Blog > B2B Credit Card Surcharging: What Manufacturers, Distributors, and Wholesalers Need to Know

B2B Credit Card Surcharging: What Manufacturers, Distributors, and Wholesalers Need to Know

Credit card processing looks very different depending on where you sit in the economy. A retail coffee shop paying 2.6% on a $5 transaction is annoying. A manufacturer paying that same rate on a $75,000 corporate card payment is losing thousands of dollars a month to a cost that most people inside the business aren’t even tracking closely.

That’s the reality of B2B payment processing today. More buyers are using corporate and purchasing cards to preserve their own cash flow, and those cards carry some of the highest interchange rates in the entire fee schedule. For manufacturers, distributors, and wholesalers absorbing these fees across large transaction volumes, credit card surcharging has become one of the most practical conversations in finance.

This article covers what makes surcharging different in B2B, how it works inside an ERP environment, what it does to AR reconciliation, and why the tool you use to implement it matters more than most merchants realize.

Why B2B Merchants Pay More Than They Should

Not all credit cards cost the same to accept. Consumer cards sit at one end of the interchange spectrum. Corporate cards, purchasing cards, and rewards cards sit at the other. Card networks charge higher interchange on these card types because they carry more benefits for the cardholder, and that cost flows directly to the merchant.

The credit card fees for businesses in B2B environments reflect this. A corporate purchasing card used on a large invoice can carry an effective interchange rate well above 2.5%, sometimes closer to 3% or higher, depending on card type and how the transaction is processed. Multiply that across millions of dollars in annual card volume, and you have a significant, recurring expense that deserves real attention.

The other compounding factor is that the B2B payment mix has been shifting for years. Buyers increasingly use cards because they extend their own cash flow and earn rewards on company spending. That’s a rational decision for them. But it means more of your incoming AR is arriving at premium interchange rates, and that trend isn’t reversing.

Why Surcharging Works Better in B2B Than Most Merchants Expect

There’s a common hesitation around credit card surcharging in B2B: the fear that customers will push back. In practice, that concern tends to be overstated, especially in industries like manufacturing, distribution, and wholesale, where the buyer is a business rather than an individual consumer.

When a procurement department or AP team is paying a $20,000 invoice, a clearly disclosed surcharge for using credit card is a known, predictable cost they can account for. Many buyers in B2B environments are accustomed to seeing fees like this and factor them into payment method decisions without much friction.

That dynamic is what makes surcharging credit cards genuinely viable in B2B in a way it often isn’t in consumer retail. The relationships are established, the transactions are larger, and the people approving payments are thinking about cost structures rather than reacting emotionally to a fee at checkout.

For distributors operating on thin margins, even partial cost recovery through a surcharge program makes a measurable difference. For manufacturers processing high-value transactions with corporate card users, the numbers get substantial quickly.

The Compliance Layer You Can’t Skip

Even in B2B contexts, surcharging rules apply in full. The card networks don’t make exceptions based on transaction size or business type, and understanding this before launching a surcharge program matters.

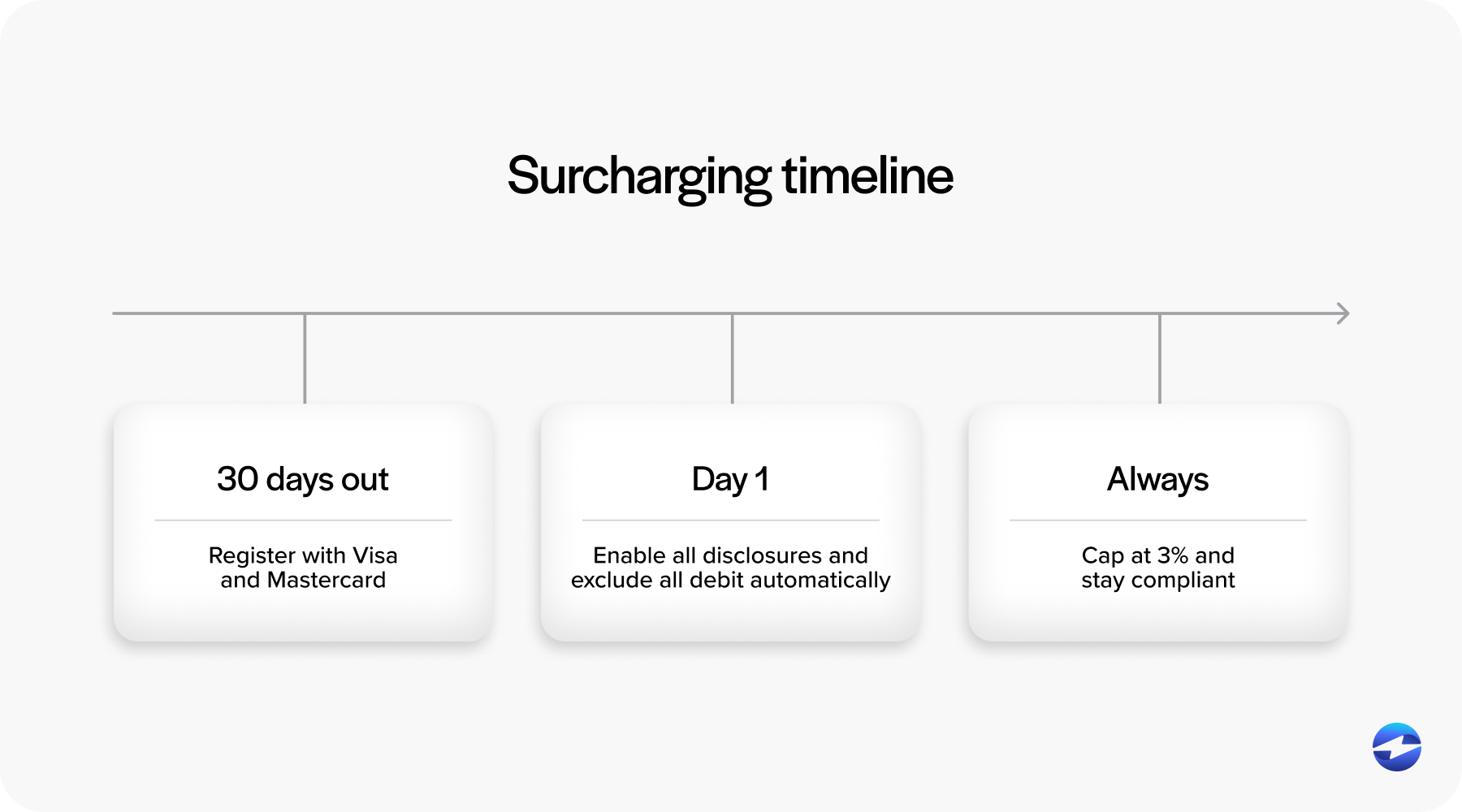

Visa and Mastercard both require merchants to register their intent to surcharge at least 30 days before doing so. The surcharge cannot exceed 3%, and it cannot exceed your actual cost of acceptance. Debit and prepaid cards can’t be surcharged under any circumstances, even when the buyer is a business. Additionally, pre-transaction disclosure is required regardless of the payment channel, whether that’s an online payment portal, an ERP-generated invoice, or a phone payment.

That last point is where B2B merchants often underestimate the complexity. B2B payment processing happens across multiple channels simultaneously. A single customer might pay through your ERP customer portal on one invoice, respond to an emailed invoice link on another, and call in a payment on a third. Surcharging rules and disclosure requirements follow the transaction across all of those channels. Applying surcharges inconsistently across channels, or failing to disclose in one of them, creates compliance exposure.

How Surcharging Works Inside an ERP Environment

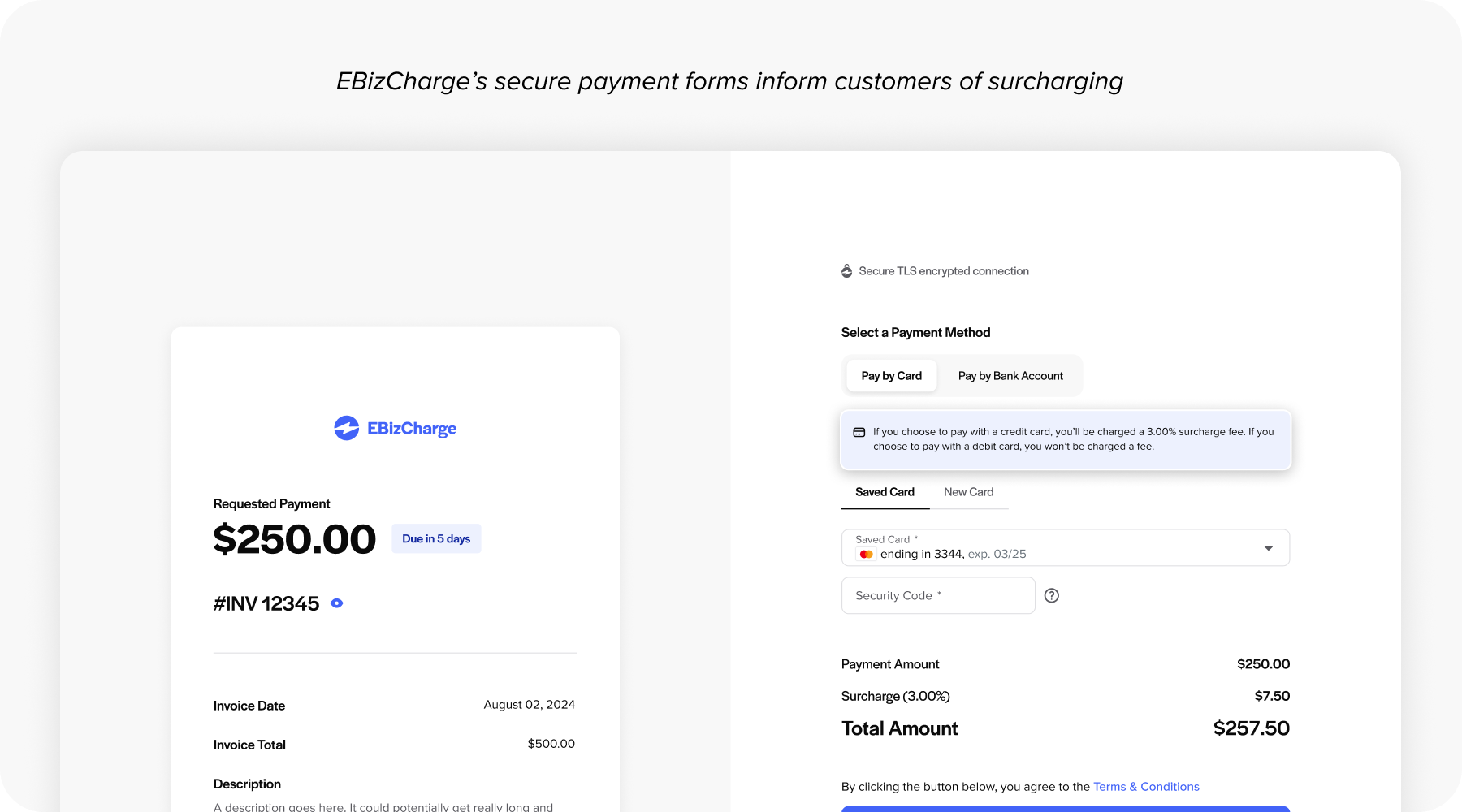

Most B2B payment activity doesn’t happen at a point-of-sale terminal. It happens inside an ERP. This is where invoices are generated, where payment links are sent from, and where AR is managed. Any surcharge credit card processing solution that doesn’t live inside that environment creates friction by default.

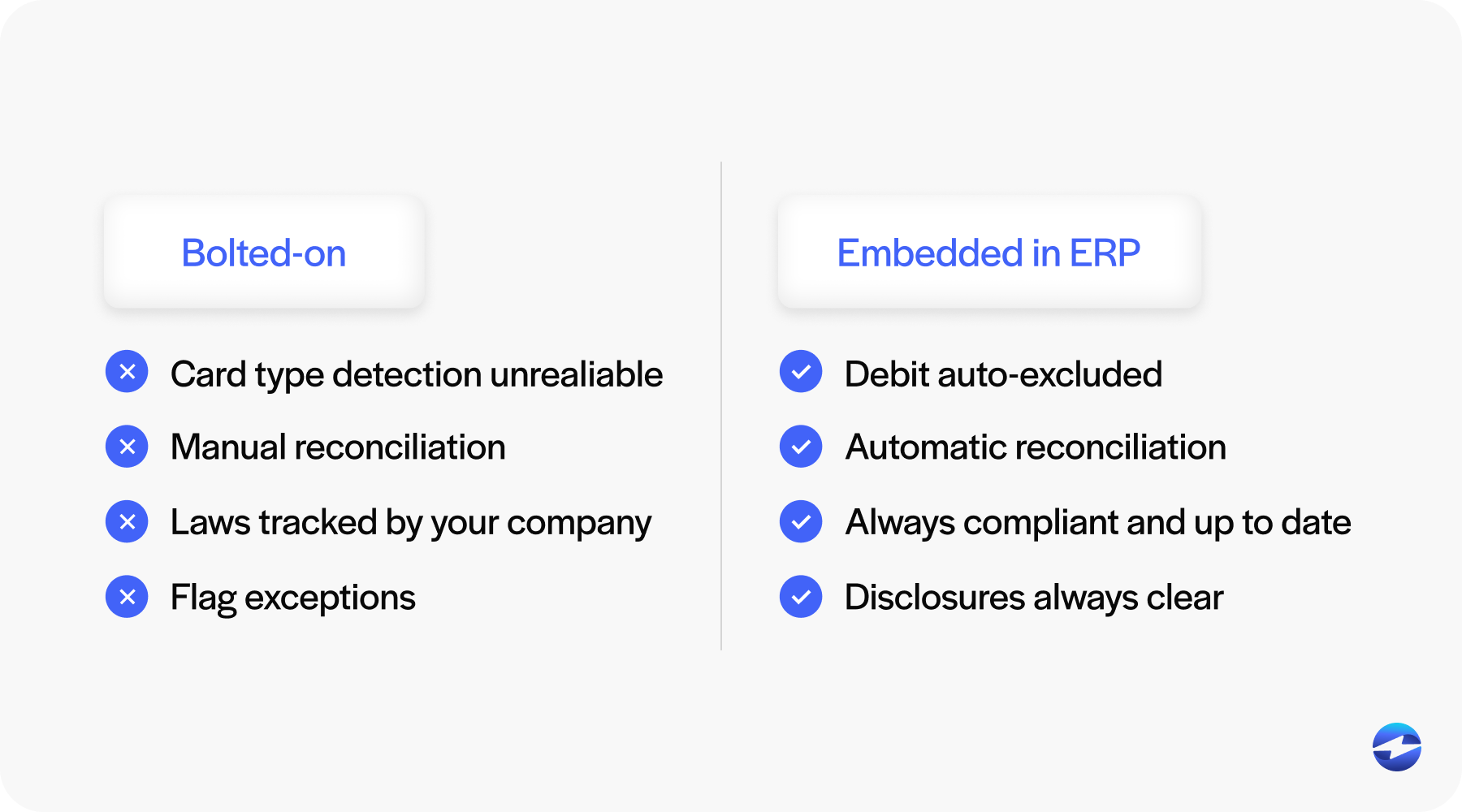

A bolted-on surcharge tool, meaning one that sits outside the ERP and applies fees through a separate interface or gateway, creates a set of operational problems that add up quickly. Card type detection may not be reliable, which means debit cards could get surcharged incorrectly. Surcharge amounts don’t post automatically to the invoice or general ledger, which means someone on your AR team has to reconcile the difference manually. State-level compliance rules aren’t tied to transaction data, so enforcing them requires manual oversight of each customer’s location.

A native payment processing solution handles all of this at the transaction level. The surcharge is calculated and displayed at the point of payment inside the ERP or customer portal. Card type detection runs automatically on every transaction. The surcharge is posted as its own line item to the invoice and to the general ledger. State restrictions based on the customer’s billing address are enforced without anyone on your team having to think about it.

That’s the operational difference between embedded and bolted-on, and it’s a significant one.

What Surcharging Does to AR Reconciliation

For the AR managers, controllers, and finance directors reading this, the reconciliation question deserves direct attention.

When surcharges are applied outside the ERP, the payment that hits your bank account doesn’t match the invoice total. Your AR team then has to manually reconcile the difference between what was invoiced, what was charged to the card, and what was actually deposited. On a high volume of transactions, this creates a daily reconciliation burden that consumes real staff hours and introduces meaningful room for error.

Embedded surcharging eliminates that problem because the surcharge is part of the transaction record from the beginning. The invoiced amount, the surcharge, and the total charged all exist in the same record inside the ERP. When the deposit hits, it matches. The invoice closes cleanly. There’s no gap to bridge manually.

The downstream effect on days sales outstanding (DSO) is also worth noting. Fewer open reconciliation items means your cash application cycle moves faster. Transactions that would have sat open for days while someone sorted out the discrepancy close on their own.

Embedded Surcharging vs. Bolted-On Solutions

The core distinction is where compliance logic lives.

A bolted-on surcharging solution can technically apply a surcharge for using credit card payments. But the compliance burden stays with the merchant because the tool isn’t connected to the data it needs to make smart decisions automatically. Your team ends up manually managing card type exceptions, state restrictions, disclosure requirements, and GL postings. That overhead undercuts the financial benefit of having a surcharge program in the first place.

An embedded solution moves compliance enforcement into the platform. Surcharging rules are applied automatically. Card type detection is reliable. State-level restrictions trigger based on billing address data already in your ERP. Required disclosures appear in the payment flow without requiring custom configuration. And when Visa or Mastercard updates its policies, those changes are reflected on the platform rather than landing on your accounting team to track and implement.

For manufacturers, distributors, and wholesalers managing high transaction volumes with lean AR teams, that difference isn’t marginal. It’s the difference between a surcharge program that actually recovers costs and one that creates new work while doing so.

How EBizCharge Handles B2B Surcharging

EBizCharge’s payment solution is built natively into more than 100 ERP, accounting, and CRM platforms. The surcharge logic lives where the transaction happens, inside the system your AR team already works in every day.

Card type detection runs automatically on every payment, so credit cards get the surcharge, and debit or prepaid cards never do. State-level compliance rules are enforced on the platform based on billing address data from your ERP. The surcharge posts as a separate line item to the invoice and the GL without any manual entry. And for eligible B2B transactions, Level 2 and Level 3 data are submitted alongside the surcharge, which can reduce interchange rates further and compound the cost recovery.

When card network surcharging rules change, the platform updates. Your team isn’t responsible for tracking policy changes across Visa, Mastercard, and Amex and adjusting your process accordingly.

The result is a payment processing solution that handles credit card fees for businesses at the transaction level, removes the compliance and reconciliation burden from your AR team, and makes the financial case for surcharging actually hold up in practice.