Blog > Understanding Accrued Expenses and When to Record Them

Understanding Accrued Expenses and When to Record Them

While simple in concept, properly accounting for accrued expenses can get complex in practice, but it is essential to create an accurate financial picture. Accrued expenses offer a better methodology to match revenues and costs within an accounting period to give a reliable view of profitability.

So, what is an accrued expense, and how can you use them to improve your financial reporting?

What are accrued expenses?

Accrued expenses represent costs incurred by a company for goods or services that have been received but have yet to be paid for. These are recorded in the company’s financial statements through adjusting entries, enabling the recognition of liabilities and expenses that still need to be received in invoice form.

Companies can better match revenues with their related expenses in the appropriate accounting period by recording accrued expenses. Accrued expenses provide a more accurate picture of the company’s profitability and financial position.

The importance of accrued expenses

Properly tracking accrued expenses enables companies to know all their outstanding liabilities. This helps ensure businesses don’t overextend themselves or take on more expenses than they can realistically afford.

A company needs visibility into unpaid vendor invoices and services to manage cash flow and prevent taking on excessive debt obligations. If a business loses track of accrued expenses, it may continue spending freely while unaware of large pending payments building up on its books. Maintaining an accurate record of accrued liabilities keeps companies financially responsible and careful not to overcommit funds.

Example of an accrued expense

Say a company called Web Design Co. completes a website design project for a client in April with net 60 payment terms. Web Design Co finishes the website after incurring $4,000 in contractor expenses and delivers it to the client on April 30. However, payment will not be made until June under the contract terms.

With accrual accounting expenses, Web Design Co. records the $5,000 as accrued revenue in April when the website was delivered, increasing accounts receivable. Web Design Co. also records $4,000 in contractor expenses to complete the website, increasing accrued expenses. This matches the revenue earned to the expenses incurred in April, even though cash has yet to be exchanged.

Accrued expenses hold many benefits to the company and are an integral part of accounting, so it’s essential to understand how they work.

How do accrued expenses work?

Despite its complexities, accruing expenses can be completed with a simple two-step accounting process.

First, when an expense is incurred but not paid, the company records an adjusting entry to debit the expense account and credit accrued liabilities. This increases expenses on the income statement and liabilities on the balance sheet.

Second, when payment is made, the company debits accrued liabilities and credits cash, reversing the original adjusting entry. This system enables businesses to capture expenses in real time when incurred rather than paid.

What are the different types of accrued expenses?

Accrued expenses are typically broken down into a few categories based on various situations. The most common types of accrued expenses include:

- Unpaid interest on loans: Interest expenses on loans that have been incurred but have yet to be paid.

- Employee compensation: Wages or salaries employees have earned but will be paid on the next payroll date.

- Unused vacation or sick days: If a company allows employees to roll over vacation or sick days, these liabilities represent a future cash outflow.

- Utilities for the month incurred: Utility expenses that have been used but not yet paid for (water, electricity, internet, etc.).

Services yet to be invoiced: These services have been used but not yet billed.

While many variations of accrued expense exist, they all typically come with similar advantages and disadvantages for businesses.

4 advantages and disadvantages of accrued expenses

When recording accrued expenses, it’s essential to understand the potential benefits and drawbacks.

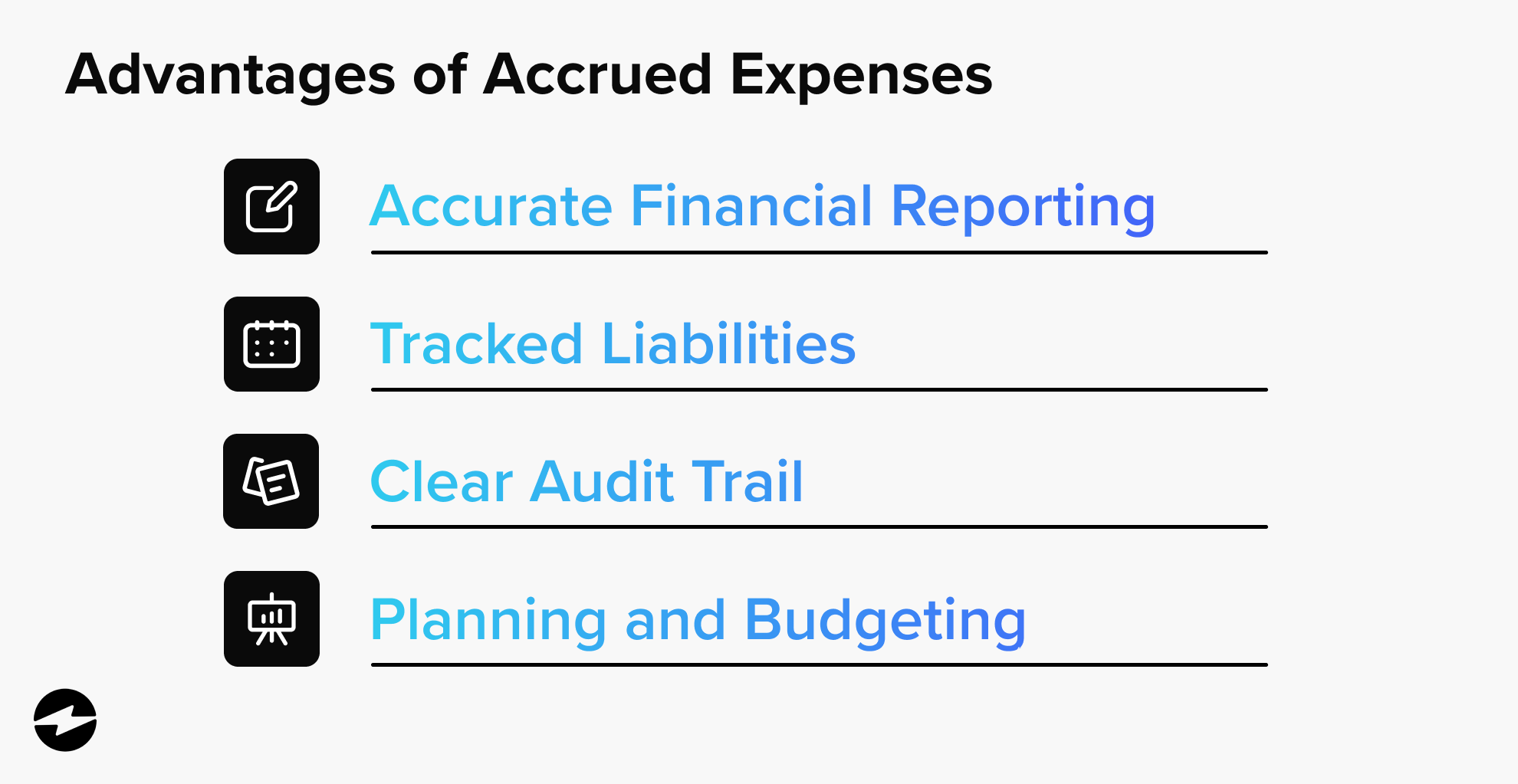

Advantages

Here are a few of the most impactful advantages of accrual basis accounting:

- Accurate financial reporting: Accrued expenses encourage better matches of revenues and expenses to show a more accurate picture of profitability in a given period.

- Tracked liabilities: Accurate expenses reflect liabilities and expenses that have been incurred but not yet billed or paid.

- Clear audit trail: Accrued expenses provide a clearer audit trail for improved financial transparency.

- Planning and budgeting: Accrued expenses enable better financial planning and budgeting when all costs are captured.

Companies should also consider any setbacks associated with accrued expenses.

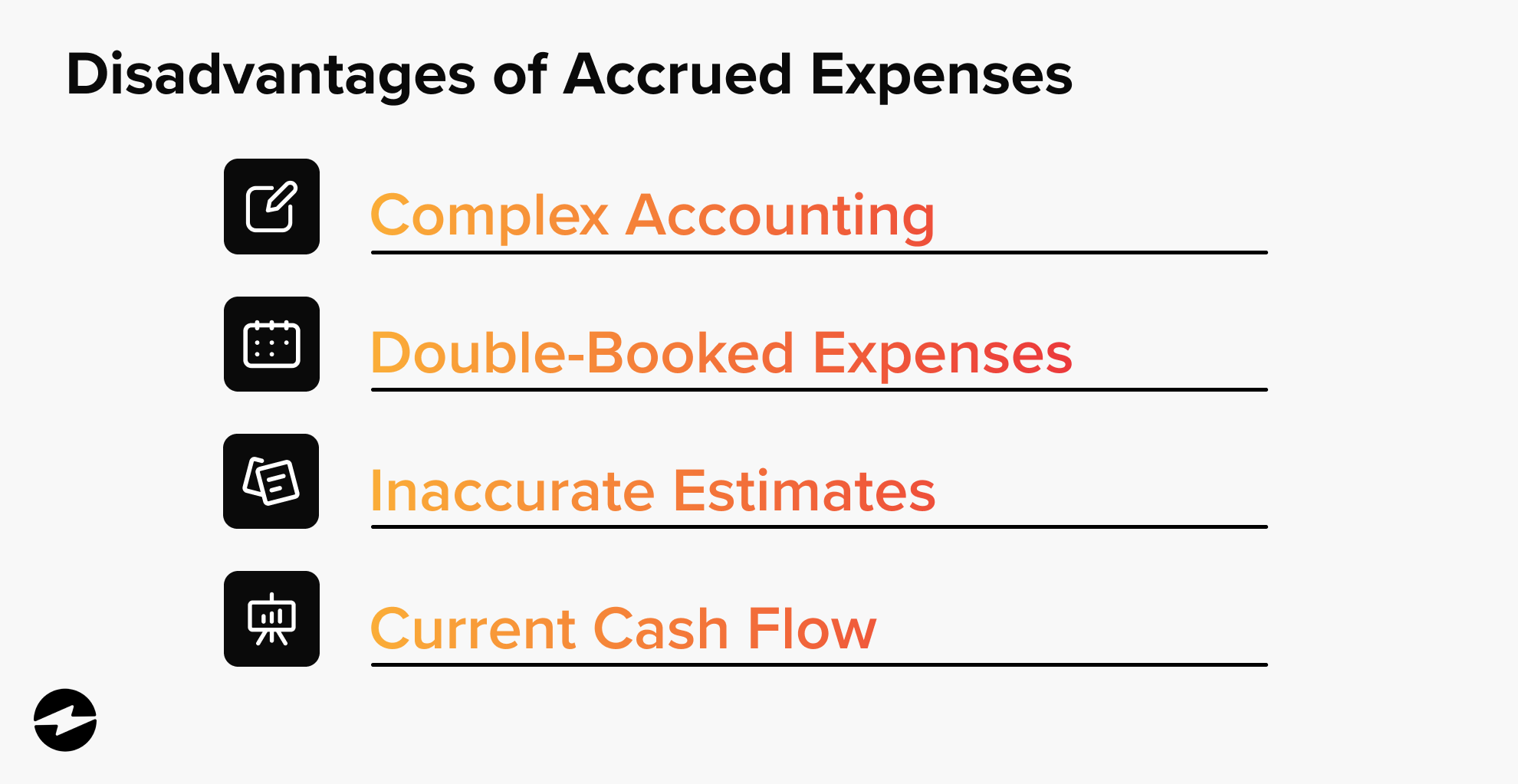

Disadvantages

Here are a few of the drawbacks of accrual basis accounting:

- Complex accounting: More complex accounting is needed to track and adjust unpaid expenses.

- Double-booked expenses: Errors can cause double-booked expenses if accruals are improperly reversed.

- Inaccurate estimates: Some accrued expenses require appraisals that need to be revised.

- Current cash flow: Relying entirely on accrual basis accounting can make determining your actual cash flow position harder.

Despite these drawbacks, roughly two-thirds of small businesses still use accrual basis accounting and, in some cases, cash basis accounting.

Accrual vs. cash basis accounting

It’s important for companies to understand the differences between cash basis accounting and accrual basis accounting.

With cash basis accounting, the moment cash exchanges hands is when revenue and expenses are recorded. So, instead of accounting for the transaction, cash basis accounting tracks when invoices are paid, and revenue is received. While simpler, this method of accounting can give a skewed view of a company’s financial health if revenues or expenses are recorded in a different period than when they were earned or incurred.

As a result of the potential for cash basis accounting to skew financial reports, the IRS requires most businesses to use accrual basis accounting. Only individuals and small businesses can use cash basis accounting unless a special exemption is granted.

Accrued expenses vs. prepaid expenses

While accrued expenses represent liabilities for expenses incurred but not yet paid, prepaid expenses are the exact opposite. They represent payments made in advance for goods or services to be received in the future. Companies receive prepaid expenses through advanced billing.

For example, if a company pays its insurance premium for the entire year in January, it records this amount as a prepaid expense. Then, each month, it transfers a portion of the prepaid expense to the expense account.

What is the journal entry for accrued expenses?

When recording an accrued expense journal entry, the company debits (increases) an expense account and credits (decreases) an accrued liabilities account. When the invoice is later received and paid, the company debits the accrued liabilities account (increasing it) and credits the expense account (decreasing it).

The manual entry of journal entries can be tedious and time-consuming for accountants. Fortunately, there is a way to automate the accrued expense journal entry aspect of accounting to lighten the load.

How to automate the accrued expense journal entry aspect of accounting

Automated accounting software can simplify the recording of accrued expenses by automatically updating expense accounts and liabilities accounts based on input accrued expenses and payments made. This technology helps accountants manage these entries, reducing the risk of errors and time spent on this task.

When it comes to accruing expenses with automation, there are four steps companies should take when doing the journal entry.

The 4 steps for accruing expenses with automated accounting software

Accounting software has simplified the accruing of expenses into a simple four-step process. Here are the four steps to create an accruing expenses journal entry with automation:

- Identify all expenses incurred during the period that have yet to be recorded.

- Make an adjusting entry in the ledger to record the accrued expenses under accounts payable.

- When the invoice is received, record the amount in the appropriate expense account and decrease the accrued liabilities account.

- When payment is made, credit the cash account and debit the accrued liabilities account.

In addition to these steps, creating accurate expense reports is vital for a company’s finances.

5 popular accounting expense reports

Creating detailed, accurate expense reports is critical to any business’s financial health. These reports can provide valuable insights into your company’s spending habits, enabling more informed decision-making and better resource allocation.

To help with this, here a five expense reports your company can use to understand and categorize its accrued expenses:

- Employee expense reports: Employee expense reports track business expenses incurred by employees, such as travel, meals, and other expenditures. These reports are essential for reimbursements and ensuring policy compliance.

- Departmental expense reports: Departmental expense reports divide expenses by department, such as marketing, sales, HR, or engineering, to help identify spending patterns and opportunities to optimize budgets.

- Vendor expense reports: Vendor expense reports track expenditures made to specific vendors and suppliers, help manage vendor relationships, and locate potential cost savings.

- Capital expenditure reports: Capital expenditure reports log high-value investments in assets like property, facilities, or equipment and analyze ROI on significant purchases.

- Advertising and marketing expense reports: Advertising and marketing expense reports track costs associated with advertising, PR, trade shows, and other marketing efforts to analyze effectiveness.

These expense reports provide valuable insights into accrued expenses and can help your company properly categorize them in its journal.

Accrued expenses transform the way businesses accept payments

Accrued expenses transform how businesses accept payments throughout the year and provide many benefits for companies.

Not only do accrued expenses improve financial transparency, but they help companies plan and budget for the future. Understanding this integral aspect of accounting puts your company ahead of the competition to promote long-term growth. EBizCharge supports that foundation with accounts receivable automation that keeps your payment records accurate and up to date, and integrates directly into your existing software so every transaction posts to the right account without manual entry.