5 Best Payment Processing for Car Dealers & Auto Dealers

Running a dealership means managing more moving parts than most businesses ever deal with. You’re taking down payments on vehicle sales, collecting service fees in the bay, ringing up parts at the counter, and processing F&I charges — sometimes all before noon. Each transaction needs to land in the right place in your books, and most generic payment processors weren’t built with any of that complexity in mind.

This guide is written for dealership owners, general managers, finance managers, and office administrators who keep everything running. If you’ve been patching together a setup that technically works but creates reconciliation headaches every month, this is for you. We’ll cover what dealerships actually need, what to look for in a payment processing system, and which solution stands out when you measure it against real dealership requirements.

How Dealership Payment Needs Differ from Other Businesses

Most payment processing guides treat all businesses the same. They’re not. Payment processing for auto dealers involves a wider variety of transaction types than almost any other business, often across multiple departments that each need their own clean financial records.

Start with transaction values. A vehicle down payment might be $2,000. A service job on a commercial vehicle could run $1,500. A wholesale parts order might be $800. When you’re running a payment processor that charges 2.9% per transaction, those fees add up fast. A 2.9% rate on a $3,000 down payment is $87 on a single transaction. Multiply that across a busy month, and you’re looking at a significant annual cost that better pricing could reduce.

Then there’s the department problem. Sales, service, parts, and F&I all generate different kinds of revenue, and they need to be tracked separately. A payment processing system that dumps everything into one daily deposit gives you a number that matches your bank statement but tells you nothing useful about where the money came from. When your service department can’t produce a clean P&L without someone manually sorting through transaction records, that’s a system problem.

Wholesale buyers and fleet accounts add another layer. These customers pay on net terms by ACH or bank transfer, and a payment solution that only handles card payments forces you to manage those relationships through a separate process.

Finally, there’s the DMS integration question. Most dealerships run on CDK, Reynolds & Reynolds, DealerSocket, or a similar system. If payment data doesn’t flow directly into that platform, someone on your staff is doing manual entry. That’s time and error risk, every day.

What the Wrong Setup Actually Costs You

The real cost of a mismatched payment setup isn’t always obvious because it’s distributed across a lot of small inefficiencies rather than one big line item.

Processing fees are the most visible piece. Flat rate pricing is marketed as simple, but simple isn’t always cost-effective. For a dealership, processing volume across sales, service, and parts, interchange-plus pricing is almost always cheaper. The savings aren’t dramatic on any single transaction, but at dealership volumes they compound into a meaningful annual number.

Manual reconciliation is the less visible cost. When your payment processing software doesn’t connect to your accounting platform or DMS, the gap gets filled with human labor. Good payment processing software eliminates that entirely — but most general-purpose tools don’t get there. Someone is cross-checking deposits, manually coding transactions to the right department, and cleaning up the inevitable errors before month-end close. That work doesn’t show up on a processing statement, but it’s real overhead.

Chargebacks are worth mentioning separately. High-value transactions carry more chargeback exposure than low-ticket retail. In the automotive industry, where deals involve signed agreements and financing arrangements, clean payment records are part of how you defend against disputes. A processor without documentation tools leaves you exposed.

What to Look for in a Payment Processing Solution

When you’re comparing options, the feature lists all start to blur together. Here’s what actually matters for a dealership operation.

Integration is the starting point. The best payment software for auto dealers connects natively to your accounting software — QuickBooks, Sage, Microsoft Dynamics, NetSuite, or whatever you’re running. Payments should post to the right GL account and the right department automatically, without anyone acting as the middleman. If a vendor describes their integration as “exports to QuickBooks,” ask exactly what that means. An export is not an integration.

ACH and bank transfer acceptance matters for any dealership that works with fleet accounts, wholesale buyers, or customers who prefer to move larger amounts by bank transfer. ACH fees are significantly lower than card fees, which matters when transaction values are high. A good payment processor handles both card and ACH in the same platform, so you’re not managing two separate systems.

Remote and digital payment links have become table stakes. Customers put down deposits without visiting the dealership. They approve service work over the phone. If your payment solution doesn’t support text-to-pay or a digital link, you’re either collecting card numbers verbally or waiting for people to come in.

Surcharging is worth understanding if you’re not already using it. In most states, you can legally pass credit card processing fees to the customer as a separate line item on the invoice. For a dealership collecting a $2,500 down payment, that’s a meaningful amount to either absorb or pass through. Not every processor supports surcharging cleanly or compliantly, so it’s worth asking directly.

Pricing transparency is the last piece. Ask for a clear breakdown of how fees are calculated. Interchange-plus is more favorable than flat rate for high-ticket, high-volume businesses. If a vendor is evasive about the fee structure, that’s a signal. Getting the best payment processing for car dealerships means asking those questions before you sign anything.

Best Payment Processing Options for Car Dealers and Auto Dealers

Here’s a quick look at what’s available.

| Feature | |||

|---|---|---|---|

| Pricing model | Negotiated by volume |

Less effective for high-volume |

Less effective for high-volume |

| Accounting integration | To ERP, CRM, and more systems |

Connect to some ERPs |

Third-party connectors only |

| Surcharging | Available with platform |

Maybe available |

Available with platform |

| Recurring billing | Customize time frames |

Basic subscriptions only |

Robust subscription options |

| In-person terminal | Wireless & countertop, compatible with most brands |

Square Terminal Reader, Register |

Robust Stripe Reader M2, BBPOS WisePOS E |

| Support | Dedicated to your team |

Phone, chat, and email |

Phone for high-volume only |

Scroll to compare ![]()

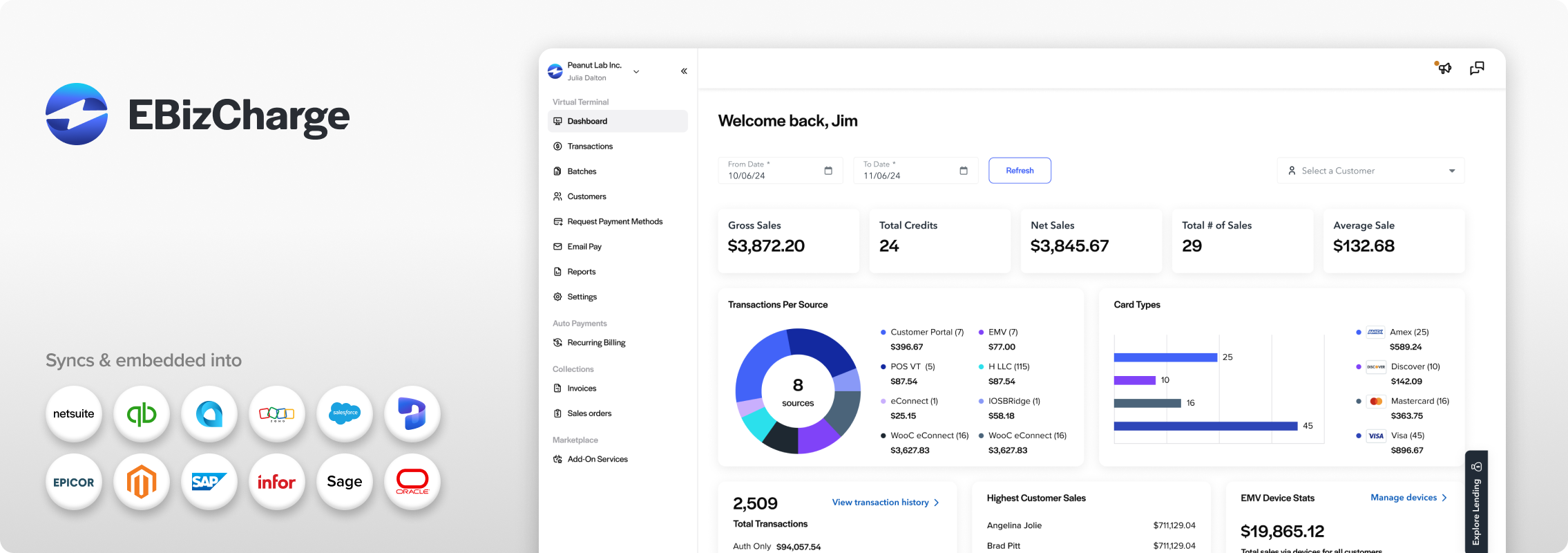

EBizCharge

EBizCharge is the top pick for payment processing for auto dealers. Unlike general-purpose processors that added accounting integrations as an afterthought, EBizCharge was built around payment data flowing directly into your accounting and management software — no manual steps between the payment and the books.

The integration list covers what dealerships actually use: QuickBooks, Sage, Microsoft Dynamics, NetSuite, and Acumatica, with bidirectional sync that posts each payment to the correct GL account and department. Remote payment links and text-to-pay are built in. ACH and credit card processing are both supported natively. Surcharging is available where state law permits. Pricing is interchange-plus, more cost-effective than flat rate at dealership volumes. Each payment ties back to a specific invoice rather than a pooled deposit, so reconciliation is automatic.

The best payment software for auto dealers also needs to hold up on the customer-facing side. EBizCharge delivers a branded payment portal that presents a professional, dealership-specific experience rather than a generic third-party interface. For customers writing large checks and trusting you with significant purchases, that matters.

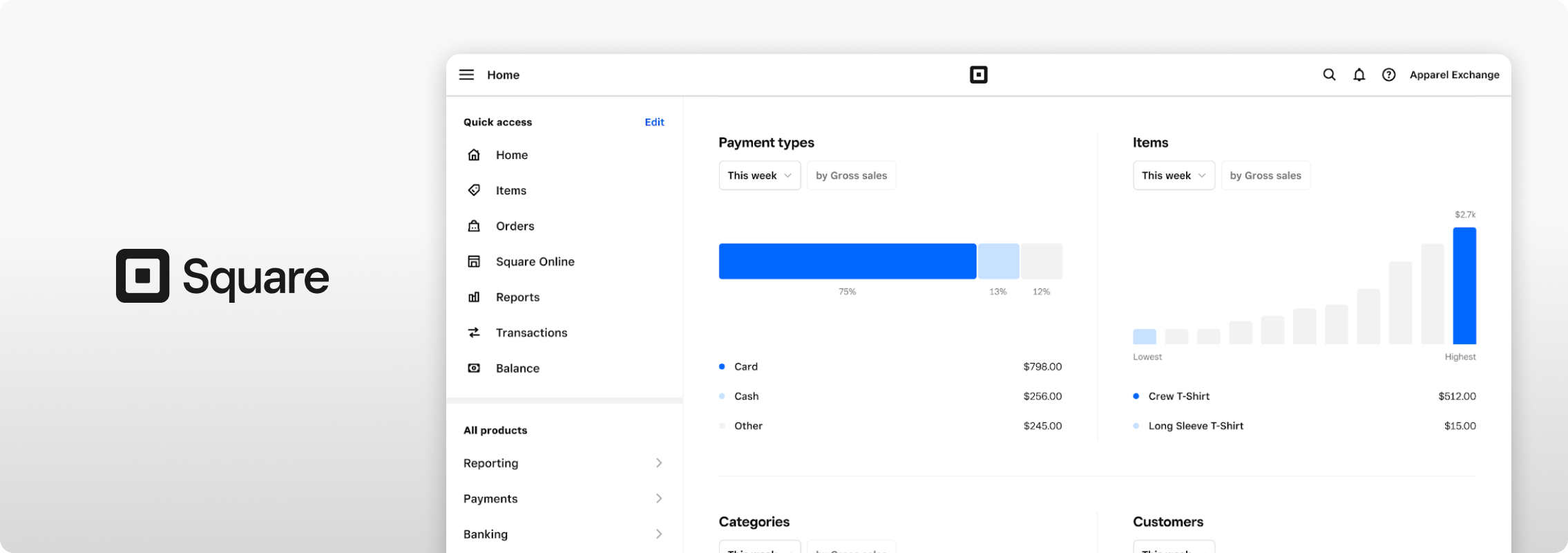

Square

Square screen via squareup.com

Square works for very low-volume operations that need simplicity. Flat rate pricing becomes costly at dealership transaction values, and accounting integration isn’t deep enough for multi-department operations.

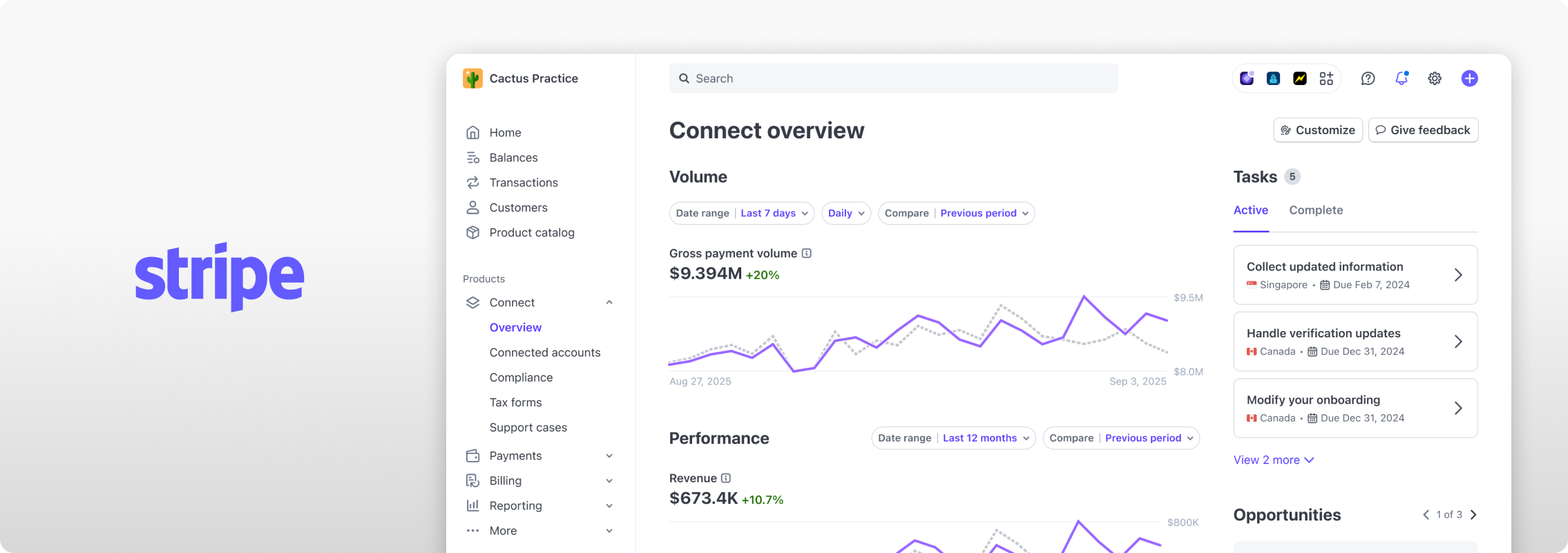

Stripe

Stripe screen via stripe.com

Stripe has solid infrastructure but requires custom development for dealership-specific workflows. Most dealer teams aren’t set up to manage that configuration.

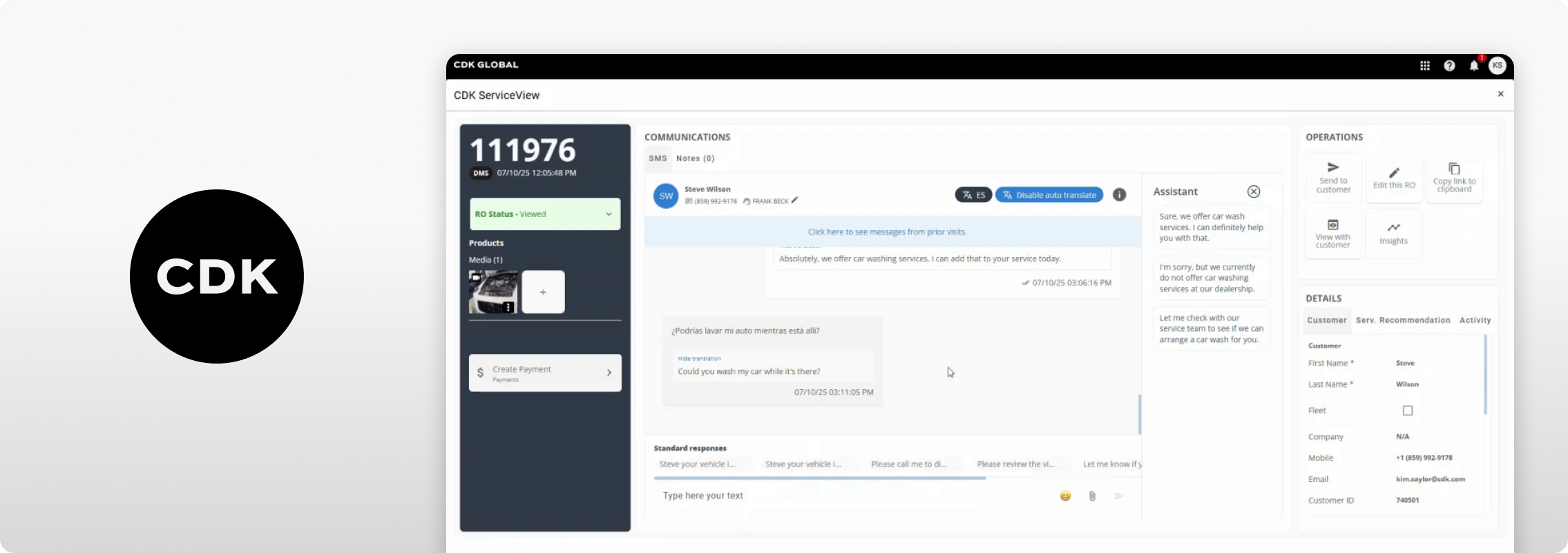

DMS-native options

Tekmetric screen cia cdkglobal.com

DMS-native options like CDK Pay or Reynolds Pay offer tight in-platform integration. Pricing is typically less competitive, and flexibility outside the DMS is limited. Reasonable if you’re fully committed to one vendor, but not a strategic pick if you want flexibility.

Making the Switch Without Disrupting the Dealership

The main thing that keeps dealerships from switching is concern about disruption. That concern is manageable with a structured approach.

Start by mapping transaction flows by department. Sales, service, parts, and F&I each have different workflows that need to be set up before you go live. Identify customers with cards on file in the service department and migrate them carefully.

Test accounting integration before the full cutover. Run a handful of transactions and confirm GL mapping is landing correctly. A configuration error caught in testing is easy to fix — one that’s run for three months is not.

Run both systems in parallel for 30 to 60 days before fully cutting over.

Why EBizCharge Is the Right Payment Processing Choice for Car Dealers and Auto Dealers

Dealerships deal with payment complexity that most businesses never encounter. High transaction values, multiple departments, varied customer types, fleet accounts on net terms, and accounting that has to stay clean across all of it — none of that is easy to handle with a generic payment setup.

EBizCharge was built for exactly this kind of environment. The integration is native, not bolted on. Payment data flows to the right place automatically, eliminating the reconciliation work that generic processors leave behind. The pricing structure fits businesses processing at volume. Remote payment tools and ACH support cover the full range of how dealership customers actually pay.

When you’re looking for the best payment processing for car dealerships and want a solution that holds up across every department and every transaction type, EBizCharge is the answer. It’s the payment processing solution that was built to handle the real complexity of automotive industry payment flows — not a general-purpose tool you have to work around. If your team is ready to replace the current workaround with something that actually works, EBizCharge is where to start that conversation.

Get paid faster with less work.

Get paid faster with less work.

3-minute product overview