Blog > Merchant Services for Professional Services Firms: A Guide for Agencies, Consultancies, and Law Firms

Merchant Services for Professional Services Firms: A Guide for Agencies, Consultancies, and Law Firms

Most payment infrastructure was designed with retail and e-commerce in mind. A customer picks a product, clicks buy, and the money moves. Clean, simple, done. But that model has almost nothing to do with how agencies, consultancies, and law firms actually get paid. If you run one of these businesses, you already know the friction: invoices that sit unpaid for weeks, retainer clients who need automated billing, milestone payments that have to be triggered manually, clients who want to pay by ACH but your processor only handles cards.

Getting your payment setup right isn’t just an operational detail. It directly affects your cash flow, your client experience, and the amount of time your team spends chasing money rather than focusing on other business operations. This guide is written specifically for principals, operations leads, and finance managers at professional services firms who need honest, practical guidance on what professional services merchant services actually look like — and how to find a setup that fits the way you bill.

How Professional Services Firms Bill Differently

The fundamental difference between a product business and a services firm is that services firms are selling time, expertise, and outcomes. Those things don’t fit neatly into a checkout flow.

Retainers are one of the most common arrangements. A client agrees to pay a fixed monthly fee for ongoing access to your team’s work, whether that’s a marketing agency managing campaigns, an accounting firm handling books, or a law firm on monthly counsel. The amount might be consistent, or it might vary based on hours used. Either way, you need a system that can charge that client automatically each month without someone on your team manually processing it.

Project-based billing works differently. The engagement has a defined scope, and payments are tied to progress. A typical structure might look like 30 or 40 percent upfront as a deposit, another payment at a midpoint milestone, and the remainder on delivery. Time and materials billing, common in consulting and staffing, means you’re invoicing based on actual hours worked — often weekly or bi-weekly — with amounts that vary every cycle.

Then there are hybrid models, where a client pays a base retainer but gets billed separately for work beyond the agreed scope. Managing that cleanly requires both recurring billing automation and the ability to send ad hoc invoices on top of it. All of this is a far cry from a point-of-sale transaction. The right merchant services provider for a services firm needs to handle this complexity natively, not as an afterthought.

Payment Methods That Matter in B2B

Most of your clients are businesses, and businesses pay differently than consumers. Understanding which payment methods to support shapes which payment processing solution makes sense for your firm.

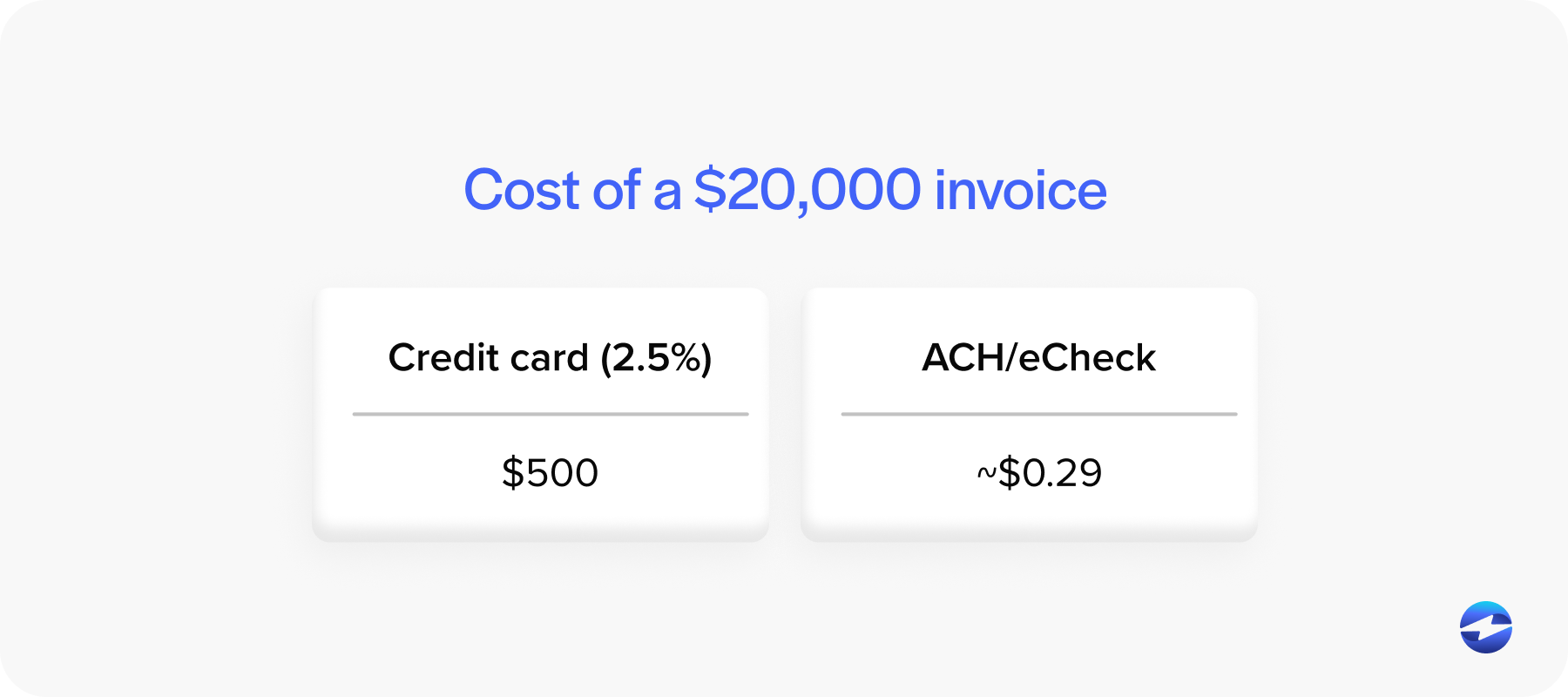

Automated Clearing House (ACH) bank transfers are the preferred method for most B2B clients when invoice amounts are significant. Card processing fees run anywhere from 2.5 to 3.5 percent, and on a $20,000 invoice, that adds up fast. ACH transfers cost a fraction of that. Many larger clients, particularly enterprise accounts and government entities, will default to ACH or even require it. If your payment processor doesn’t handle ACH natively alongside card payments, you are creating unnecessary friction.

Credit and charge cards still come up regularly — smaller invoices, one-time engagements, or clients who want to capture rewards on business spending. Some firms pass the processing fee through to clients as a surcharge where legally permitted. Others build it into their pricing. Either approach is valid, but you need a payment processing solution that supports whichever path you choose.

Wire transfers are common in legal work and high-dollar engagements. Checks aren’t going away either, especially in industries like law and government contracting. You need a practical workflow for handling both.

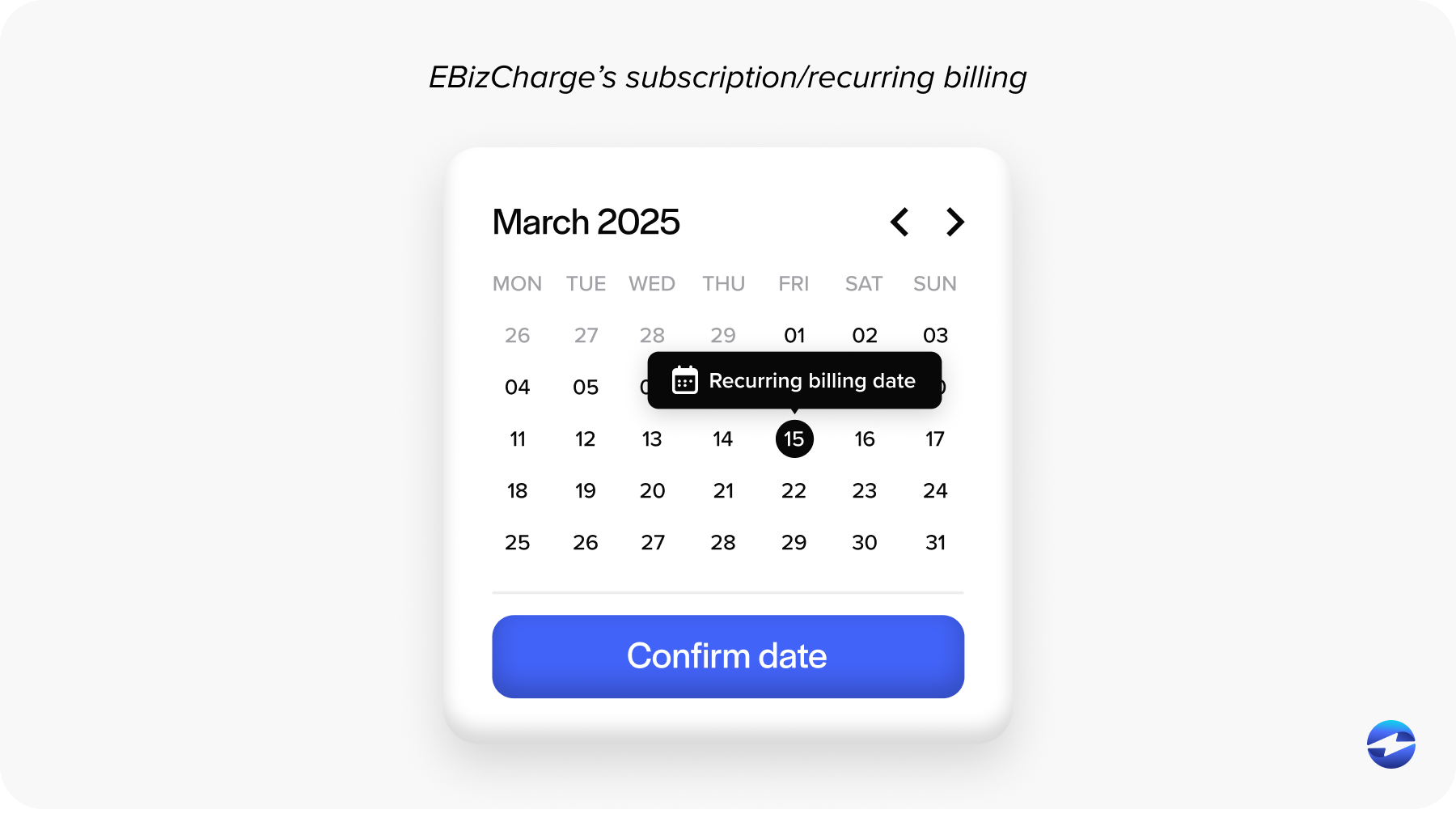

Recurring Billing for Retainer Clients

A good B2B merchant services setup for retainer billing starts with properly collecting and tokenizing your client’s payment method. That means storing a card or ACH authorization in a way that lets you charge it on a set schedule without the client re-entering details every time. Getting a signed payment authorization agreement upfront is both a legal best practice and good client communication.

From there, your credit card processing or ACH billing system should handle the scheduled charge automatically, send a receipt, and record the transaction against the right project in your accounting software. If a payment fails, the system should retry it and notify both your team and the client rather than silently failing. For retainers with variable amounts, you need the flexibility to adjust the charge each cycle without a lengthy re-authorization process. That flexibility isn’t universal across payment processors, and it’s worth asking about directly when evaluating options.

Milestone and Invoice-Based Collection

Project billing requires a different workflow. Your trigger for collecting payment is a project event or deliverable sign-off, not a calendar date. At minimum, you should be sending invoices with clear line items, a project reference number, explicit payment terms, and a direct payment link. The fewer steps between “receive invoice” and “pay invoice,” the faster you get paid.

Payment terms deserve some thought. Net-30 is standard in many industries, but Net-15 or due-on-receipt works in plenty of contexts. Automated reminders before and after the due date aren’t aggressive — they’re just good accounts receivable hygiene. The best payment processing software handles this automatically, so your team isn’t manually tracking who owes what.

Integrations and Fees

If your payment processor doesn’t integrate cleanly with your accounting software, someone on your team is reconciling payments manually. Good payment processing software bridges that gap — your payment solution should post transactions to the right accounts without manual data entry, match payments to open invoices automatically, and handle partial payments and refunds in a way your accounting system understands.

On fees, the headline processing rate is only part of the story. Pay attention to monthly account fees, ACH transaction fees, and charges for features like recurring billing or customer portals. PCI compliance is manageable for most firms if you use a modern payment processor that handles tokenization and hosts the payment page on its infrastructure rather than yours. Never store card data in emails or spreadsheets — that’s how data breaches happen.

Why EBizCharge Works Well for Professional Services Firms

If you’ve read this far, you have a clear sense of what professional services merchant services actually require. It’s not a checkout button. It’s recurring billing with flexible amounts, invoice-based collection, ACH and card support in one place, and deep integration with the accounting software your firm already runs.

EBizCharge is a payment processor built with exactly that kind of B2B complexity in mind. As a dedicated B2B merchant services solution, it doesn’t dilute its tools and features like a basic services provider. It offers focused tools and features designed for business-to-business work, ensuring you have everything you need to streamline your workflow.

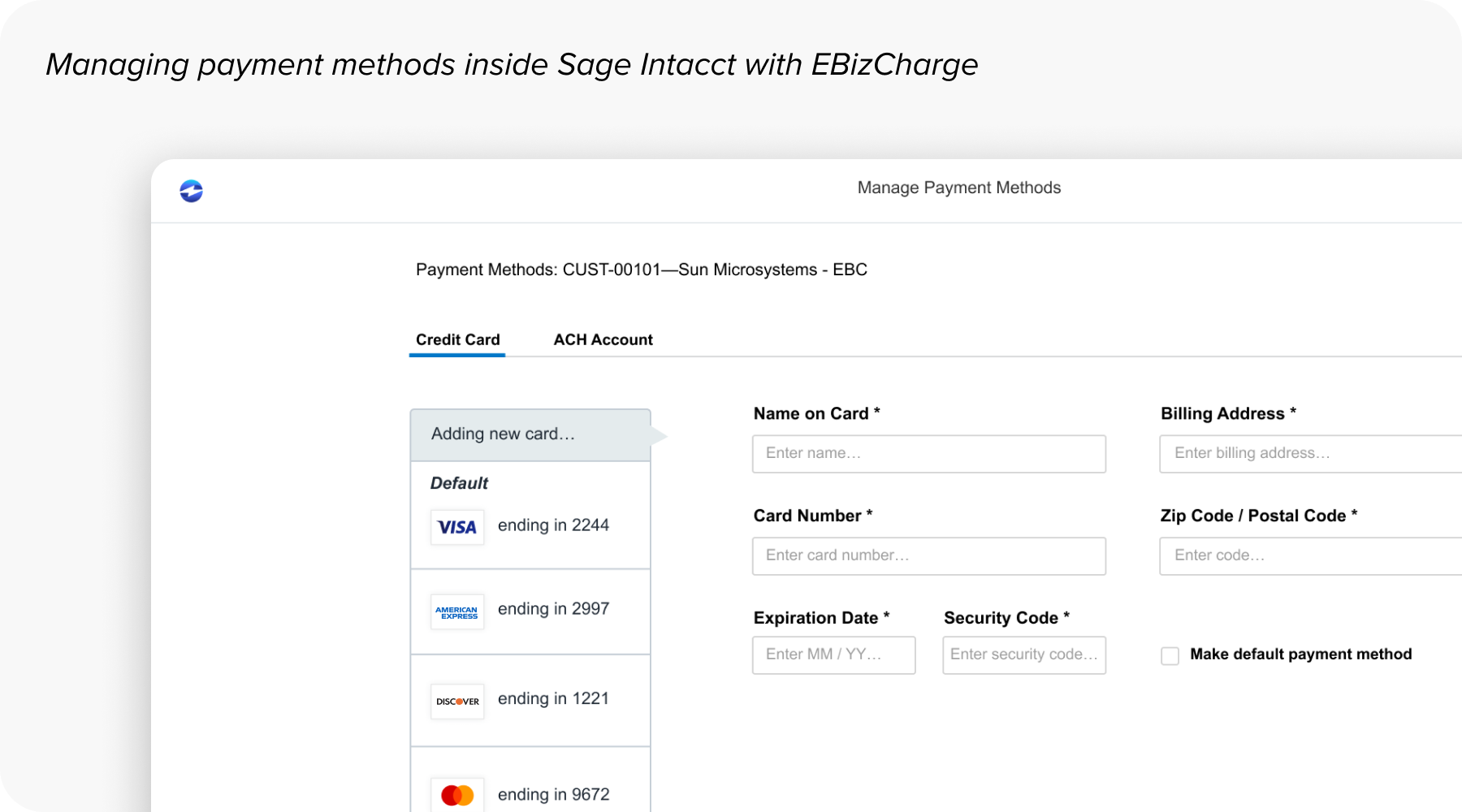

The integration depth is one of its strongest points. EBizCharge has native integrations with QuickBooks, NetSuite, Sage, Microsoft Dynamics, and several other platforms. Payments post automatically, invoices are marked paid, and reconciliation work shrinks dramatically. On payment methods, EBizCharge supports both ACH and credit card processing under one platform, so clients can pay however works best for them.

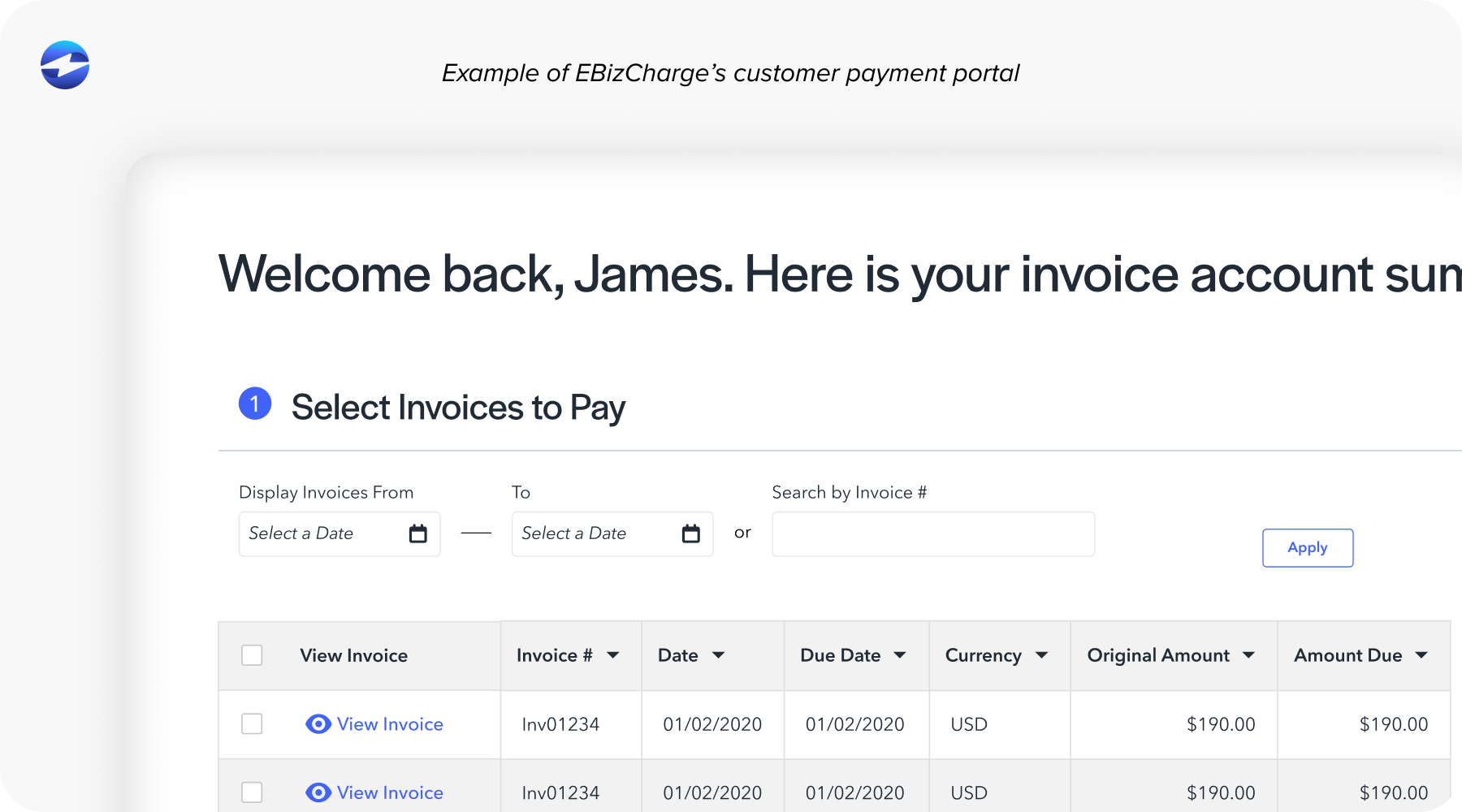

For retainer clients, the recurring billing tools allow you to automate charges on a schedule, adjust amounts as needed, and handle failed payments with retry logic. The customer payment portal gives clients a self-serve place to view invoices and pay outstanding balances, which reduces the back-and-forth your team has to manage.

EBizCharge consistently earns strong ratings on G2, Capterra, and other review platforms, particularly for its integration quality and U.S.-based customer support. For anyone evaluating the best merchant services provider for a services-based business, those reviews tell a consistent story: it works well, and when something goes wrong, you can actually reach someone.

The best merchant services provider for your firm is the one that fits how you actually operate. For agencies, consultancies, and law firms that need flexible recurring billing, strong accounting integrations, and a genuinely good client payment experience, EBizCharge delivers exactly that. It’s the kind of payment solution that tends to quietly eliminate the friction that most professional services firms have come to accept as normal.