Once a B2B company understands the savings potential of level 3 processing, the next question is almost always the same: What software actually supports it? It sounds like it should be a simple question. It isn’t.

Level 3 support isn’t a switch that’s either on or off. It exists on a spectrum. Some platforms support it fully and automatically. Others support it in theory but require significant developer work to activate. And some claim support in their marketing materials while delivering something that functions more like level 1 in practice. Knowing the difference matters because inconsistent data submission is what causes transactions to downgrade silently to higher interchange rates without anyone noticing.

This guide breaks down the main categories of software that supports level 3 processing, what genuine support looks like in each category, and what questions to ask any vendor before you commit.

A Quick Level 3 Recap

Before getting into the software landscape, a brief refresher for anyone who needs it.

Level 3 credit card processing is the most detailed tier of interchange data submission. To qualify for level 3 rates, a transaction must include full line-item data at settlement: product codes, item descriptions, quantities, unit of measure, unit prices, line-level tax, freight amounts, PO number, and ship-to ZIP. All of it must be submitted at the time of authorization and settlement. It can’t be added retroactively.

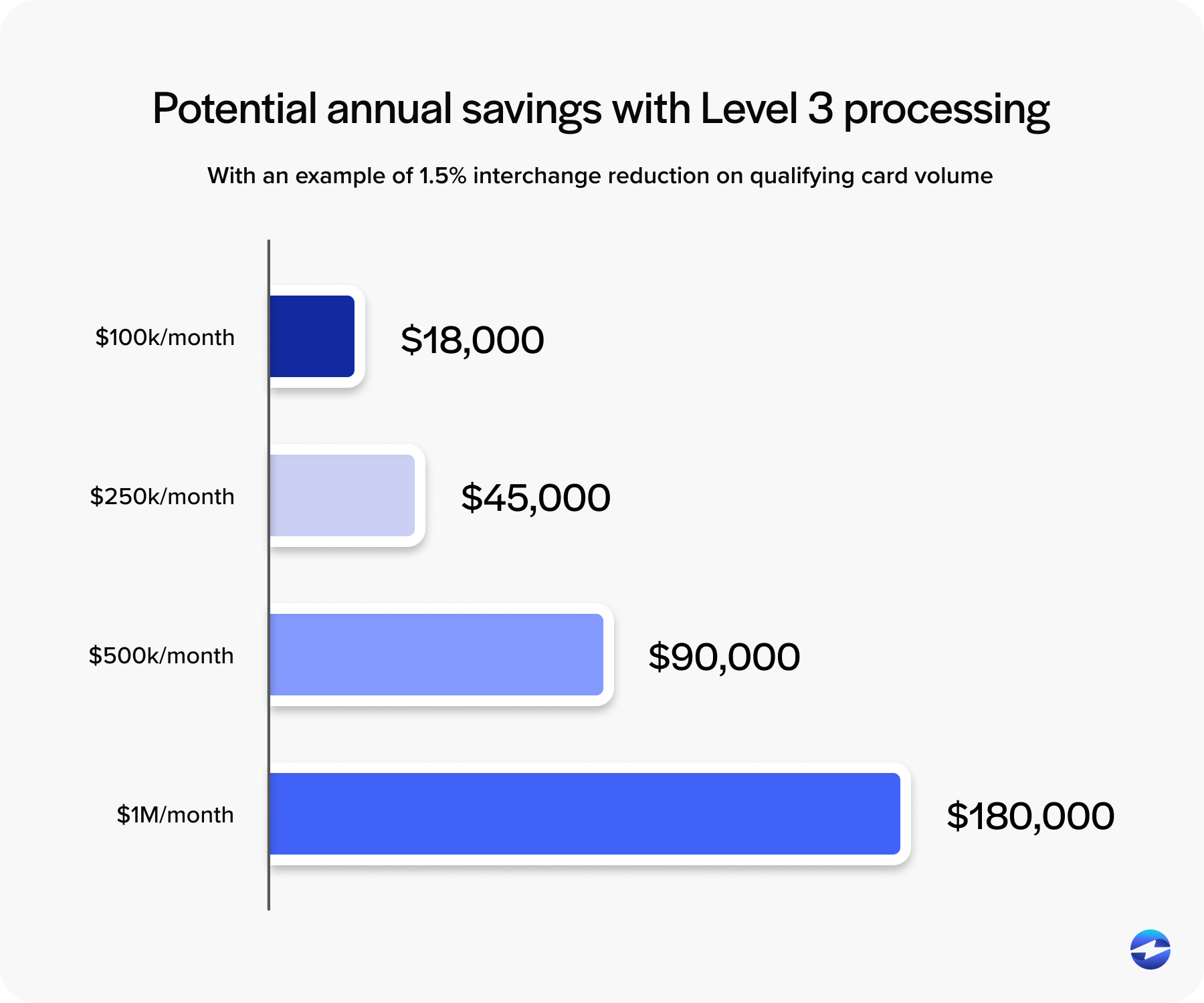

The payoff is meaningful. Level 3 processing rates on qualifying corporate purchasing cards and government procurement cards are typically 0.80% to 1.50% lower than level 1 rates. At $300,000 or more per month in commercial card volume, that’s a real number.

The reason software selection matters so much here is that the data has to flow automatically from wherever it’s created to the card network at settlement. Any break in that chain — missing fields, manual entry that doesn’t happen consistently, or a processor that isn’t configured to receive the data — results in a downgrade. This is why level 3 processing requirements apply to the entire payment stack, not just the processor.

What Genuine Level 3 Software Support Actually Means

When evaluating what software supports level 3 processing, there are four things that distinguish real support from nominal support.

First, the software has to capture all required line-item fields at the invoice or order level. Not just tax amount and PO number, but commodity codes, unit of measure, line-level discounts, freight, and ship-to address. Second, it needs to pass that data to the processor automatically at settlement without anyone on the AR team manually entering anything. Third, it should integrate natively with a payment processor that’s configured to submit level 3 data to the card network. Fourth, it should handle incomplete data gracefully, flagging gaps rather than silently downgrading the transaction.

If a platform requires custom application programming interface (API) development to activate level 3, or if it technically passes some fields but not all of them, that’s partial support at best. And partial support produces the same outcome as no support: transactions default to a lower interchange tier, and the savings evaporate.

The concept to keep in mind is the data chain. Level 3 qualification depends on an unbroken connection between the system where order data is created, the payment software that reads and transmits it, the processor that submits it, and the card network that applies the rate. The weakest link in that chain determines the tier the transaction lands at.

ERP Payment Integration Software

For CFOs, controllers, and AR managers evaluating level 3 processing software, ERP-integrated payment solutions are the strongest starting point, and the reason is straightforward: the data level 3 requires already exists in the ERP.

Every invoice in a properly configured ERP has product codes, quantities, unit prices, line-level tax, freight amounts, and customer PO numbers. That’s the full set of level 3 processing requirements right there, already captured as part of the normal invoicing workflow. An embedded payment solution that lives inside the ERP can read all of that data directly from the invoice record and submit it with the transaction automatically. No manual entry, no separate data mapping, no extra steps for the AR team.

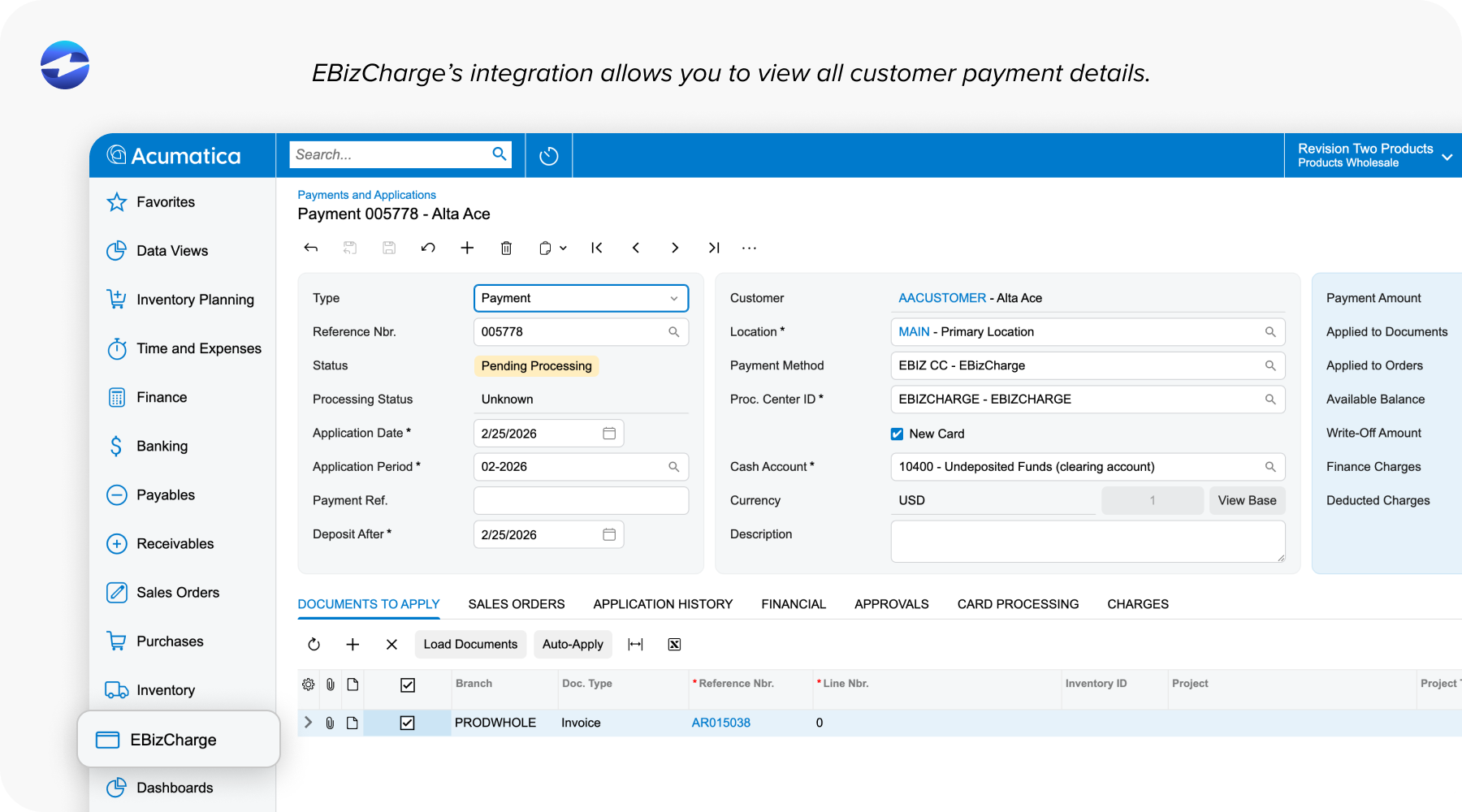

The major ERP platforms where level 3-capable payment integrations exist include NetSuite, Microsoft Dynamics (Business Central, Finance and Operations, and AX), Sage (Intacct, 100, 300, and 500), Acumatica, Epicor, Infor, and SAP Business One. Each of these environments captures the line-item data that level 3 needs. The question is always about the integration depth of the specific payment provider.

A payment provider that has built a native integration into the ERP, one that maps product codes, unit of measure, line-level tax, and freight from the invoice record directly to the transaction, will produce very different level 3 outcomes than one using a generic API connection. Ask any ERP payment provider specifically which fields are mapped and submitted at settlement. “We support level 3” is not a sufficient answer. The field-level detail is what matters.

Payment Gateway Software

Payment gateways sit between the merchant’s systems and the payment processor, transmitting transaction data at settlement. Many widely used gateways do include level 3 data submission capability in their API documentation, and on paper, that sounds like level 3 processing software.

The practical reality is different. Gateway-level level 3 support is almost always developer-dependent. The gateway can pass the required line-item fields if it has been specifically configured to do so, but that configuration doesn’t happen automatically for a standard merchant account. Someone has to build it, test it, and maintain it.

For a B2B company without dedicated engineering resources, a gateway that supports level 3 through its API but requires custom development to activate is functionally no different from one that doesn’t support it at all. The transactions still downgrade. The fees are still higher than they need to be.

When evaluating any gateway as part of a level 3 processing solution with low rates, the relevant question isn’t whether level 3 appears in the API documentation. It’s whether level 3 data is being submitted automatically and completely on every eligible transaction in a standard merchant account, without any custom development work from your team. If the answer to that is no, the gateway’s level 3 capability is theoretical rather than practical.

Accounting Software with Embedded Payment Features

Many accounting platforms include native payment processing features, and it’s worth understanding what those features can and can’t do for level 3.

Most accounting software with embedded payment functionality is built for small business and consumer-facing transactions. The interchange optimization built into those native payment tools rarely extends meaningfully to level 3 commercial card data. B2B companies processing significant corporate purchasing card volume through native accounting software payment features are typically defaulting to level 1 or level 2 rates with no reliable path to consistent level 3 qualification.

That said, accounting platforms are often excellent data sources for level 3. Most capture invoice-level line-item detail that covers the full set of level 3 processing requirements. The limitation isn’t the data; it’s the payment integration layer sitting on top of the accounting software.

Third-party payment integrations built specifically for a given accounting platform and connected to a level 3-capable processor offer a much more viable path. The accounting software provides the data. The right integration layer determines whether that data actually makes it to the card network at settlement.

Standalone B2B Payment Platforms

Dedicated B2B payment platforms are built specifically for commercial transaction environments, and level 3 support tends to be more reliable in this category precisely because the platforms are designed for the transaction types level 3 serves.

Where general-purpose gateways and consumer-oriented accounting tools treat level 3 as an edge case, B2B payment platforms treat it as a core requirement. Invoice-based payment flows, corporate purchasing card transactions, PO-driven purchasing, and multi-ERP environments are the default use cases, not an afterthoughts.

When evaluating a standalone B2B platform as a level 3 processing solution with low rates, the key questions are whether it has native integrations with your specific ERP or accounting system, whether level 3 data is captured from the invoice record automatically, and whether the provider can show documented experience processing corporate and government purchasing card transactions at level 3 rates. Ask for proof, not just claims.

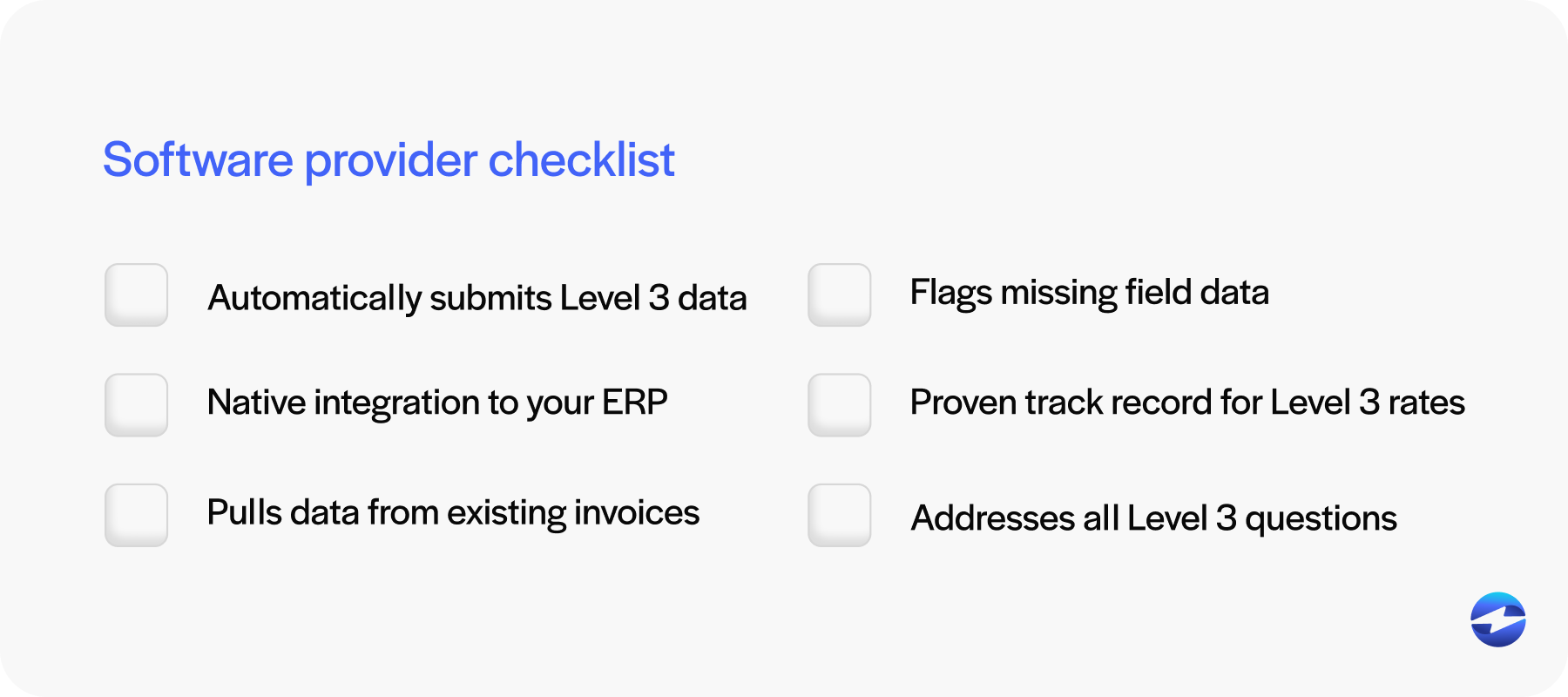

Questions to Ask Any Software Provider

Regardless of which category of software you’re evaluating, these questions will separate genuine level 3 processing software from surface-level claims.

Which specific line-item fields does your software capture and pass to the processor at settlement? Is level 3 data submitted automatically on every eligible transaction, or does it require manual input or custom development? Do you integrate natively with my ERP, and does that integration map line-item data from existing invoice records? How do you handle transactions where required fields are missing? Can you show me a processing statement demonstrating what percentage of eligible transactions qualified at level 3 rates?

A provider who genuinely supports level 3 credit card processing should answer all of those questions clearly and specifically. Vague responses or redirects to API documentation are worth paying attention to.

Building the Right Stack

Level 3 qualification depends on three components working together: a source system that captures line-item data, a payment integration that reads and transmits that data automatically at settlement, and a payment processor configured to submit it to the card network. The weakest link determines the outcome.

For most mid-market B2B companies, the most efficient path to all three components working correctly is choosing a payment processor whose software is built natively into the ERP environment they’re already using. The data is already there. The integration just needs to use it.

EBizCharge as a Level 3 Processing Solution

The landscape for software that supports level 3 processing is fragmented. Gateways require developer work. Accounting platforms have limited native support. ERP payment integrations vary significantly in depth depending on the provider. Knowing what software supports level 3 processing in a meaningful, automatic way narrows the field considerably.

The EBizCharge payment processing solution is purpose-built for this environment. It integrates natively into 100+ ERP, CRM, and accounting platforms, including NetSuite, Microsoft Dynamics, Sage, Acumatica, Epicor, Infor, and SAP Business One, and is specifically designed to capture and submit the full set of level 3 data fields at settlement without manual entry or custom development. With over 20 years in B2B payment processing, it’s built from the ground up for the commercial card transaction environments that level 3 serves.

For any B2B company evaluating a payment processing solution for level 3 support, start with the questions above. If your current software can’t answer them clearly, that’s the signal to look for something built specifically for the way B2B payments actually work.