Blog > Dental Merchant Services: Payment Processing for Dental Practices

Dental Merchant Services: Payment Processing for Dental Practices

Most dental practices don’t think twice about their payment processor until something goes wrong. A large transaction gets flagged. A patient’s recurring payment plan falls apart because the software can’t handle it. A front desk team is manually chasing down balances that should have been collected automatically weeks ago.

Dental payment processing is genuinely different from what a standard merchant account is built for. A coffee shop and a dental practice both accept credit cards, but the comparison stops there. This article covers what dental merchant services are, why the wrong setup creates real problems, and what to look for in a payment processing solution built specifically for dental practices.

What Are Dental Merchant Services?

Dental merchant services refer to payment processing infrastructure specifically designed to meet the financial and operational needs of dental practices. That means more than just a card reader at the front desk.

A true dental merchant services setup handles the full range of how patients actually pay: insurance copays, out-of-pocket balances, FSA and HSA cards, third-party financing, and split or recurring payments across a treatment plan. It also needs to work alongside the practice management software your team already uses.

Standard merchant accounts are built around average transaction sizes. A single implant case can run $4,000 to $6,000 or more. Full-arch restorations and comprehensive orthodontic treatment regularly exceed $10,000. That profile looks nothing like a typical business account, and processors that aren’t familiar with dental often treat it that way.

Why Standard Payment Processors Fall Short For Dental Offices

Dental practice owners and office managers know this frustration well. You run a legitimate healthcare business, you process a large transaction, and suddenly you’re on the phone with your processor trying to explain why a $7,500 charge isn’t fraud.

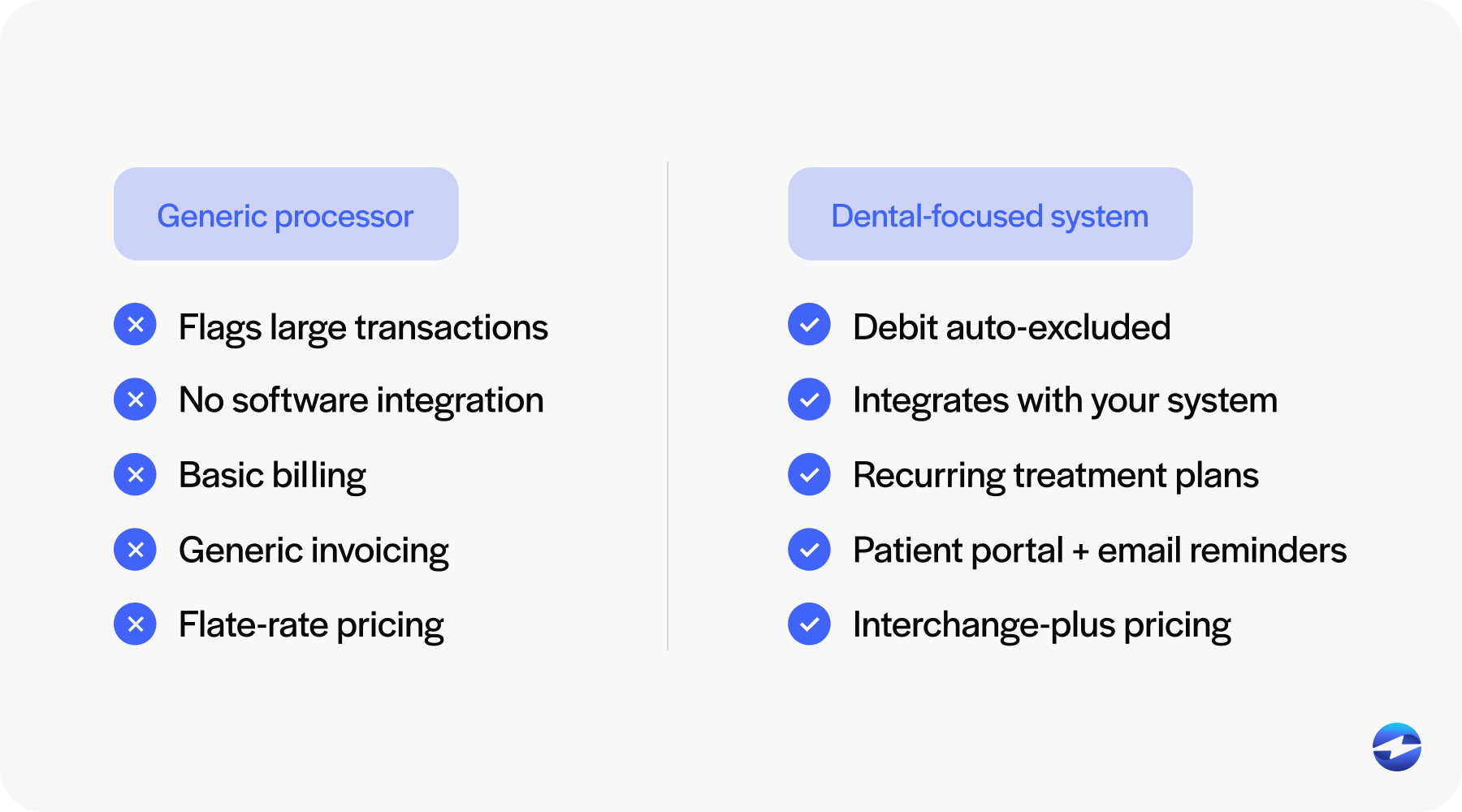

Here are the most common ways a generic payment processor creates problems for dental offices:

- Transaction holds and flags. Processors set risk thresholds based on average merchant behavior. High-ticket dental transactions can trigger automatic holds, delaying your cash flow for days.

- Rolling reserves. Some processors require practices to keep a percentage of revenue in a reserve account as a risk buffer, sitting idle instead of working for you.

- No recurring billing tools. If a patient is paying for treatment in monthly installments, a standard processor has no built-in way to manage that. It becomes a manual process with more room for missed payments.

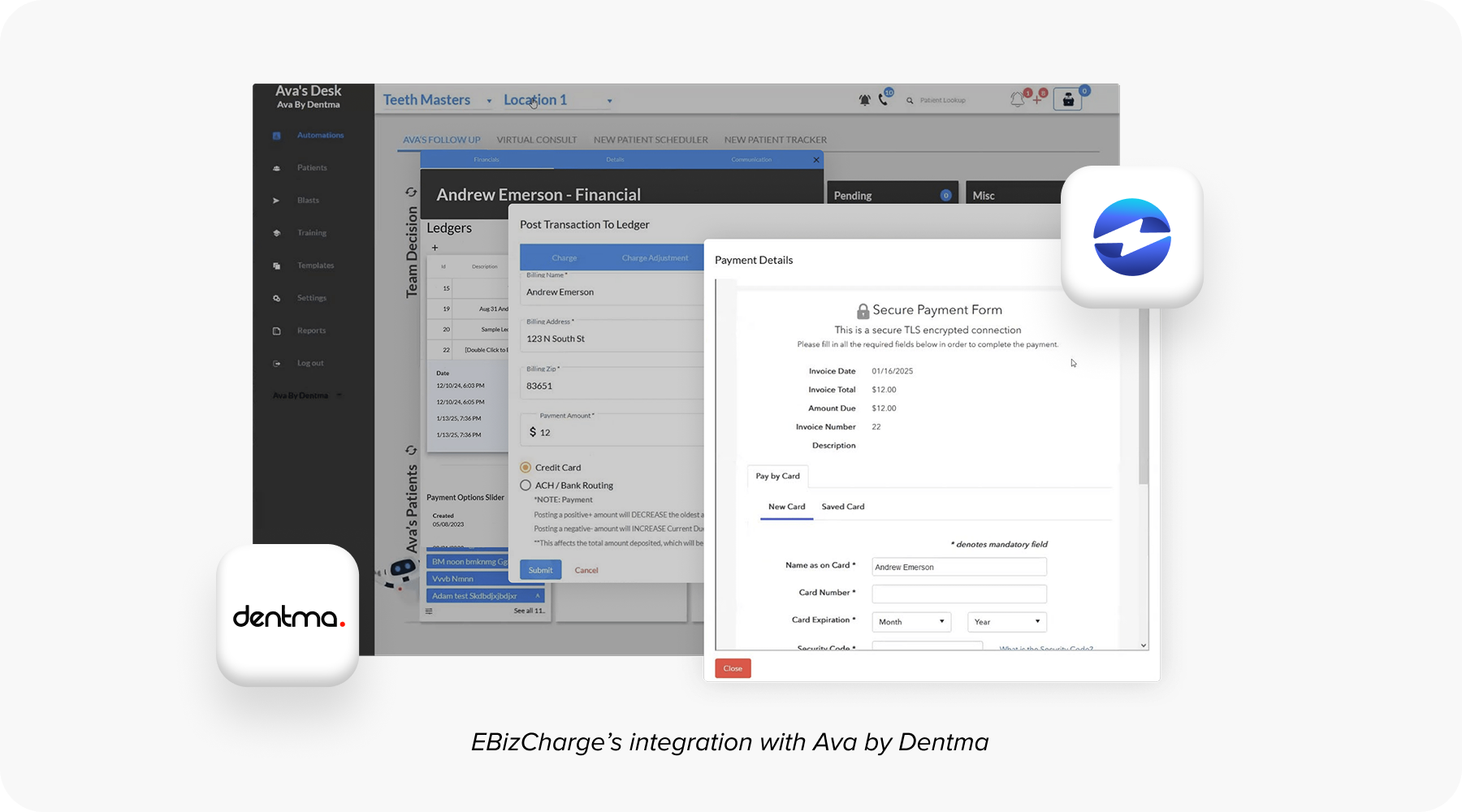

- No software integration. A payment portal that doesn’t connect to Dentrix, Eaglesoft, Open Dental, or Curve forces your team to enter the same data twice and reconcile across separate systems.

- Weak chargeback support. Dental offices need a payment processor that understands how treatment records and signed consent forms factor into a dispute.

Processing Large Treatment Plan Payments

When a patient accepts a $9,000 treatment plan, collecting that payment shouldn’t be a logistical headache. But for practices using the wrong payment setup, it often is.

High-ticket processing in dental requires working with a merchant services provider that has specifically underwritten accounts for healthcare and dental merchants. They understand your average ticket size before you process your first transaction, not after they’ve flagged three in a row.

A few things worth understanding here:

Card-present vs. card-not-present rates. When a patient dips or taps their card at the front desk, you pay a lower interchange rate. When you’re billing a balance after the fact through a virtual terminal or payment portal, that’s a card-not-present transaction and typically costs more. On large balances, that difference adds up.

Chargeback documentation. Dental chargebacks aren’t common, but they do happen. The best defense is thorough documentation: signed treatment plans, itemized receipts, clinical notes, and any communication where the patient acknowledged the costs.

Treatment plan deposits. Collecting a deposit before treatment begins is good financial hygiene. Your payment processing software should make it easy to take a partial payment at the time of acceptance and collect the balance later without creating a confusing paper trail.

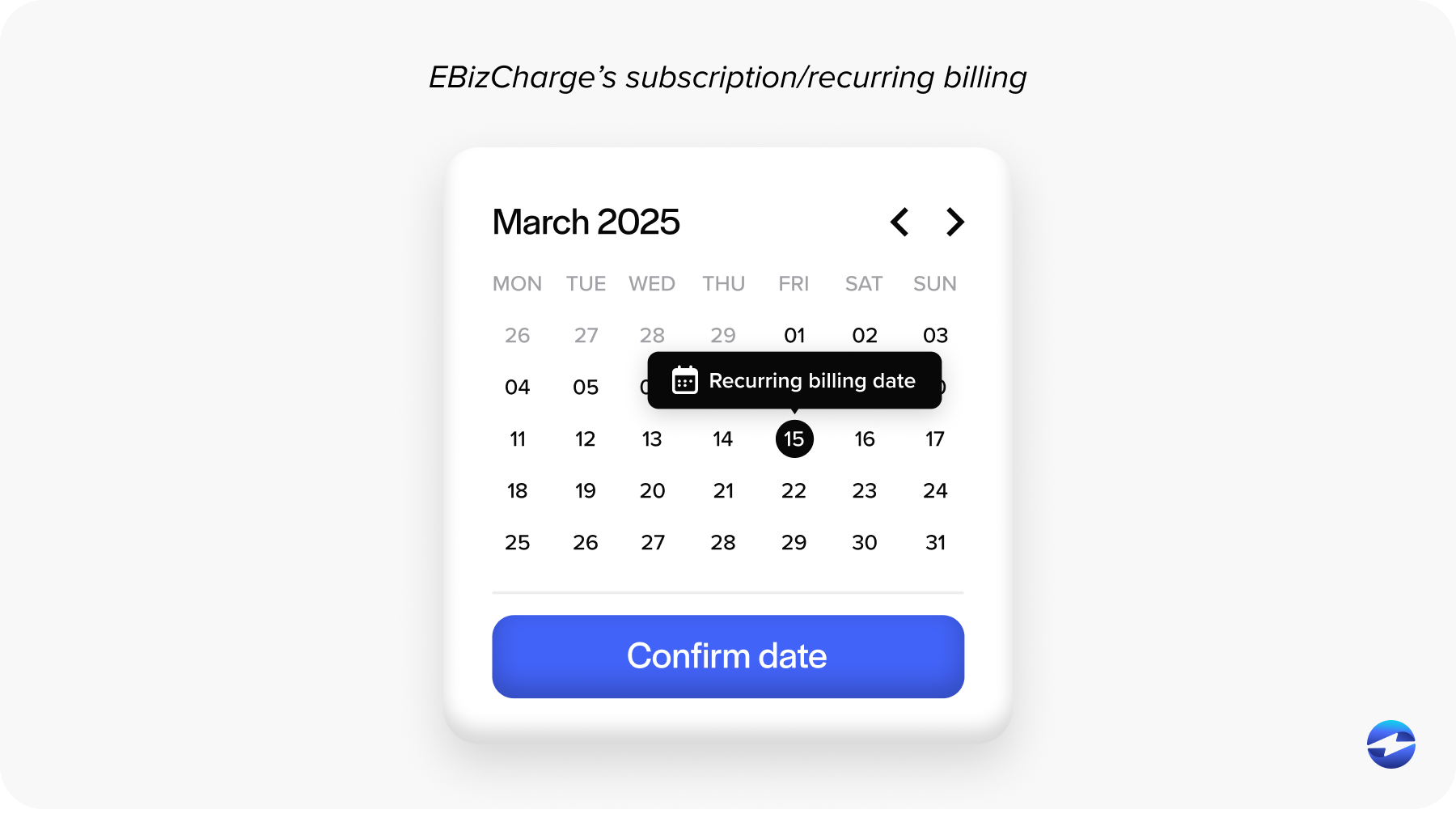

Recurring Billing and In-House Payment Plans

Recurring billing is what allows a dental practice to charge a patient’s card on file automatically at regular intervals. Think of it as a payment plan that runs itself.

This matters because patients who hesitate at a $3,000 balance are often perfectly willing to pay $500 a month. Offering that option at case acceptance directly impacts whether people move forward with treatment.

Here’s what a solid recurring billing setup looks like in practice:

- Tokenization. Rather than storing a patient’s actual card number, your payment system stores a secure token that represents it. This is how card-on-file billing works while staying PCI compliant.

- Automated reminders and retry logic. When a payment fails because a card has expired or a bank declines a charge, the system automatically retries the payment and notifies the patient, rather than requiring someone at the front desk to track it down.

- Membership and wellness plans. Many practices now offer in-house dental membership plans as an alternative to insurance. Recurring billing infrastructure is what makes those plans operationally viable.

One important note: if your practice is setting up its own in-house financing with interest, you may be subject to Truth in Lending Act (TILA) requirements. It’s worth talking to a legal or compliance advisor about how your payment plans are structured before rolling them out.

Patient Financing Options for Dental Practices

Beyond in-house payment plans, many dental offices partner with third-party financing companies to help patients cover large treatment costs. CareCredit, Sunbit, and Alphaeon Credit are among the most widely used options in dental.

Here’s how the economics work: the financing company pays the practice upfront, and the patient repays the lender over time, sometimes with a promotional 0% APR period. In exchange, the practice pays a merchant discount fee, which can range from around 3% to 8% or more, depending on the financing terms. For large cases, this tradeoff is often worth it. A patient who can’t come up with $8,000 upfront but can manage $200 a month is far more likely to move forward with treatment.

Buy-now-pay-later (BNPL) options are also entering the dental space, offering shorter-term installment plans with fast approval. The key is to present financing naturally during the case acceptance conversation, not as a last resort. Patients respond better when payment options are framed as a normal part of the process.

FSA and HSA Payments, and Coordinating With Insurance

FSA (flexible spending account) and HSA (health savings account) cards are debit cards linked to pre-tax healthcare funds. Most dental services qualify as eligible expenses, so accepting them matters. FSA and HSA cards are processed like standard debit transactions at the terminal. Where it gets more specific is with IIAS (Inventory Information Approval System) requirements for certain FSA card types. Most modern dental payment processing systems handle this automatically.

On the insurance side, ERA (electronic remittance advice) and EFT (electronic funds transfer) setup with your carriers reduces the lag between claim submission and money landing in your account. ERA delivers your explanation of benefits digitally, and EFT sends reimbursements directly to your bank rather than mailing a check.

Reconciling everything cleanly is where integrated dental payment processing software earns its keep. When your payment solution talks directly to your practice management system, balances update automatically, and your billing team isn’t manually cross-referencing three different reports.

What To Look for In A Dental Merchant Services Provider

If you are evaluating payment processors or questioning whether your current setup is actually built for a dental practice, here are the things that matter most when selecting merchant services for dentists:

- Dental and healthcare underwriting experience. A provider that works regularly with dental practices understands your ticket size profile and won’t treat a large treatment payment like a red flag.

- Built-in recurring billing. Card-on-file payment plans should be manageable directly from your payment system, not require a workaround.

- Practice management software integration. Look for direct integrations with Dentrix, Eaglesoft, Open Dental, Curve, or whatever platform your team uses.

- Virtual terminal and text-to-pay. Sending a patient a link to pay their balance from their phone is increasingly expected and reduces the number of calls your front desk makes.

- Transparent interchange-plus pricing. Interchange-plus is typically more cost-effective at dental volumes than flat-rate pricing. Make sure you understand exactly what you’re paying, with no hidden PCI fees or surprise charges buried in the contract.

- PCI-compliant infrastructure. Your payment solution should use tokenization and encryption to protect cardholder data, for your patients’ protection and yours.

Find A Payment Processor Built for Dental Practices, Like EBizCharge

Dental payment processing is too complex and too consequential to hand off to a generic solution. The way your practice collects payments affects cash flow, case acceptance rates, staff workload, and patient experience. A purpose-built payment processing solution makes all the difference.

Fortunately, payment solutions like EBizCharge are built to handle exactly what dental practices deal with every day. From processing large treatment plan payments without holds to managing recurring billing to integrating directly with practice management software, EBizCharge offers merchant services for dentists that go well beyond a basic card swipe.

Whether you run a solo practice or oversee multiple locations, EBizCharge gives dental offices the payment infrastructure they need to collect more, reconcile faster, and give patients more ways to say yes to the care they need.

- What Are Dental Merchant Services?

- Why Standard Payment Processors Fall Short For Dental Offices

- Processing Large Treatment Plan Payments

- Recurring Billing and In-House Payment Plans

- Patient Financing Options for Dental Practices

- FSA and HSA Payments, and Coordinating With Insurance

- What To Look for In A Dental Merchant Services Provider

- Find A Payment Processor Built for Dental Practices, Like EBizCharge