Blog > How Long Do ACH Transfers Take? Everything you need to know

How Long Do ACH Transfers Take? Everything you need to know

In today’s fast-paced environment, money moves quickly, and the speed of transactions needs to keep up. Luckily, payment methods like ACH transfers provide a rapid and efficient process for businesses to make purchases and get paid in a timely manner.

Although ACH bank transfers are gaining popularity, you may still wonder how long ACH transfers take. This article will clarify this process by explaining what they are, their benefits, the general time frame, and any outliers that can affect the standard duration.

What are ACH transfers?

An ACH transfer is the method of digitally transferring funds between bank accounts — no physical checks or cash are involved in these transfers. ACH transfers are processed through the Automated Clearing House network to help manage these transactions and ensure they’re secure and reliable.

The ACH network is a digital payment system primarily used in the U.S. that processes various transfers between bank accounts and credit unions in a secure, efficient, and cost-effective manner. The Federal Reserve also plays a role in managing security and efficiency among these transactions.

Furthermore, there are two main categories of these electronic transfers: ACH credit and ACH debit. These two transfers share similarities, but they differ in features and functionality.

ACH credit vs. ACH debit

ACH debit transfers, or pull payments, involve withdrawing funds from one bank account and pulling them into another — the sender initiates this transfer and requests funds to withdraw from the recipient’s account. ACH debit transfers are typically used for recurring payments such as subscriptions and general bills.

Whereas ACH credit transfers, or push payments, involve pushing the funds from one bank account into the recipient’s bank account. ACH credit transfers are typically used for depositing funds such as payroll, tax refunds, and other government benefits.

Now that you clearly understand what ACH transfers are, you can learn more about the transfer times associated with these transactions.

How long does an ACH transfer take?

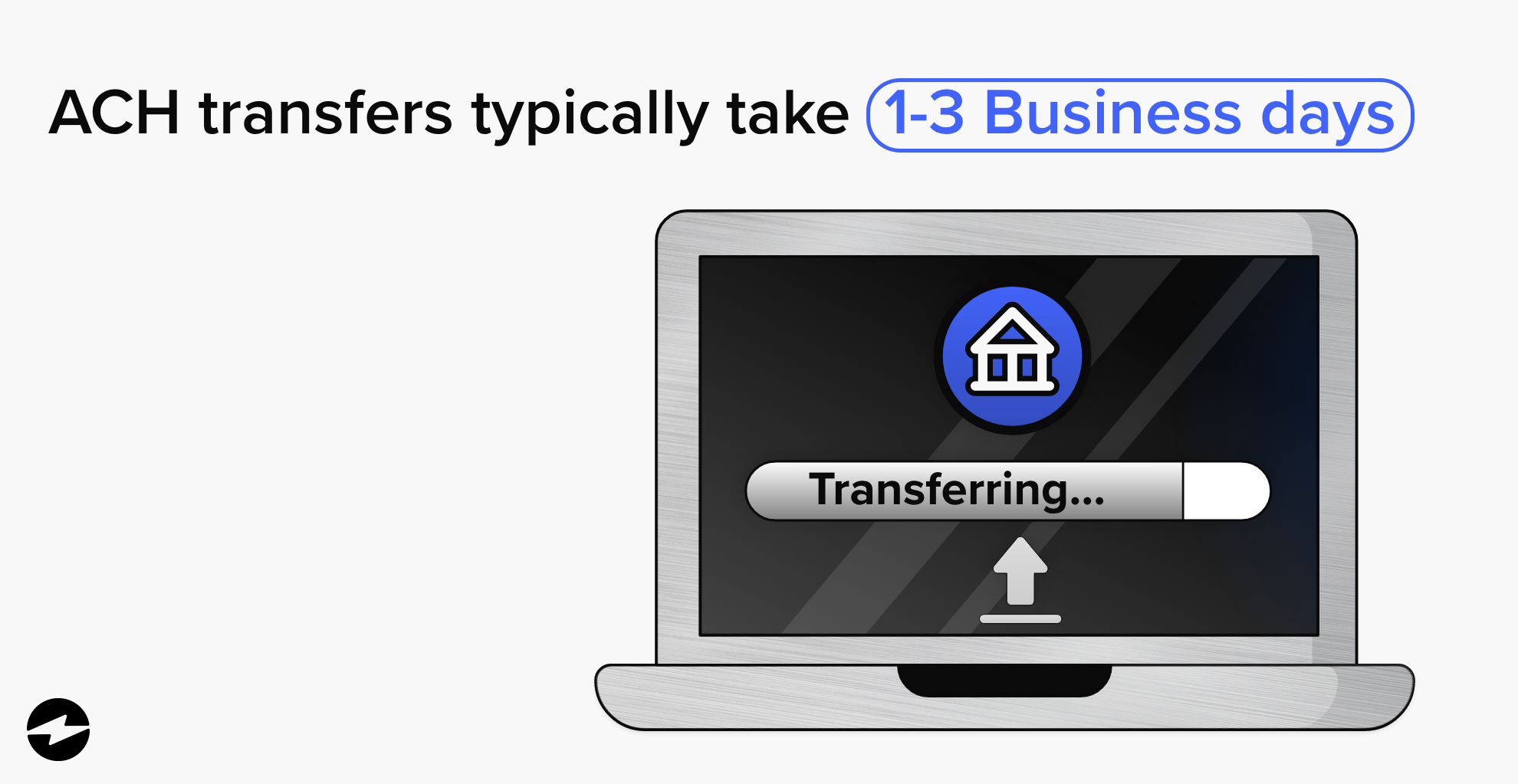

While ACH clearing times can vary, these transactions typically take one to three business days to complete. In some cases, ACH transfers can be processed on the same day if the transfer is initiated earlier in the day, and both banks involved can process it quickly.

The average ACH transfer time frame depends on a couple of factors such as the transfer type (eCheck, direct deposit) and the banks involved. Additionally, larger transfers may require additional verification, potentially extending the processing time.

The average ACH transfer time frame depends on a couple of factors such as the transfer type (eCheck, direct deposit) and the banks involved. Additionally, larger transfers may require additional verification, potentially extending the processing time.

What are the cut-off times for ACH payments?

The ACH network processes transactions at specific times throughout the day, 6 a.m., 12 p.m., 4 p.m., 5:30 p.m., and 10 p.m. Eastern Time (E.T). ACH transactions are transmitted in accordance with these schedules and the recipient bank’s rules. Any transactions filed after the final cut-off time (usually 10 p.m. ET) will be processed the next business day. ACH transactions are not completed on weekends or holidays.

What time do ACH deposits post?

ACH deposit times vary based on the kind of transaction. Standard ACH credit transaction posting timeframes can start as early as 8:30 a.m. the next day. However, ACH debit transactions typically take one to three business days to process and post.

All these factors can significantly influence how long ACH transfers take, so it’s important to be aware of them. It’s also beneficial to familiarize yourself with the steps behind the transfer process to make more informed decisions about payment methods for different transactions.

What is the process behind ACH transfers?

Now that you know the general ACH timeline, it’s time to look at the process behind these transactions. The process is relatively straightforward. Here’s a quick breakdown to help you understand how it all works:

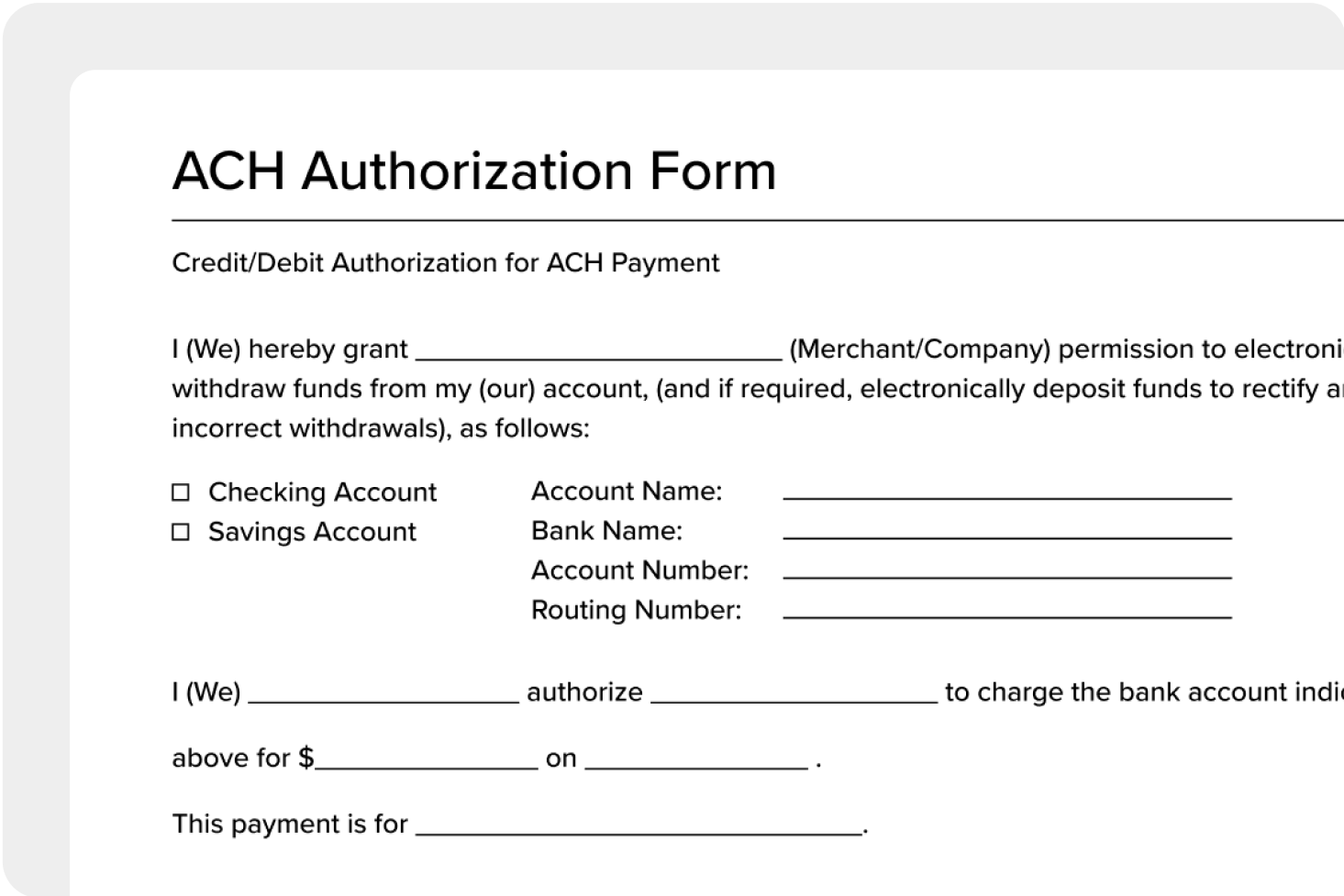

- Authorization: The individual or organization that wants to transfer money initiates the transaction by providing their bank with the necessary information, such as the recipient’s name, account number, and routing number. This is typically done using an ACH authorization form, which grants permission to a financial institution to debit or credit an individual or business account, allowing for the transfer of funds between bank accounts.

- Verification: The bank verifies the provided information and confirms the sender has enough funds to cover the transfer. If everything checks out, the bank sends the transfer request to the ACH network.

- ACH network: The ACH network is a batch-processing system that clears and settles electronic payments between banks. The transfer request is sent to the recipient’s bank through this network.

- Receiving bank: The recipient’s bank receives the transfer request and credits the recipient’s account with the funds. The transfer is considered complete at this point.

- Settlement: Finally, the banks involved in the transfer settle the transaction through the ACH network. The ACH deposit time is about one to three business days, during which the transfer is considered pending.

Each of these steps can be subject to discrepancy for various reasons including incorrect information or business holidays, all of which can affect the ACH time frame.

In other words, while one step may be completed without a problem, a problem could potentially arise in another step, extending the ACH deposit time. In order to ensure a speedy and seamless transaction, be sure to verify that all information is correct and that there will be no time conflicts.

4 benefits of ACH transfers

Whether you’re paying bills or processing payroll, ACH transfers are a valuable tool that provides a seamless payment process to give you peace of mind knowing your funds will get to where they need to go.

While there are numerous benefits of ACH transactions, here are four main advantages of using these payments:

- Speed of transfers

- Ease of use

- Automated payments

- Enhanced payment security

1. Speed of transfers

While ACH transfers aren’t the fastest option for transferring funds, they’re still quicker than traditional paper checks and provide a convenient and cost-effective way to move money between accounts.

As mentioned, same-day ACH transfers are an option for some instances. Although average ACH clearing times can be up to three business days, the ACH network offers same-day processing on select transactions, including credit and debit transactions. It’s important to note these transfers have cut-off times that can vary depending on the financial institution handling the transfer.

2. Ease of use

ACH transfers generally offer a user-friendly method of transferring funds. The ability to be initiated online via a mobile app or even over the phone also makes them accessible to both businesses and individuals.

Automating these transfers to be issued as recurring payments also simplifies the process of scheduling future payments.

3. Automated payments

Automated ACH payments can eliminate the need to manually initiate each transaction, saving you time by streamlining the payment process and allowing you to avoid any late fees, penalties, or other consequences of missed payments.

Manual electronic payments require manual data entry, increasing the likelihood of human error. For example, a person may input an incorrect routing or account number, resulting in funds being transferred to the wrong account or being rejected.

Therefore, automation gives businesses and individuals the flexibility to easily change or cancel a recurring payment at any time if their needs or circumstances change.

4. Enhanced payment security

Electronic transfers offer a secure way to pay since they require the sender and recipient to have valid bank accounts verified before the transaction is authorized.

These transactions are highly regulated by both the ACH network and federal law.

ACH transfers use many cybersecurity measures to help protect them against hackers and unauthorized users. Some of these security measures include:

- Secure Sockets Layer (SSL): SSL is designed to provide secure online communication. When active, data transmitted between web servers and clients is secured and protected from interception by unauthorized parties. This encryption is commonly used to protect passwords, credit card numbers, and other personal information transmitted electronically.

- Multi-factor authentication (MFA): MFA requires users to provide two or more forms of authentication to verify their identity and grant them access to a device or service.

- Risk management: Risk management systems identify, assess, and mitigate organizational or individual risks.

- Data encryption: Encryption converts plain text or other forms of data into a coded or encrypted format that can only be read by authorized parties with access to the encryption key.

- Firewalls: Firewalls are security systems designed to monitor and control incoming and outgoing network traffic between a computer or network and the internet.

Although ACH transfers have numerous benefits and levels of protection that make them a secure and efficient tool, these transactions have some limitations.

Do ACH transfers have any limitations?

Despite the many benefits of ACH transfers, there are a few disadvantages associated with these payments, such as slow ACH transaction times, lack of availability, and more.

While ACH transactions are typically faster than traditional methods like paper checks, there are more efficient methods of transferring funds. These transactions are also used primarily in the U.S., so they may not be available for international transactions.

ACH transactions carry transfer limits for dollar amounts.

ACH transaction limits refer to the maximum amount of money that can be spent or received via ACH transfers within a specific time frame, typically per day. These limitations are set by banks and designed to protect against fraud and other financial risks. Each financial institution sets its own transfer limits based on internal policies and procedures, so check with your bank to determine your limit.

It’s important to note that these limits are separate from the overall account balance or credit limit, as they only apply to ACH transfers specifically.

Finding suitable payment methods for your business

Now that you know how ACH transactions are processed and ACH time frame involved, your business can determine if these payments are the right fit and the best plan of action to process them efficiently.

For the most efficient ACH processing, finding a reliable financial institution, verifying all your information before sending, and monitoring your transfer are essential. You can also look into reliable payment providers like EBizCharge that process ACH payments and more to streamline the AR process.

Businesses that rely on ERP systems like NetSuite or Sage can further streamline ACH processing by connecting their payments directly to their existing workflows. With NetSuite payment processing, transactions are automatically recorded and reconciled within your ERP, while a Sage payment integration keeps your payment data synced across your accounting system in real time. Both options help reduce manual entry and give your finance team full visibility into the status of every ACH transfer.

Frequently Asked Questions

What is an ACH transfer?

An ACH transfer is the method of digitally transferring funds between bank accounts — no physical checks or cash are involved in these transfers. ACH transfers are processed through the Automated Clearing House network to help manage these transactions and ensure they’re secure and reliable.

The ACH network is a digital payment system primarily used in the U.S. that processes various transfers between bank accounts and credit unions in a secure, efficient, and cost-effective manner. The Federal Reserve also plays a role in managing security and efficiency among these transactions.

What does reached ACH period limit mean?

“Reached ACH period limit” happens when a bank or financial institution limits the number or amount of ACH (Automated Clearing House) transactions an account holder can initiate within a specific period. If the user exceeds the limit, they may only be able to initiate further ACH transactions once the next period begins. These limits are established for security reasons and to prevent fraud or misuse of the account. If required, users may contact their bank to request an increase in their ACH transaction limit or explore alternative payment options.

Are ACH transfers instant?

No, ACH transfers are typically not instantaneous. These electronic payments can take from a few hours up to three business days to process, depending on the type of transaction:

- ACH debits (like bill payments or withdrawals) generally take 1–3 days to complete.

- ACH credits (such as direct deposits or vendor payments) usually process within a day.

Some financial institutions offer the option to expedite ACH transactions for an additional fee.