Blog > What Is a Cash Discount Program? Definition, Examples & How It Works

What Is a Cash Discount Program? Definition, Examples & How It Works

Have you noticed businesses offering lower prices for paying with cash? That’s a cash discounting program in action. For business owners, this practice isn’t just a thoughtful nod to customers—it’s a smart move to reduce payment processing costs and encourage more cash transactions.

This article will explore what cash discount programs are, how they work, and the pros and cons involved. Whether you’re a small business owner or a curious customer, this is your guide to understanding cash discounts better.

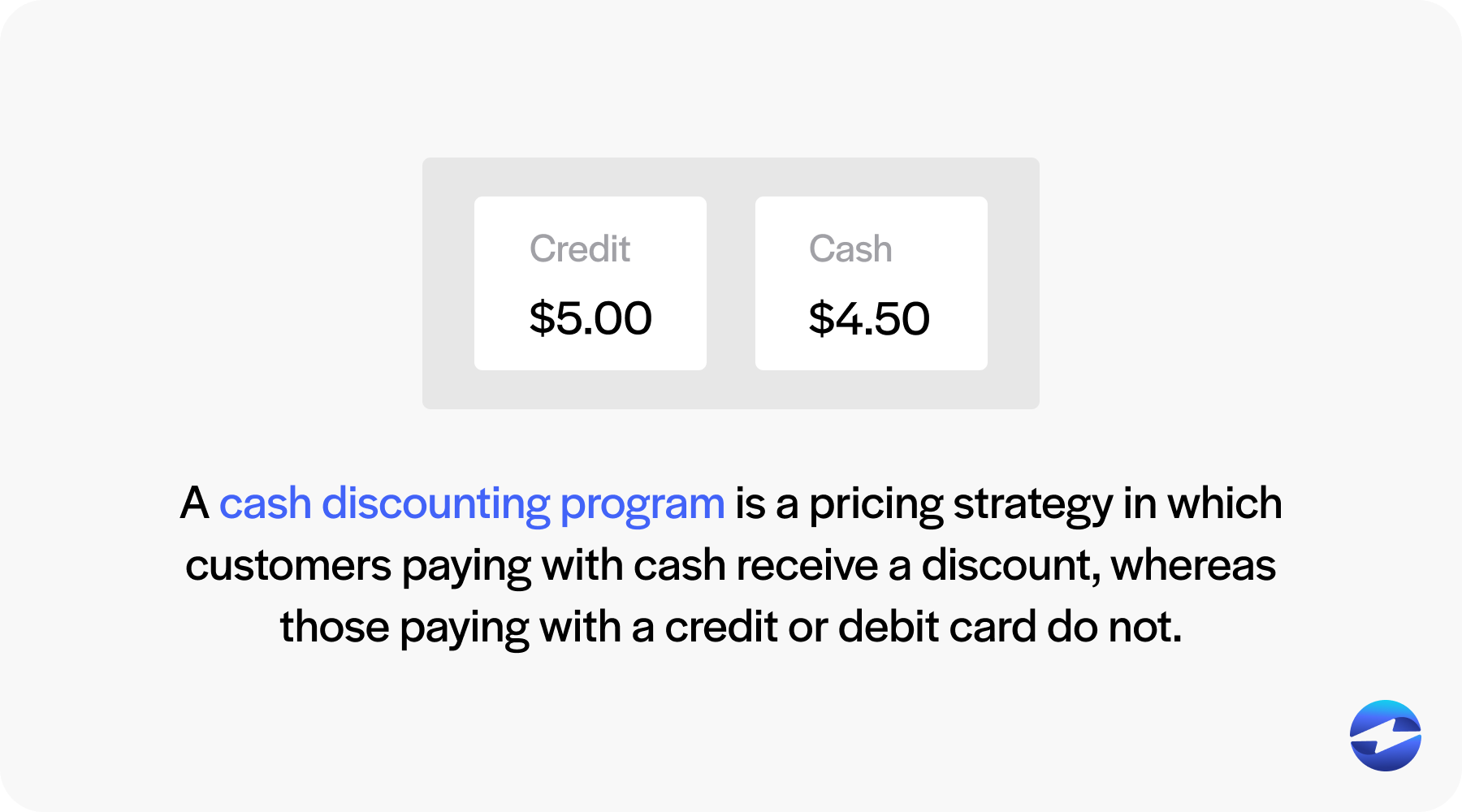

What is a cash discounting program?

Businesses often implement this strategy to offset the costs of card payment processing fees. Essentially, customers save money by paying with cash, while businesses reduce their reliance on card payments.

For example, imagine a café that advertises coffee for $5.00 but offers a 10% discount to cash payers. Customers paying by cash would only pay $4.50—a straightforward cash discount example.

Cash discounts are legal across the United States but must comply with specific guidelines and transparency requirements to avoid legal discrepancies.

Cash discount example

Say you own an auto parts shop and sell a set of brake pads for $120. You offer a 3% cash discount to offset your processing costs.

- A customer paying by credit card pays the full $120.

- A customer paying with cash pays $120 × 0.97 = $116.40.

The $3.60 difference is roughly what you would have paid the card network in processing fees on that transaction anyway, so the economics come out close to even. The math behind a cash discount is simple. Take your card price and multiply it by one minus your discount rate:

Cash discounting formula

Cash Price = Card Price × (1 − Discount Rate)

| Card Price | Discount Rate | Cash Price | Savings |

|---|---|---|---|

| $50 | 3% | $48.50 | $1.50 |

| $120 | 3% | $116.40 | $3.60 |

| $250 | 3% | $242.50 | $7.50 |

| $500 | 3% | $485.00 | $15.00 |

| $1,000 | 3% | $970.00 | $30.00 |

The discount is always calculated off the full displayed card price, not your cost or margin. That distinction matters for compliance and is what separates a cash discount program from a surcharge.

Why would a business offer a cash discount?

Processing fees are the main driver. Every card transaction costs the business a percentage, typically between 1.5% and 3.5%, paid to the card network and processor. A cash discount program makes that cost visible and gives customers a reason to opt out of cards entirely. Cash also settles immediately, which improves day-to-day cash flow without waiting on bank settlement windows. For businesses that deal with high chargeback rates, cash payments eliminate that exposure entirely since there is no card network to dispute through after the fact.

Types of cash discounts

Most cash discount programs use one of three structures. Percentage-based discounts are the most common, where the business reduces the card price by a fixed rate, typically 2.5% to 3%, mirroring the processing fee it is trying to offset. Flat-fee discounts work better for businesses with consistent transaction sizes, where offering a set dollar amount off is simpler to communicate. Tiered discounts scale the savings by order size, which can encourage larger cash purchases.

In B2B settings, cash discounts also appear in invoice terms, written as “2/10 net 30,” meaning the buyer earns a 2% discount by paying within 10 days instead of the full 30. The mechanics differ from a retail cash discount, but the underlying goal is the same: incentivizing faster, lower-cost payment.

Online businesses typically do not have cash as a payment option, so the equivalent is ACH or eCheck, which are direct bank transfers that carry much lower processing fees than credit cards. Offering a small discount for ACH payments at checkout follows the same logic as a cash discount at a physical register.

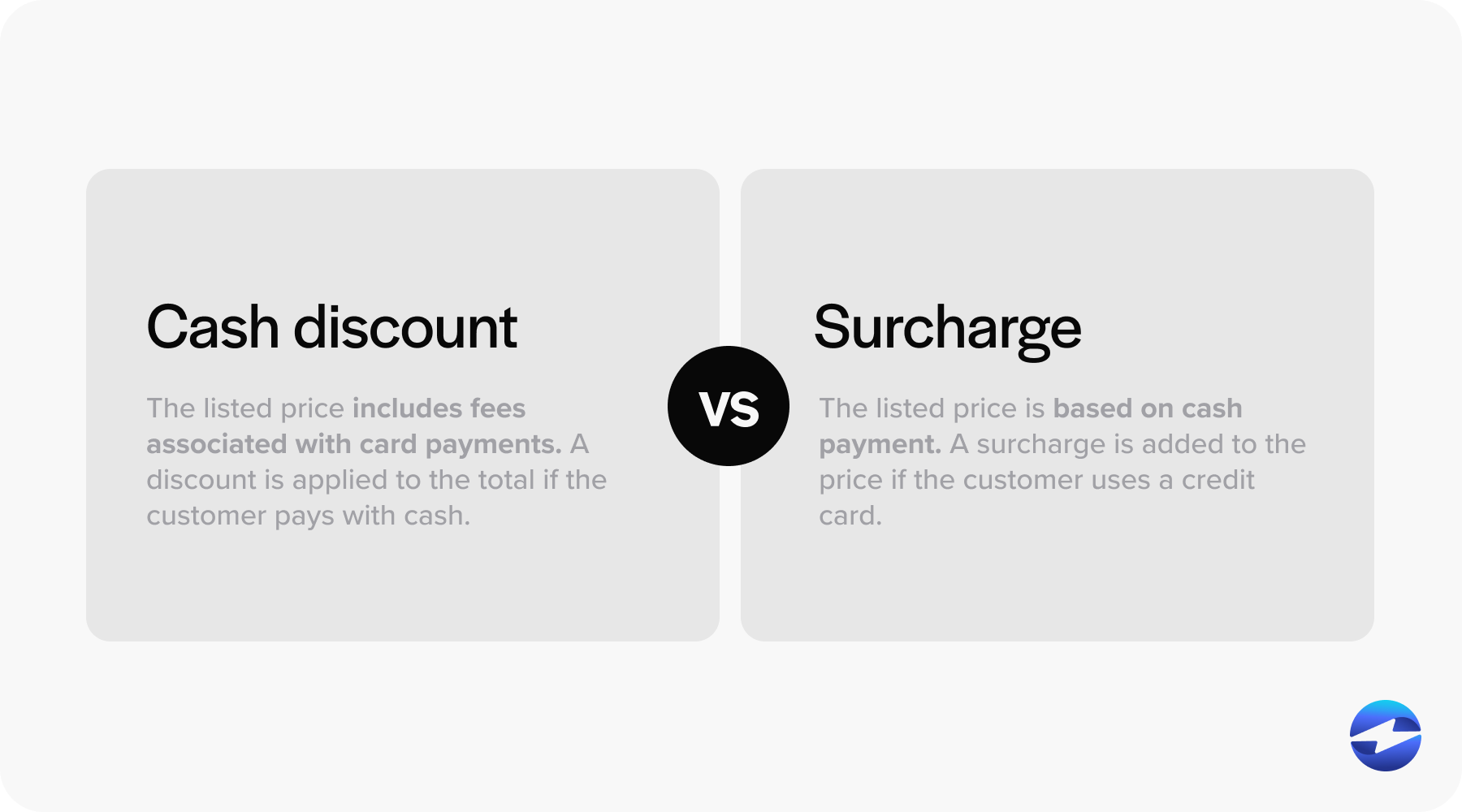

Cash discount vs. surcharge: What’s the difference?

One common point of confusion is the difference between cash discounting programs and surcharging. While both address the costs of card payments, they work in opposite ways:

- Cash Discount Program: The listed price includes fees associated with card payments. A discount is applied to the total if the customer pays with cash, avoiding the card processing fees entirely.

- Surcharge: The listed price is based on cash payment. A surcharge is added to the price if the customer uses a credit card.

For instance, if a pizza shop lists a slice at $3.50 and offers cash discount pricing, customers paying by credit card pay the full price of $3.50, while cash customers pay less. Conversely, if surcharging is in place, the $3.50 price applies to cash payments, but an additional fee (e.g., $0.25) is added for card users.

Both methods require care to ensure transparency, as misleading pricing can damage customer relationships or lead to legal non-compliance.

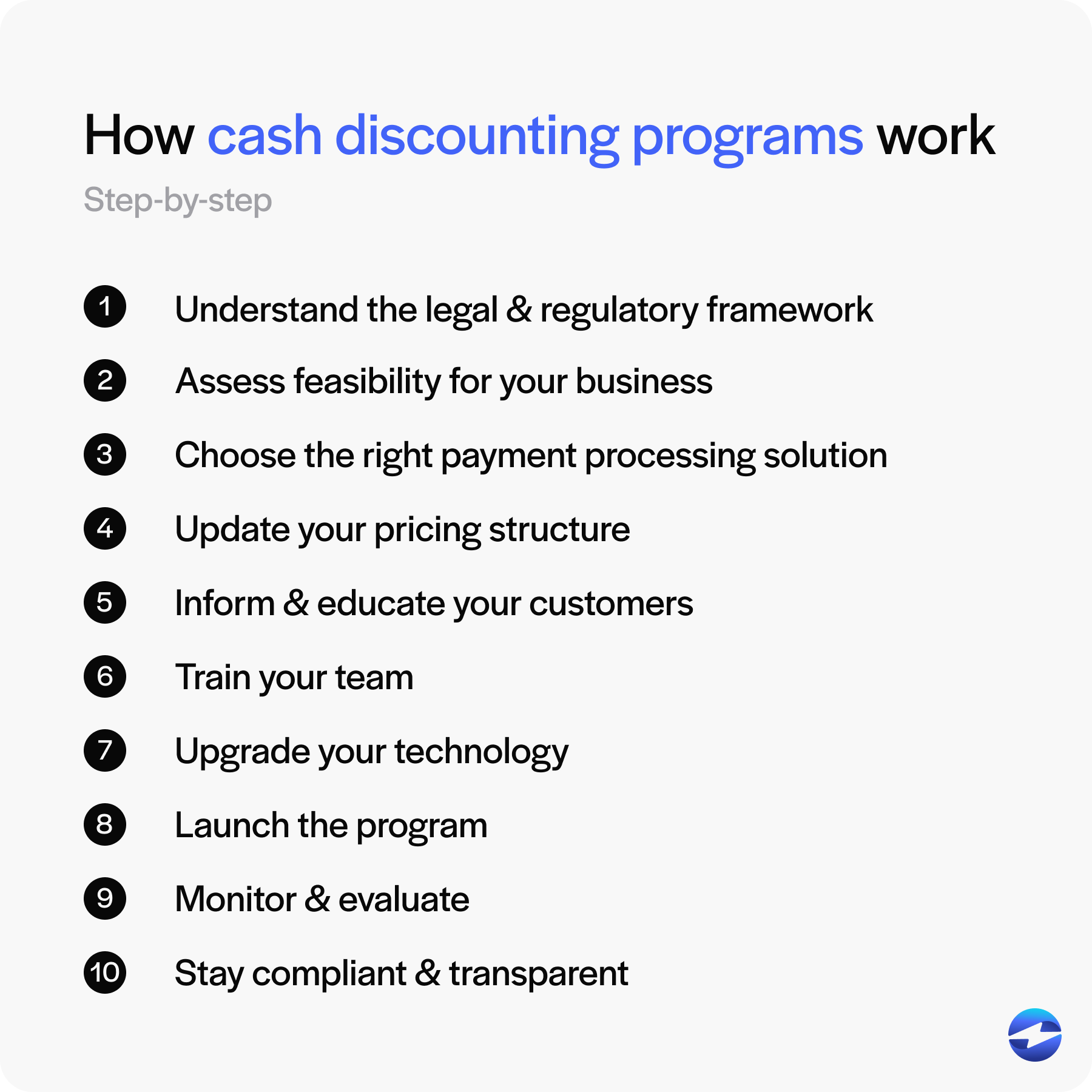

How do cash discounting programs work?

Implementing cash discounting programs involves several steps, requiring a balance of legal, operational, and customer-focused considerations.

Here’s a detailed guide to getting started:

1. Understand the legal and regulatory framework

Before starting a cash discount program, it’s important to understand the legal requirements to stay compliant. Cash discounts are legal nationwide but adhere to specific rules and regulations. A key factor is displaying pricing policies to ensure transparency and avoid disputes. Some states may have unique requirements, so it’s important to research and follow local guidelines.

2. Assess feasibility for your business

Evaluate your customer base and transaction trends carefully to determine if implementing a cash payment discount program aligns with your business model. Start by analyzing how your customers prefer to pay—are they primarily using cash, cards, or mobile payment options? If the majority of your customers favor card or mobile payments, a cash discount program might not generate significant savings for your business. Additionally, consider whether offering cash discounts would appeal to your target audience or incentivize behavior changes. Weigh the potential benefits against the administrative effort and assess how it might impact overall customer satisfaction and profitability.

3. Choose the right payment processing solution

Many payment processors provide features specifically designed to facilitate cash discounting programs, making it easier for businesses to implement this cost-saving strategy. These programs allow merchants to offer customers a discounted price when paying with cash, helping to offset credit card processing fees. When selecting a payment processor, choosing one that aligns with your specific operational needs is essential, as well as offering tools and support for smooth program implementation. Look for a provider that provides user-friendly technology, comprehensive customer support, and transparent pricing.

4. Update your pricing structure

Adjust your pricing strategy to incorporate cash discount pricing and clearly differentiate between cash and card payment prices. This approach allows you to offer customers a discount for paying with cash while covering the processing fees associated with card payments. Ensure the final prices for both payment methods are clearly displayed to avoid any confusion at the point of sale. Transparency is key to building trust with your customers, ensuring they fully understand the pricing structure and their options.

5. Inform and educate your customers

Transparent communication is essential for building trust with your customers. To ensure clarity, use prominent signage at your business to explain that the listed prices reflect card payments while cash transactions qualify for a discount. This helps customers understand the pricing structure upfront and minimizes confusion. Additionally, providing a cash discount receipt that clearly outlines the details of the discount reinforces transparency and professionalism. This receipt shows the savings customers earn by paying with cash, creating a more positive experience.

6. Train your team

Equip your staff with the knowledge, skills, and tools they need to explain the program confidently and effectively. Ensure they are well-prepared to address common questions, clarify details, and can handle any potential customer objections. Providing thorough training and resources will help build their confidence and significantly improve customer interactions.

7. Upgrade your technology

Ensure your point-of-sale (POS) system is equipped to handle dual pricing for smooth transactions. Modern POS systems often use built-in features that simplify implementing cash discounts and calculating surcharges. This ensures compliance, improves efficiency, and provides a seamless experience for both businesses and customers.

8. Launch the program

Begin by rolling out the program and paying close attention to customer responses. Gathering feedback during the initial stages is essential for identifying potential issues and making necessary adjustments. A smooth and positive launch experience lays the foundation for effective implementation and long-term success, ensuring customer satisfaction and program efficiency.

9. Monitor and evaluate

Your cash discount program shouldn’t operate on autopilot. It’s important to regularly evaluate its performance by analyzing its impact on your finances and customer satisfaction. By consistently reviewing and gathering feedback, you can identify areas for improvement and make necessary adjustments to ensure the program remains effective and beneficial for your business.

10. Stay compliant and transparent

Compliance is critical for maintaining trust and avoiding legal issues. It’s essential to stay updated on the latest regulations within your industry and ensure your business aligns with them. Additionally, prioritize clear, transparent, and honest communication about your pricing model to build credibility and customer trust over time.

Now that you understand how these programs work, you should understand what signage should say.

What your cash discount signage needs to say

Visa and Mastercard both require that customers be informed of your cash discount policy before the transaction, not at the moment they hand over their card. At minimum, your signage should state that displayed prices reflect the card payment rate and that cash customers receive a discount at the specified percentage.

Something like: “All listed prices reflect the standard card rate. Pay with cash and receive a [X]% discount.”

Post it at your entrance and at the register. A single notice tucked near the terminal is not enough. Some states have additional disclosure requirements beyond what card networks mandate, so it is worth confirming local rules before you launch.

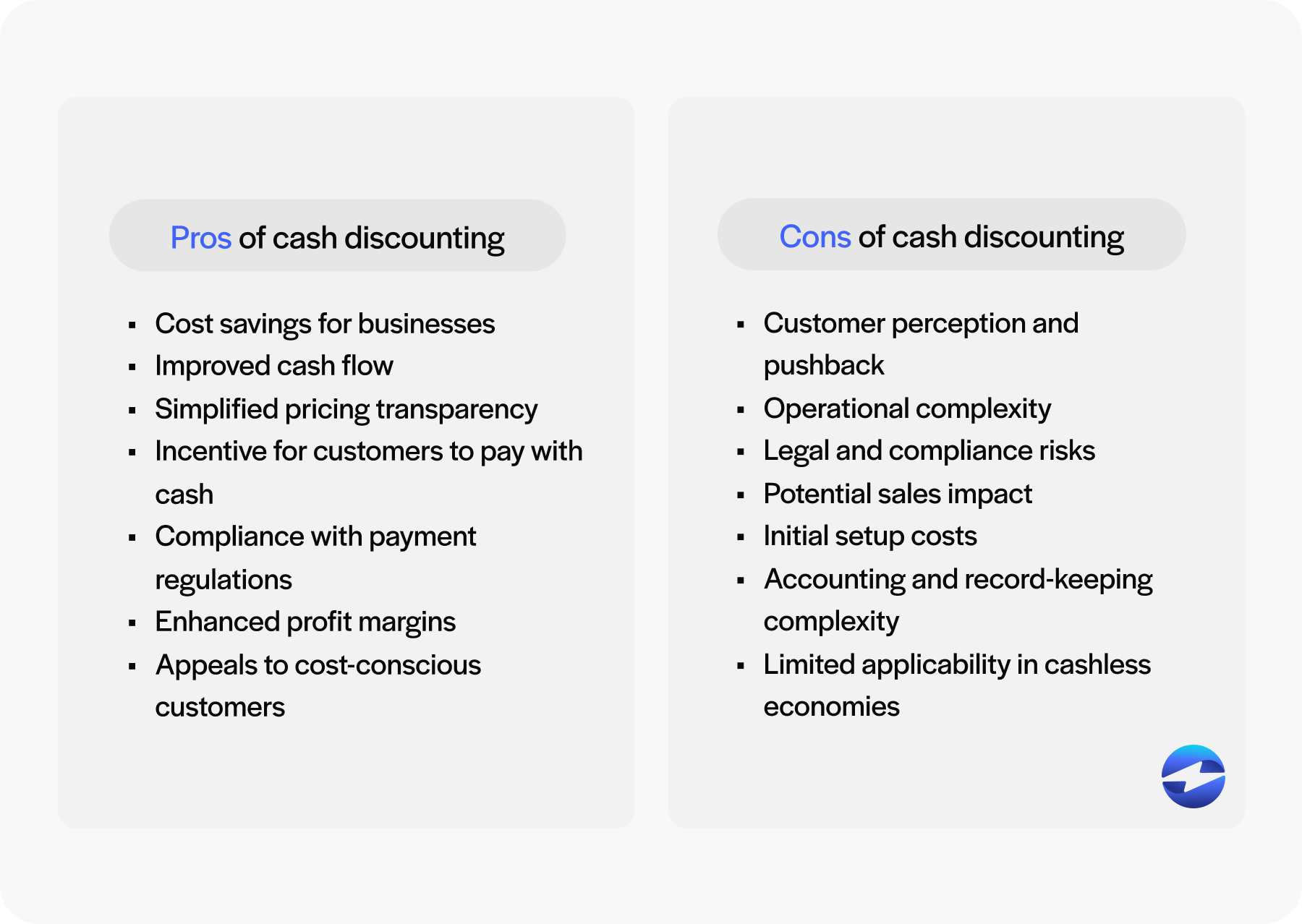

7 pros and cons of cash discounting programs

Cash discounting programs offer a strategic way for businesses to save on credit card processing fees by incentivizing customers to pay with cash. While these programs can be a powerful tool for cost reduction and customer engagement, they also come with potential challenges.

Below is a detailed look at their pros and cons:

Pros

- Cost savings for businesses: By offering a cash discount, you can reduce your dependency on card transactions and avoid steep processing fees.

- Improved cash flow: Cash transactions provide immediate liquidity, easing day-to-day business operations.

- Simplified pricing transparency: Customers appreciate honesty. Clear communication about cash discounts builds trust.

- Incentive for customers to pay with cash: Cash discounts encourage customers to opt for cash over cards, indirectly reducing costs for your business.

- Compliance with payment regulations: Unlike surcharges, cash discount programs generally face fewer legal hurdles when implemented correctly.

- Enhanced profit margins: Without processing fees eroding profits, businesses can enjoy wider margins on sales.

- Appeals to cost-conscious customers: Offering savings for cash payments resonates with buyers looking to stretch their dollar further.

Cons

- Customer perception and pushback: Some customers may misinterpret a card payment as a penalty and feel alienated.

- Operational complexity: Implementing a cash discount program requires coordination across pricing, staff training, and point-of-sale updates.

- Legal and compliance risks: Businesses that fail to follow transparent practices risk fines or legal action.

- Potential sales impact: Customers who prefer cards may go elsewhere, affecting sales negatively.

- Initial setup costs: The cost of upgrading POS systems or revamping pricing models can be significant.

- Accounting and record-keeping complexity: Tracking discounts and reconciling accounts may increase administrative burdens.

- Limited applicability in cashless economies: As digital payments grow in popularity, cash-based incentives may become irrelevant in some markets.

By weighing the pros and cons, businesses can determine whether this approach aligns with their operational goals and customer preferences.

Common barriers to implementing a cash discount program

The most common sticking point is POS compatibility. Older terminals were not built for dual pricing, and getting them there often means upgrading hardware or switching processors. It is usually easier to evaluate your payment processor first and your POS second, since most processors that specialize in cash discounting provide compatible equipment as part of the setup.

Customer resistance is the other factor worth planning for. Shoppers who rely on credit card rewards may see the card price as a penalty rather than the cash price as a savings opportunity, regardless of how you frame it. Clear signage and well-trained staff reduce friction significantly, but some portion of your customer base will push back. Staff training gaps during rollout are also worth planning around. Inconsistent explanations at the register create confusion that is entirely avoidable with a short team briefing before launch.

Reducing costs with cash discounting programs

Cash discounting programs present a compelling opportunity for businesses to optimize costs and engage with value-conscious customers. However, their success depends on careful implementation, clear communication, and a solid understanding of your customer base. This approach isn’t a one-size-fits-all solution – it requires assessing whether the benefits align with your operational goals and customer preferences.

By prioritizing transparency and compliance, businesses can build trust while navigating the challenges of adopting a cash discount program. Whether you’re considering cash discounts to save on fees or enhance customer loyalty, weighing the potential advantages against the challenges is essential to making an informed decision. EBizCharge’s credit card surcharge program handles the compliance and dual pricing setup automatically, and connects through 100+ software integrations so your cash discount program runs cleanly inside the accounting or POS system your team already uses.

Frequently Asked Questions.

Are cash discounts legal?

Yes, cash discounts are legal in all 50 states. The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 explicitly permits businesses to offer discounts for paying by cash, check, or debit card. Card networks including Visa and Mastercard also allow cash discounts, provided they’re disclosed properly at the point of sale.

What’s a cash discount receipt?

A cash discount receipt is a transaction record that clearly shows the original card price, the discount amount applied for paying with cash, and the final amount paid. It documents that the customer received a price reduction, not that a surcharge was added.

What’s the main difference between a cash discount vs. surcharge?

The pricing baseline is what separates them. In a cash discount program, your listed price already includes the cost of card acceptance. Customers who pay with cash get a reduction off that price. In a surcharge model, your listed price is the base (cash) price, and an additional fee is added when a customer pays by credit card. Both approaches shift processing costs to card-paying customers, but a cash discount is legal everywhere in the U.S., while credit card surcharges are still restricted in some states. Cash discount programs also tend to create less customer friction because the framing is a savings opportunity rather than a penalty.

Can any business implement a cash discount program?

Most businesses can, though some industries see better results than others. Retail stores, restaurants, medical offices, auto repair shops, and service-based businesses are among the most common adopters. The program works best when a meaningful portion of your customers are willing and able to pay with cash. Businesses where nearly all transactions are digital may not see a practical benefit.

How does cash discount processing work?

A cash discount processing program runs through your payment terminal and POS system. When a customer is ready to pay, the system displays the standard card price by default. If the customer chooses to pay with cash, the terminal or cashier applies the discount, and the cash price appears on the receipt. Most processors that support cash discounting configure this automatically. The processor typically adjusts your merchant statement to reflect the reduced card transaction volume, and your records show cash transactions at the lower price. Setup usually takes a few days to a week, depending on your equipment and processor.

What should a cash discount sign say?

Your cash discount sign should clearly state that displayed prices reflect the card payment rate and that a discount is available for cash payments. It should specify the discount amount either as a percentage or the actual cash price. Posting this notice at the entrance and at the point of sale covers the card network disclosure requirements.

Something like: “Prices listed are the standard payment rate. Cash customers receive a [X]% discount.” Both Visa and Mastercard require disclosure before the transaction is initiated, so signage needs to be visible before the customer reaches the register, not only at checkout.

What is the cash discount formula?

Cash Price = Card Price × (1 − Discount Rate)

For example, if your card price is $150 and your discount rate is 3%, the calculation is: $150 × (1 − 0.03) = $150 × 0.97 = $145.50. The customer pays $145.50 with cash. The $4.50 difference roughly offsets what you would have paid in card processing fees on that transaction.

- What is a cash discounting program?

- Cash discount example

- Why would a business offer a cash discount?

- Cash discount vs. surcharge: What’s the difference?

- How do cash discounting programs work?

- What your cash discount signage needs to say

- 7 pros and cons of cash discounting programs

- Common barriers to implementing a cash discount program

- Reducing costs with cash discounting programs

- Frequently Asked Questions.