Blog > Credit Card Surcharge: What It Is, How It Works, Types, and Examples

Credit Card Surcharge: What It Is, How It Works, Types, and Examples

What is a surcharge?

A surcharge, also known as a checkout fee, is an additional fee that merchants charge customers to offset the cost of processing credit card payments.

Each time a business accepts a credit card payment, they pay a small fee (either a percentage or a fixed rate) to various entities, including the card brand (Visa, Mastercard, American Express, etc.) and the credit card processor. Small businesses may find this credit card processing fee a barrier to accepting credit cards from their customers. But with a surcharge, businesses are able to pass the costs of accepting credit cards onto customers, allowing their business to have zero cost processing.

The major card brands have a negative view of surcharging, as it adds costs for customers and may discourage them from purchasing. However, when done thoughtfully, surcharging can be a benefit to both businesses and customers.

For example, some customers may want the added convenience of paying via credit card versus cash and would be happy to pay a small fee for the ease of use. Businesses that would otherwise not be able to afford credit card processing can leverage surcharging to offer additional payment methods to their customers.

What is a credit card surcharge fee?

A credit card surcharge fee is the specific amount a merchant adds to a transaction when a customer pays with a credit card. It exists to cover the interchange fees, assessment fees, and processor markup that the merchant would otherwise absorb. Most credit card surcharge fees fall somewhere between 1.5% and 4%, depending on the card brand and the merchant’s processing agreement.

One thing worth knowing is that surcharge fees only apply to credit card transactions. Debit cards, prepaid cards, and cash payments cannot be surcharged under current card brand rules. So if a customer swipes their debit card, the surcharge does not apply to that transaction, even if it runs through a Visa or Mastercard network. This distinction trips up a lot of merchants who are new to surcharging.

The fee itself should reflect the merchant’s actual cost of processing, not a round number pulled out of thin air. Visa caps surcharges at 3% of the transaction amount as of April 2023. Mastercard’s cap is currently 4%, though a pending settlement from November 2025 could bring it down to 3% as well. In practice, most merchants set their surcharge at or below 3% to stay compliant across both networks. Regardless of the cap, the surcharge can never exceed the merchant’s actual cost of acceptance, whichever is lower.

Why do businesses charge surcharges?

Businesses charge surcharges because credit card processing is not free. Every time a customer taps, swipes, or enters a card number, the merchant pays a processing fee that typically ranges from 1.5% to 3.5% of the transaction. For a business processing $500,000 in credit card sales per year, that can add up to $7,500 to $17,500 in fees annually. Surcharging shifts some or all of that cost to the cardholder.

This is especially common in industries with tight profit margins. Think medical offices, government agencies, utility companies, and B2B businesses where invoice amounts are large and the processing fees on a single transaction can run into the hundreds of dollars. For these merchants, absorbing processing fees on every transaction eats directly into their bottom line.

The option to surcharge also became more accessible after a 2013 class action settlement allowed merchants in most states to pass credit card fees to customers. Before that settlement, card brand rules prohibited it. Since then, surcharging has grown steadily as more businesses look for ways to manage their cost of doing business without raising prices across the board.

Is surcharging legal?

Surcharging is currently legal only on a state-by-state basis. Some states allow surcharging, while others don’t. Businesses in New York, California, Florida, and Texas have each brought the issue to court, demonstrating the strong feelings that surcharging elicits in both customers and businesses. When determining if surcharging is right for your business, first check the laws regulating surcharging in your state.

Common regulations include:

- Merchants can’t profit off of surcharging. Visa caps surcharges at 3% and Mastercard’s cap is currently 4%. Regardless of the network cap, the surcharge can never exceed the merchant’s actual cost of accepting the credit card, whichever is lower.

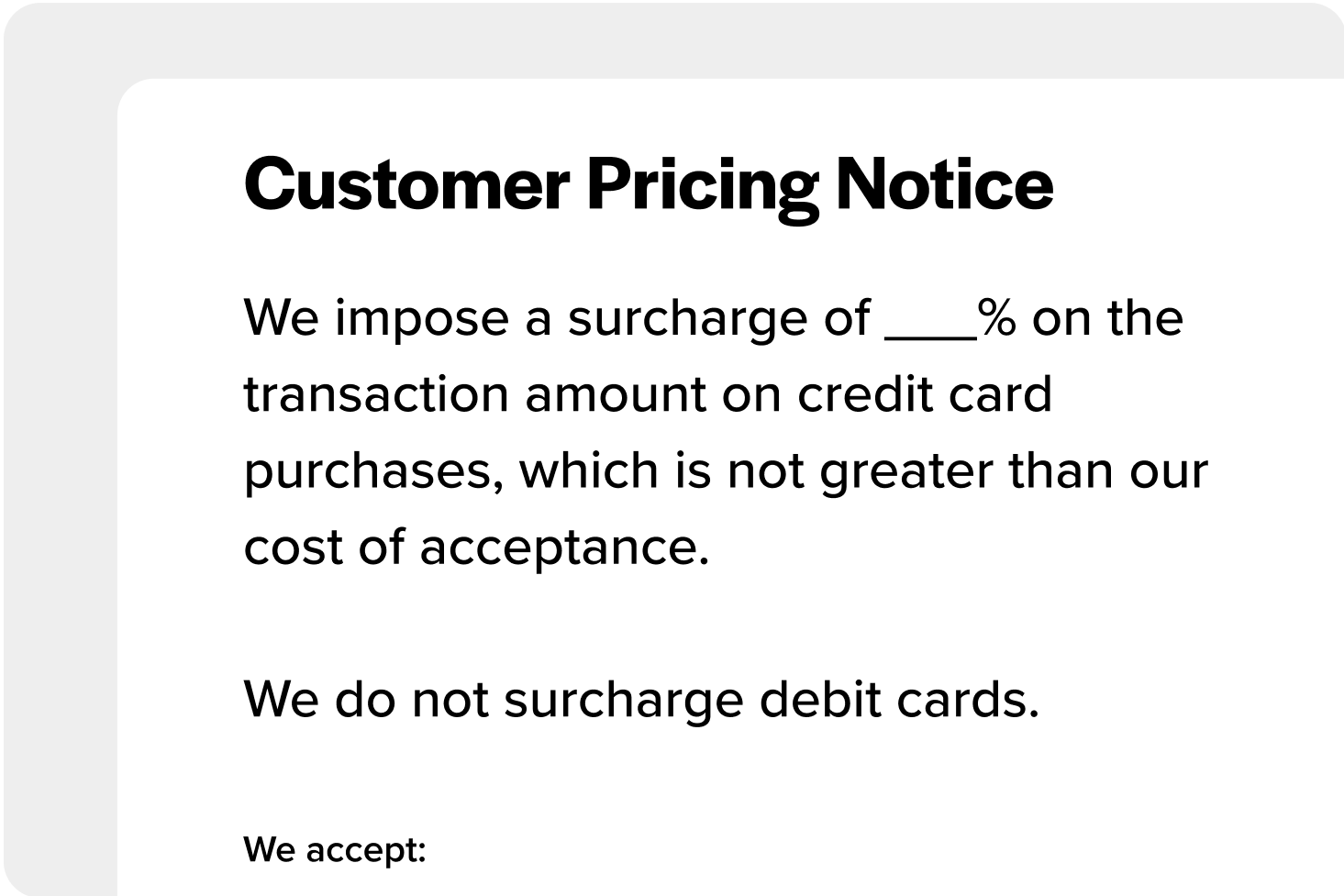

- Before beginning to surcharge, merchants must provide notice, typically 30 days in advance, to the card brands and other relevant parties.

- Merchants must notify their customers about surcharges. In a physical store, this means clear signage at the cash register. On a website, this means a disclaimer on the checkout page.

- Merchants must itemize the surcharge on receipts and invoices.

- Merchants can’t privilege certain card brands over others. For example, if they impose a 2% surcharge on American Express cards, then they must apply that same percentage to all other card brands.

Card brands may alter these regulations at any time, so be sure to research the most recent requirements for surcharging.

Who pays the surcharge?

The customer pays the surcharge. When a merchant applies a surcharge to a credit card transaction, the additional fee appears as a separate line item on the customer’s receipt. So if a purchase totals $100 and the merchant applies a 3% surcharge, the customer pays $103. The merchant then uses that extra $3 to cover all or part of the credit card processing fee they owe their payment processor.

From the customer’s perspective, they always have the option to avoid the surcharge by paying with a different method. Debit cards, cash, and checks are surcharge-free. Merchants are required to disclose surcharges before the transaction, so customers should know about the fee and have time to choose their preferred payment method.

Pros and cons of surcharging

There are two main benefits to surcharging customers:

- Surcharging helps merchants recoup the cost of accepting credit card payments and may even allow them to accept credit card payments in the first place.

- Surcharging allows merchants to offer additional, more convenient payment methods to customers.

On the flip side, there are two main drawbacks:

- Customer opinion. If customers see that you’re imposing a surcharge and don’t like it, they may take their business elsewhere. The decision to surcharge could negatively affect your business’s reputation.

- Rules and regulations. The burden is on the merchant to do their research and stay compliant with all state laws and card brand regulations.

Each merchant must weigh these pros and cons before deciding if surcharging is the right decision for their business.

Credit card surcharge examples

Here’s how a surcharge looks in practice. Say a plumbing company charges $500 for a service call. Their credit card processing fee is 2.9%. If they surcharge at 2.9%, the customer’s total becomes $514.50 when paying by credit card. If the customer pays by check or cash, they pay the original $500.

For a B2B distributor invoicing $10,000 in product, a 3% surcharge adds $300 to the credit card total. That $300 goes directly toward the processing cost the distributor would have otherwise absorbed.

| Transaction Amount | Surcharge Rate | Surcharge Fee | Customer Total |

|---|---|---|---|

| $100 | 3% | $3.00 | $103.00 |

| $500 | 2.9% | $14.50 | $514.50 |

| $10,000 | 3% | $300.00 | $10,300.00 |

How to add a surcharge to credit card payments

If your business decides to move forward with surcharging, you can use a payment integration like EBizCharge to automatically add a surcharge to all your transactions. Using a payment integration means you won’t have to manually calculate a surcharge with every transaction; you simply set up the surcharge as either a percentage or a dollar amount, and the integration automatically adds it to the transaction.

What should I do if surcharging is illegal in my state?

If surcharging is illegal in your state or if your businesses has decided surcharging isn’t the way to go, but you’re still struggling with the cost of accepting credit card payments, it’s time to work on those fees.

Merchants can lower their credit card processing fees in a number of ways:

- Change the pricing model. There are several different credit card processing pricing models. Each model has pros and cons and are better suited to different business types. If you’re using a pricing model that doesn’t make sense for your business, then switching to a different pricing model may cut costs.

- Change the way you accept cards. Collecting AVS data, using EMV chip readers instead of manual entry, and matching your preauthorization and capture amounts can all help lower your interchange rates. B2B merchants should also look into Level II and Level III processing, which passes additional transaction details like tax amounts and line-item data to qualify for lower rates. These small adjustments add up to meaningful savings, especially on high-volume or large-ticket transactions.

- Negotiate with your processor. Ultimately, if you’re unhappy with your credit card processing fees, it’s worth it to speak with your credit card processor and discuss options.

- Get a quote from a different processor. If you think you’re paying too much for credit card processing, do some comparison shopping. The quotes you receive will help you assess if your fees are truly too high.

- Use a payment integration to automatically lower costs. A payment integration allows you to accept credit card payments directly in your accounting software. In addition to using automation to simplify the accounting workflow, payment integrations also automatically lower your credit card processing costs. Solutions like EBizCharge offer QuickBooks credit card integration and payment processing for Epicor, so you can process transactions, apply surcharges, and reconcile payments all within the software you already use.

So, what is a surcharge? It’s up to the merchant

While surcharging may involve a lot of forethought, merchants can still do it in a responsible way that benefits their business. Ultimately, each merchant must consider the pros and cons of surcharging and decide what makes the most sense for their business. If you’re ready to get started, EBizCharge offers a surcharge program that automates the entire process, from calculating the correct surcharge amount to applying it at checkout and keeping your transactions compliant across all major card brands.

Frequently Asked Questions

Is a surcharge a one-time payment?

Yes. A surcharge applies per transaction. Each time a customer pays with a credit card, the surcharge is calculated on that specific purchase amount. It does not carry over or repeat.

What does “surcharge-free” mean?

Surcharge-free means the merchant does not add any extra fee to credit card transactions. The price the customer sees is the price they pay, regardless of how they choose to pay.

What is a terminal surcharge?

A terminal surcharge refers to the surcharge applied at the point of sale terminal when a customer pays in person with a credit card. The terminal is typically configured to automatically calculate and add the surcharge to the transaction total.

Can a business profit from surcharging?

No. Card brand rules require that the surcharge amount does not exceed the merchant’s actual cost of processing the credit card payment. Visa’s cap is 3% and Mastercard’s is currently 4%, though a pending 2025 settlement could align both at 3%.

Is a surcharge the same as a processing fee?

Not exactly. A processing fee is what the merchant pays to their payment processor. A surcharge is what the merchant passes along to the customer to cover that processing fee. The surcharge is the customer-facing charge; the processing fee is the behind-the-scenes cost.