Growth is crucial to the success of any business but it can also be very challenging to manage if the necessary protocols and software tools aren’t implemented properly.

Luckily, merchants that experience growth in the form of high-ticket sales and large volume transactions on a monthly basis can work with a reliable payment processor to set up a high-volume merchant account to better manage these payments.

What is a high-volume merchant account?

High-volume merchant accounts are merchant accounts tailored to support businesses with significant credit card transaction volumes that exceed monthly standards.

Merchants that have access to a high-volume merchant account have the ability to meet the demand of rapid expansion while simultaneously maintaining their day-to-day operations. This is due to these merchant accounts being designed to process high-volume transactions and large-ticket items without any complications.

Without a high-volume merchant account, businesses with high volume sales can be flagged for unusual activity, receive amount limits from their provider, or have their funds held.

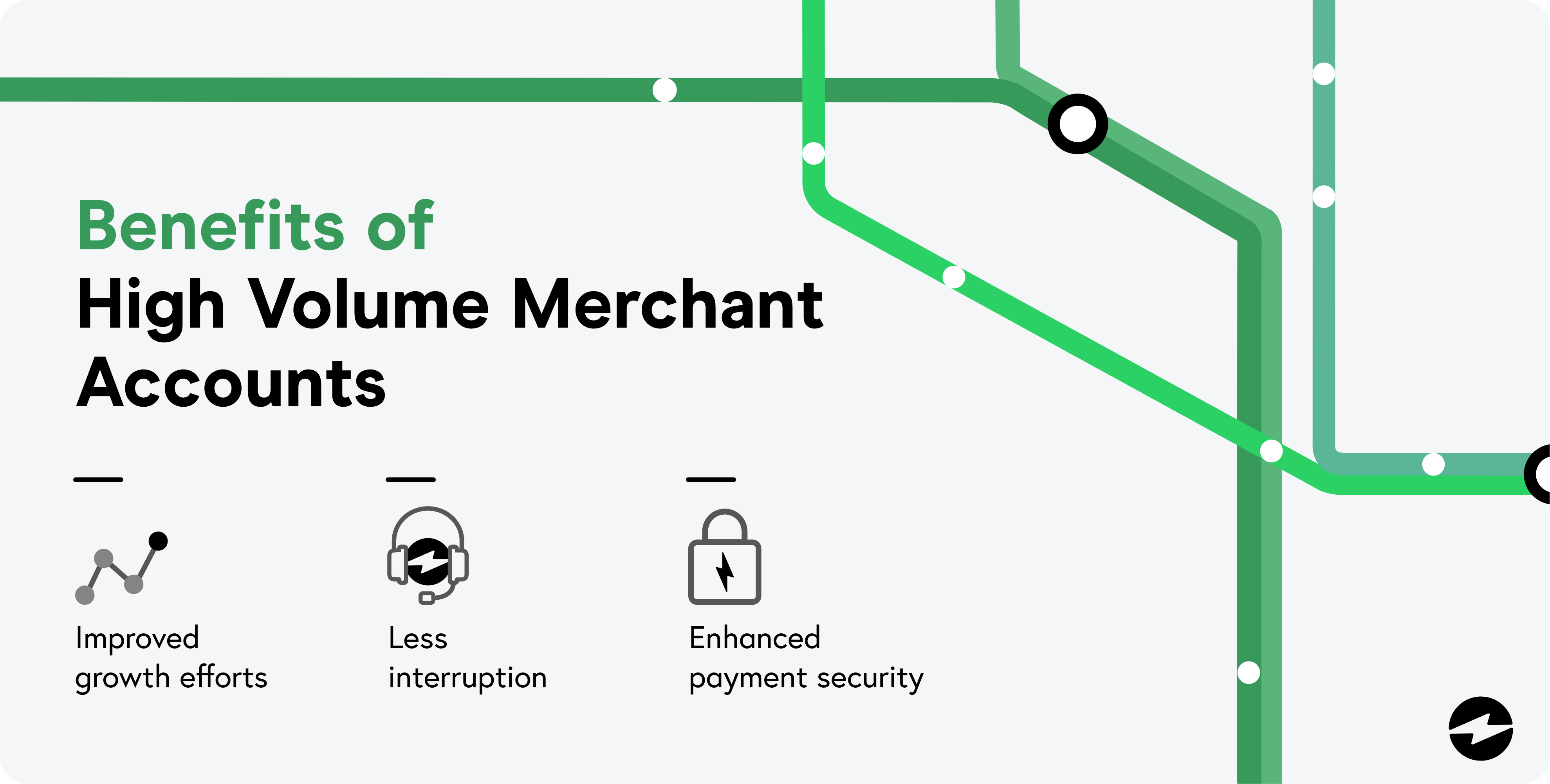

Benefits

High-volume merchant accounts can yield a wide variety of benefits for businesses that include:

- Improved growth efforts: Merchants that take advantage of high-volume merchant accounts can seamlessly accept a high volume of transactions and large amounts at a rapid pace, thus encouraging more growth and profits.

- Less interruption: High-volume merchant accounts eliminate any roadblocks that halt or hinder the transaction process, allowing businesses to accept and process payments without any interruptions.

- Enhanced payment security: Due to the nature of large purchases and high-volume tickets, merchants benefit from high-volume merchant accounts because they provide the necessary security software and protocols to mitigate fraud and other threats.

Despite the benefits of high-volume merchant accounts, there are also some drawbacks that can occur if these accounts aren’t properly managed.

Disadvantages

Some disadvantages that can result from high-volume merchant accounts include:

- Greater risk of fraud: Due to the influx of transactions and handling of high-priced items, high-volume merchant accounts may be subject to more fraud. These threats and businesses in riskier industries can lead to accounts being labeled as high risk.

- Increased chargebacks: Similar to fraud, larger transaction volumes often result in an increase in chargebacks. Both legitimate and fraudulent chargebacks can lead to greater revenue losses for your business.

- Higher fees: Payment processors may charge higher fees for high-volume merchant accounts since they’re processing large numbers of transactions on a monthly basis.

- Delayed approval process: High-volume merchant accounts that substantially exceed monthly transaction volume limits may experience a delayed approval process for funds.

Before applying for a high-volume merchant account, businesses should thoroughly assess the benefits and disadvantages associated with these accounts.

What qualifies as high-volume processing?

Even if your business processes many transactions or high-value tickets, this doesn’t necessarily mean you’ll qualify for a high-volume merchant account.

To qualify as a high-volume business, you’ll need to process credit card payments that amount to a minimum of $100,000 in monthly sales.

If your business meets this requirement, you can apply for a high-volume merchant account by submitting an application — the same way you would apply for a standard processing account — and providing additional documentation which may include:

- Valid, government-issued ID (driver’s license or passport) for the account owner

- Social Security Number (SSN) or Employer Identification Number (EIN)

- Bank letter or printed voided check

- Articles of Incorporation or LLC

- Three months of most recent payment processing statements

- Three months of most recent business bank statements

- Secure, fully functioning website

- Proof of low chargeback ratios (below 2%)

The underwriting team will review your application, supportive documents, and your business as a whole, to see if it’s the right fit. The approval process for high-volume merchants usually takes 1-3 days, with the exception of high-risk companies which can range between 3-5 days.

What types of businesses need a high-volume merchant account?

In addition to companies that receive large quantities of monthly credit card transactions, there are specific businesses that may require a high-volume merchant account.

Some business models that may need high-volume merchant accounts include:

- Companies with recurring monthly or annual service fees

- Subscription-based companies that offer monthly products or services

- Property management companies that process monthly rental payments

- Companies with recurring monthly or annual membership fees

Other common industries in which businesses may require high-volume merchant accounts include vehicle sales, travel, high-end retailers, credit repair, debt collection, eCommerce, etc.

You may notice similarities in businesses and industries when it comes to high-volume merchant accounts and high-risk merchant accounts, they are not the same account models.

High-volume merchant account vs. high-risk merchant account

While there is overlap between high-volume merchant accounts and high-risk merchant accounts, there are critical differences between these two accounts.

High-risk merchant accounts are dedicated to businesses with bad credit history, high chargeback ratios, and greater fraud risks. Merchants can also be categorized as high-risk if they process a lot of international payments (I.e. offshore high-risk merchant accounts) or are a new business with no proven track record of sales or trustworthiness.

Industries that are commonly known to be at higher risk than others include CBD/marijuana products, firearms and ammo, adult products and/or services, gambling, online dating, cigarettes/vape shops, debt collection, and many more.

Whereas, high-volume merchant accounts are applied to businesses with high-volume transactions or high-ticket products/services that equate to $100,000 or more in monthly sales.

Since high-volume merchant accounts consist of large transaction volumes and purchases, they can incur greater fraud risks involving compromised payment data and chargebacks. Due to this increase in threats, high-volume merchant accounts can also be considered high-risk.

Tips to increase high-volume transactions and merchant account limits

Most merchants share the common goal of wanting to increase their transaction volumes and sales to yield long-term success. However, businesses with high-volume transactions may run into the issue of volume limits being placed on their merchant accounts by payment processors.

Merchant account limits are typically determined by your monthly credit card processing sales and high-ticket purchases. Once this limit is reached, businesses can no longer accept credit card payments for the duration of the month which hinders growth.

While merchants can increase their account limits to handle high credit card sales volumes, it’s important to first confirm this transition is necessary — your monthly credit card processing volumes regularly exceed account caps.

After verifying your business requires a higher account limit, you can request this change when your account is nearing its limit by contacting your payment processor. Processors typically require a minimum of 3-6 months of processing history before entertaining a limit increase.

If your business meets all these requirements, you can request to increase your high-volume merchant account limit. At the time of this request, merchants should:

- Ensure their chargeback ratios are low

- Ensure their company is in good standing with its processor (all statements are paid)

- Ensure processing statements are readily available

Make sure your online reputation and overall business standing are well-maintained to promote more trust and better relations with your payment processor.

As your transaction volumes grow, having a payment solution that connects directly to your existing software becomes even more important. A QuickBooks credit card integration helps high-volume businesses automatically reconcile large numbers of transactions without manual data entry, while BigCommerce credit card processing ensures online sellers can handle surges in order volume without disrupting the checkout experience. Both options help merchants scale their operations without outgrowing their payment infrastructure.

EBizCharge provides a seamless experience for high-volume merchants

High-volume merchant accounts can be challenging for businesses to implement and maintain which is why choosing the right payment processor can make a world of difference.

Luckily, merchants can look to reliable and affordable payment processors like EBizCharge to seamlessly integrate a high-volume merchant account into their business to promote more growth.

Frequently Asked Questions

How can I apply for a high-volume merchant account?

Applying for a high-volume merchant account typically involves contacting a payment processor or a financial institution that offers merchant services. You can initiate the application process by contacting the provider of your choice. They will guide you through the necessary steps, which often include submitting business documentation, financial statements, and information about your transaction volume.

Can a business switch from a standard merchant account to a high-volume account?

Yes, businesses can generally switch from a standard merchant account to a high-volume one. However, it depends on the specific payment processors’ or financial institutions’ policies. The process typically involves contacting your current provider, expressing your need for a high-volume account, and following their account upgrades or transition guidelines.

- What is a high-volume merchant account?

- Benefits

- Disadvantages

- What qualifies as high-volume processing?

- What types of businesses need a high-volume merchant account?

- High-volume merchant account vs. high-risk merchant account

- Tips to increase high-volume transactions and merchant account limits

- EBizCharge provides a seamless experience for high-volume merchants

- Frequently Asked Questions