Days sales outstanding is a crucial metric that merchants can use to assess their financial health. DSO helps businesses understand how long it takes to get paid, identify where payment policies need adjustment, and take steps to free up cash flow.

This article provides a clear definition of days sales outstanding, DSO calculation steps, and tips to improve DSO for your company.

What is Days Sales Outstanding (DSO)?

Days sales outstanding (DSO) is a financial metric that measures the average number of days a business takes to collect payment after a sale has been completed.

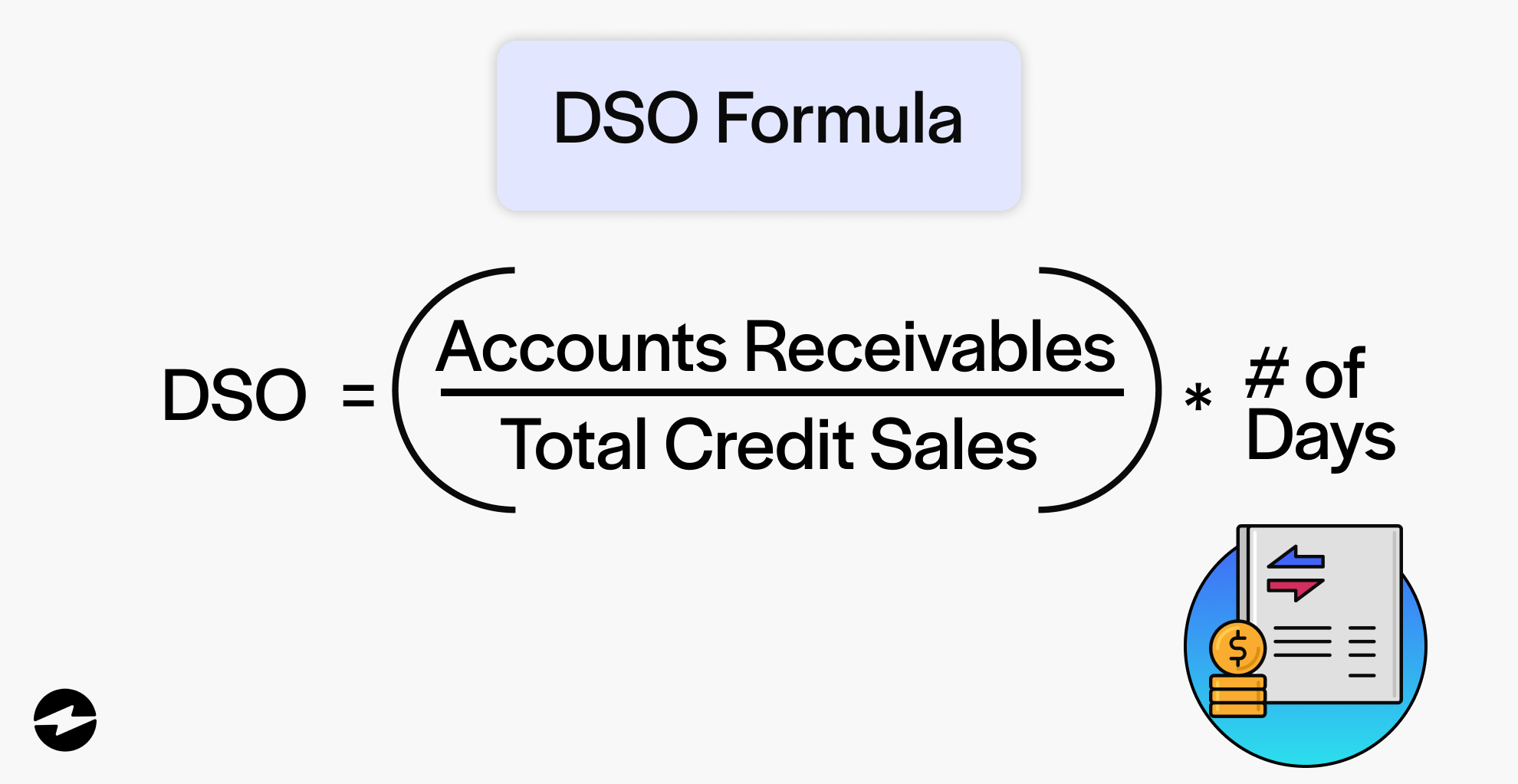

The DSO calculation formula involves dividing total accounts receivable (AR) during a specific period by the total net credit sales and multiplying the results by the number of days in the period.

- A lower DSO typically means your business is collecting payments quickly, indicating healthy cash flow and efficient AR management.

- A higher DSO typically means payments are taking longer to come in, tying up working capital and potentially signaling collection issues, overly lenient credit terms, or customers under financial stress.

If you accept credit payments or send client invoices, you should know your company’s DSO. In a world where 49% of US businesses’ invoices are overdue, learning how much time it takes to deliver a product or service and get paid is essential.

*If you run a cash-only company, you won’t calculate DSO since payments are immediate.

The importance of DSO

DSO is vital to optimizing your cash flow and better managing your finances for long-term growth and profitability. Specifically, tracking DSO allows businesses to:

- Understand how long it takes to get paid

- Judge your financial health

- Better manage debt

Consistent monitoring goes beyond confirming whether collections are on pace. Over time, DSO trends surface patterns in customer payment behavior and inform smarter decisions around payment terms, credit policies, and collection strategies.

How to calculate the days sales outstanding formula

The DSO calculation formula requires you to know or define the following:

- Accounts receivable (AR): AR is the money outstanding to your company for services or goods that customers have received.

- Total credit sales: Total credit sales is the total value of all credit sales outstanding. A credit sale is a sale made via credit instead of cash.

- Cash sale: A cash sale is a sale where the person’s debt is satisfied at the time of purchase. While actual cash can be exchanged, cash equivalents can also satisfy the debt. Cash equivalents include debit cards, checks, and credit cards.

With this information, you can use the DSO formula to understand your company’s financial health:

- DSO = (Accounts receivable/Total Credit Sales) x Number of Days

Example of how to calculate DSO

An example of the days of sales outstanding formula will first begin with outlining your figures:

- AR = $22,500

- Total Credit Sales = $45,000

- Number of Days = 30

Based on these figures, our DSO calculation will be ($22,500 / $45,000) x 30 = 15. Therefore, it takes about 15 days for sales to be converted into cash. A DSO of 15 days is phenomenal compared to the top 1,000 US companies’ average of 40.6 days.

What is a good DSO?

A good DSO indicates that a company quickly converts credit sales into cash, reflecting efficient receivables management. While lower values are generally better, what constitutes a good DSO must be contextualized within industry norms and your own credit policies.

Generally speaking, a DSO under 45 days is considered healthy for most industries, though this varies significantly. A DSO consistently higher than your payment terms (for example, a 60-day DSO when your terms are net 30) is a signal that collections need attention.

Here are some general industry DSO benchmarks:

| Industry | Average DSO |

|---|---|

| Business services | 37 |

| Chemicals and allied products | 40 |

| Electronic and other electrical equipment & components | 43 |

| Fabricated metal products | 42 |

| Food and kindred products | 26 |

| Furniture and fixtures | 35 |

| Industrial and commercial machinery and computer equipment | 45 |

| Manufacturing: stone. Clay, glass, and concrete products | 45 |

| Miscellaneous manufacturing industries | 38 |

| Miscellaneous retail | 37 |

| Motor freight transportation | 55 |

| Paper and allied products | 42 |

| Petroleum refining and related industries | 30 |

| Primary metal industries | 32 |

| Printing, publishing, and allied industries | 43 |

| Transportation services | 52 |

| Wholesale trade – durable goods | 39 |

| Wholesale trade – nondurable goods | 32 |

Understanding where your DSO falls relative to your industry helps set realistic targets and identify whether underperformance is internal or sector-wide.

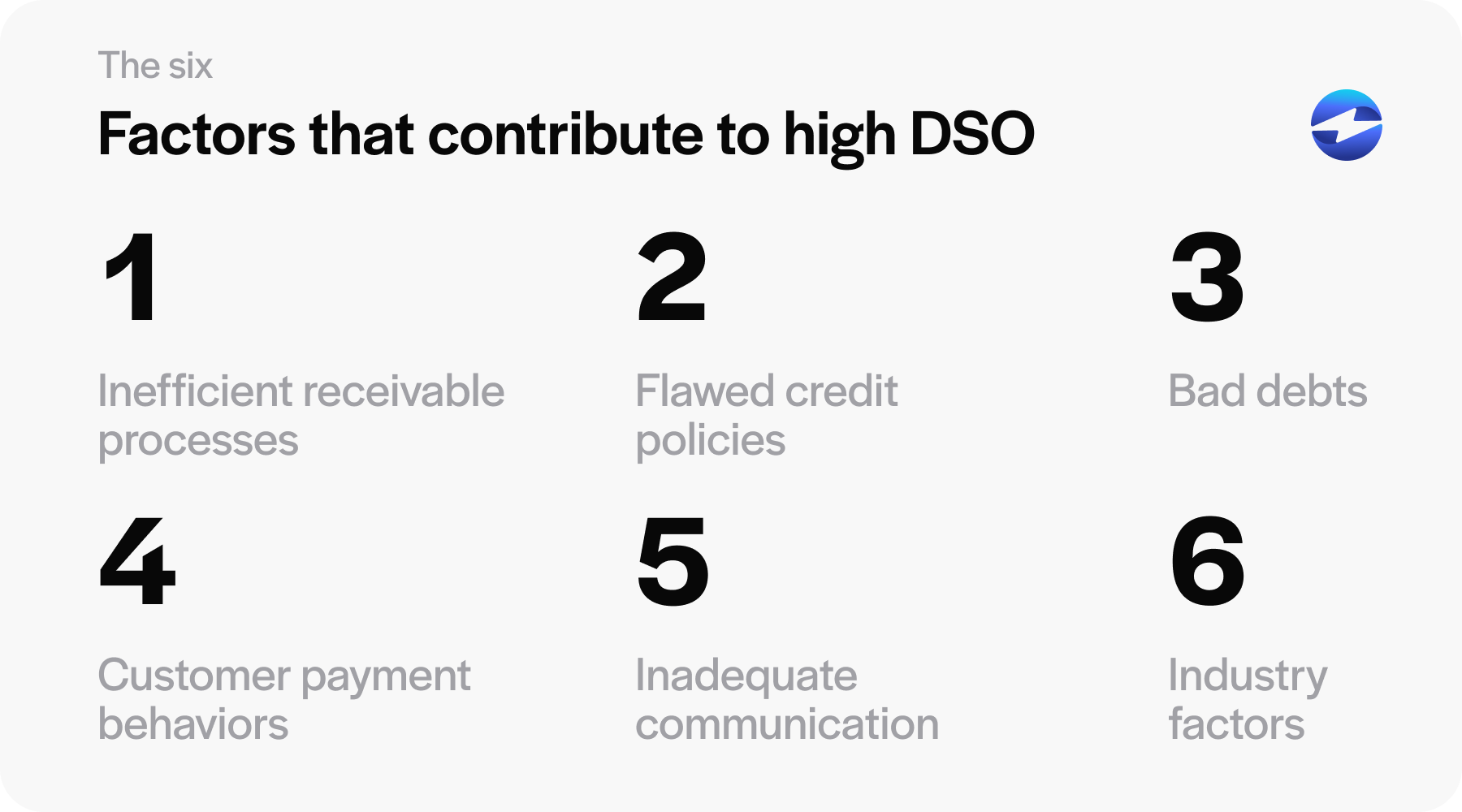

6 factors that contribute to high DSO

Before improving DSO it helps to understand what’s driving it up in the first place. Six common contributing factors include:

- Inefficient receivable processes. Poorly managed invoicing systems and collection strategies delay payment receipts and extend the collection cycle.

- Flawed credit policies. Offering credit terms that are too lenient or misaligned with industry standards results in longer collection periods.

- Customer payment behaviors. Customers experiencing financial difficulties or habitual late payers directly impact DSO regardless of how efficient your internal processes are.

- Bad debts. A high volume of unpaid invoices extends the time it takes to convert sales into cash and inflates DSO figures.

- Inadequate communication. Insufficient follow-up with customers about payment terms and expectations causes confusion and delays that compound over time.

- Economic and industry factors. External conditions like economic downturns or sector-specific payment practices can push DSO higher across the board.

Identifying which of these factors is driving your DSO is the first step toward addressing it effectively.

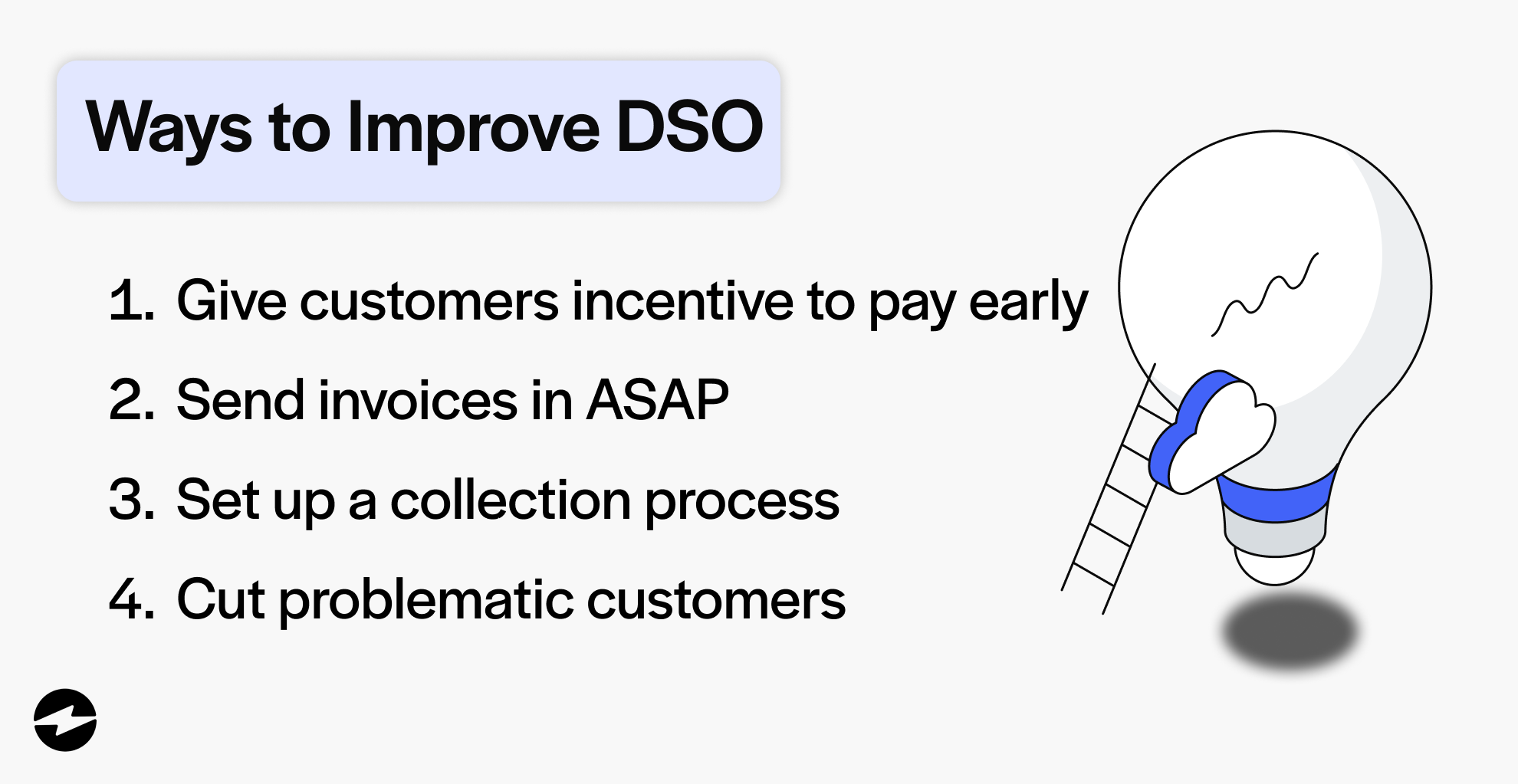

How to improve DSO for your company

Knowing how to calculate your days sales outstanding is the first step to reducing it.

Here are four ways you can improve DSO for your company:

- Give customers an incentive to pay early

- Send invoices ASAP

- Set up a collection process

- Cut problematic customers

- Improve your overall cash flow

1. Give Customers an Incentive to Pay Early

One way to simultaneously improve your cash flow and DSO is to incentivize your customers to pay early.

For example, offer a 2% discount for making payment within 10 days. Other incentives include gift cards, merchandise, and discounts on future orders.

It’s important to ensure these incentives are mentioned on the invoice to entice customers to take advantage of them.

2. Send invoices ASAP

Sending invoices in a timely manner is essential to promote on-time or early payments. To help with this, you can include incentives with your invoices and auto reminders to improve collection times. Businesses can automate invoices to this process for more streamlined payment collections. Accounts receivable automation handles this automatically, sending invoices the moment an order is placed and following up with payment reminders on a set schedule. It connects with over 100 ERP, CRM, and accounting integrations, so everything flows into your existing system without extra data entry.

3. Set up a collection process

Setting up an efficient collection process is a last-step measure to ensure you collect on missed or late payments.

Companies can create a customer support team that calls customers to collect these payments or work with a third party that handles overdue invoice collection.

4. Cut problematic customers

If specific customers are considered problematic because they continue to fail to pay on time, you may need to cut ties.

Dissolving a customer relationship may be challenging, especially if you’ve worked with them for a long time. In this case, you can discuss these invoice issues with them before taking these measures.

Reducing DSO directly strengthens cash flow, but there are additional steps worth taking alongside it:

5. Improve your overall cash flow

Reducing DSO directly strengthens cash flow, but there are additional steps worth taking alongside it:

- Review your accounts payable terms. Rather than paying bills immediately upon receipt, wait until the deadline. Some vendors may also be willing to negotiate longer payment terms, giving you more flexibility between outflows.

- Reduce unnecessary spending. Review expenses carefully and cut anything that isn’t essential. Freeing up cash on the cost side complements faster collections on the revenue side.

Managing DSO

A healthy flow of funds will keep your business in operation and help you avoid becoming one of the 82% of small businesses that fail due to poor cash flow. Understanding and actively managing your DSO gives you a clear window into your collections efficiency, your customers’ financial health, and your business’s ability to sustain growth over time.

By calculating DSO regularly, identifying the factors driving it up, and implementing the right improvement strategies, businesses can convert credit sales into cash faster, reduce reliance on debt, and make more informed financial decisions. Reducing DSO is one of the most direct levers you can pull, but pairing it with smarter accounts payable management and disciplined spending puts your cash flow in the strongest possible position.