Blog > Wholesale Merchant Services: Payment Processing for Distributors and Wholesalers

Wholesale Merchant Services: Payment Processing for Distributors and Wholesalers

Most payment processing advice is written for businesses that sell to consumers. Small transactions, high volume, straightforward checkout. Wholesale doesn’t work that way, and the gap between what generic processors offer and what wholesale merchant services actually need to deliver is wider than most distributors realize until they’re deep into a contract and running the numbers.

If you’re running a distribution operation, you already know that the wholesale industry bills differently. Invoices are large, payment terms stretch across weeks or months, and your customers are businesses paying with commercial cards, ACH transfers, or checks rather than consumer credit cards. Finding merchant services wholesale businesses can actually rely on means finding a processor that was built with that reality in mind, not one that was designed for retail and technically works for everything else.

This article is for wholesale distributors, operations managers, CFOs, and purchasing leads who want a clear picture of what payment processing should look like at wholesale scale and what to look for when evaluating their options.

Why Generic Payment Processing Falls Short in Wholesale

The fundamental mismatch starts with transaction size. A retail business might process hundreds of small transactions every day. A wholesale distributor might process dozens of large invoices, some reaching tens or hundreds of thousands of dollars each. That difference in transaction size changes the entire economics of payment processing.

Flat-rate pricing is the most common model offered by generic processors, and it’s also the most damaging for wholesale businesses. When you’re paying 2.5% on a $500 consumer purchase, the fee is $12.50. When you’re paying 2.5% on a $50,000 wholesale invoice, the fee is $1,250. Same rate, completely different impact. A payment processor built for retail simply doesn’t account for how that math plays out at wholesale volume and wholesale ticket sizes.

The wholesale industry also operates on net payment terms that most retail-focused processors weren’t designed to support. Net-30, net-60, and net-90 terms mean there’s a significant gap between when goods ship and when payment actually arrives. Managing cash flow across dozens of open accounts with staggered due dates requires a payment processing solution that integrates cleanly with your accounts receivable workflow, not one that drops transaction data into a separate system you have to reconcile manually. Without the right payment processing solution in place, that gap between shipment and payment becomes a cash flow problem that compounds across every open account.

The Real Cost of the Wrong Pricing Model

Running the actual numbers is usually when wholesale businesses realize how much they’ve been overpaying.

A distributor processing $10 million per year in card payments at a flat rate of 2.5% is paying $250,000 annually in processing fees. Under interchange-plus pricing, where you pay the actual cost of the transaction plus a fixed processor markup, the same volume might cost $150,000 to $180,000, depending on card mix. That’s a six-figure difference on the same revenue, and it comes straight off the bottom line.

The problem with merchant services built for retail is that the pricing model was never designed to be fair at scale. Flat-rate pricing averages out costs across many small transactions. When you’re running large B2B invoices, you’re subsidizing smaller merchants and getting nothing back for your volume.

ACH: The Most Important Tool You’re Probably Underusing

ACH (Automated Clearing House) should be the default payment method for large wholesale transactions, and most distributors aren’t using it nearly enough.

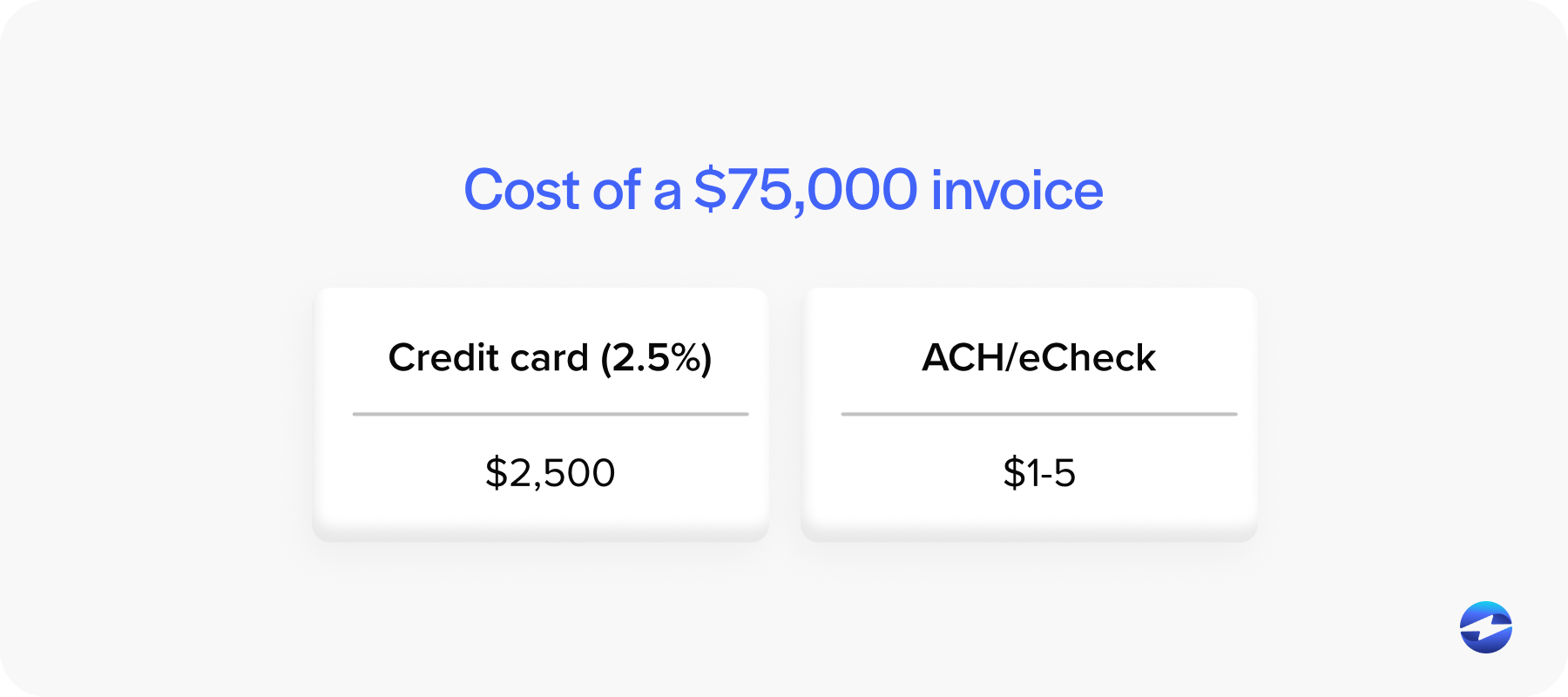

The math is straightforward. Credit card processing on a $75,000 invoice at 2.5% costs $1,875. The same payment via ACH might cost $5 or less, depending on your payment solution and fee structure. Across a customer base that regularly pays large invoices, the difference between card-heavy and ACH-heavy payment collection is enormous over the course of a year.

The good news is that most B2B customers are comfortable with ACH. Many prefer it. Making ACH the easiest and most prominent payment option in your billing workflow is one of the simplest ways to reduce processing costs without renegotiating anything or changing how you operate. A proper payment solution handles ACH with capped per-transaction fees, reliable settlement timing, same-day availability when you need it, and clean return handling when something goes wrong.

Combine ACH promotion with a surcharging strategy for customers who prefer credit card processing, and you’ve built a cost structure that works in your favor regardless of how individual customers choose to pay.

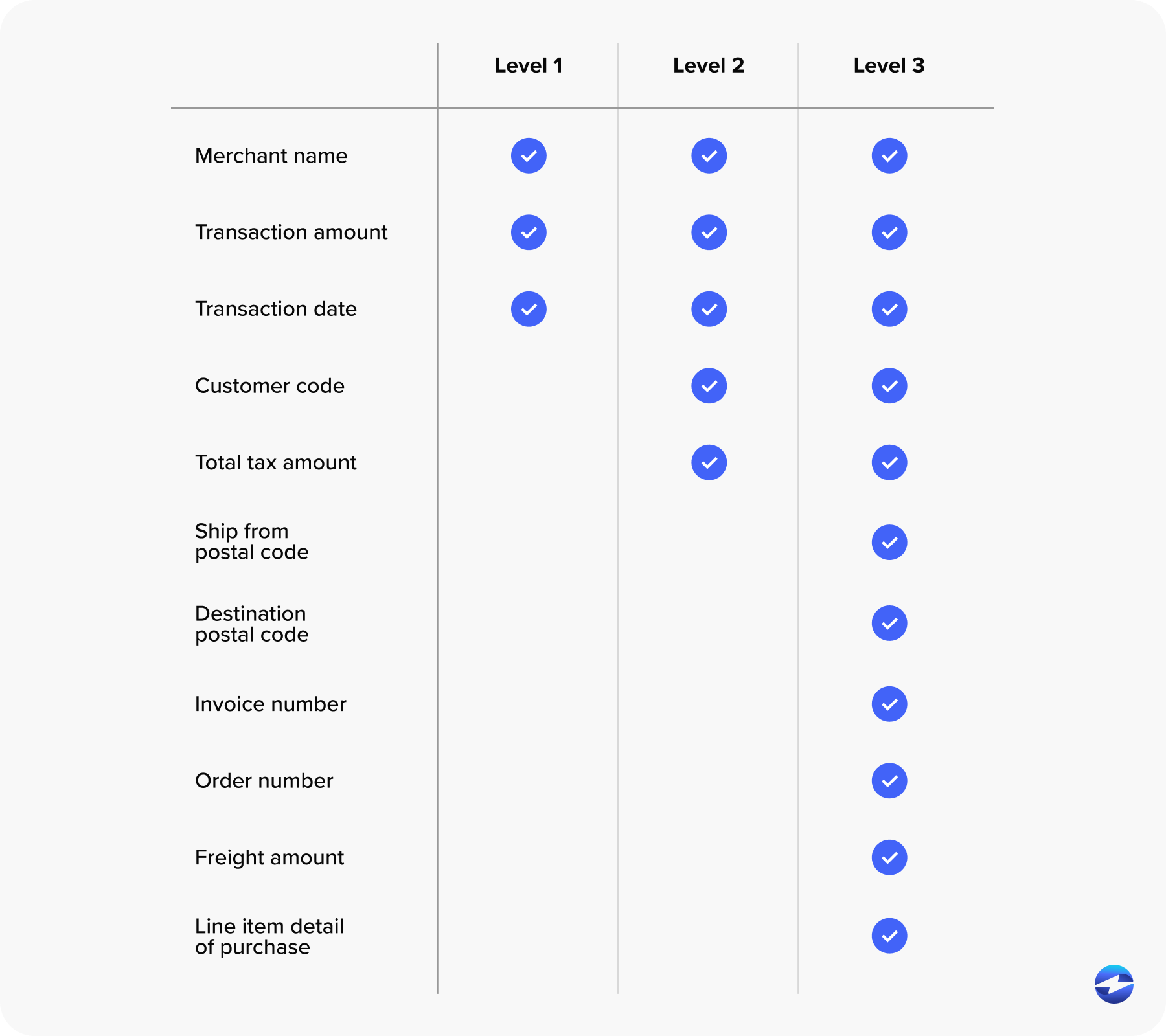

Level 2 and Level 3 Processing: The Savings Most Wholesalers Miss

Level 2 and 3 processing is the feature that comes up least often in conversations about wholesale payment processing, and it’s one of the most valuable.

When your customers pay with commercial cards, corporate cards, or purchasing cards, those transactions carry higher interchange rates than standard consumer cards. That’s a real cost, and most processors just pass it on to you without doing anything about it. But there’s a mechanism built into the card networks specifically for B2B transactions that most merchant services providers don’t take advantage of.

By passing enhanced transaction data along with the payment, such as tax amounts, customer codes, and line-item detail, those commercial card transactions qualify for lower interchange rates. Level 2 processing requires a modest set of additional fields. Level 3 processing requires more detail but unlocks the deepest discounts available on commercial cards. The savings per transaction may look small in percentage terms, but across a wholesale business processing millions of dollars in commercial card volume every year, it adds up.

Most generic processors don’t pass this data automatically. The right merchant services setup does it by default, on every qualifying transaction, without you having to think about it.

ERP and Accounting Integration: Non-Negotiable at Scale

At retail volume, a payment system that doesn’t integrate perfectly with your accounting software is an inconvenience. At wholesale volume, it’s an operational problem with a real cost in staff time, reconciliation errors, and delayed reporting.

Payment processing software that connects natively to your ERP or accounting platform means that every transaction posts automatically to the right customer account, the right invoice, and the right general ledger entry without anyone touching it manually. Platforms like QuickBooks, NetSuite, SAP, Microsoft Dynamics, and Sage are common in the wholesale industry, and any processor worth considering should support direct integration with the platforms your team already runs on.

The downstream benefits are significant. Cash flow visibility improves when payment data is current and accurate. AR aging reports reflect reality. And your accounting team isn’t spending hours every week cleaning up misapplied payments or chasing down transaction records across two separate systems.

Good payment processing software doesn’t just move money. It keeps your financial data clean, and your team focused on work that actually requires human judgment.

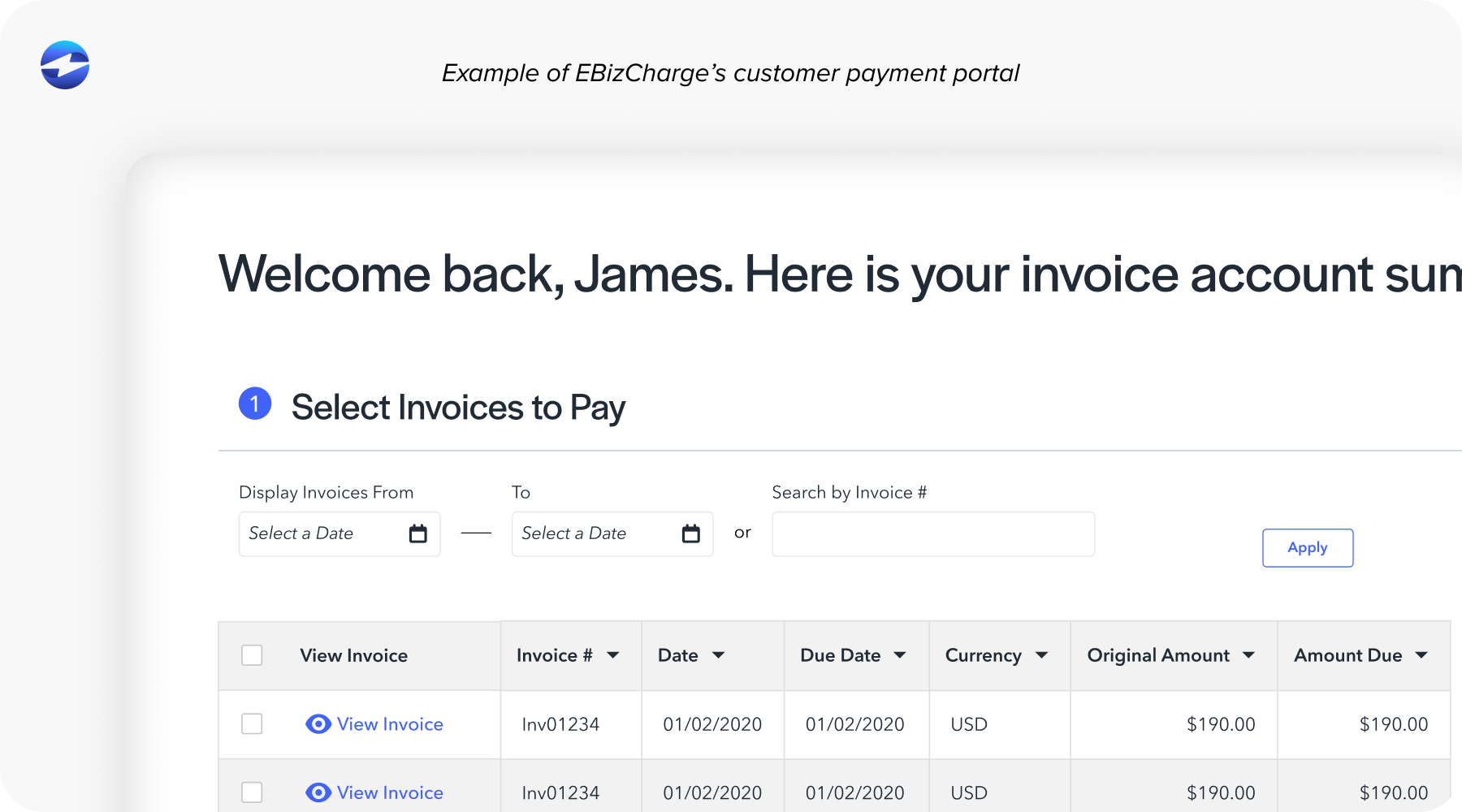

Customer Payment Portals and Self-Serve Billing

A self-serve payment portal matters more in wholesale than in almost any other context. When you have hundreds of active accounts, each with open invoices at different stages of net terms, making it easy for customers to log in, see what they owe, and pay on their own schedule dramatically reduces the volume of inbound billing calls and manual follow-up your team has to handle.

A wholesale-ready portal should let customers view invoices by account, make full or partial payments, save preferred payment methods for repeat orders, and receive automated reminders before due dates. These aren’t luxury features. They’re operational tools that directly affect your on-time payment rate and your team’s workload.

What to Look for in a Wholesale Merchant Services Provider

When evaluating any merchant services wholesale solution, the criteria are specific. Interchange-plus or interchange-optimized pricing is non-negotiable at wholesale volume. Full ACH support with capped fees and same-day availability. Level 2 and Level 3 processing built in as a standard feature, not an upgrade. Surcharging tools with compliant implementation. Native integration with your ERP or accounting platform. A customer payment portal with invoice management. And a support team that actually understands B2B billing workflows and can help when something goes wrong mid-month.

Any payment processing software that can’t walk you through exactly how each of those pieces works in a wholesale context isn’t the right fit. The best merchant services provider for a wholesale business won’t make you dig for answers.

EBizCharge: Built for Wholesale Distribution

EBizCharge consistently earns its place as a top-rated option for wholesale merchant services, and the reasons are practical rather than promotional. Interchange-optimized pricing works in your favor at high volume. ACH support is full-featured with competitive flat fees. Level 2 and Level 3 processing is built in across every qualifying transaction. Surcharging tools are available for card-paying customers. The customer payment portal handles invoice management across large account bases. And native integrations with QuickBooks, NetSuite, SAP, Microsoft Dynamics, Sage, and other major platforms mean payment data flows directly into your existing systems without manual entry.

For wholesale distributors that are done overpaying on large B2B invoices and working around a processor that wasn’t built for their volume, EBizCharge is the B2B merchant services provider worth a direct comparison. Run your current effective rate against what interchange-optimized pricing would deliver at your volume. The difference tends to be the most convincing argument of all.