Blog > What Is Payment Tokenization? How It Works, Benefits & PCI Compliance

What Is Payment Tokenization? How It Works, Benefits & PCI Compliance

In today’s digital era, businesses and individuals increasingly rely on online transactions. As this dependency grows, the need for advanced security measures to protect sensitive data becomes critical. This is where tokenization comes into play. But what is the tokenization of data, and how does it work?

In this article, we’ll break down how payment tokenization works, why it matters for credit card processing security, and how it connects to PCI DSS compliance requirements.

What is tokenization and how does it relate to payments?

Simply put, tokenization payments work by replacing sensitive card data with a unique, randomly generated token that has no exploitable value outside the system that issued it.

In the context of payments, tokenization substitutes the original credit or debit card information with a unique token. This token serves as a reference to the sensitive card details that are securely stored in a separate, protected location — a token vault — to reduce the risk of data breaches and identity theft.

How does tokenization work?

The tokenization process begins when a customer initiates a transaction by entering their card information at checkout. That data is immediately encrypted and sent to a secure tokenization system, which generates a unique token to represent the card. The original card number never touches your servers. Instead, the token is what gets passed through your payment gateway, stored in your records, and used for future transactions like recurring billing or refunds.

This is what makes tokenized payment processing fundamentally different from simple encryption. Encrypted data can theoretically be decrypted with the right key. A token has no mathematical relationship to the original card number, so even if someone intercepts it, there’s nothing to reverse-engineer.

Credit card tokenization vs. encryption: what’s the difference?

Both tokenization and encryption protect payment data, but they work differently and serve different purposes. Encryption scrambles card data using an algorithm, and the original data can be recovered using a decryption key. Tokenization replaces the data entirely with a substitute value that has no connection to the original. There’s nothing to decrypt.

For credit card processing specifically, tokenization is generally the stronger approach for stored data because it removes the risk that comes with holding decryption keys. Many processors use both: encryption in transit and tokenization for stored card data.

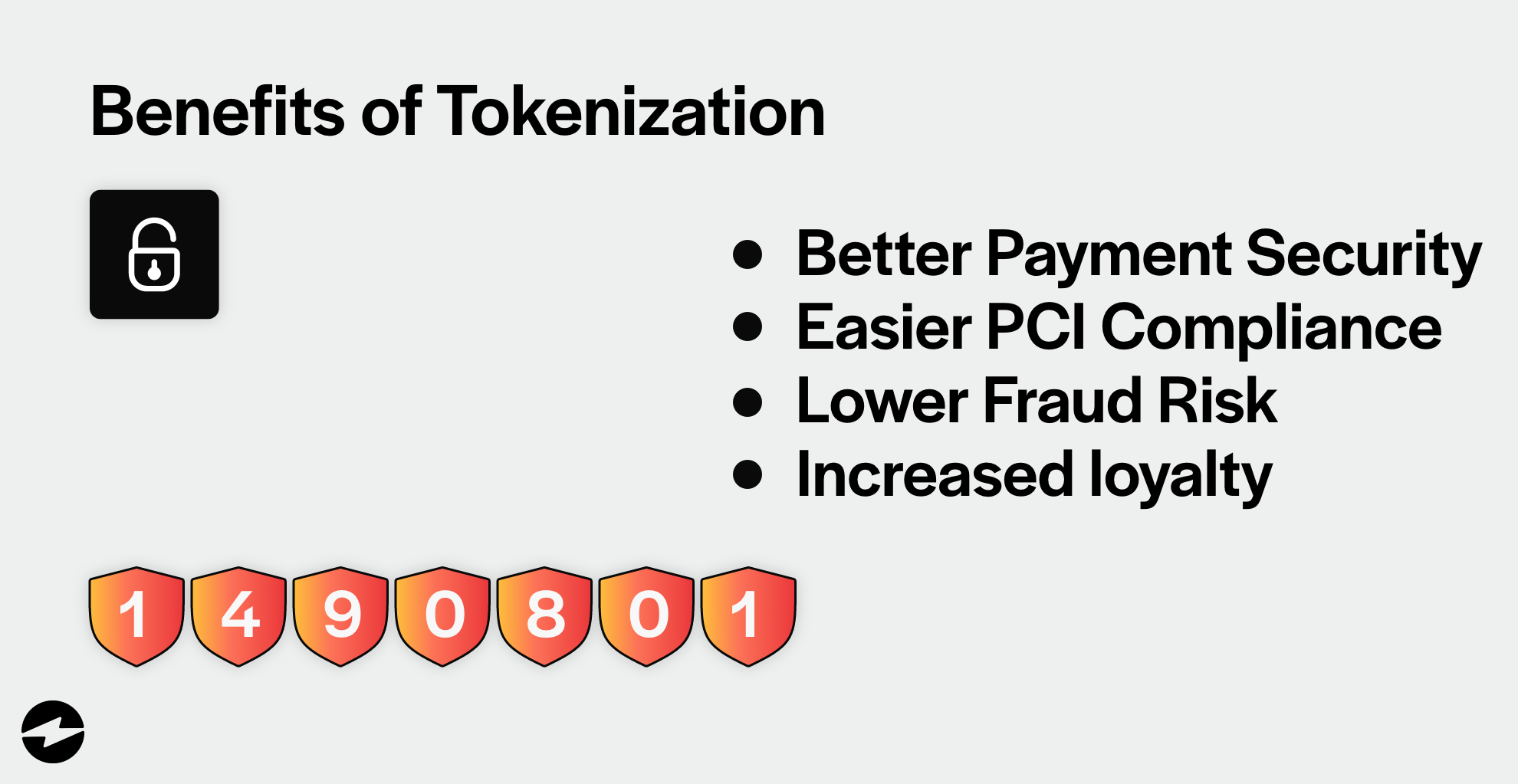

4 benefits of tokenization

Tokenization provides numerous benefits in the realm of payment processing and cybersecurity.

Four main benefits of tokenization include:

- Enhanced payment security

- Simplified PCI compliance

- Reduced risk of fraud

- Increased customer trust and loyalty

1. Enhanced payment security

Tokenization mitigates the risk of data breaches and identity theft by ensuring sensitive data is never exposed.

This enhanced security is particularly valuable for businesses that handle large volumes of sensitive information.

2. Simplified PCI compliance

Tokenization and PCI DSS compliance go hand in hand. The Payment Card Industry Data Security Standard requires merchants to protect cardholder data at every point in the transaction process. When you use payment tokenization, sensitive card data never actually enters your environment in a usable form. That significantly reduces the scope of your PCI DSS audit because systems that only handle tokens rather than real card numbers fall outside the full compliance requirement.

For merchants processing high volumes of credit card transactions, this is one of the most practical benefits of tokenization. Fewer systems in scope means fewer controls to implement, fewer audits to pass, and lower overall compliance costs.

3. Reduced risk of fraud

Tokenization helps prevent fraud by making it more challenging for hackers to access payment information.

Tokenization reduces this risk by replacing sensitive cardholder data with symbols of no value that can’t be decrypted.

4. Increased customer trust and loyalty

Using tokenization to increase payment security allows businesses to provide customers with a more reliable and seamless payment experience.

As a result, customers are more inclined to trust your business and return since they feel more secure knowing their sensitive card information is protected.

The importance of tokenization in cybersecurity and payment processing

Security tokenization plays a crucial role in both cybersecurity and payment processing.

In cybersecurity, tokenization helps protect sensitive data from unauthorized access, reducing the risk of data breaches and identity theft. In payment processing, tokenization ensures the secure transmission and storage of cardholder data, simplifying PCI DSS compliance and reducing the risk of fraud.

Optimize your online payment process with tokenization and other advanced security tools

Tokenization is an essential security measure for businesses and individuals who process payments online. By understanding what tokenization is, how it works, and its benefits, you can make informed decisions to protect your sensitive data and build trust with your customers.

To further strengthen your security measures, consider employing cybersecurity services like those offered by LogixCare, and for a seamless payment experience, explore the payment services provided by EBizCharge. Combining these solutions with tokenization will help you avoid cyber threats and provide a safer environment for your customers.

Frequently Asked Questions

What is payment tokenization?

Payment tokenization is the process of replacing a customer’s sensitive card data with a randomly generated token. That token has no usable value on its own. It acts as a stand-in for the real card number throughout the transaction, so the actual account information never passes through your systems in a form that can be stolen or misused.

How does payment tokenization work?

When a customer enters their card details at checkout, that information is sent to a secure tokenization system, which generates a unique token to represent it. The token is what gets passed through your payment gateway and stored in your records. The real card data sits in a separate, protected vault. For recurring transactions, the token is reused rather than re-entering the card number, so sensitive data is only handled once.

Is tokenization the same as PCI compliance?

They are related but not the same thing. PCI DSS is the set of security standards that card networks require merchants to follow. Tokenization is one of the tools that helps you meet those standards. When card data never enters your systems in a usable form, it reduces the number of systems that fall within your PCI audit scope, which simplifies compliance and lowers the cost of maintaining it.

What is the difference between tokenization and encryption?

Encryption scrambles card data using an algorithm, and the original data can be recovered with the right decryption key. Tokenization replaces the data with a substitute value that has no mathematical relationship to the original. There is nothing to reverse-engineer. Most payment processors use both: encryption to protect data in transit, and tokenization to protect stored card data.

How does tokenization reduce fraud?

If a fraudster intercepts a token, it is worthless outside the specific system that issued it. Tokens cannot be used to make purchases elsewhere, cannot be decoded to reveal the original card number, and are typically tied to a single merchant or transaction context. That makes a data breach far less damaging than one involving raw card numbers.

Does tokenization work for debit cards?

Yes. Debit card tokenization works the same way as credit card tokenization. The card number is replaced with a token at the point of entry, and the real account information is stored securely off your systems. This applies whether the debit card is processed as a card-present transaction at a terminal or as a card-not-present transaction online.

What is EMV tokenization?

EMV tokenization happens at the hardware level when a customer taps or dips an EMV chip card. The chip generates a unique, one-time cryptogram for each transaction rather than transmitting the actual card number. This dynamic tokenization is why EMV chip transactions are significantly more resistant to counterfeit fraud than magnetic stripe swipes, where the same static card data is transmitted every time.

What is a payment token vault?

A token vault is the secure, isolated environment where the original card data is stored and matched to its corresponding token. Only the tokenization system itself can look up the real card number using a token. Merchants and payment gateways only ever see and store the token, which means even if your systems are compromised, there is no card data to expose.

- What is tokenization and how does it relate to payments?

- How does tokenization work?

- Credit card tokenization vs. encryption: what’s the difference?

- 4 benefits of tokenization

- The importance of tokenization in cybersecurity and payment processing

- Optimize your online payment process with tokenization and other advanced security tools

- Frequently Asked Questions