Blog > AI in Payment Processing and Accounts Receivable (What 1,001 Financial Professionals Actually Think)

AI in Payment Processing and Accounts Receivable (What 1,001 Financial Professionals Actually Think)

Artificial intelligence (AI) is showing up in nearly every corner of the financial technology conversation right now. AI in the payments industry is promising smarter collections, faster reconciliation, and payment processes that practically run themselves. The pitch sounds good, but for the people responsible for processing payments every day, the reality looks quite different.

To get a clearer picture, we surveyed 1,001 financial decision-makers about artificial intelligence in payment processing and accounts receivable (AR).

Some of the findings confirm what you’d expect. Other results might surprise you.

Key Statistics

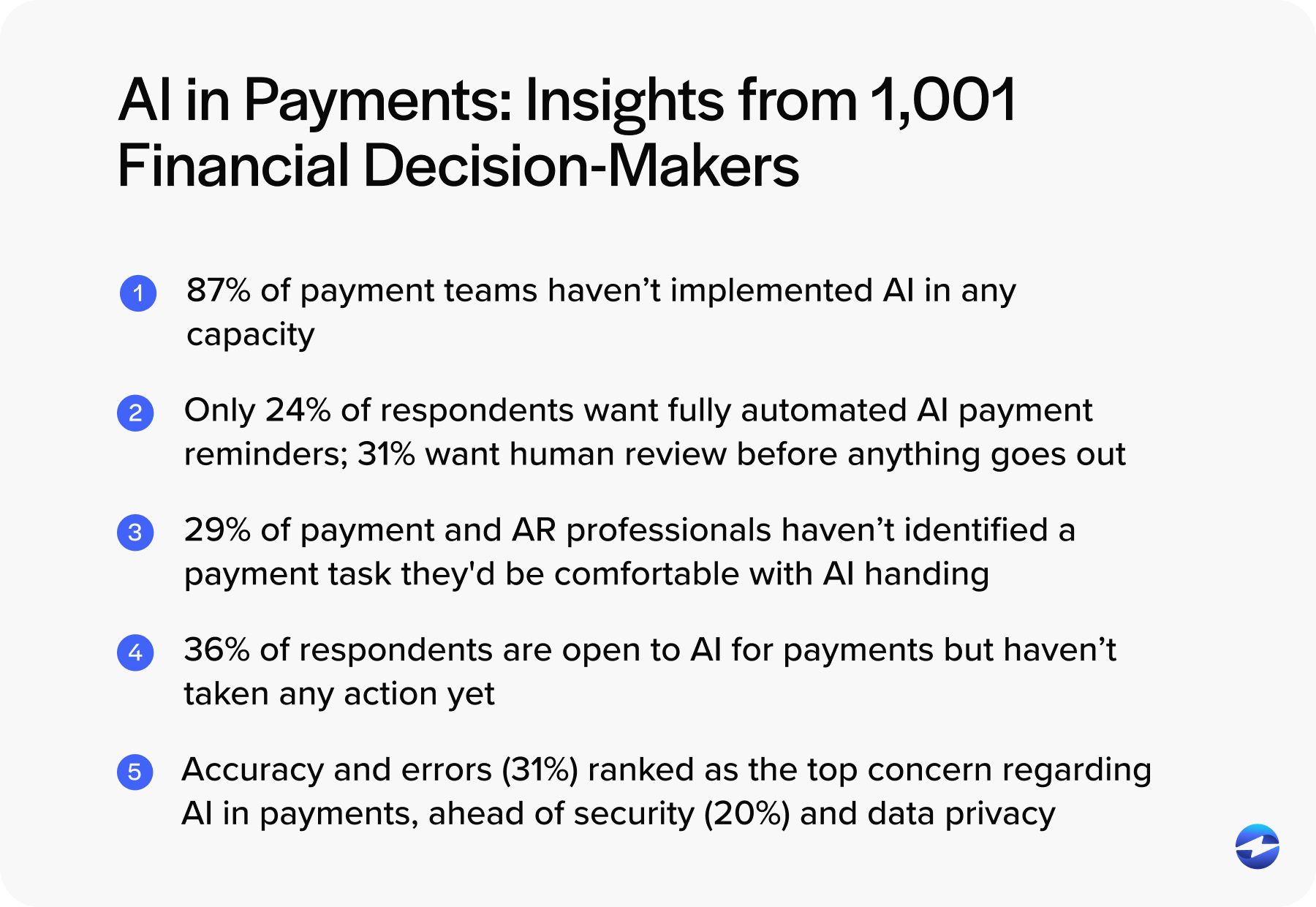

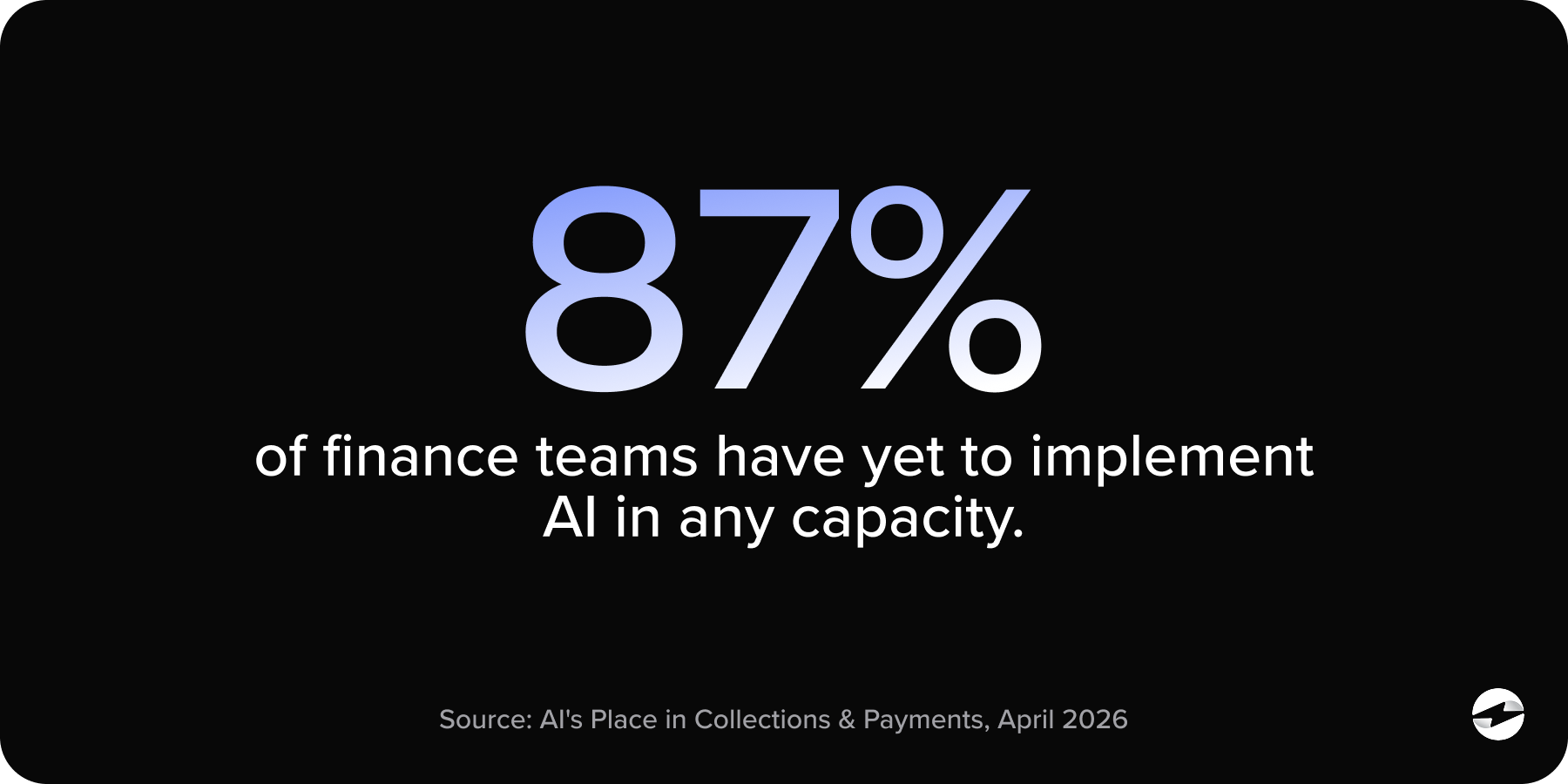

- 87% of payment teams haven’t implemented AI in any capacity

- Only 24% of respondents want a fully automated AI payment reminder workflow; 31% want human review before anything goes out

- 29% of payment and AR professionals haven’t identified a payment task they’d be comfortable with AI handling

- 36% of respondents are open to AI for payments, but haven’t taken any action yet

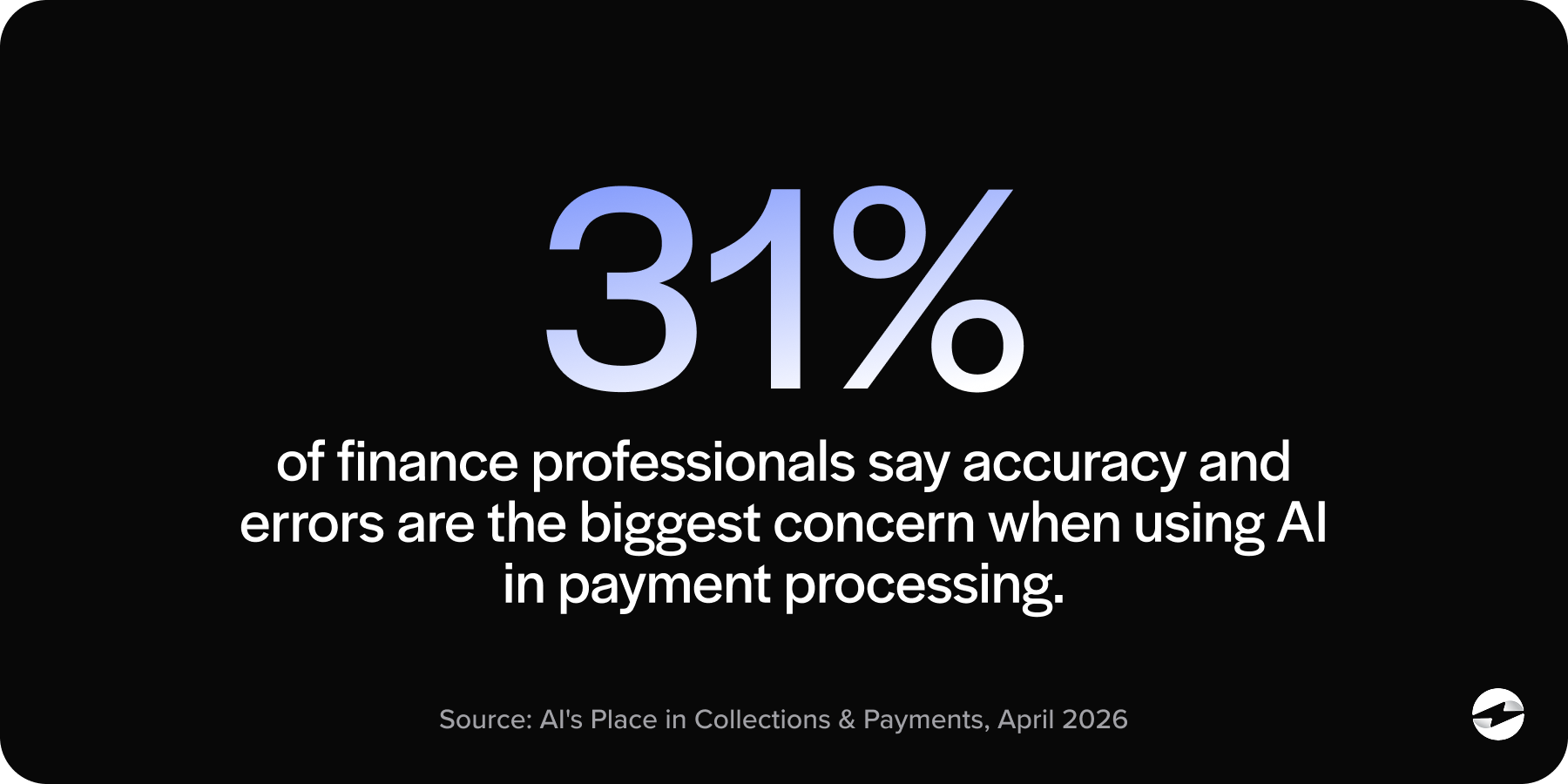

- Accuracy and errors (31%) ranked as the top concern regarding AI in payments, ahead of security (20%) and data privacy

- 1 in 5 payment professionals (21.6%) say customer reaction is a top concern with AI, placing it ahead of data privacy

- Cost ranks last among AI concerns at 9.7% (well behind accuracy, customer relationships, and security)

- Only 8.3% of businesses are actively using AI for payments or AR today

Methodology

This survey was conducted between November 2025 and April 2026. A total of 1,001 responses were collected across four questions covering AI task comfort, automation preferences, adoption concerns, and current usage status. Respondents were financial decision-makers involved in payment processing, accounts receivable, and collections within their company. Questions one through three received 1,001 responses each. Question four received 979 responses, reflecting a small drop-off at the final question.

The survey was designed to capture structured responses and open-ended write-ins. When relevant, open-text responses have been reviewed and incorporated into the analysis to add context beyond the multiple-choice data.

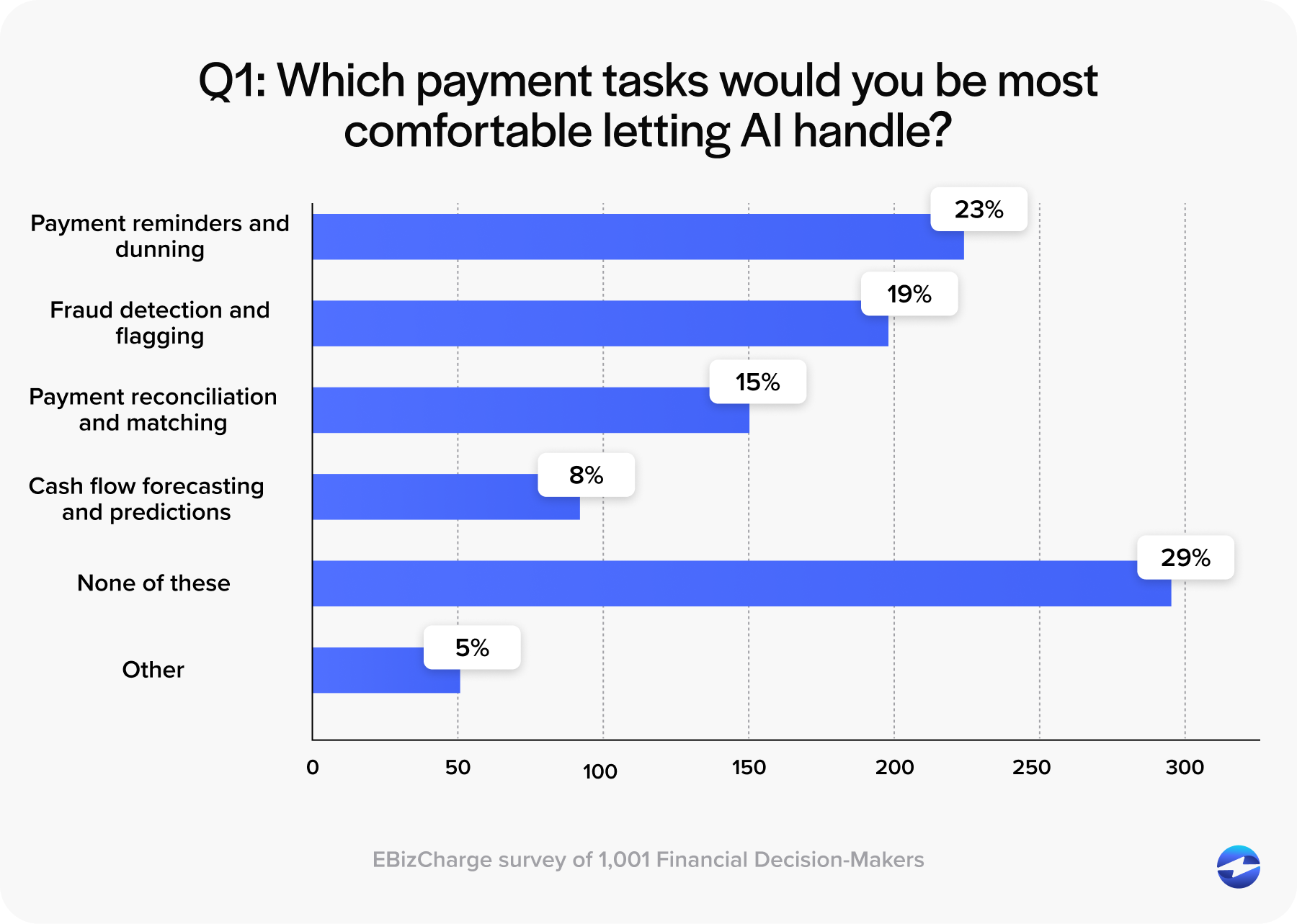

Q1: Which Payment Tasks Would You Be Most Comfortable Letting AI Handle?

The Question

Respondents were asked which payment-related tasks they felt comfortable delegating to AI.

Results:

- None of the above | 290

- Payment reminders and dunning | 234

- Fraud detection and flagging | 194

- Payment reconciliation and matching | 150

- Cash flow forecasting and predictions | 82

- Other | 51

Main Findings

The most common answer was “none of these,” selected by 290 respondents (29%), meaning nearly three out of ten finance professionals have yet to find a payment application they feel comfortable letting AI handle. These results may simply reflect an unidentified opportunity, tool, or use case, not necessarily a rejection of AI itself.

Among respondents who selected a task they would trust AI with, “payment reminders and dunning” came first at 23.4%. “Fraud detection and flagging” ranked second at 19.4%. “Payment reconciliation and matching” came in third at 15%, followed by “cash flow forecasting and predictions” at 8.2%.

Unexpected Findings

The ranking of fraud detection at number two is interesting. Fraud flagging is a high-stakes function since a false positive can block a legitimate payment, and a false negative can let fraud through. You may expect risk-averse finance professionals to hesitate here more than anywhere else on the list, but they didn’t.

The likely explanation is familiarity. AI-powered fraud detection has been embedded in consumer credit card networks for over a decade. Respondents may be more comfortable with AI identifying fraud, even if they’ve never implemented it in their own systems.

Takeaway

29% of respondents selected “none of the above.” For some, that may reflect a genuine resistance toward AI. For others, it may simply mean the right application has not come along yet.

For those who identified a task they’d feel comfortable letting AI handle, the ranking reveals a hypothesis about how trust works in this space: the more rule-based and predictable the task, the more comfortable people are handing it off. Reminders and dunning ranked first, and they follow a pattern. Forecasting ranked last as it requires AI to make a judgment call on something that hasn’t happened yet.

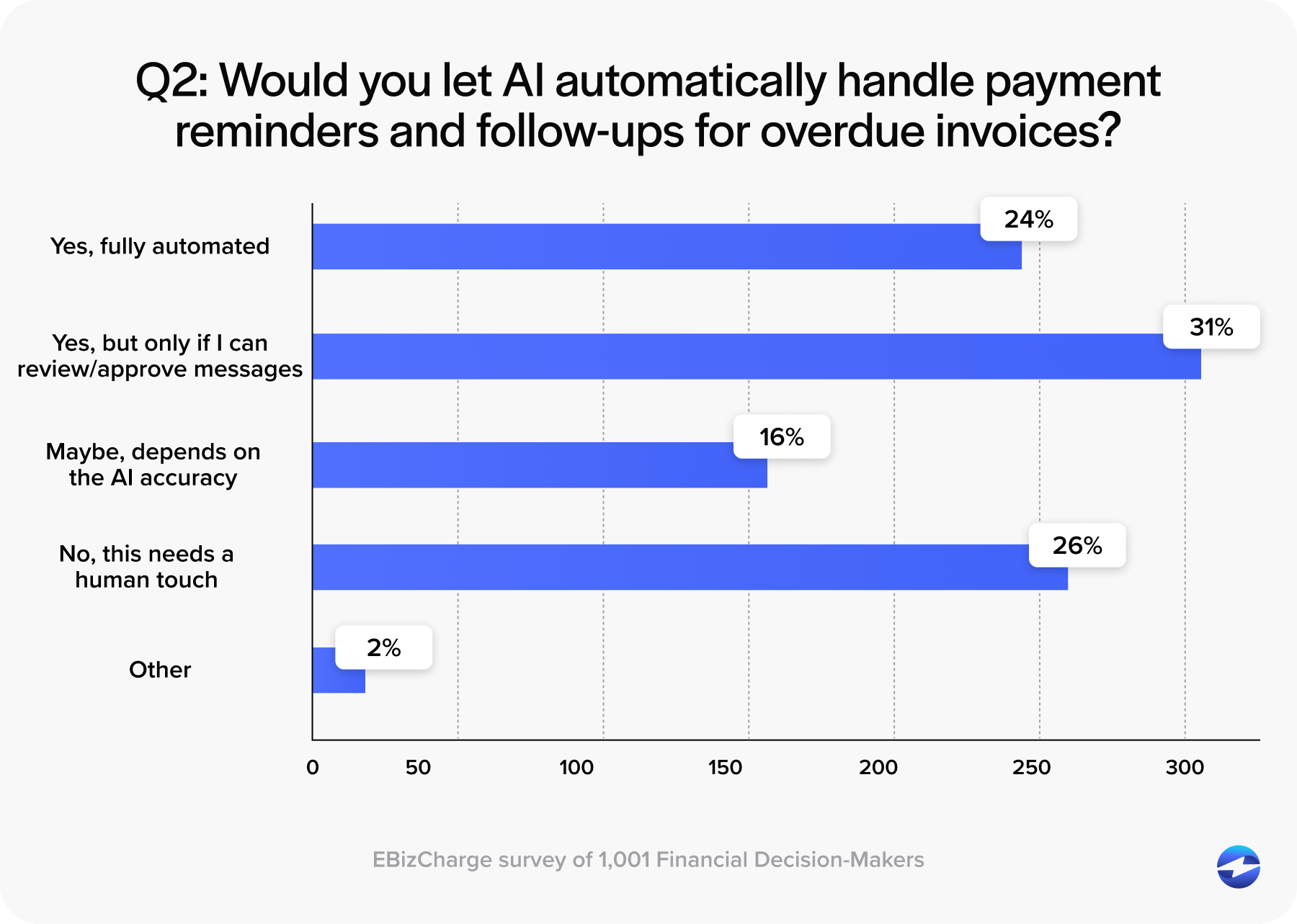

Q2: Would You Let AI Automatically Handle Payment Reminders and Follow-Ups?

The Question

Since payment reminders and dunning ranked as the most trusted AI task, respondents were asked a more specific follow-up question: Would you let AI automatically handle reminders and follow-ups?

Results:

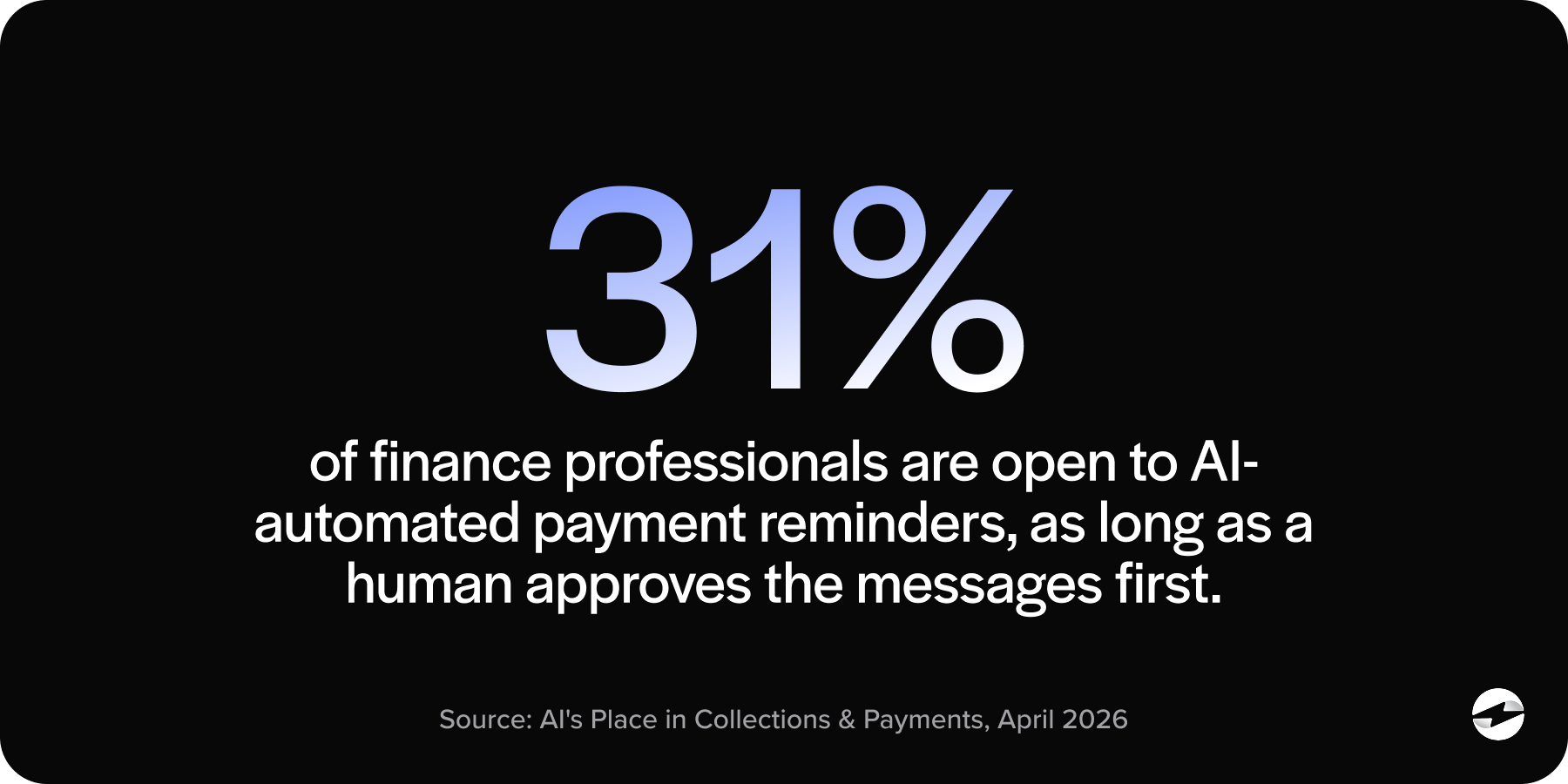

- Yes, but only if I can review/approve messages first | 308

- No, this needs a human touch | 265

- Yes, fully automated | 243

- Maybe, depends on the AI accuracy | 163

- Other | 22

Main Findings

The most common response, chosen by 309 participants (30.8%), was “yes, but only if I can review and approve messages first.”

The remaining results: 26.5% of respondents answered “no, this needs a human touch,” followed by full automation at 24.3% and “maybe, depends on AI accuracy” at 16.3%.

Altogether, 55.1% of respondents would allow AI to handle reminders in some capacity. The remaining 44.9% are either opposed or open to this technology on a conditional basis.

Unexpected Findings

In question one, respondents chose payment reminders as the task they were most willing to trust AI with. In question two, when asked if they’d commit to automating those reminders and follow-ups, only 24.3% said yes to full automation. The abstract comfort did not translate into operational confidence.

To expand this, 26.5% of respondents selected “No, this needs a human touch” as the second-highest response. In business-to-business (B2B) operations, for example, the customer receiving that reminder is often a long-term partner or a key decision-maker at a company representing significant revenue. The cost of a poorly timed or worded AI message can far outweigh the benefit of getting paid a few days faster.

One open-text response raised a fair challenge: “Those things were able to be done before AI. They are simple settings to change. Why would AI be necessary?” It’s a reasonable question since scheduled reminders and basic follow-up functionality have existed in AR software for years.

The honest answer is that not everything marketed as AI today actually uses this technology. The commercial benefits of genuine AI in payment processing show up in places like adjusting tone based on customer history, flagging accounts that need a personal call, or learning which timing sequences lead to more paid invoices. The value is real, but for most professionals, it has yet to be proven in practice.

Takeaway

The majority of finance professionals prefer supervised automation. Most respondents are open to AI for payment reminders and follow-ups but want human review before anything reaches a customer.

Full autonomy is a minority position. For any finance team evaluating AI-powered AR tools, the human approval workflow is not a nice-to-have feature. It’s the feature that will drive adoption for the largest segment of the market.

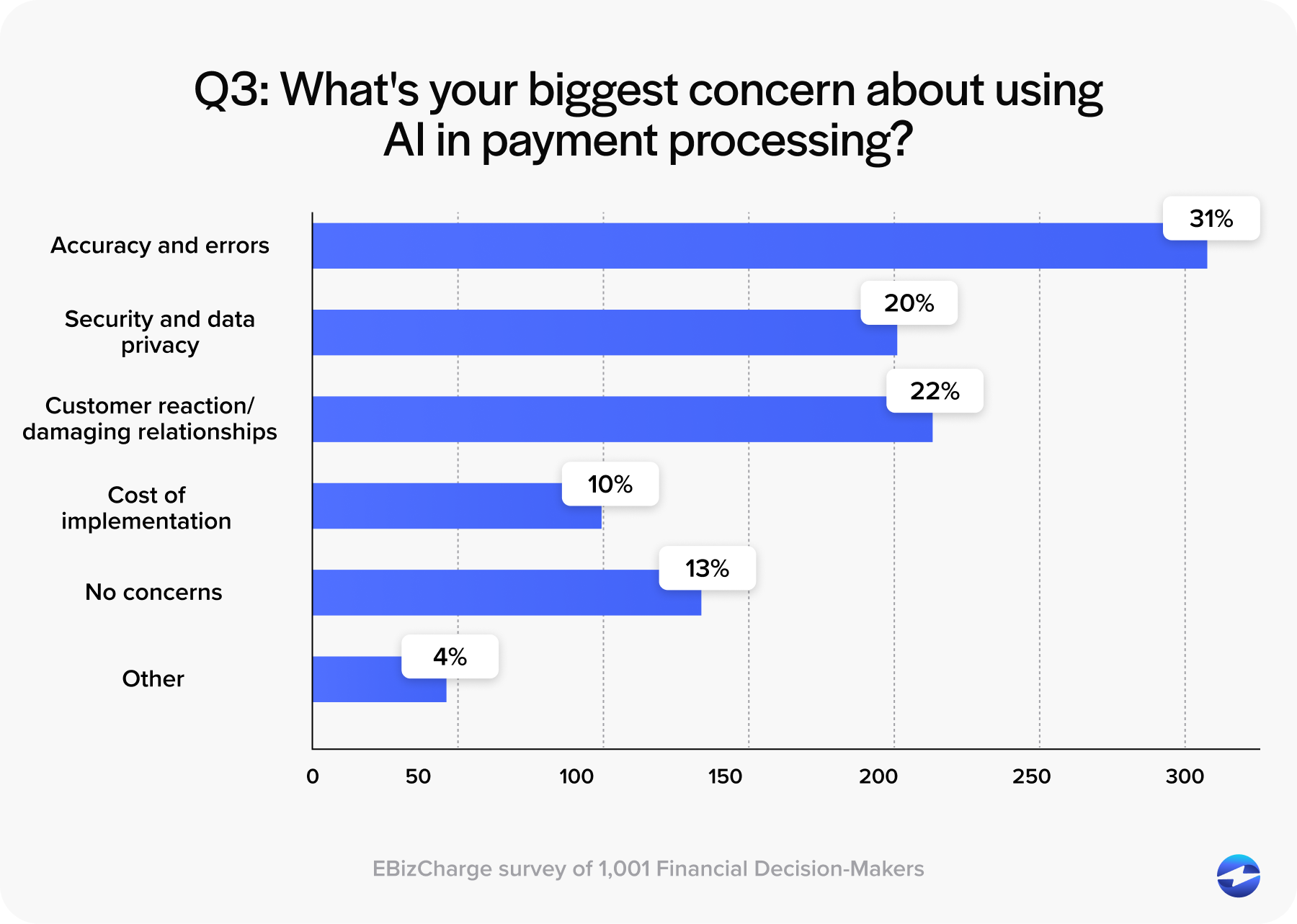

Q3: What’s Your Biggest Concern About Using AI Payment Processing?

The Question

Respondents were asked to identify their single biggest concern about using AI in payment processing.

Results:

- Accuracy and errors | 310

- Customer reaction and damaging relationships | 216

- Security and data privacy | 203

- No concerns | 135

- Cost of implementation | 97

- Other | 40

Main Findings

“Accuracy and errors” were ranked as the top concern by 310 respondents (31%). “Customer reaction and damaging relationships” came in second at 21.6%, followed closely by “security and data privacy” at 20.3%.

The “cost of implementation” ranked last among concerns at 9.7%. While 13.5% of respondents reported no concerns at all.

Unexpected Findings

Accuracy above security may be the most surprising finding in the entire survey. The payments industry has spent years building their infrastructures to ensure strong security and data protection. Responsible AI frameworks from major cloud providers reflect this same priority. PCI compliance, tokenization, encryption, and other safety standards often dominate conversations, yet the majority of survey respondents are more worried about AI making mistakes than about data breaches. The reasoning makes sense: a billing manager who sends an AI-generated invoice for the wrong amount owns that problem. Security breaches can feel external, but accuracy failures feel like your own mistake.

The second-ranked concern, “customer reactions and damaging relationships,” is equally noteworthy. Finance professionals are managing accounts, not just transactions. Tone-deaf dunning emails, automated follow-ups sent during contract negotiations, or messages sent at the wrong moment are mistakes that happen even with a human in the loop. Adding automation to the mix is not exactly a recipe for fixing that.

The “cost of implementation” ranking near the bottom of concerns indicates trust, accuracy, and relationship risks as the real barriers. If cost were the issue, the conversation would be about pricing and ROI. Instead, finance teams are likely asking about which safeguards are in place to ensure AI doesn’t act on bad information or contact a customer at the wrong moment.

Takeaway

The data reframes where the real barriers to AI adoption actually sit. Accuracy is the top concern, not security. Relationship risk ranks ahead of data privacy, and cost ranks last.

For finance teams weighing AI tools, the decision is less about budget and more about trust. The real question finance teams are asking is not about budget. It is whether the system can get it right, and whether it can do so without putting customer relationships at risk in the process.

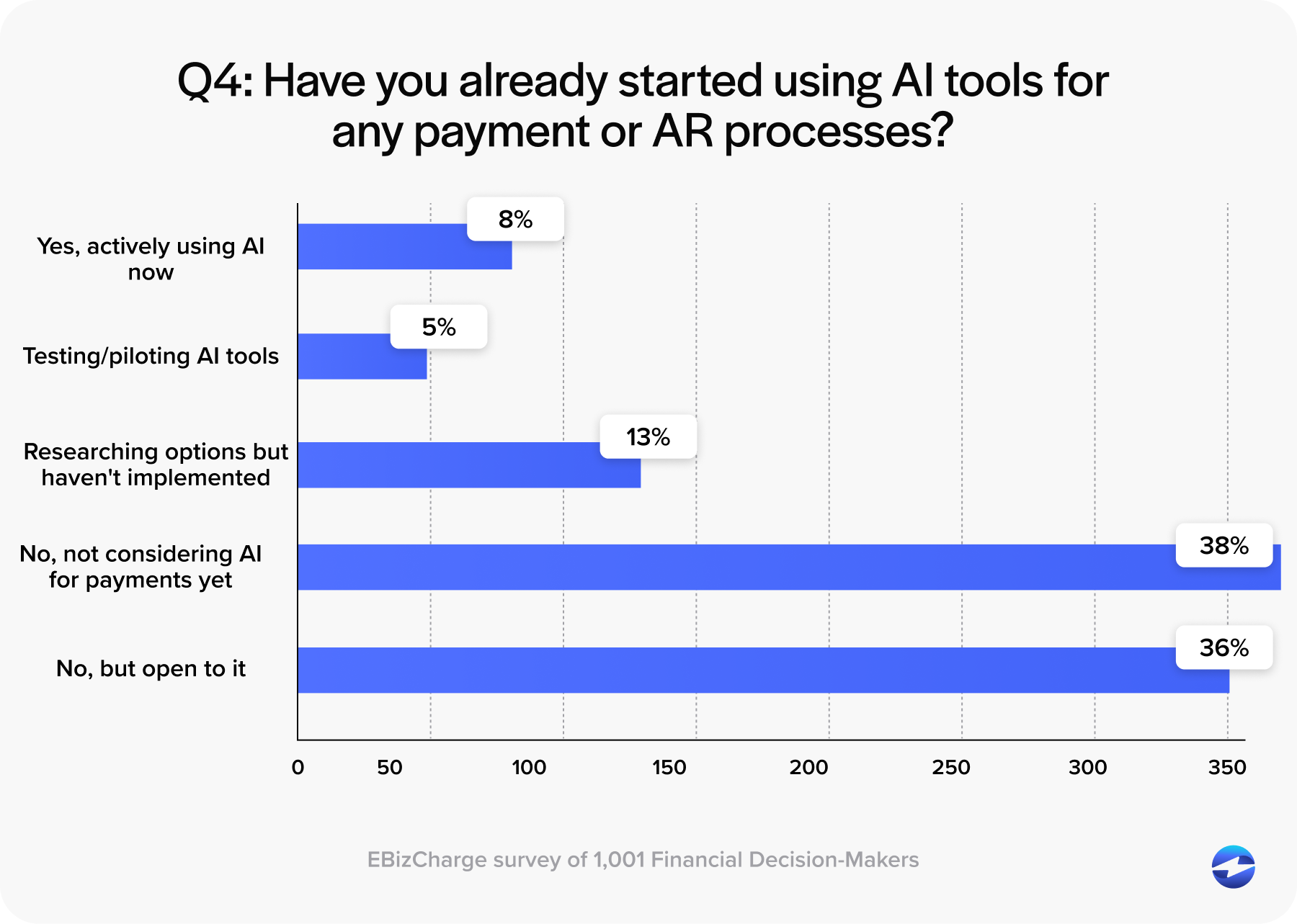

Q4: Have You Already Started Using AI Tools for Any Payment or AR Processes?

The Question

Respondents were asked to describe their current relationship with AI in the context of payment processing and AR.

Results:

- No, not considering AI for payments yet | 370

- No, but open to it | 352

- Researching options but haven’t implemented | 129

- Yes, actively using now | 81

- Testing/piloting AI tools | 47

Main Findings

370 finance professionals (37.8%) said they’re not considering AI for payments at this time.

Close behind, 352 respondents (36%) said they’re not currently using AI but are open to it. Another 129 respondents (13.2%) are researching options but haven’t yet implemented. Active AI users accounted for just 81 respondents (8.3%), and only 47 respondents (4.8%) are in AI testing or piloting phases.

Combined, only 13.1% of respondents are doing anything with AI in payments today. The other 86.9% have not moved past research or consideration.

Unexpected Findings

Among the 29% of respondents who said they would not hand any payment task to AI in question one, roughly 22% still identified themselves as open to AI in question four. Their resistance is task-specific, not technology-general. They are not opposed to AI in their business. They just have not been shown a payment application they trust yet.

That distinction matters more than the overall adoption numbers. It suggests the “not considering” group back in question one is not a wall. For a portion of them, the right use case has simply not presented itself yet.

Takeaway

The adoption gap between stated openness and actual implementation is wide. Roughly 62% of respondents fall somewhere on the spectrum from curious to active, yet only 13% have done anything.

The barrier is not cost or awareness, it’s trust. Respondents don’t want to risk implementing an AI workflow that creates relationship problems that are harder to fix than the efficiency gains are worth. Closing that gap requires demonstrating reliability in controlled, low-risk use cases before asking finance teams to commit to broader automation.

What the Data Tells Us

Taken question by question, the findings paint a picture of a market that’s paying attention but not yet moving. Taken together, they reveal something more specific.

The Trust Gap

There is a consistent trust gap running through all four questions. Most respondents are open to AI in payments and can identify the tasks they’d consider delegating. They even acknowledge that adoption is probably coming. What they are not willing to do is extend AI operational autonomy without proof that it can be trusted. AI that drafts, queues, and flags with a human review step before anything goes out is where most of these finance professionals are comfortable starting. You get the efficiency of automation without giving up the judgment calls that matter.

Accuracy Is the Real Barrier

The accuracy-over-security finding in question three reframes what the industry needs to prove. Everyone expects payment software to be secure. Accuracy is the variable many finance professionals are actually uncertain about, and uncertainty about accuracy translates directly into hesitation to adopt. Several open-text respondents also questioned whether AI in payment tools is really AI at all, or just rebranded automation logic that has existed for years. That skepticism reflects a real gap between how vendors describe their products and how users understand what they are actually buying.

Ready to Adopt, Given the Right Controls

One response in particular stands out: “We have special rules and exceptions for each customer. I would only want it to send automatic dunning messages if I could have a checkbox on each invoice to exclude them.” This respondent is not opposed to AI but is carefully examining their current workflow and identifying the specific accommodations their company would require. The market is full of people like this who are ready to adopt, given the right controls.

Where AI Powered Payment Processing Solutions Go From Here

The survey data points toward a future shaped less by full automation and more by collaboration between human judgment and machine efficiency.

Many financial professionals are waiting for evidence that AI can perform accurately in their environment without creating new problems to manage. The first AI applications to provide that evidence in a credible, verifiable way will define what AI in payments looks like for the next several years.

More than one in five respondents cited customer reactions and damaging relationships as their top fear, placing it ahead of data privacy and implementation cost. A human review step before anything reaches a customer goes a long way toward addressing that concern. Whether AI can fully earn that trust in customer-facing payment communication is still an open question, and it will remain one until real track records exist to point to.

What the survey makes clear is that the professionals closest to these payment tasks are not waiting passively. They have opinions and specific conditions. The market is not opposed to AI in payments. It’s just resistant to unproven AI in payments. The path forward runs through demonstrated accuracy, transparent limitations, and tools built by people who understand how payment workflows of businesses everywhere actually operate.

AR Automation Built for the Way Your Team Works

The survey data is clear: finance teams want automation that saves time without taking the wheel entirely. EBizCharge’s AR automation is built around that exact workflow.

Send payable invoices directly from your accounting software, automate payment reminders and follow-ups, and let customers pay through a self-service portal on their own time. When payments come in, they reconcile automatically back into your system with no manual entry required.

EBizCharge connects natively to 100+ enterprise resource planning (ERP), customer relationship management (CRM), eCommerce, and accounting platforms, so it fits into the systems your team already uses rather than adding another one to manage. One customer reduced their average DSO from 45 days down to 5.

Get a demo today to see how it works.

Frequently Asked Questions

Are businesses actually using AI for payments and accounts receivable yet?

Not at scale. According to EBizCharge’s survey of 1,001 financial decision-makers, only 8.3% of businesses are actively using AI for payment or AR processes today. Another 4.8% are in testing or piloting phases. The remaining 86.9% have not implemented AI in any capacity, though 36% say they are open to it and 13.2% are actively researching options. The interest exists across the market. The implementation does not.

What is holding businesses back from adopting AI in payment processing?

Trust, not cost. EBizCharge’s survey found that cost of implementation ranked last among concerns at just 9.7%. The top barriers are accuracy and errors at 31%, customer reaction and damaging relationships at 21.6%, and security and data privacy at 20.3%. Finance professionals are less worried about what AI adoption will cost them and more worried about whether AI will perform reliably without putting customer relationships at risk in the process.

What payment tasks are finance professionals most willing to let AI handle?

Payment reminders and dunning ranked first at 23.4%, followed by fraud detection and flagging at 19.4%. Notably, 29% of respondents selected none of the above.

Do finance teams trust AI to send payment reminders automatically?

Most do not, at least not without oversight. EBizCharge’s survey found that only 24% of finance professionals want fully automated AI payment reminders. The largest group, 31%, said they would allow AI to handle reminders only if a human could review and approve messages before anything went out. Another 26.5% said the task needs a human touch entirely. The dominant preference is supervised automation, not full autonomy.

What are finance professionals most concerned about when it comes to AI in payments?

Accuracy ranks first. According to EBizCharge’s survey, 31% of finance professionals said accuracy and errors was their single biggest concern with AI in payment processing. This places accuracy ahead of security and data privacy at 20.3%, and also the cost of implementation at 9.7%. The reasoning is straightforward: a billing manager who sends an AI-generated invoice for the wrong amount owns that problem directly. Security breaches can feel external. Accuracy failures feel personal.

Why do finance professionals rank accuracy above security as their top AI concern?

The payments industry has spent decades building security infrastructure. PCI compliance, tokenization, and encryption standards have become baseline expectations for any payment tool, which means security is largely treated as a given rather than a variable. Accuracy has no equivalent track record yet in AI-powered workflows. Finance teams have no established benchmark for how reliably an AI system will match payments, generate invoices, or time collections outreach. That uncertainty is what we contribute the 31% accuracy concern reflects.

Is AI in payment processing the same as AI in banking?

They overlap but operate in different contexts. AI in banking typically refers to large-scale applications like credit scoring, algorithmic trading, risk modeling, and fraud detection across consumer accounts.

AI in payment processing, particularly in B2B environments, focuses on more operational functions: automating invoice delivery, matching incoming payments to open invoices, timing and personalizing collections outreach, and reducing manual reconciliation work. The stakes in B2B payment processing also carry a relationship dimension that consumer banking does not. A poorly handled AI-generated collections message in a B2B context can damage a long-term customer relationship in a way that has no real equivalent in consumer banking.

What payment tasks are finance professionals most concerned about handing to AI?

Cash flow forecasting and predictions ranked last among tasks finance professionals would trust AI with, selected by just 8.2% of respondents. The likely reason is that forecasting requires AI to make predictions about future outcomes rather than react to existing data. Every other task on the list, reminders, fraud detection, reconciliation, involves AI acting on something that has already happened. Asking AI to predict something that hasn’t happened yet, and then making financial decisions based on that prediction, requires a level of trust that most respondents have not yet extended.

How does AI fraud detection in payments work?

AI fraud detection works by analyzing transaction patterns in real time and flagging activity that deviates from established norms. Machine learning models are trained on large volumes of historical transaction data to identify signals associated with fraudulent behavior, such as unusual transaction amounts, unfamiliar geographic locations, atypical timing, or patterns inconsistent with a customer’s history. When a transaction triggers enough of these signals, the system flags it for review or blocks it automatically. This capability has been embedded in consumer credit card networks for over a decade, which likely explains why fraud detection ranked second among tasks finance professionals are comfortable delegating to AI in EBizCharge’s survey, despite being a high-stakes function.

What does supervised automation mean in payment processing?

Supervised automation refers to workflows where AI handles the preparation and queuing of actions while a human retains approval authority before those actions execute. In an AR context, this might mean AI drafts and queues payment reminders based on account status and history, but a team member reviews and approves the outreach before it reaches the customer. EBizCharge’s survey found this is the preferred adoption model for most finance professionals, with 31% specifically selecting the option to use AI for reminders only if they could review messages first. It captures efficiency gains without removing human judgment from the decisions that carry the most consequence.