Blog > Your Step-by-Step Guide to Filling Out a Merchant Application

Your Step-by-Step Guide to Filling Out a Merchant Application

While navigating merchant applications can feel daunting, it’s a crucial step for any business looking to accept payments. These applications enable merchants to partner with payment processors to seamlessly process customer transactions.

To open up a merchant account, you will need to fill out a merchant application. This requires careful preparation and documentation, as several vital details influence the approval process. By knowing what to expect, businesses can streamline their applications and improve their chances of approval.

What is a merchant application?

A merchant application is a formal document a business owner must complete and submit to a merchant account provider to be able to accept and process customer credit and debit cards and electronic payments.

Merchant applications require detailed information about the business, including its type, structure, anticipated sales volumes, and business plan. These applications typically involve merchants submitting financial and bank statements, business licenses, and other relevant documentation.

Merchant application information is critical in the underwriting process, which assesses the risk of providing merchant services to a business. The merchant service provider also uses the information gathered to determine transaction fees, setup fees, and other terms of service.

Once approved, a merchant account is established, enabling the business to integrate various payment solutions, such as payment gateways for online, mobile, and in-person payments. The ultimate goal is to provide flexibility in accepting customer payments, which is vital for business owners in today’s increasingly digital and cashless economy. The approval process can vary in length, often depending on the business’s complexity and the submitted application’s completeness.

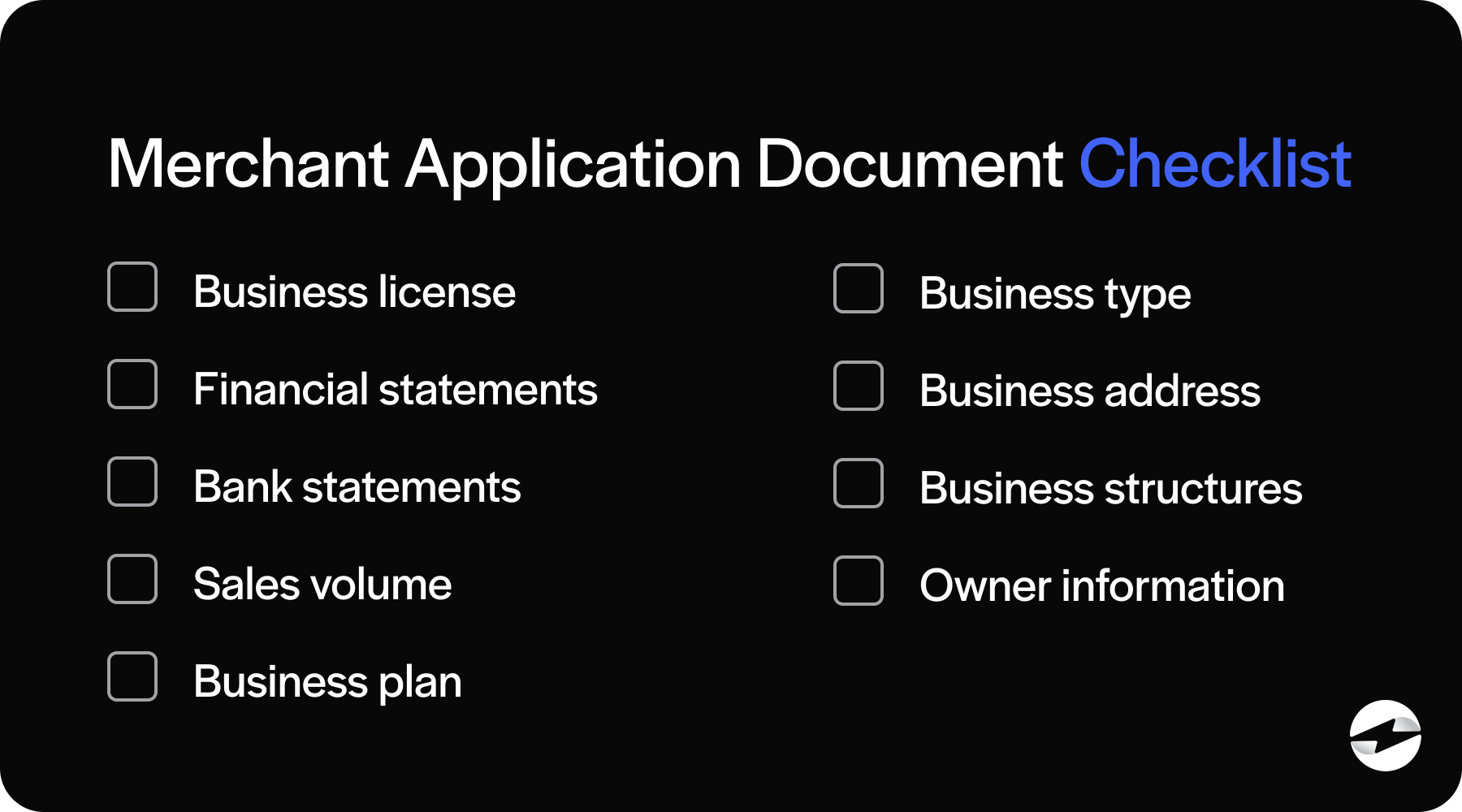

Before starting your merchant application, you should have various documentation and business details ready to include.

Required documents and details to submit a merchant application

When filling out a merchant application, it’s imperative to have all required documentation prepared to enable a smooth application process.

Here’s a list of critical documents and information typically needed:

- Business license: Proof of your legal right to operate the business.

- Financial statements: Recent financial records to assess financial stability.

- Bank statements: Last month’s statements to verify business cash flow.

- Sales volumes: Document monthly sales volumes to evaluate transaction levels.

- Business plan: An overview of your business model and growth projections.

- Business type: Information about the nature of your goods or services.

- Business address: The physical or registered address of the business.

- Business structures: Details regarding whether your business is a sole proprietorship, partnership, corporation, etc.

- Owner information: Personal identification and contact information of the business owner(s).

Exact requirements may vary based on the merchant service provider, business type, and intended use case for credit and debit card payments (online, mobile, in-person, etc.). Confirm with your desired merchant services provider to verify if additional information is necessary for the underwriting process.

Once you’ve collected all the required documents and information, you can follow six steps to complete the application.

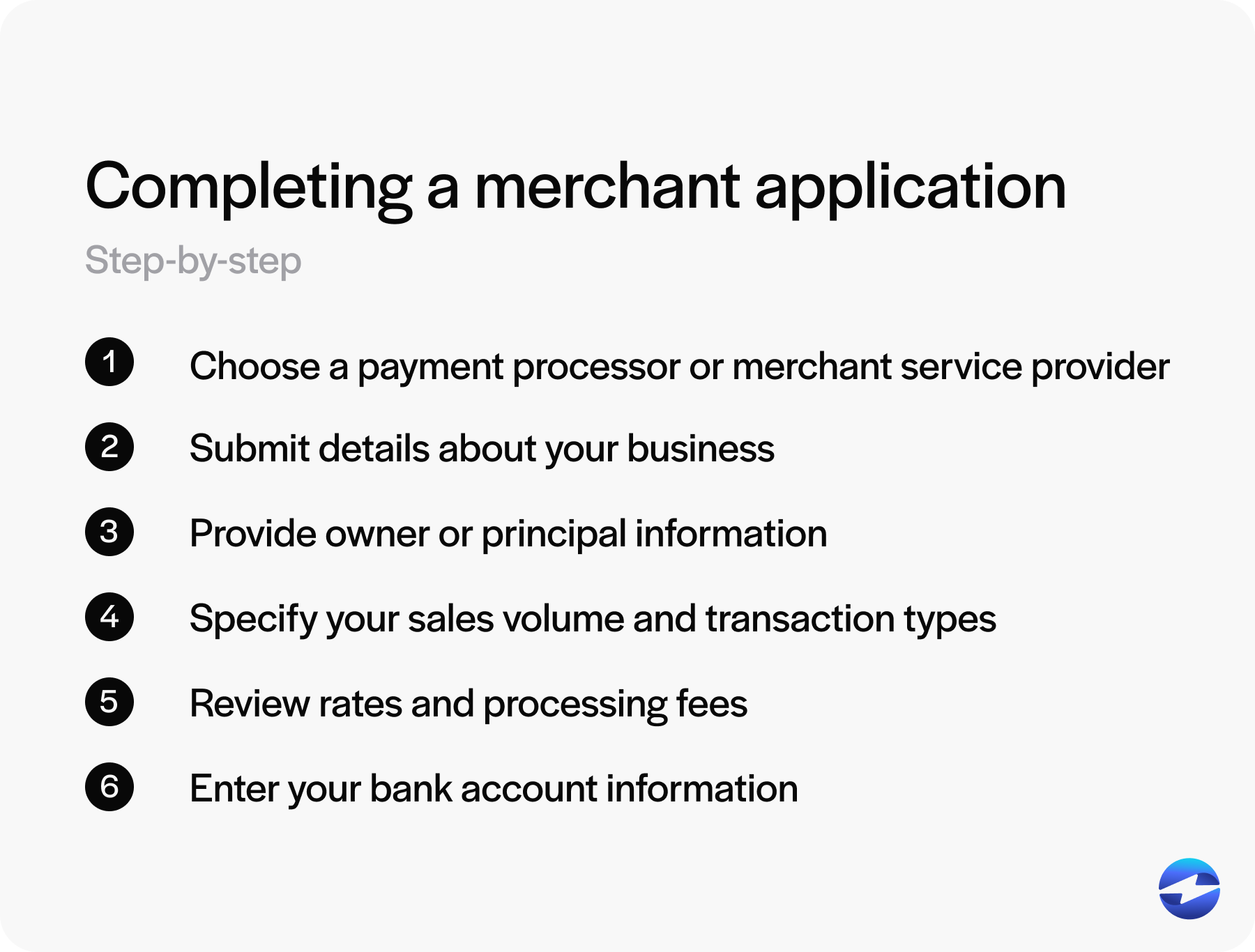

6 steps to complete a merchant application

Businesses can complete the merchant application process to start accepting customer payments by following six simple steps. These steps ensure your merchant service provider or payment processor has all the necessary information to support these transactions.

Here are the six steps you need to follow to complete your merchant application:

- Choose a payment processor or merchant service provider

- Submit details about your business

- Provide owner or principal information

- Specify your sales volume and transaction types

- Review rates and processing fees

- Enter your bank account information

Step 1: Choose a payment processor or merchant service provider

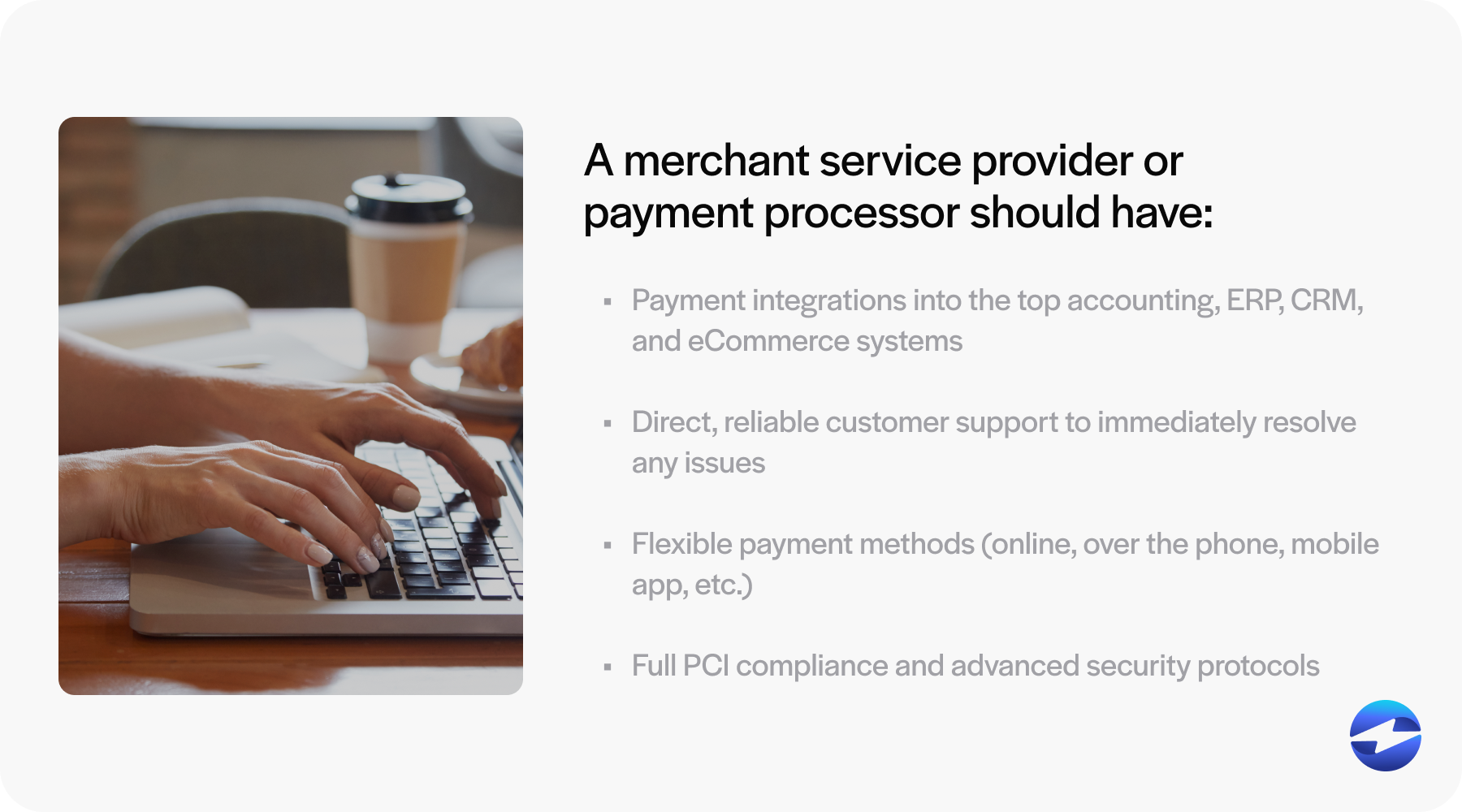

Before starting the merchant application process, your business must select a merchant service provider or payment processor.

You should thoroughly research and compare different providers to see which offer the most cost-effective solutions with:

- Lower transaction costs and fees

- Payment integrations into the top accounting, ERP, CRM, and eCommerce systems

- Direct, reliable customer support to immediately resolve any issues

- Flexible payment methods (online, over the phone, mobile app, etc.)

- Full PCI compliance and advanced security protocols

It’s also essential to ensure the compatibility of the provider’s services with your business infrastructure. Finding a top-rated payment processor like EBizCharge will provide your business with all these features while maintaining competitive pricing.

Once you’ve chosen a provider that meets your needs, you can proceed with the application process.

Step 2: Submit details about your business

Merchant applications contain a business information section where you must provide specific details about your operations and ownership.

Merchants will need to provide fundamental information such as business licenses, business addresses, and business structure types (sole proprietorship, partnership, LLC, or corporation). You’ll also be required to describe the nature of your business, including a detailed explanation of the products or services you offer.

Additional information may be required, such as your years in operation, number of employees, and annual revenue. This helps the payment processor assess your business’s risk profile.

Filling out every field accurately and truthfully is essential, as incorrect or incomplete information can lead to delays or rejected applications.

Step 3: Provide owner or principal information

Merchant account providers and payment processors require the personal identification and contact information of the business owner(s) or principal(s) to perform necessary background checks as part of the underwriting process.

This typically includes providing your full name, date of birth, Social Security number, email address, and physical address. If there are multiple owners or a hierarchy of stakeholders, follow the application requirements to detail the information for each individual involved.

Step 4: Specify your sales volume and transaction types

Another component of the merchant application process is to estimate your company’s credit card and debit card sales volumes, including your average transaction amount, total monthly sales, and highest anticipated transaction size.

These figures help merchant service providers and payment processors assess your processing needs and evaluate the risk associated with your account, as higher transaction volumes or large individual transactions may increase exposure to more chargebacks or fraud.

Merchants may need additional documentation to support their sales volume estimates, such as historical sales data, bank statements, or financial projections. This is typically necessary for new businesses submitting a merchant application.

Accuracy is essential since significant discrepancies between your estimated and actual sales volumes can lead to account freezes or adjustments in your processing limits. Transparent and detailed information also helps build trust with the provider and ensures a more seamless onboarding process.

Step 5: Review rates and processing fees

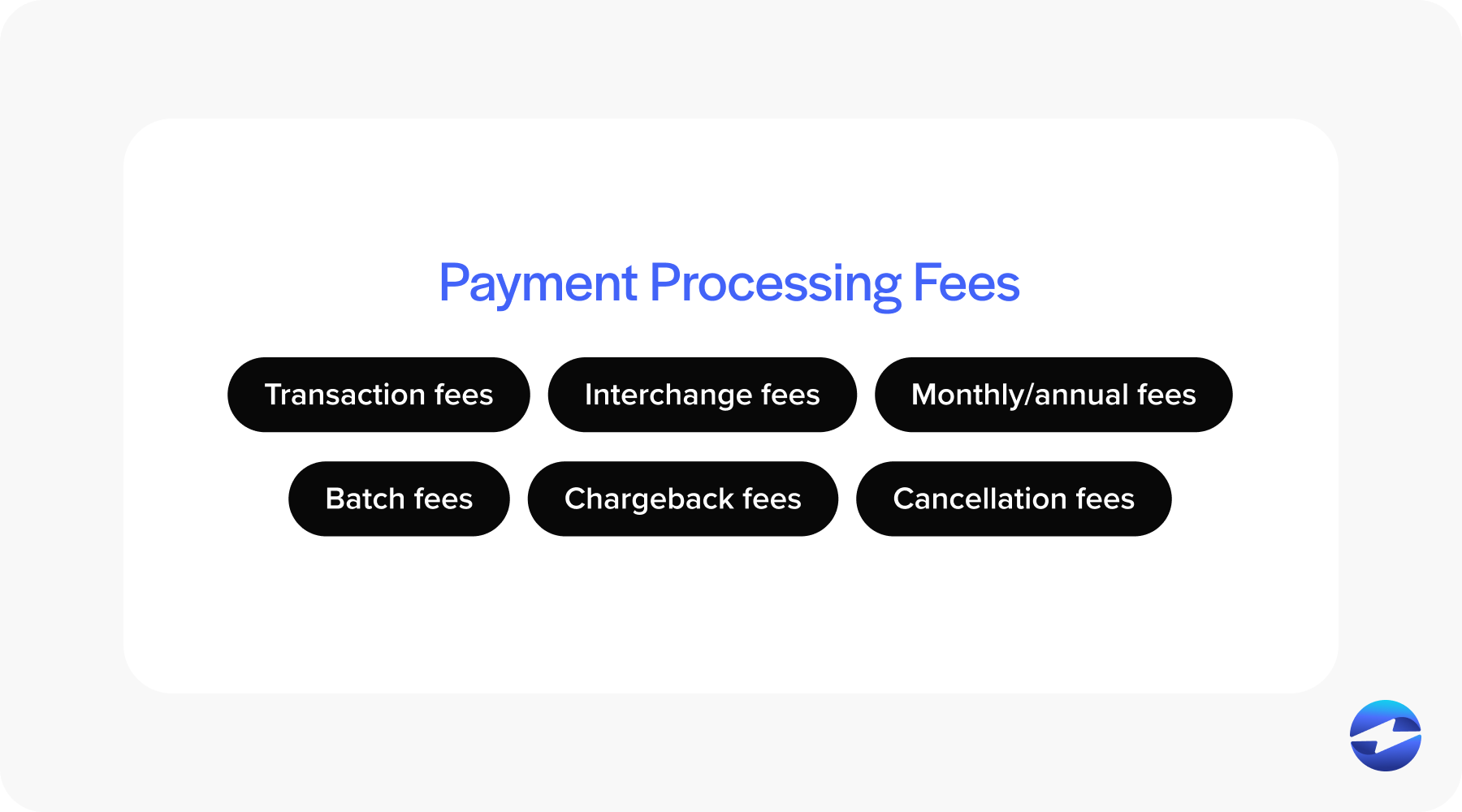

After submitting all the information above, businesses will receive a breakdown of rates and fees associated with processing credit card transactions from their provider.

Since costs can vary depending on factors such as the type of transaction and credit card type, it’s crucial to understand the different payment processing fees you may be charged:

- Transaction fees: Transaction fees can be a flat or a percentage of the transaction amount, depending on the payment processor’s pricing model. In-person payments typically have lower fees since they’re considered less risky. Online and mobile payments usually incur higher fees due to increased fraud risk.

- Interchange fees: Interchange fees are usually non-negotiable and paid to the card-issuing bank to cover the cost of processing credit and debit card payments. These fees vary depending on the card type and transaction method.

- Monthly or annual fees: Some providers charge recurring fees, such as monthly service fees, PCI compliance fees, or account maintenance fees.

- Batch fees: If you process multiple transactions simultaneously (e.g., at the end of the day), there may be batch processing fees for grouping them together.

- Chargeback fees: If customers dispute transactions, merchants may incur chargeback fees in addition to refunded transaction amounts. Chargebacks can be costly, especially if they’re frequent.

- Cancellation fees: Some providers may charge an early termination fee if you decide to cancel the service before the end of your contract.

Before signing any agreements, thoroughly review and understand all the terms related to these fees. Ask for clarification on anything unclear, especially hidden fees or tiered pricing structures where various card types incur different fees, affecting your overall processing costs. It’s also wise to inquire about pricing models (interchange-plus, flat-rate, or tiered pricing) to determine which will work best for your business.

Understanding how fees impact your bottom line is essential for maintaining profitability.

Step 6: Enter your bank account numbers

Lastly, your company must provide business bank account numbers so its merchant service provider can deposit your funds from processed transactions.

Bank account information typically includes bank names, routing numbers, and account numbers. Verify this information is accurate before submitting, as any errors can result in payment delays or misdirected funds.

Some providers may ask whether the account is a checking or savings account and request a voided check or bank letter to confirm the account details. Having this information ready can accelerate the merchant account setup process.

Working with a reliable payment processor to secure a merchant account and improve customer payments

In addition to following the proper steps and providing all the necessary documentation, partnering with a reputable merchant account provider can streamline your payment processing operations, enhance revenue, and secure a reliable merchant account.

EBizCharge payment processing is an excellent choice for businesses that want a cost-effective solution with lower transaction fees and a comprehensive payment suite that consists of a payment gateway, merchant services, and over 100 payment integrations into the top business systems.

EBizCharge’s most notable features include click-to-pay email links, an online customer payment portal, recurring billing, mobile payments, 24/7 direct support, and more. It’s also fully PCI compliant, with advanced security protocols such as tokenization, encryption, 3D Secure, and more, to ensure all transactions are safe and secure.

Overall, EBizCharge enables merchants to simplify their invoicing operations, lower costs, and deliver an efficient and secure payment experience to all customers. Get started by applying for a merchant account today.