should also support the way your customers actually pay.

Strong ERP Integration

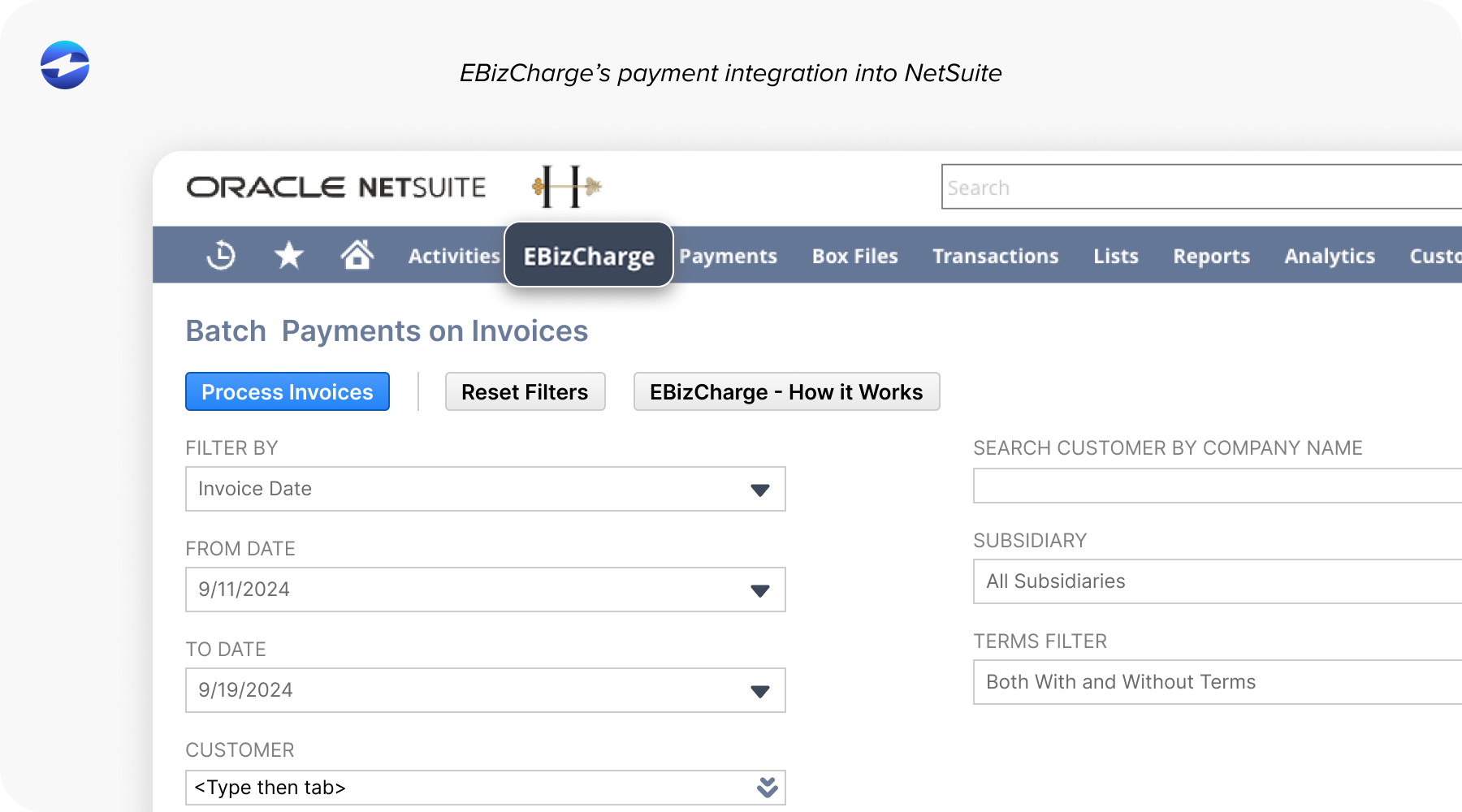

For B2B businesses, ERP integration should be one of the highest priorities when evaluating a merchant services provider. Payments connect directly to invoices, customer records, accounting workflows, and reporting. When systems are disconnected, teams waste time entering data manually and fixing avoidable errors.

A strong ERP integration automatically allows payment information to sync with your accounting or ERP system in real time. Invoices update automatically, payments reconcile faster, customer records stay accurate, and accounting teams spend less time on manual entry.

For businesses already working inside systems like NetSuite, Sage, QuickBooks, Microsoft Dynamics, SAP, or Acumatica, integrated payments remove a significant amount of operational friction. This is where many companies begin to recognize the difference between a standard payment processor and a specialized B2B merchant services provider.

Support for Net Terms and Invoice Payments

B2B customers expect flexibility. Unlike consumers, business buyers rarely pay everything upfront. Payment terms are a standard part of B2B operations, especially in industries like manufacturing, distribution, construction, and professional services.

A proper payment processing solution should support Net 30 and Net 60 terms, invoice-based payments, partial payments, customer self-service portals, and automated payment reminders. These tools help businesses collect payments faster without creating additional work for accounting teams.

The customer experience also improves when invoice payments are simple and convenient. If customers struggle to pay invoices online or navigate outdated payment systems, delays become more common. Businesses that modernize the payment experience often see improvements in both payment speed and customer satisfaction.

Built-In ACH Capabilities

Automated Clearing House (ACH) plays a major role in B2B payments because it helps reduce processing costs on large transactions. For many companies, ACH can significantly lower merchant services credit card processing fees compared to traditional card payments.

However, ACH only works well when it’s fully integrated into the payment workflow. The best merchant services provider should allow customers to easily pay invoices through ACH while automatically syncing those payments back into the accounting system.

Modern ACH functionality should include secure bank account processing, recurring ACH payments, same-day ACH options, automated reconciliation, and customer authorization management. For businesses handling high-dollar invoices, ACH often becomes one of the most valuable parts of a complete payment solution.

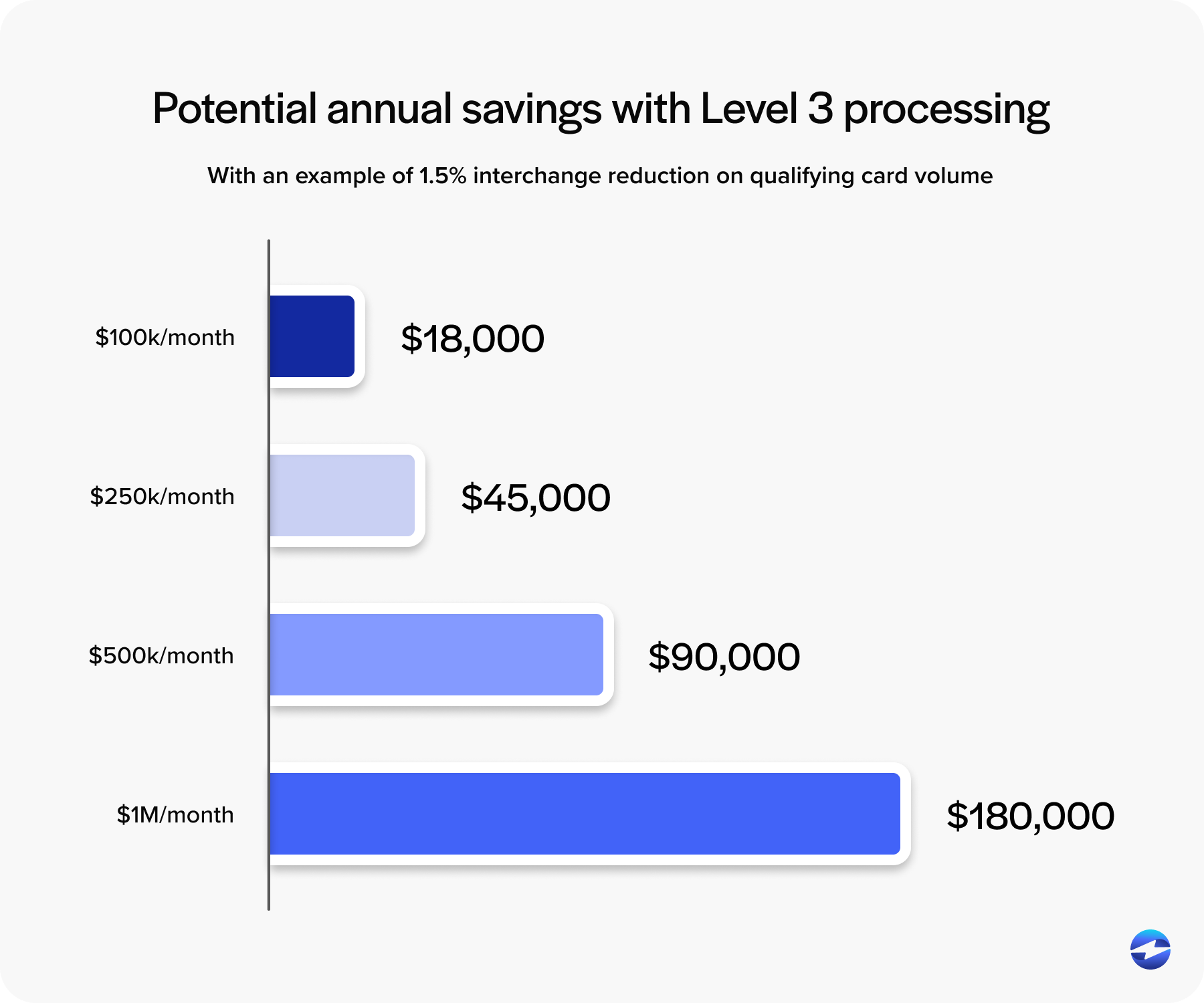

Level 2 and Level 3 Processing

One of the most overlooked aspects of B2B merchant services is Level 2 and Level 3 processing. Many business customers pay using commercial cards, purchasing cards, or corporate cards. These transactions can qualify for lower interchange rates if additional transaction data is submitted during processing.

That extra information may include invoice numbers, tax amounts, customer codes, line-item details, and shipping information. Without Level 2 and Level 3 support, businesses often pay higher merchant services fees than necessary.

A specialized merchant services provider can automate much of this process through ERP integration, helping businesses qualify for lower interchange rates without adding more administrative work. Over time, those savings can become substantial.

Security and Reliability

Any payment solution should support PCI compliance, encryption, and tokenization to protect sensitive payment data. Reliability matters just as much because payment failures or broken reconciliation workflows can affect both customer experience and internal operations.

For finance teams already managing heavy workloads, stable and reliable systems become extremely important. That’s why many growing companies move away from disconnected payment tools and toward more unified B2B merchant services platforms.

Why Specialized B2B Providers Make a Difference

B2B payments aren’t simply larger versions of consumer payments. They involve entirely different workflows, customer expectations, and operational requirements. A specialized B2B merchant services provider understands those differences and builds systems around them.

Instead of forcing businesses to adapt to a retail-focused platform, specialized providers design their tools around invoicing, accounts receivable workflows, ERP systems, and commercial payment methods. That often leads to faster payment collection, lower processing costs, less manual reconciliation, and better visibility into accounts receivable performance.

For finance leaders, controllers, AR teams, and operations managers trying to scale efficiently, those improvements can make a meaningful difference over time.

How EBizCharge Supports B2B Companies

EBizCharge’s payment solution was built specifically for B2B payments and accounts receivable workflows. Instead of functioning as a generic payment processor, the platform focuses on helping businesses streamline invoice payments, automate reconciliation, and reduce payment friction across accounting operations.

One of the biggest advantages is its deep ERP integration capabilities. EBizCharge integrates directly with leading ERP and accounting systems, allowing businesses to manage payments inside the platforms they already use every day. Payments sync automatically with invoices and customer records, which helps reduce manual work and improve accuracy.

The platform also supports both credit card and ACH payments within a single payment processing solution. For businesses managing large B2B transactions, EBizCharge supports Level 2 and Level 3 processing to help reduce merchant services credit card processing fees where possible.

Customers can pay invoices online, manage outstanding balances, and use payment methods that fit their purchasing process. Meanwhile, accounting teams gain better visibility and more streamlined reconciliation workflows behind the scenes.

Final Thoughts

Choosing a merchant services provider isn’t only about accepting payments. For B2B companies, it’s about building a payment infrastructure that supports long-term growth, operational efficiency, and healthy cash flow.

Generic systems may work temporarily, but many growing businesses eventually run into limitations around ERP integration, ACH processing, reconciliation, and rising merchant services fees. That’s why specialized B2B merchant services matter.

The right payment solution should fit naturally into your financial workflows, support the way your customers actually pay, and help your team spend less time managing payments manually. For businesses preparing to scale, investing in the right merchant services setup early can prevent major operational headaches later on.