Blog > PCI Compliance: Safeguarding Cardholder Data in the Digital Age

PCI Compliance: Safeguarding Cardholder Data in the Digital Age

In the modern era of digital transactions, ensuring cardholder data security has become a paramount concern for businesses and consumers alike. As the frequency and sophistication of cyber threats continue to rise, organizations must adopt stringent measures to protect sensitive cardholder data.

By understanding the significance of cardholder data and its relationship to PCI compliance, businesses can establish robust security frameworks, mitigate risks, and build customer trust.

This article will explore the crucial role of cardholder data in PCI compliance and answer frequently asked questions like what is primary account number (PAN) data, what is the cardholder name, and what is cardholder data?

What is cardholder data?

Cardholder data (CHD) refers to the data associated with credit and debit cards, consisting of information required to access funds on the payment cards such as the cardholder name, primary account number, expiration date, and service codes. Without this data, users can’t access funds on their cards.

Like stealing the key to a locked safe, cybercriminals often try to acquire cardholder data to make fraudulent purchases, create counterfeit cards, and engage in identity theft. This is why organizations must implement robust security measures to safeguard cardholder data.

The role of cardholder data in PCI compliance

Cardholder data and PCI compliance have a very close relationship, as PCI DSS guidelines are used to protect cardholder data. Without PCI compliance, cardholder data is susceptible to data breaches.

What is PCI compliance?

Payment Card Industry (PCI) compliance refers to a comprehensive framework of security requirements and best practices businesses must follow to safeguard cardholder data, maintain secure payment environments, and reduce the risk of data breaches and fraud.

Merchants accepting payments from their customers should know what PCI compliance entails and the requirements it enforces to ensure they meet these standards.

What is PCI DSS?

Payment Card Industry Data Security Standard (PCI DSS) is the set of security standards established by the Payment Card Industry Security Standards Council (PCI SSC) to protect cardholder data and ensure secure payment card transactions.

PCI standards consist of a list of 12 high-level requirements covering various security aspects:

- Install and maintain a secure network

- Protect cardholder information

- Maintain a vulnerability management program

- Implement strong access control measures

- Regularly monitor and test networks

- Maintain an information security policy

- Restrict access to cardholder data

- Assign a unique ID to each person with computer access

- Restrict physical access to cardholder data

- Track and monitor all access to network resources and cardholder data

- Regularly test security systems and processes

- Maintain a policy that addresses information security for employees and contractors

Now that you know the requirements of PCI compliance, you should also familiarize yourself with the terms and codes associated with cardholder data.

8 terms and codes associated with cardholder data

Cardholder data includes numerous terms and codes that are important for businesses to understand since they typically relate to security measures that protect sensitive authentication data.

Here are 8 of the most commonly used terms associated with cardholder data:

- Cardholder: A cardholder is an individual or entity that a financial institution issues a credit, debit, or prepaid card for to make purchases and withdrawals. This individual is the card’s authorized user and is responsible for making purchases, conducting transactions, and managing the associated account. The cardholder’s name is printed on the card to help identify the authorized user.

- Primary account number (PAN): This number is a unique identifier assigned to each payment card and can be found on the front of the card. This series of numbers is meant to identify the cardholder and the financial institution that issued the card.

- Personal identification number (PIN): This numeric code is another unique identifier primary account holders use to verify their identity to access specific systems, devices, or accounts. The PIN is a confidential and unique combination of numbers, usually four to six digits in length, chosen by the cardholder or assigned by the card issuer. When making a transaction or accessing a system, the cardholder enters the PIN into a keypad or terminal to verify their identity and authorize the action.

- Service codes: These codes go by many names, including card validation code (CVC), card authentication value (CAV), card validation code (PAN CVC), card verification value (CVV), and card security code (CSC). Service codes are three- to four-digit codes following the card’s expiration date that typically indicate the types of services and transactions that can be performed with the card.

- Cardholder data environment (CDE): The cardholder data environment is responsible for storing, processing, and transmitting cardholder data. This network includes databases, servers, applications, and network devices for handling CHD and carries stringent security measures to protect sensitive information from unauthorized access.

- Self-assessment questionnaire (SAQ): The SAQ allows merchants to assess their PCI compliance by asking questions about their operations, policies, and security controls concerning cardholder data. Organizations can then determine their level of PCI compliance and adjust areas that don’t meet these standards.

- Truncation: Truncation shortens or removes sensitive cardholder information during transactions to enhance security by only storing or displaying a portion of this data and hiding the whole card number or the expiration date.

- Qualified security assessor (QSA): A QSA is an individual authorized to assess the PCI compliance of businesses. QSAs perform on-site audits, review documentation, and conduct interviews with relevant personnel to determine the effectiveness of security controls and identify any vulnerabilities or non-compliance issues.

Since cardholder data includes various terminology, it’s essential to clear up any confusion and understand the roles and codes associated with this data.

Common misconceptions about cardholder data

As cyber threats continue to evolve, cybersecurity must adapt to changing environments, and users rely on reliable sources to stay updated on new standards and avoid any misconceptions about cardholder data.

To help your business make more informed decisions to protect customers’ cardholder data, there are three common misconceptions to be aware of:

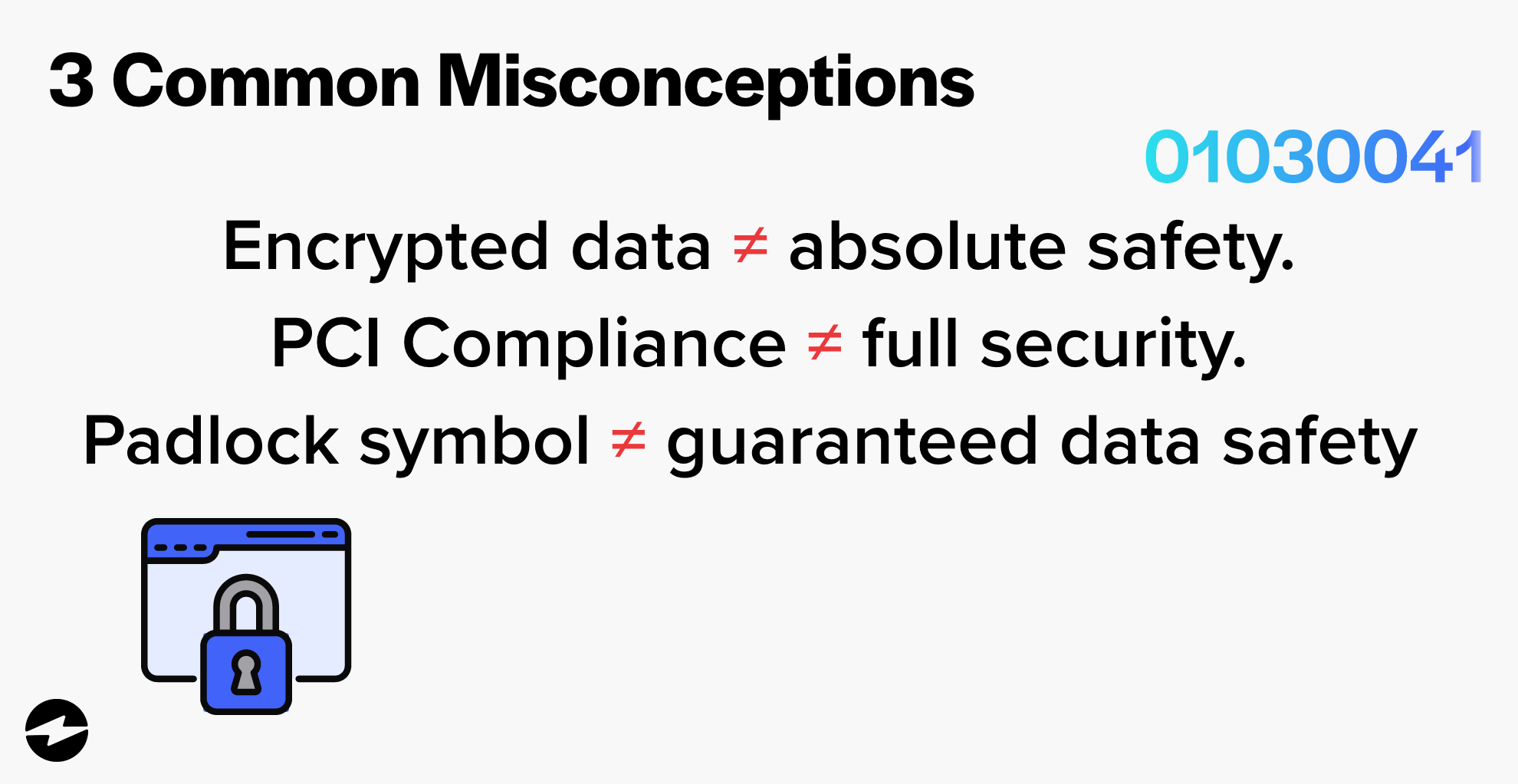

- Storing cardholder data is safe as long as it’s encrypted. Although encryption is an essential security measure, it’s not bulletproof. With threats constantly advancing, even encrypted data runs the risk of being breached. Implementing a data minimization approach when storing sensitive cardholder information to retain only necessary information can help.

- PCI compliance guarantees cardholder data is fully secure. When it comes to cardholder data, PCI compliance is an absolute necessity. That said, it doesn’t ensure complete protection. PCI compliance is essentially the baseline of security measures — additional security is recommended to prevent data breaches.

- Cardholder data is not at risk if a website has a padlock symbol. A padlock symbol means a secure sockets layer (SSL) and transport layer security (TLS) encrypt the connection and provide secure data transmission. However, this doesn’t guarantee total website security or the protection of cardholder data on the server. Although SSL and TLS are essential, websites should add other security measures and remain PCI-compliant for comprehensive data protection.

Clearing up misconceptions about cardholder data is only one step. Merchants can also implement other measures and protocols to enhance their payment security.

10 ways to protect cardholder data

Although PCI standards carry their own guidelines and regulations, there are also steps you can take as a business to keep your cardholder data safe and secure.

Ten ways your company can protect its customers’ payment information include:

- PCI DSS Compliance

- Encryption

- Tokenization

- Use a secure network

- Limit access to sensitive data

- Keep up with software updates

- Provide employee training

- Minimize data storage

- Use a secure payment gateway

- Conduct regular security audits

PCI DSS compliance

One of the best ways to protect cardholder data is to comply with Payment Card Industry Data Security Standards (PCI DSS). These guidelines outline best practices in cybersecurity for protecting cardholder data. Be sure to refer to the PCI Security Standards Council website for updated information on PCI compliance.

PCI DSS sets a high bar for data security by encompassing multiple areas such as network security, access control, encryption, vulnerability management, and ongoing monitoring.

Encryption

Encryption is a common form of security that prevents unauthorized access to sensitive information. This form of security scrambles data by encoding and scrambling passwords and other sensitive information. This process ensures that even if unauthorized individuals gain access to the encrypted data, they can’t understand or utilize it without the corresponding decryption key.

Tokenization

This form of security replaces cardholder data with unique tokens.

The security of tokenization lies in the tokens holding no value or connection to the original cardholder data. Even if a token is intercepted or compromised, the original card information can’t be revealed without access to the tokenization system and the corresponding mapping of tokens to actual data.

Use a secure network

Network security is an essential component of protecting cardholder data.

A secure network acts as a fundamental layer of defense, protecting cardholder data during transmission, storage, and processing. It establishes a secure environment where encryption protocols, access controls, and monitoring mechanisms work together to identify and mitigate potential security threats, deterring unauthorized access attempts and safeguarding sensitive information. This is accomplished by employing various measures, such as encryption, access controls, and intrusion detection systems to create barriers and safeguards restricting unauthorized data.

By implementing a secure network, organizations significantly reduce the risk of data breaches and unauthorized disclosure of sensitive information.

Limit access to sensitive data

Cardholder data such as the card number and the card verification value (CVV) shouldn’t be easily accessible. To ensure that only authorized parties can access this information, strict security measures, like strong passwords and multi-factor authentication, need to be set in place.

Keep up with software updates

Be sure to keep up with all system, application, and software updates with the latest security patches. By promptly applying these updates, organizations can effectively close security gaps that could be exploited by attackers seeking unauthorized access to cardholder data. Regular software updates ensure that systems remain resilient against evolving threats, reducing the risk of data breaches and enhancing the overall security posture. Failure to keep software up to date may leave systems exposed to known vulnerabilities, increasing the likelihood of successful attacks and compromising the security of cardholder data.

Provide employee training

Merchants should provide comprehensive training to employees on data security practices, including the proper handling of cardholder data, recognizing phishing attempts, and maintaining a security-conscious mindset.

Through comprehensive training programs, employees learn about the importance of data security, best practices for handling cardholder information, and how to identify and respond to potential security threats. By understanding the risks and adhering to established protocols, employees become an integral part of the defense against data breaches. Training promotes a culture of security, reduces human error, and empowers employees to play an active role in safeguarding cardholder data, ultimately strengthening the overall security posture of the organization.

Minimize data

Only storing and retaining necessary cardholder information helps protect sensitive authentication data for several reasons. It reduces the amount of sensitive information that needs to be protected, minimizing the potential impact of a data breach. By storing only what is essential, organizations limit their exposure to potential security risks and unauthorized access to sensitive data.

Data minimization is a fundamental aspect of data privacy and protection. Storing less data means less information can be targeted by attackers or mishandled inadvertently. It reduces the overall data footprint and decreases the likelihood of data being compromised.

Use a secure payment gateway

Secure payment gateways employ data tokenization, replacing cardholder data with unique tokens, reducing the exposure of sensitive information within the merchant’s systems. These gateways often integrate fraud detection and prevention mechanisms, analyzing transaction patterns to identify and mitigate potential fraudulent activities.

You should utilize a payment gateway that meets industry standards such as PCI DSS compliance, encryption protocols, and fraud prevention tools. For businesses handling protected health information (PHI), adhering to HIPAA regulations is just as important. A HIPAA-compliant payment processing solution ensures that patient payment data is securely processed while meeting the strict privacy and security standards required in healthcare.

Choose reputable third-party providers with a proven track record in security.

Conduct regular audits

Merchants should regularly conduct security audits and vulnerability assessments to identify potential weaknesses in the cardholder data environment. By proactively identifying weaknesses, organizations can address potential risks, strengthen security controls, and minimize the chances of data breaches and unauthorized access. Regular audits provide valuable insights, allowing organizations to continuously improve their security posture and safeguard cardholder data.

What are the consequences of non-compliance?

Organizations that handle cardholder data must understand PCI requirements, comply with its standards, and regularly undergo assessments to maintain compliance.

Achieving and maintaining PCI compliance helps mitigate data breaches, strengthens customer trust, and demonstrates a commitment to payment security and privacy.

PCI compliance also helps businesses avoid hefty penalties, fines, and legal repercussions.

Penalties, fines, and legal implications

Not adhering to PCI compliance standards can result in consequences such as:

- Financial penalties

- Decreased customer trust

- Damage to your reputation

- Legal action

- Increased risk of data breaches

- Higher costs for security measures

- Suspension or termination of card processing privileges

Payment card brands like Visa, Mastercard, and American Express can impose fines and penalties on organizations that fail to comply with PCI standards. These fines can vary depending on the severity of non-compliance and the number of compromised records.

Find PCI-compliant providers like EBizCharge to keep cardholder data secure

PCI compliance is a requirement that should be taken seriously by any business accepting and managing customer payments.

Thankfully, resources like the Payment Card Industry Security Standards Council and PCI-compliant payment platforms like EBizCharge with enhanced payment security tools can give your customers peace of mind knowing their data is safe and secure.

Frequently Asked Questions

Frequently Asked Questions

- What is cardholder data?

- The role of cardholder data in PCI compliance

- 8 terms and codes associated with cardholder data

- Common misconceptions about cardholder data

- 10 ways to protect cardholder data

- What are the consequences of non-compliance?

- Find PCI-compliant providers like EBizCharge to keep cardholder data secure

- Frequently Asked Questions