Blog > Surcharge vs. Convenience Fee: What’s the Difference?

Surcharge vs. Convenience Fee: What’s the Difference?

Credit card surcharges and convenience fees are both ways to recover payment processing costs, but they work differently, apply in different situations, and carry different legal requirements. Using the wrong structure, or applying either fee incorrectly, creates compliance exposure that can result in fines or losing card acceptance entirely. Here’s how to tell them apart and which one fits your business.

What Is a Credit Card Surcharge?

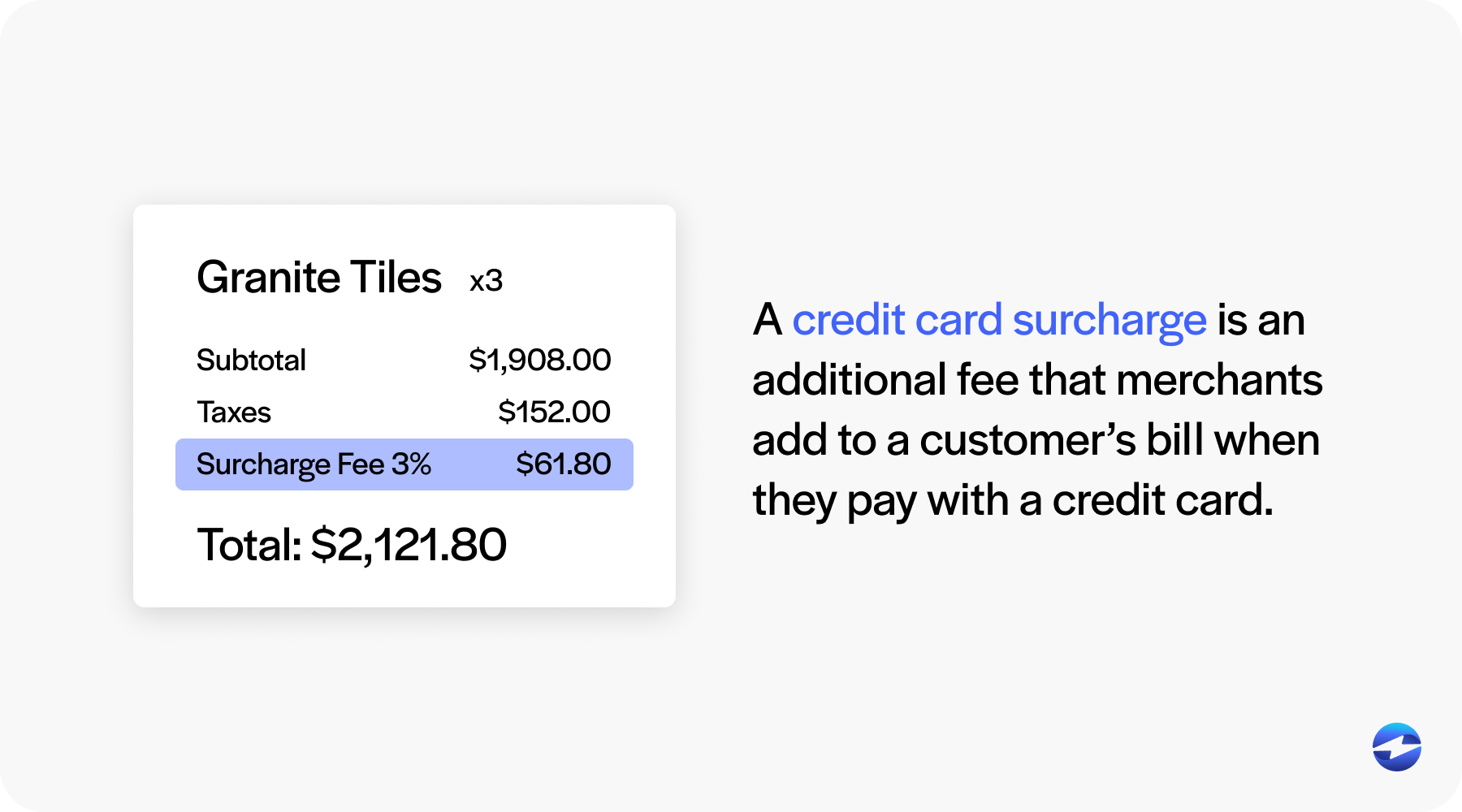

A credit card surcharge is an additional fee that merchants add to a customer’s bill when they pay with a credit card. This fee helps businesses recoup the costs of processing those transactions.

Common Use Cases:

- Frequently used in service-based industries where margins are thin.

- Popular among providers such as auto shops, travel and property managers.

- Used by merchants who want to keep prices competitive without absorbing card processing costs.

Guidelines:

- Only applies to credit cards, not debit or prepaid cards.

- Must be clearly disclosed at the point of sale and on the receipt.

- Capped at the actual cost of processing, with network-specific limits, 3% for Visa, 4% for Mastercard.

- Requires registration with Visa and Mastercard before implementation.

Visa and Mastercard require merchants to register before applying surcharges and follow strict notification and receipt disclosure rules. The surcharge amount must be listed separately on the receipt.

What Is a Convenience Fee?

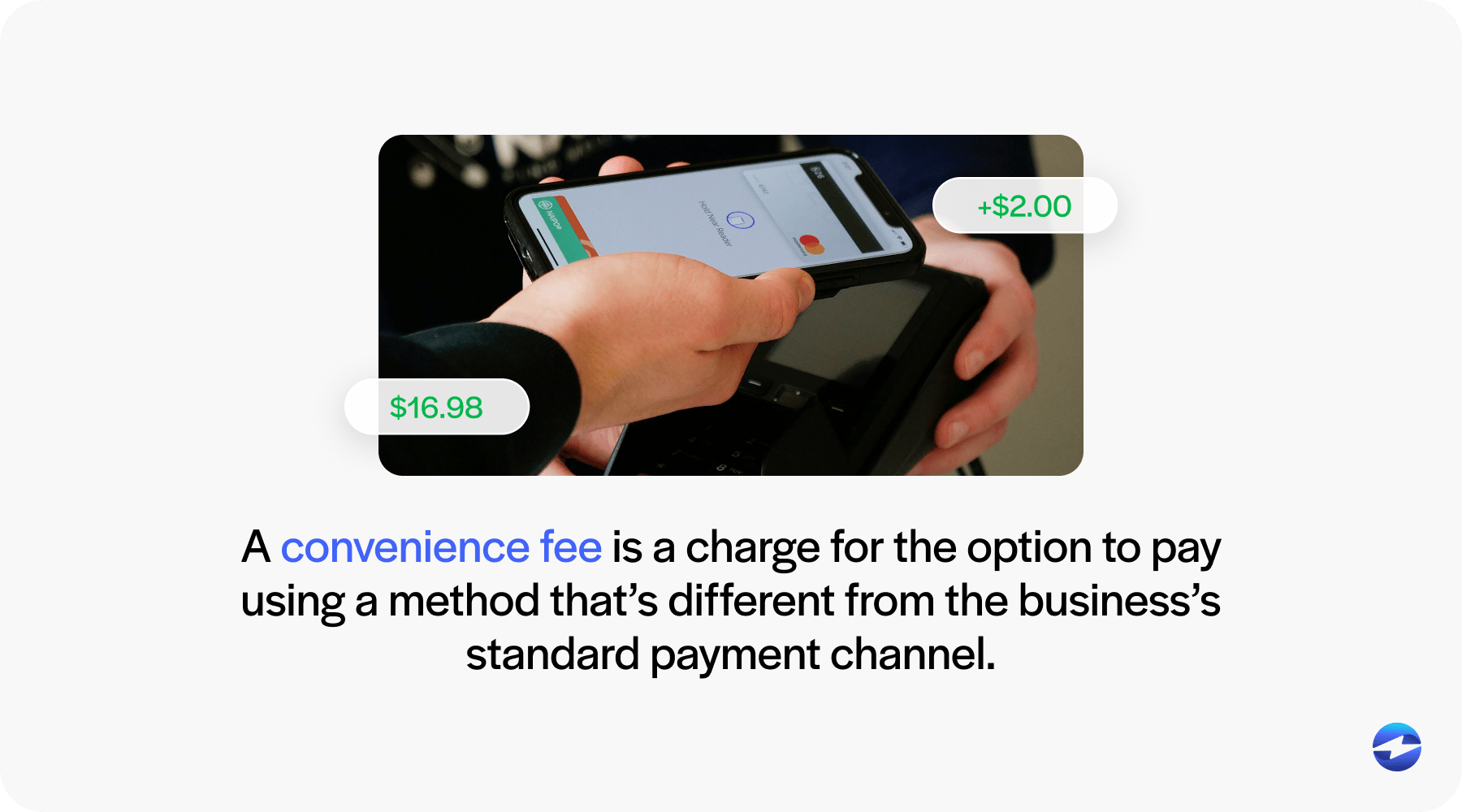

A convenience fee is a charge for the option to pay using a method that’s different from the business’s standard payment channel. For example, if a school accepts checks but allows online credit card payments, they might charge a convenience fee for the extra option.

Common Use Cases:

- Educational institutions

- Government agencies

- Utility companies

Guidelines:

- Can apply to credit or debit cards depending on the situation.

- Must be flat-fee based, not percentage-based.

- Can’t be used if the card is accepted in person (Visa rules).

- Requires advance notice to the customer.

Surcharge vs. Convenience Fee: Key Differences

Here’s a side-by-side comparison

| Feature | Surcharge | Convenience Fee |

|---|---|---|

| Applies to | Credit card only | All payment types (depends) |

| When charged | Always on card | Only when using non-standard method |

| Legal restrictions | Varies by state | Fewer but still regulated |

| Notice requirement | Yes | Yes |

| Who can charge | Most merchants | Limited types of merchants |

Real-world example: An auto body repair shop might add a 3% surcharge to invoices paid by credit card. A university might charge a $3 flat convenience fee for online tuition payments.

Are Convenience Fees Legal?

Yes, convenience fees are legal in the United States, but the rules are specific. The fee has to be a flat dollar amount, not a percentage, charged for a genuinely non-standard payment channel, and disclosed before the customer completes the transaction. Visa and Mastercard both permit them under these conditions. Most states don’t have statutes specifically restricting convenience fees the way some restrict credit card surcharges, though general consumer protection laws still apply.

Can you charge a convenience fee on a debit card?

Yes, in certain situations. Unlike surcharges, which are prohibited on debit cards entirely, a convenience fee can apply to debit transactions when the channel qualifies as non-standard, the fee is flat, and it’s applied consistently across all card types. The fee has to be tied to the channel, not the card type. Applying it to standard in-person debit transactions doesn’t meet the requirement.

Are Credit Card Surcharges Legal?

Credit card surcharges are legal in most U.S. states as of 2026, with the exception of states like Connecticut and Massachusetts, which prohibit them outright. Where permitted, merchants must register with Visa and Mastercard at least 30 days before implementing, disclose the surcharge at the point of sale and on receipts, and stay within network caps: 3% for Visa, 4% for Mastercard. Surcharges cannot be applied to debit or prepaid card transactions under any circumstances.

Consider:

Consider:

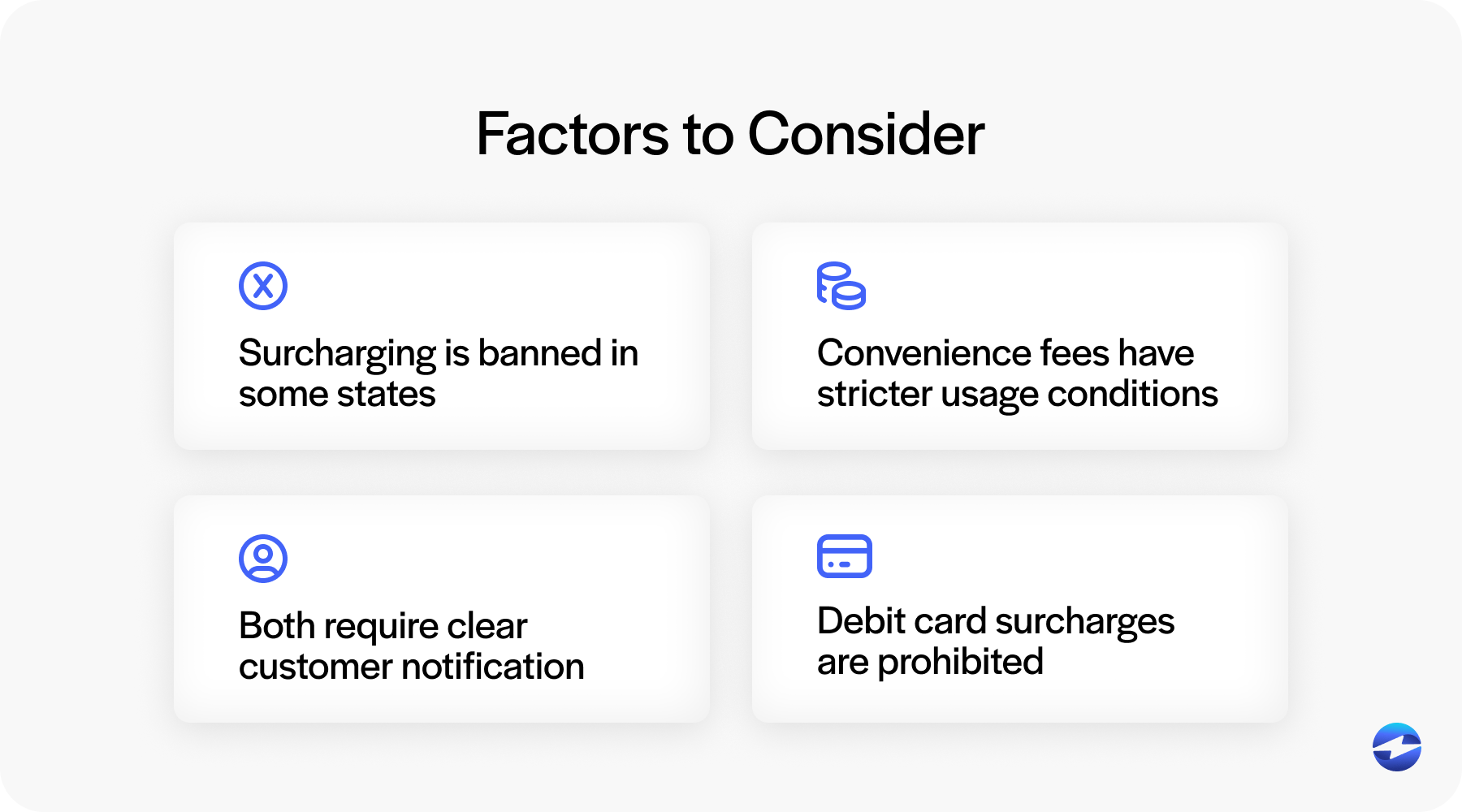

- Surcharges are banned in some states like Connecticut and Massachusetts.

- Convenience fees have fewer state restrictions but stricter usage conditions.

- Both require clear customer notification.

- Debit card surcharges are prohibited by card brand rules.

Non-compliance can result in fines, customer disputes and the loss of your ability to accept card payments.

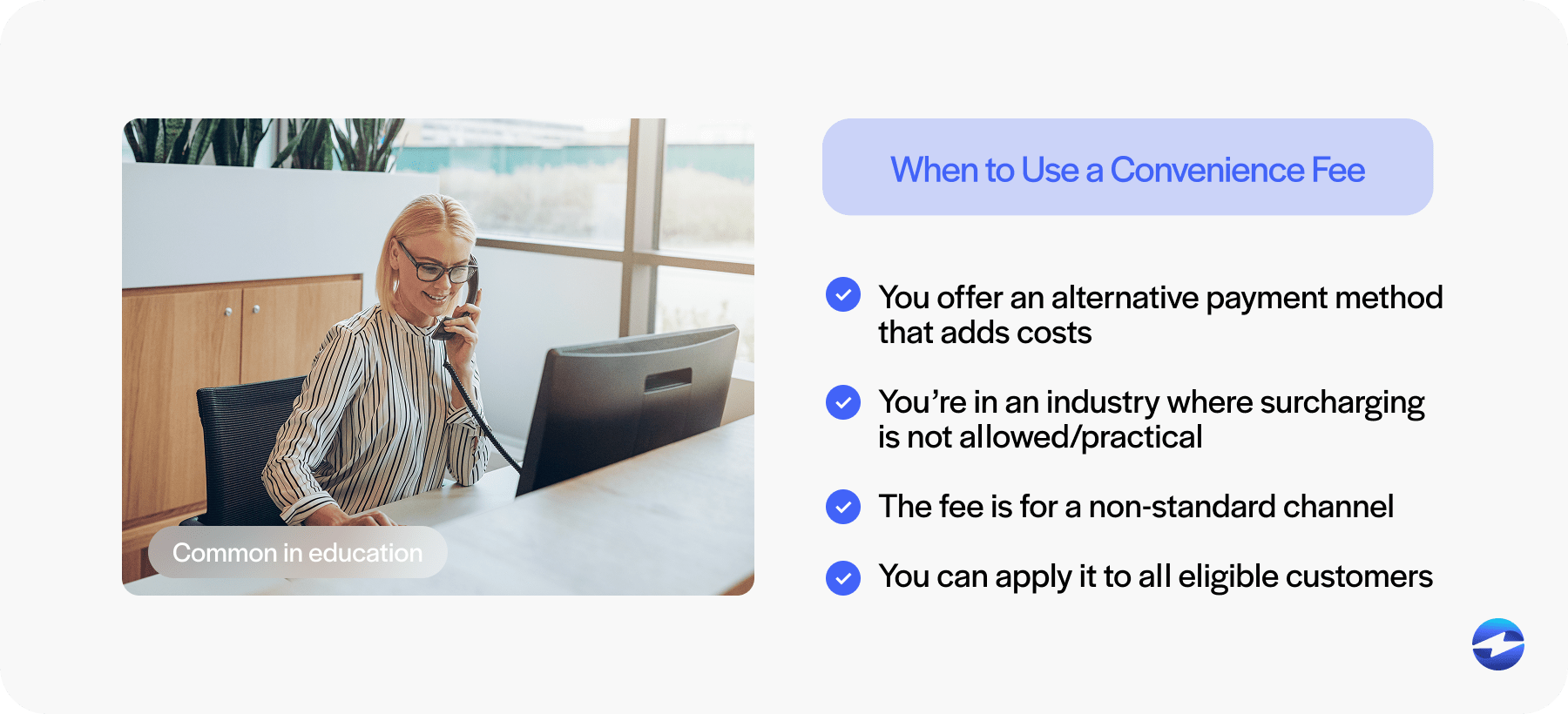

When to Use a Convenience Fee?

A convenience fee might be your best option when you’re offering customers an optional, alternate way to pay that adds costs to your business. This usually happens when businesses accept payments outside their standard or normal methods—for example, accepting online or phone payments when in-person transactions are the norm.

Convenience fees are useful for businesses in industries where surcharging is either restricted or discouraged by customer expectations. If you’re in an industry like education, government or utilities where offering flexible payment channels is key—adding a small fee can help offset those costs without surprising customers.

A convenience fee might be your best option when:

- You offer an alternative payment method that adds processing or administrative costs.

- You’re in an industry where surcharging is not allowed or practical.

- The fee is for a non-standard channel (e.g., online vs. in-person).

- You can apply it to all eligible customers.

Make sure to structure the fee according to Visa/Mastercard rules and don’t apply it to in-person payments. Always notify the customer of the fee before the transaction is completed to be transparent and avoid disputes.

When to Use a Surcharge?

A surcharge is good when your business processes a high volume of credit card transactions and you want to reduce overhead without raising prices. For many companies, especially those with thin margins, absorbing the full cost of credit card fees can eat into profits quickly.

This works well if your business is in a state where surcharging is allowed and you serve a customer base that won’t mind a transparent, well-communicated surcharge policy. Surcharging is good for professional services firms, B2B companies and other service-based businesses where large invoices or recurring payments are common.

A surcharge is good when:

- You accept credit cards and want to offset costs.

- Your business is in a state where surcharging is legal.

- You’re in a B2B or professional services industry.

- Transparency and cost savings are key.

Surcharging helps protect margins without raising prices across the board. When done correctly, it creates a fair system where customers who choose to use credit cards help cover the transaction fees.

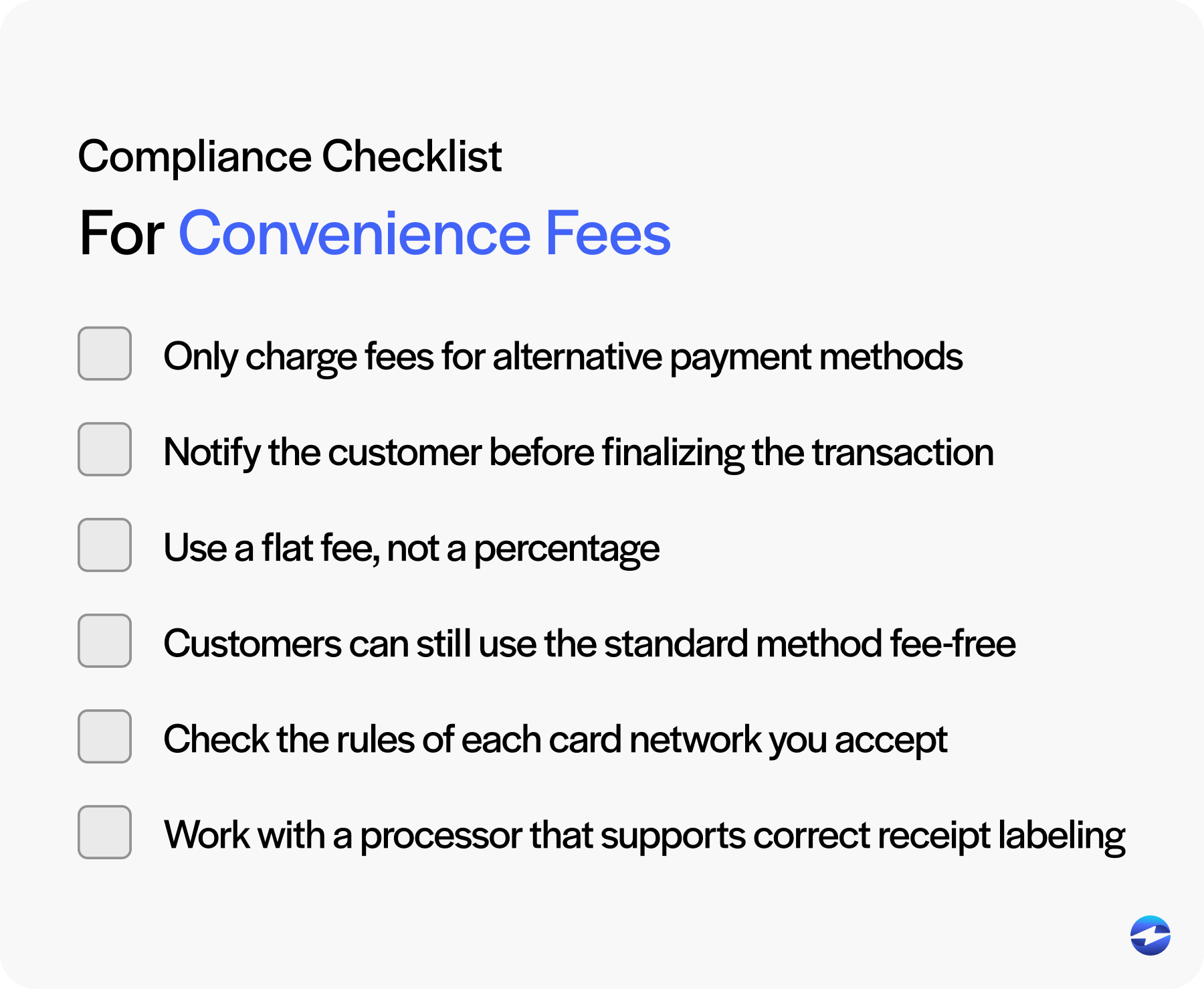

How to Legally and Effectively Charge a Convenience Fee

Charging a convenience fee requires more than just adding a line item to an invoice. It involves understanding card network rules, transparency with customers and setting up your systems to support the fee.

Convenience fees are only allowed when offering a payment method that’s different from the merchant’s normal payment channel. For example, if a business usually accepts payments in person, it can charge a convenience fee for online or phone payments. But this fee must be a flat amount—not a percentage—and disclosed before the transaction is completed.

To be compliant:

- Only charge the fee for alternative payment methods.

- Notify the customer before finalizing the transaction.

- Use a flat fee, not a percentage.

- Customers can still use the standard method fee-free.

- Check the rules of each card network you accept.

- Work with a processor that supports correct receipt labeling.

Correct implementation also means making sure your POS or payment gateway can clearly and separately show the convenience fee on the customer’s receipt. Train staff and include a clear explanation on your payment page or invoice to avoid misunderstandings and build trust with your customers.

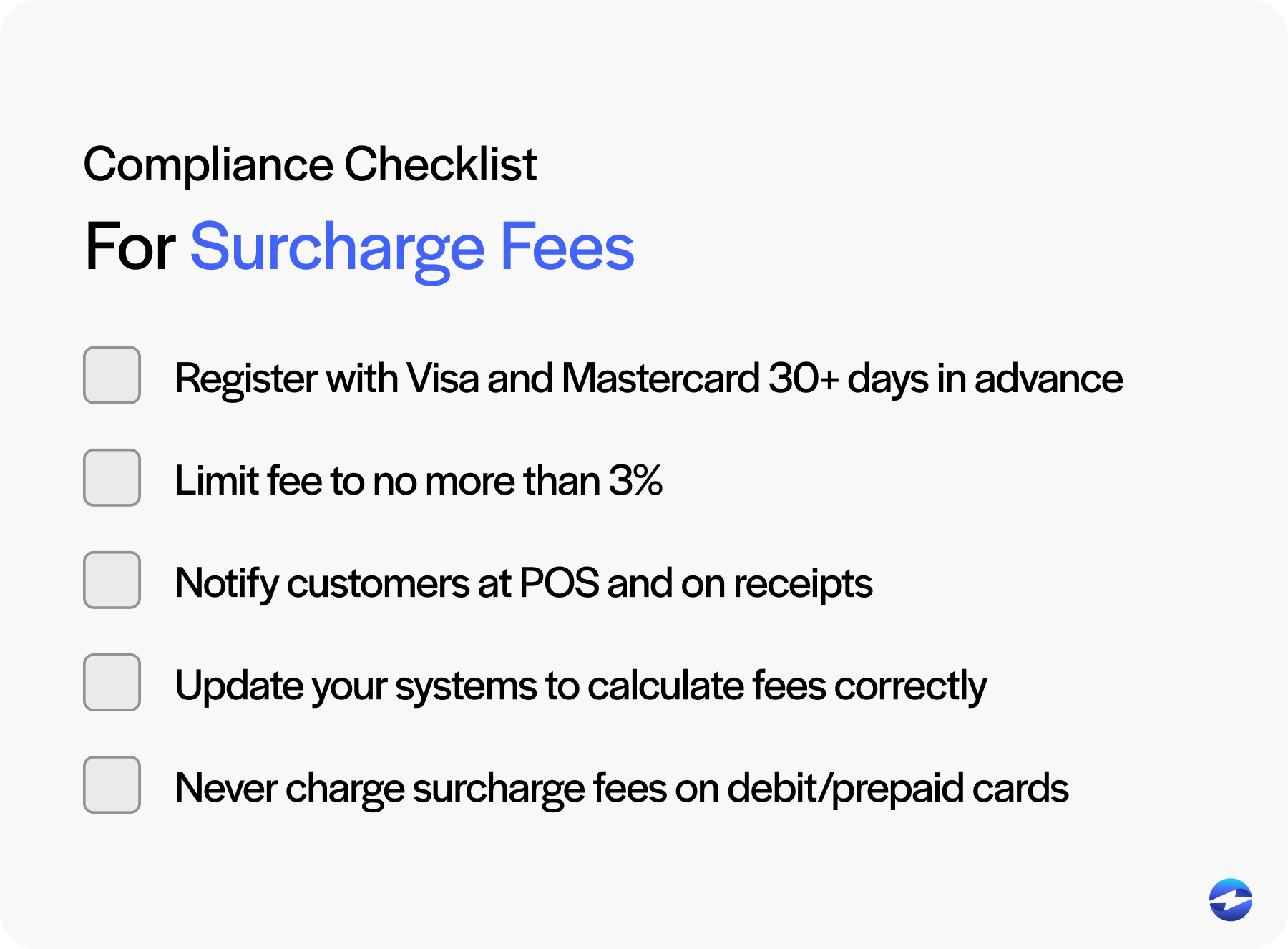

How to Legally and Effectively Charge a Surcharge Fee

Charging a surcharge fee is a straightforward process if you do it right and follow the rules. The goal is to be transparent to your customers while being fully compliant with card brand rules and state laws.

Before charging a surcharge fee, you must notify the card networks—Visa and Mastercard require at least 30 days’ notice. You’ll also need to make sure your systems can calculate and display the fee. This includes your POS system, online checkout and any invoicing platforms you use.

Notices should be at the point of entry, at the point of sale and on receipts so customers are aware of the fee before they complete the purchase. Follow these steps to charge a surcharge fee legally:

- Register with Visa and Mastercard at least 30 days in advance.

- Limit fee to no more than 3%.

- Notify customers at point of sale and on receipts.

- Update your POS, invoice or payment gateway to calculate fees correctly.

- Never charge surcharge fees on debit or prepaid cards.

Proper training for staff, good customer messaging and coordination with your payment processor will all help your convenience fee program run smoothly and legally.

How EBizCharge Makes Charging Surcharge Fees Easy

EBizCharge takes the complexity out of charging surcharge fees. Our credit card surcharge program is designed to help you charge convenience fees legally, efficiently and with minimal disruption to customer experience.

With EBizCharge you get:

- Automated fee calculation and labeling, reducing manual errors

- Built-in compliance with card brand and state regulations

- Seamless integration with top accounting, ERP and invoicing systems

- Detailed reporting and analytics to track convenience fee revenue and compliance

- Customizable settings to fit your industry and workflow

By making setup and operations easier, EBizCharge lets you pass credit card fees to customers transparently and compliantly—more revenue for your business.

Contact us today to learn how EBizCharge can support your surcharge.

Conclusion and Next Steps

Understanding the difference between a credit card surcharge and a convenience fee is crucial to making an informed decision. Each has its own rules, risks and use cases.

Evaluate your business model, industry and legal environment before you choose. And remember, whether you surcharge or charge for convenience, transparency and compliance are non-negotiable.

Need help setting up a compliant surcharge program? Contact EBizCharge to get started.

Frequently Asked Questions

What is the difference between a surcharge and a convenience fee?

A surcharge is a percentage-based fee added to credit card transactions to recover processing costs. A convenience fee is a flat fee charged for using a non-standard payment channel — such as paying online or by phone when in-person is the standard method. Surcharges apply only to credit cards. Convenience fees can apply to debit and credit cards depending on the channel and structure.

Are convenience fees legal?

Yes, convenience fees are legal in the United States under card network rules when structured correctly. The fee must be flat, not a percentage, tied to a genuinely non-standard payment channel, and disclosed before the customer completes the transaction. State-level consumer protection laws still apply, but most states do not have specific statutes restricting convenience fees the way some restrict credit card surcharges.

Are convenience fees legal on debit cards?

Yes, in certain situations. A convenience fee can apply to debit card transactions when the payment channel qualifies as non-standard, the fee is a flat amount, and it’s applied consistently across all card types using that channel. This is different from surcharges, which are prohibited on debit cards entirely. Merchants cannot use a convenience fee as a workaround to charge debit card customers more at the point of sale.

Why are convenience fees legal if surcharges are banned in some states?

Convenience fees and surcharges are treated differently under both state law and card network rules. Surcharge bans in states like Connecticut and Massachusetts specifically target percentage-based fees added to credit card transactions. Convenience fees, which are flat and tied to a payment channel rather than a card type, fall into a different legal category. That said, convenience fees are not unregulated — disclosure requirements and channel restrictions still apply.

What is the surcharge cap?

The cap depends on the card network. Visa limits surcharges to 3% of the transaction or the actual cost of processing, whichever is lower. Mastercard’s cap is 4%. Merchants must also stay within the actual cost of processing, so if your effective rate is 2%, you cannot surcharge 3%. The fee must be disclosed separately on the receipt.

Can I charge both a convenience fee and a surcharge?

No. Card network rules prohibit applying both a surcharge and a convenience fee to the same transaction. You need to choose one model and apply it consistently.

What happens if I charge a convenience fee incorrectly?

Card networks can flag the merchant account, issue fines, or in repeated cases terminate the ability to accept card payments. In states with active consumer protection enforcement, incorrect fees can also trigger complaints to the attorney general or civil action. The most common mistake is applying a convenience fee to in-person transactions or structuring it as a percentage rather than a flat amount.

- What Is a Credit Card Surcharge?

- What Is a Convenience Fee?

- Surcharge vs. Convenience Fee: Key Differences

- Are Convenience Fees Legal?

- Are Credit Card Surcharges Legal?

- How to Legally and Effectively Charge a Convenience Fee

- How to Legally and Effectively Charge a Surcharge Fee

- How EBizCharge Makes Charging Surcharge Fees Easy

- Frequently Asked Questions