Templates | Cash Discount Signage

Printable Cash Discount Sign Templates

Printable Cash Discount Sign Templates

Download free, ready-to-print cash discount signs built to meet card network disclosure requirements. Whether you’re running a 3% or 4% cash discount program, these templates are formatted to post at your entrance and point of sale so your program stays compliant from day one.

Download free, ready-to-print cash discount signs built to meet card network disclosure requirements. Whether you’re running a 3% or 4% cash discount program, these templates are formatted to post at your entrance and point of sale so your program stays compliant from day one.

Get Your Free Cash Discount Sign Template

Posting the right signage is one of the most important steps in running a compliant cash discount program. These templates are free to download, print-ready, editable, and formatted to cover both your entrance and your point of sale. No design work needed.

What is a Cash Discount Program?

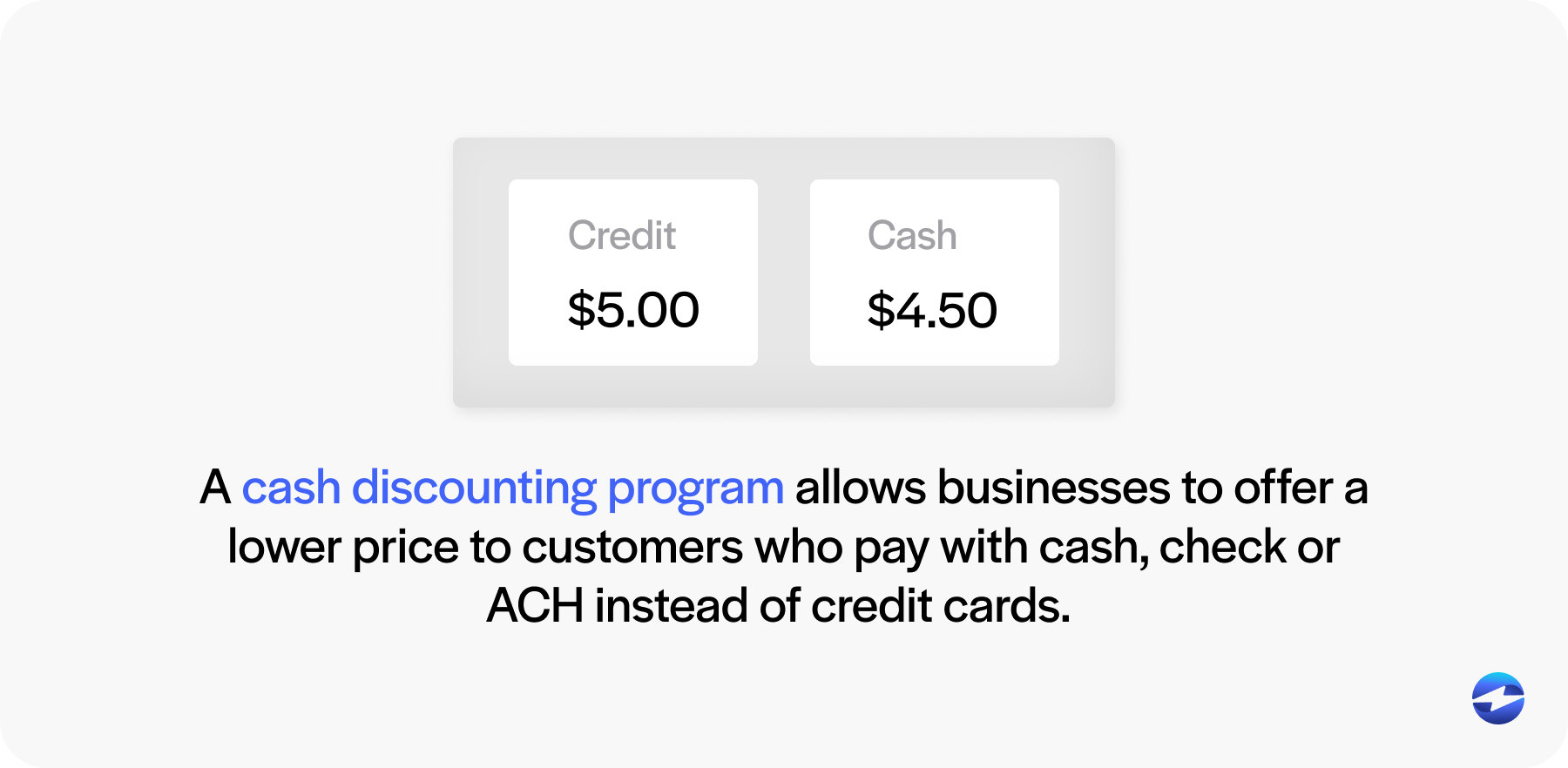

A cash discount program is a pricing setup that lets merchants offer a slightly lower price to customers who pay with cash instead of a credit or debit card. The card price is set as the standard price, and cash-paying customers receive a discount off that amount at the point of sale.

This is different from surcharging. With surcharging, you start with a base price and add a fee on top for card payments. With a cash discount program, you do the reverse. You build the cost of card acceptance into your standard pricing and then reward customers who help you avoid that cost. That distinction matters, and it has real implications for how your program needs to be structured and disclosed.

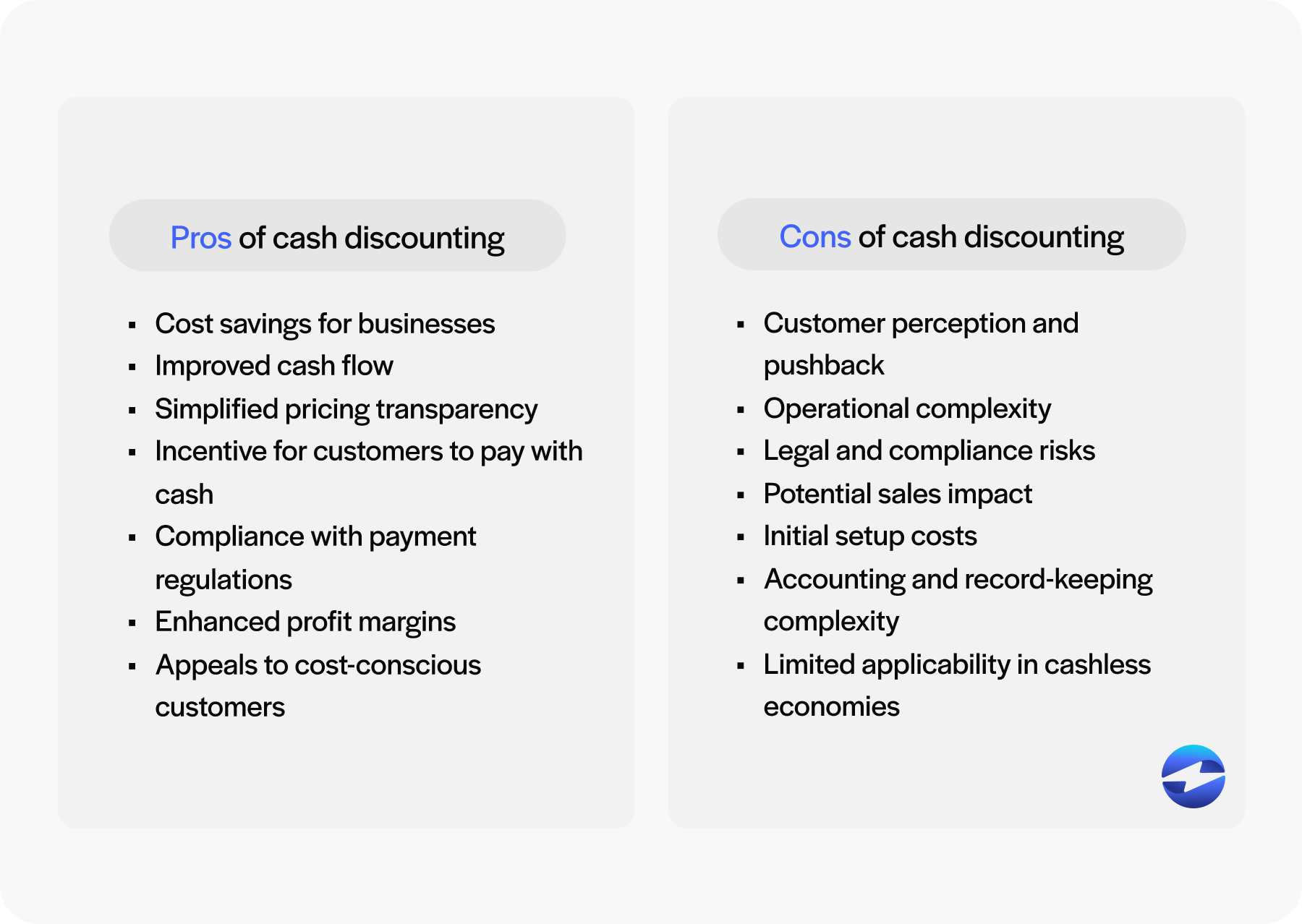

For business owners dealing with thin margins, a merchant cash discount program is one of the more practical ways to offset processing costs without simply raising prices across the board. It puts the choice in the customer’s hands rather than silently absorbing a fee on every transaction.

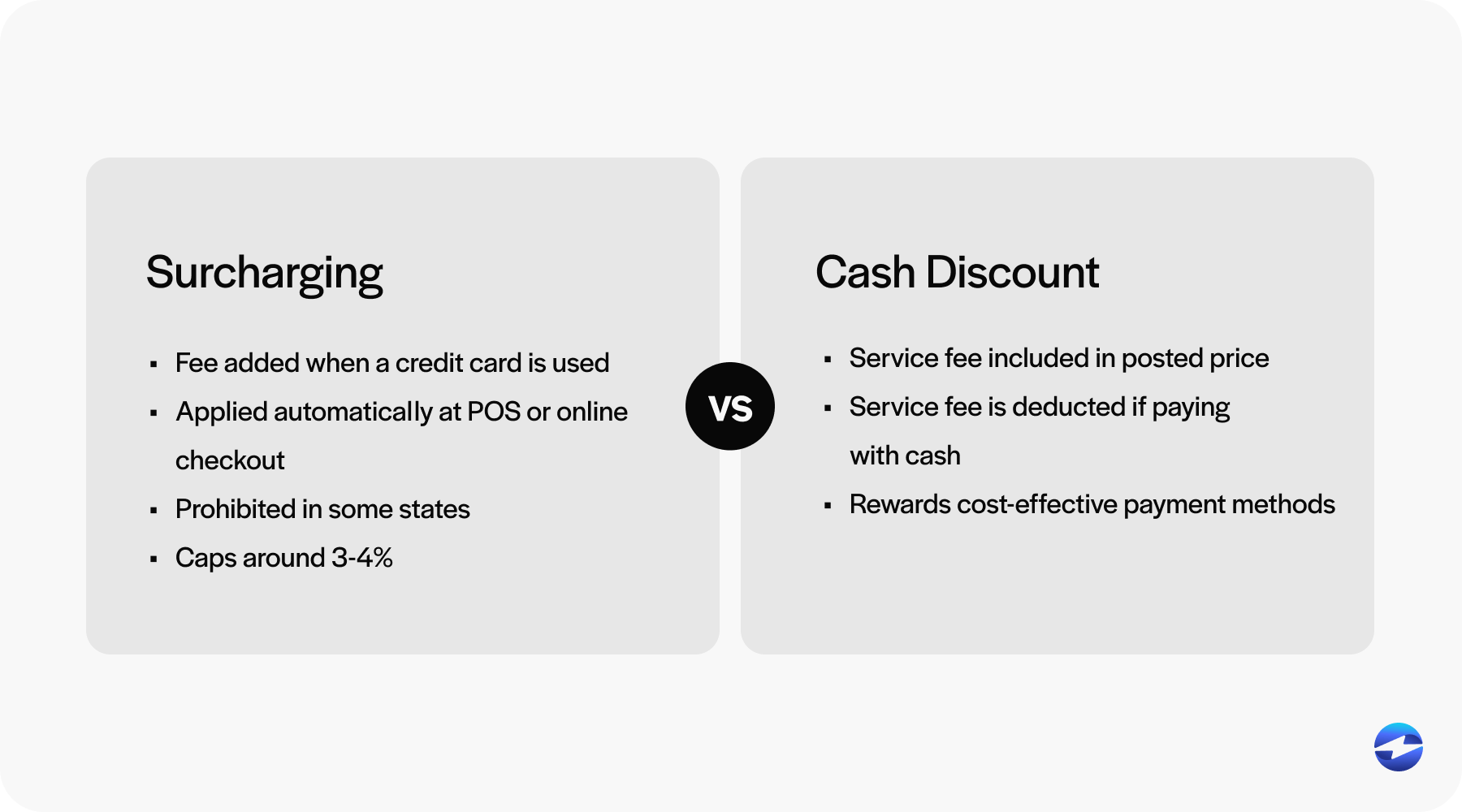

Cash Discounting vs. Surcharging: What’s the Difference?

A lot of merchants confuse cash discounting with surcharging, and it’s easy to see why. Both involve the cost of card processing. Both affect what customers pay at checkout. The difference is in how each program is framed and regulated.

Surcharging means adding a fee on top of a stated base price specifically for card payments. It is subject to stricter rules, card network approval requirements, and state-level restrictions that vary widely.

Cash discounting works the other way. The card price is the standard price, and cash customers receive a discount off it. This framing gives merchants more flexibility and avoids many of the compliance hurdles that come with surcharging. Most processors that offer a merchant cash discount program are specifically structured around this distinction to keep merchants compliant.

If you’re a finance manager, controller, or business owner researching whether cash discounting credit card processing is right for your operation, the short answer is that it depends on your customer mix, your transaction volume, and your state’s rules.

What is a Cash Discount Sign?

A cash discount sign is the required customer-facing notice that informs shoppers of your pricing structure before they reach the register. It needs to communicate that a cash price and a card price exist, explain the discount amount, and give customers enough information to make an informed decision about how they want to pay.

Cash discount signage is not optional. Visa, Mastercard, and most major card networks require merchants enrolled in a cash discount program to post compliant disclosures at the entrance to their business and again at the point of sale.

A 3% cash discount sign, for example, would communicate that customers paying by card are charged the standard listed price, and customers paying with cash receive 3% off that amount. A 4% cash discount sign follows the same logic, just at the maximum rate most processors allow. The format can vary, but the disclosure must be visible, accurate, and placed where customers see it before committing to a purchase.

Failing to post proper signage can put your entire program out of compliance. Some merchants treat this as a formality. It is not.

Cash Discount Signage/Disclosure Rules

- Post Prices at Entry & Point of Sale: Signs must be visible when customers arrive (door, entrance, menu, etc.) and at the point of purchase. Disclosure only at checkout is not sufficient under most card network rules.

- Frame It as a Discount, Not a Fee: The card price must be positioned as the “regular” or “standard” price. Framing it the other way around – as a “credit card surcharge” – triggers separate, stricter surcharging rules.

- Show the Discount Amount or Percentage: Customers must know exactly what they save by paying cash. Display either the discount percentage or both prices (cash price vs. card price). Vague language like “you may save money” is not sufficient.

- Cap the Discount at 4%: Cash discount programs through most processors and card networks cap the discount at 4% of the transaction total. Check your specific processor agreement. Amounts above this threshold may not be permissible.

- State Law Varies: While cash discounts are federally permitted under the Dodd-Frank Act, a handful of states have their own disclosure or surcharging statuses. Connecticut, Massachusetts, and others have historically had unique rules.

- Debit Card Rules Differ: Surcharging on debit cards is prohibited under Visa and Mastercard rules. Cash discount programs handle this differently – confirm with your processor that your program is structured correctly to cover debit transactions.

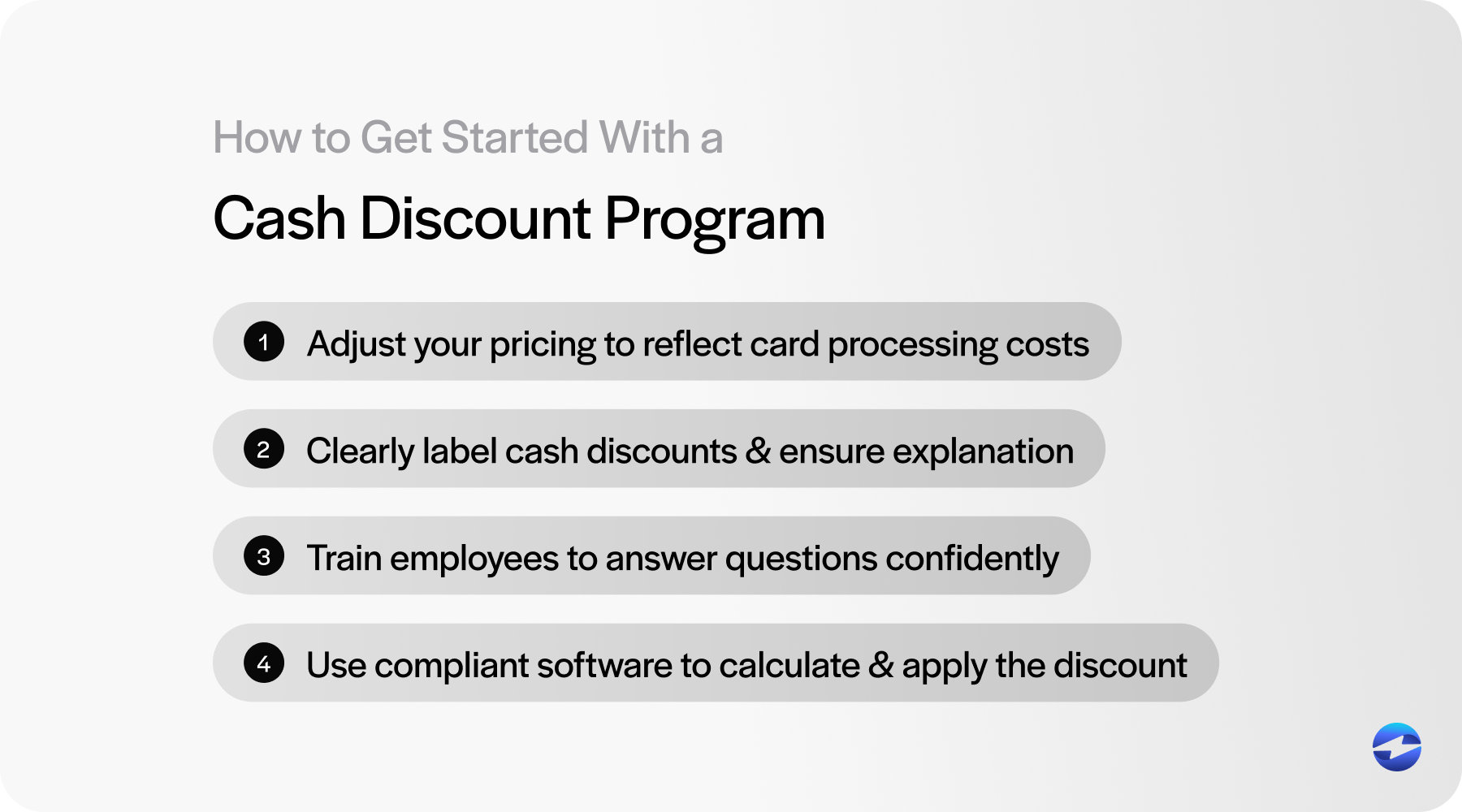

Do You Need a Downloadable Cash Discount Sign?

Once you understand the rules, the practical question becomes: what does the actual sign look like, and where do you get one?

Most processors that offer a merchant cash discount program will provide compliant signage as part of onboarding. Some provide physical materials, others provide printable templates. If you’re setting up a program or auditing an existing one, make sure the signage you are using matches your current discount rate, reflects the correct framing, and is posted in both required locations.

A 3% cash discount sign template should clearly state the standard card price as the listed price and identify the cash discount percentage. A 4% cash discount signage template follows the same format. If you are unsure whether your existing signage meets card network requirements, the safest step is to run it by your processor before you display it.

Cash discount compliance is not complicated once you know what the rules require. It just needs to be done right.

FAQ’s

FAQ’s

What should a cash discount sign say?

A compliant cash discount sign needs to communicate three things: that a standard card price exists, that cash-paying customers receive a discount off that price, and the exact percentage or dollar amount of that discount. Vague language is not sufficient under card network rules. Your sign should clearly state something along the lines of: “Our listed prices reflect the standard card price. Customers paying with cash receive a 3% discount.” The simpler and more direct the language, the better.

Where do I need to post my cash discount signage?

Card network rules require disclosure at two points: when the customer first enters your business and again at the point of sale. Posting a sign only at checkout does not meet compliance requirements because customers need to see the pricing structure before they decide to make a purchase. Common placement includes the front door or entrance, the service counter, printed menus, and directly at the register or payment terminal.

Is a cash discount program legal?

Yes. Cash discount programs are federally permitted under the Dodd-Frank Act, which prohibits card networks from preventing merchants from offering discounts for cash payments. That said, state laws vary. A small number of states have historically had their own disclosure or surcharging rules that add an extra layer of complexity. If you operate in Connecticut, Massachusetts, or another state with known restrictions, it is worth confirming the current rules with your processor before launching your program.

What is the difference between a cash discount sign and a surcharge sign?

The difference comes down to framing. A surcharge sign communicates that card-paying customers are being charged an additional fee on top of a base price. A cash discount sign communicates that cash-paying customers are receiving a discount off the standard price. These may seem like two ways of saying the same thing, but card networks and regulators treat them very differently. Cash discount programs are more broadly permitted and carry fewer compliance requirements than surcharge programs, which is why the framing on your signage needs to be accurate and consistent with how your processor structured your program.