In finance, precision is paramount, and understanding the language of numbers can be the key to unlocking better financial strategies. The basis point (BPS)is a common term that often arises in discussions surrounding interest rates, investment returns, and fees.

Knowing what basis points are and how they function is essential since they can eliminate confusion around interest rates and reflect borrowers’ credit status and risk.

What are basis points?

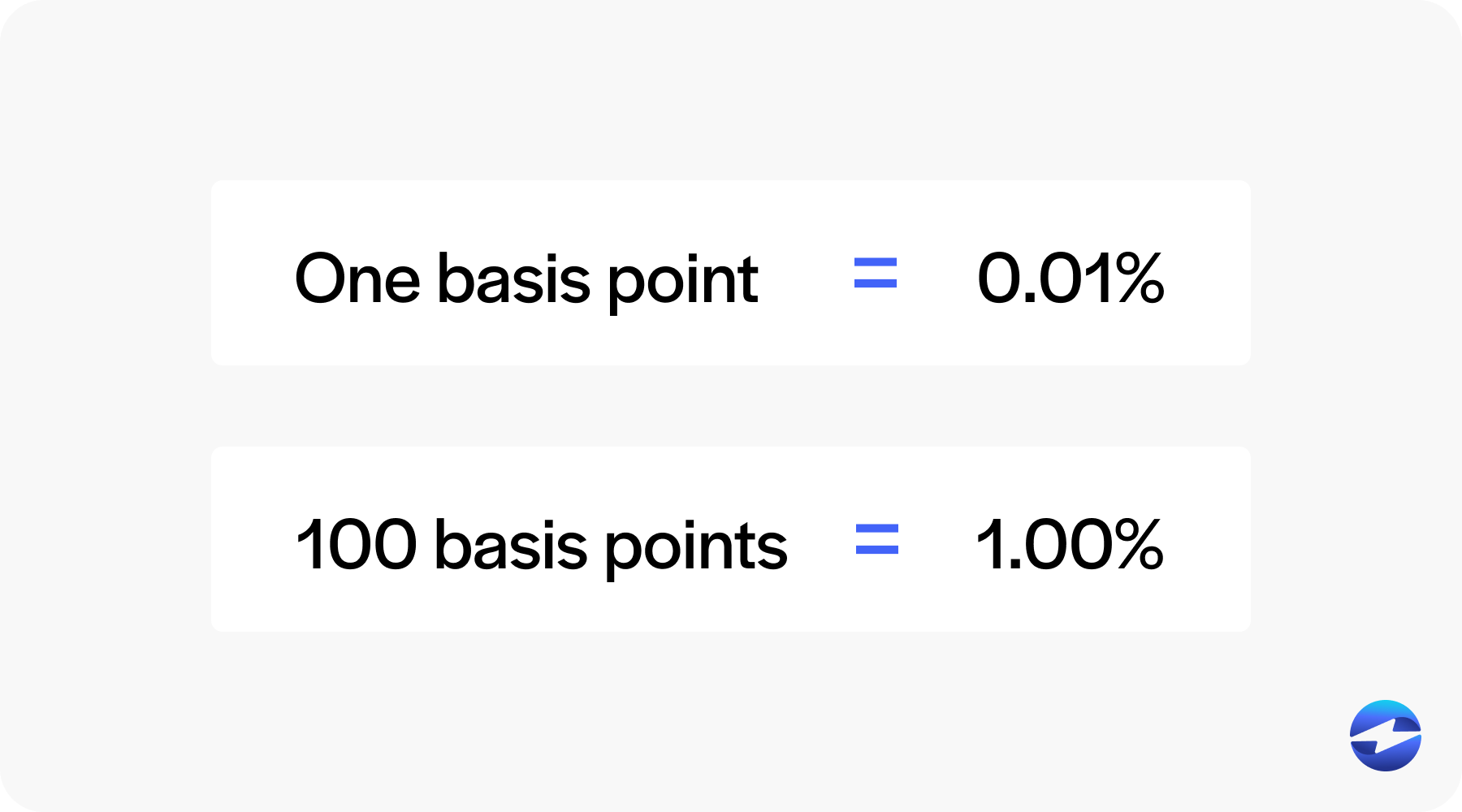

Basis points (BPS) are units of measurement used in finance to describe interest rates and other percentages.

One basis point equals one-hundredth of a percentage point, or 0.01%. Therefore, 100 basis points equal 1%. This unit of measurement is essential when discussing subtle changes in financial metrics. For example, if a mortgage rate increases from 3.25% to 3.50%, the increase can be described as 25 basis points.

Using basis points helps avoid confusion from using percentages alone, especially for mortgage loans, savings accounts, and credit cards, where even a small change can significantly affect monthly payments.

Basis points calculator

Why are basis points important?

Whether analyzing financial products, adjusting interest rates, or managing risk, basis points serve as a universal language in complex financial discussions. Their importance extends beyond numbers, influencing decisions that can have significant economic and personal financial consequences.

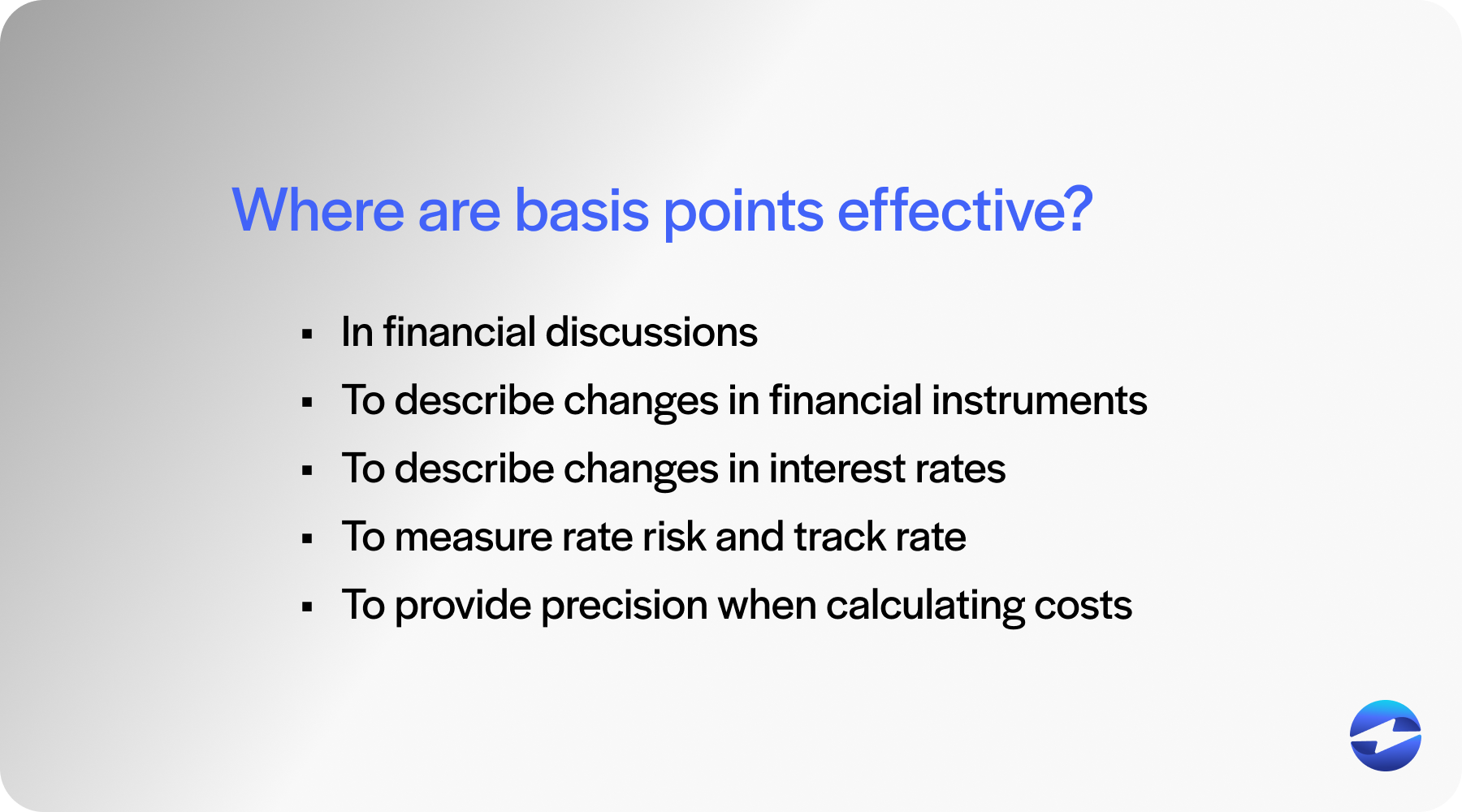

Here are five areas where basis points are effective:

- Transparent communication: Using basis points in financial discussions can eliminate ambiguity, since these points enhance the comprehension of financial details or calculating current rates.

- Financial instruments: Basis points describe changes in financial instruments like mutual funds, corporate bonds, and fixed-income securities. For instance, a bond yield may rise or fall by a certain number of basis points, affecting investors’ returns.

- Interest rates: Basis points are critical when discussing changes in rates the Federal Reserve sets, like the federal funds rate. Even a small rate hike in absolute interest rates can have vast economic implications.

- Risk measurement: Basis points help measure rate risk and track rate increases accurately. From percentages to basis points, understanding the change is key to managing financial risk effectively.

- Contracts and agreements: Basis points provide precision when calculating costs such as credit derivatives and mortgage interest rates. They’re used to express terms of basis point rates in agreements.

Using this unit of measure correctly can provide a clearer view of financial movements and potentially save money in the long run, as it directly impacts monthly mortgage payment calculations and other financial decisions.

What are the main benefits of basis points?

Basis points help investors and analysts avoid confusion, especially when discussing small changes in interest rates or yields.

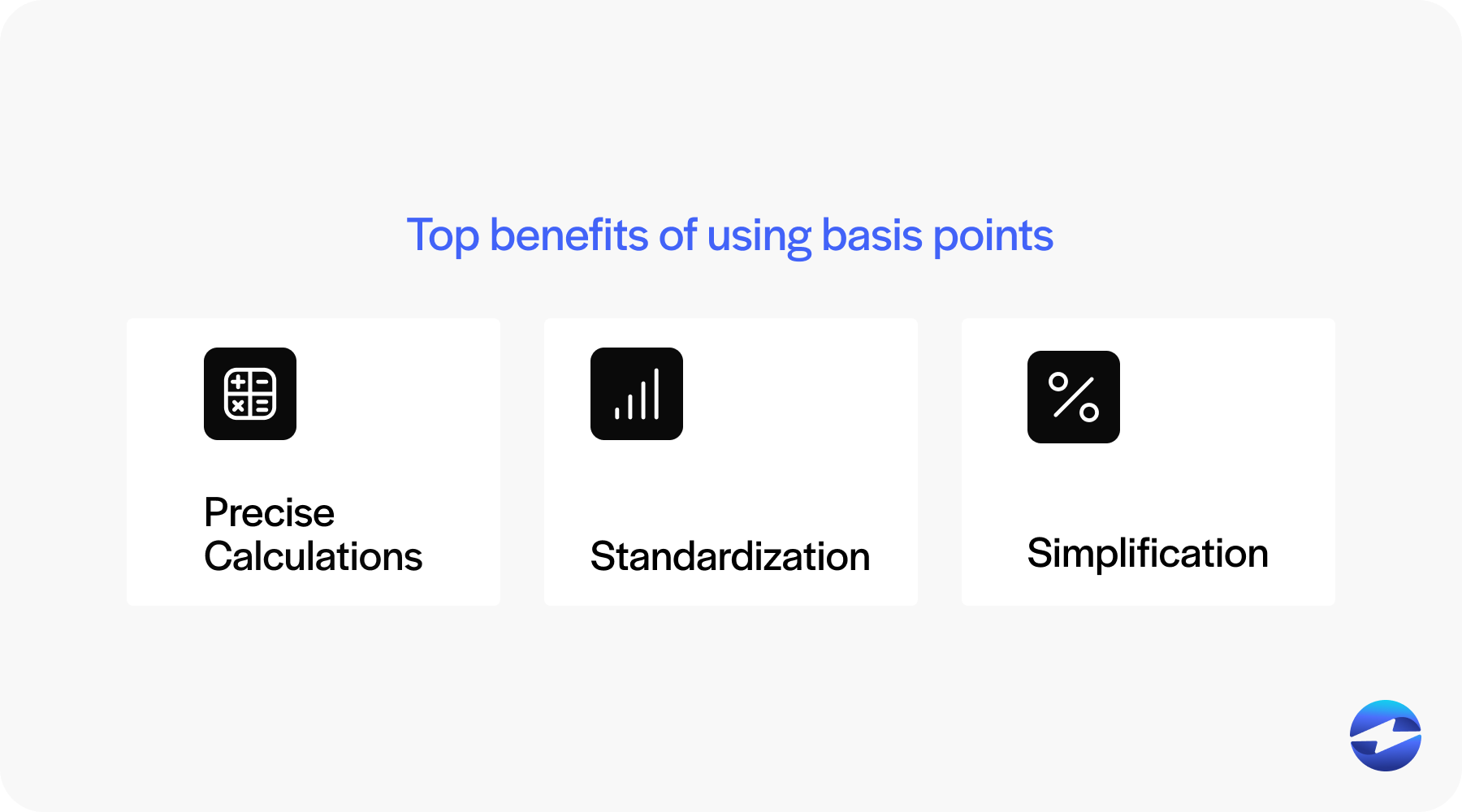

Here are three top benefits of using basis points:

- Precise calculations: Since financial markets rely on accuracy, basis points clearly express changes, which are crucial for mortgage loans, corporate bonds, and mutual funds.

- Standardization: Using basis points provides a universal method of detailing interest and other financial percentage changes, whether dealing with credit cards, fixed-income securities, or the federal funds rate.

- Simplification: Basis points streamline calculations, especially when comparing rates or changes. Converting between percentages and basis points is straightforward, aiding financial professionals in presenting and interpreting data efficiently.

Overall, basis points enhance accuracy and clarity in financial communications, providing a reliable standard for measuring even the smallest changes in rates and yields.

Now that you understand the benefits of basis points, you should familiarize yourself with how this measurement is used.

How are basis points used in practice?

Basis points are essential in financial settings as they offer a precise way to describe small changes in interest rates and yields.

Since basis points equate to one-hundredth of a percentage point or 0.01%, they’re crucial for applications like mortgage loans, savings accounts, and corporate bonds, where even minor changes can significantly impact financial outcomes.

For instance, if the Federal Reserve announces a rate hike of 50 basis points, it means an increase of 0.50% in the federal funds rate. This change affects auto loans, monthly mortgage payments, and credit cards, altering monthly payment obligations.

Similarly, shifts in bond yields, mutual funds, and exchange-traded funds are often expressed in basis points to convey precise movements.

Here’s a simple conversion table to illustrate the concept:

| Percentage (%) | Basis Points (bps) |

|---|---|

| 0.01% | 1 bps |

| 0.10% | 10 bps |

| 1.00% | 100 bps |

| 2.50% | 250 bps |

Understanding these terms helps analyze fixed-income securities and credit derivatives, where absolute interest rates and rate risk are critical. This clear unit of measure is preferred over percentages for accuracy in financial reporting.

How are basis points calculated and converted to percentages?

Understanding basis points is critical in finance, especially when dealing with loan rates, bonds, and investment yields.

A basis point (bp) is a unit of measurement equal to 0.01%. This means that one basis point is 1/100th of a percentage point. Thankfully, converting basis points to percentages is straightforward and helps in accurate financial analysis.

Here’s a quick guide to calculating basis points:

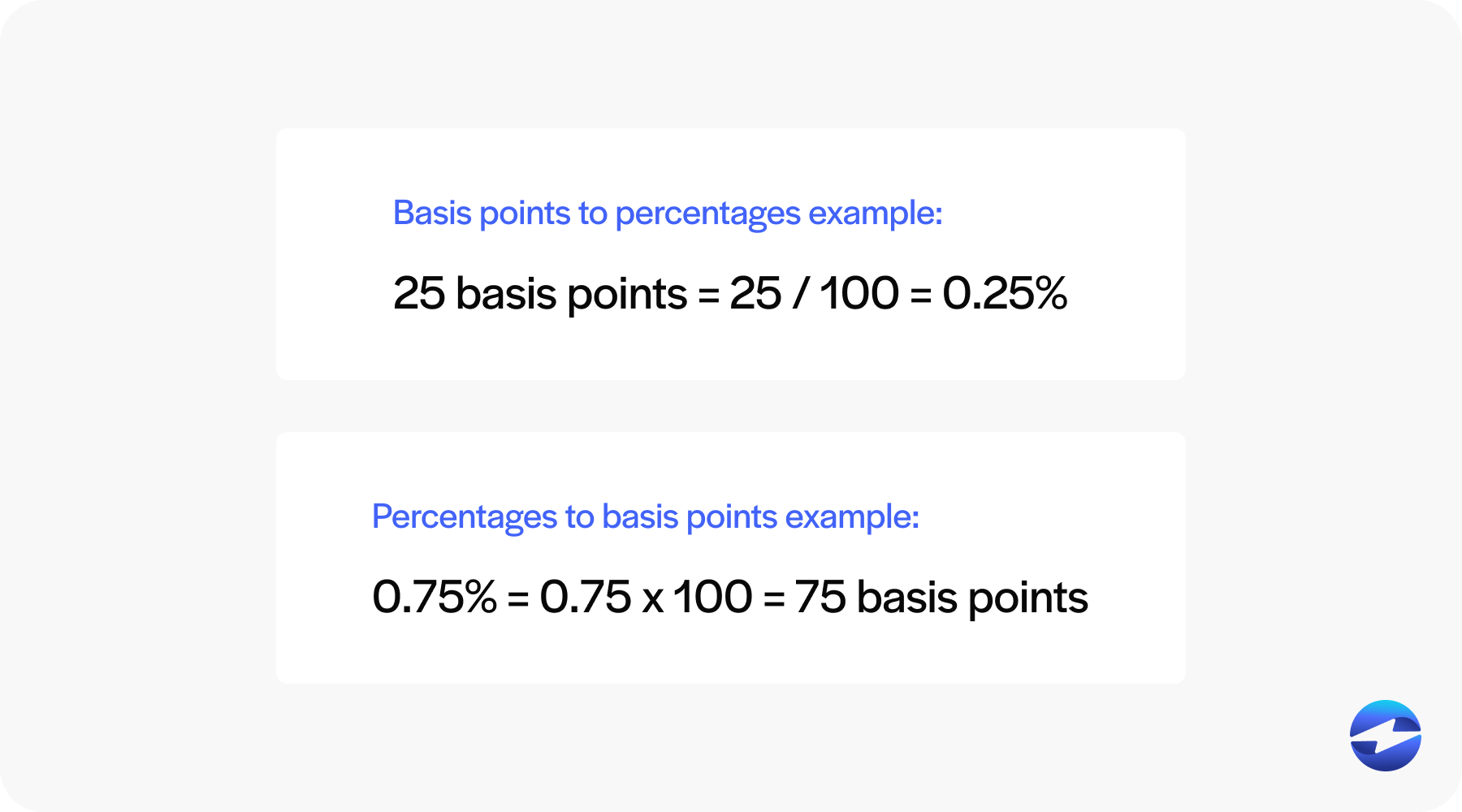

Converting basis points to percentages: Percentage = Basis points / 100

- Example A: 25 basis points = 25 / 100 = 0.25%

Converting percentages to basis points: Percentage x 100 = Basis Points

- Example B: 0.75% = 0.75 * 100 = 75 basis points

Knowing how to convert basis points and percentages helps you understand rate hikes, bond yields, and more.

Why do people use basis points instead of percentages?

Using basis points instead of percentages in financial settings brings clarity and precision. When dealing with small rate changes, percentages can be misleading.

A shift of 0.25% might seem negligible, but the difference is clear and precise when expressed as 25 basis points.

In addition to limiting miscommunications, basis points simplify rate adjustments by making it easier to express and track minor rate movements and simplifying reporting abilities.

Investors also use basis points for various financial purposes and clarity.

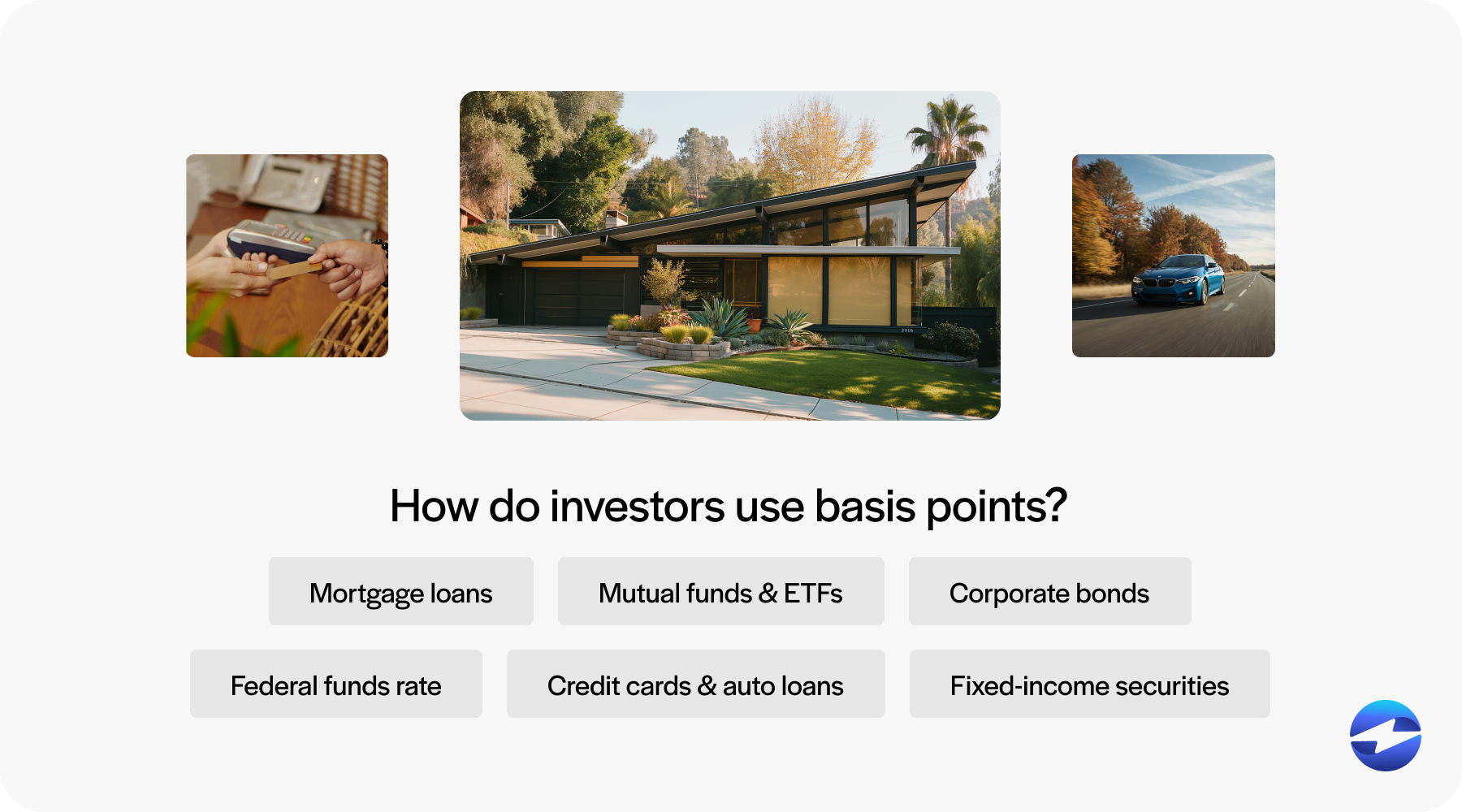

How do investors use basis points?

The clarity provided by basis points is essential for assessing the risks and returns associated with various financial products, from mortgage loans to fixed-income securities.

For investors, basis points enable a detailed analysis of rate changes and their implications, such as how adjustments in the federal funds rate might influence borrowing costs of savings yields.

Here are six ways investors use basic points:

- Mortgage loans: Basis points clarify changes in mortgage rates. For instance, a 50-basis point increase raises the mortgage rate by 0.50%.

- Mutual funds and ETFs: Investors analyze basis points when assessing management fees and fund performance.

- Corporate bonds: Basis points help determine yield differences and assess risk.

- Federal funds rate: The Federal Reserve may adjust this rate by several basis points, impacting loan and savings account rates.

- Credit cards and auto loans: Small rate hikes or reductions in terms of basis points affect monthly payments.

- Fixed-income securities: Determining rate risk involves basis points for precise calculation.

In summary, basis points translate percentage changes into a clear and standard format, aiding investors in assessing rate hikes, yields, and risks across various markets for better financial decision-making.

Navigating the complexities of finance with clarity and precision

Understanding basis points is essential for navigating the complexities of finance with clarity and precision. This simple yet powerful unit of measurement eliminates confusion, ensures consistent communication, and enhances decision-making in contexts ranging from mortgage rates to investment returns.

By mastering the concept of basis points and their conversion, individuals and businesses can better evaluate financial changes, negotiate terms effectively, and make informed decisions that align with their financial goals.

For businesses managing payment processing costs, embedded payment solutions EBizCharge makes it easier to track and reduce those costs across over 100 ERP, CRM, and accounting integrations so every basis point saved shows up directly in your books.