Blog > Level 3 Processing for B2B Companies: A Practical Guide

Level 3 Processing for B2B Companies: A Practical Guide

Most B2B companies spend a lot of time thinking about payment terms, collections, and cash flow. Very few spend time thinking about what actually happens at the interchange level when a customer pays with a commercial card. That’s understandable. It’s not exactly the most visible part of running a business. But it’s where a lot of money quietly walks out the door every month.

The conversation around B2B level 3 processing tends to get buried under technical jargon, which is a shame, because the core idea isn’t complicated. If you send more detailed data along with a card transaction, the card networks reward you with a lower processing rate. That’s really what this comes down to. The challenge is knowing what data to send, whether your current setup supports it, and whether you’re actually getting the benefit.

This guide breaks it all down in plain terms

The Three Levels of Card Data, Explained Simply

Card transactions aren’t all treated the same way by Visa and Mastercard. The networks categorize transactions based on how much information is submitted with them, and that categorization directly affects how much interchange you pay.

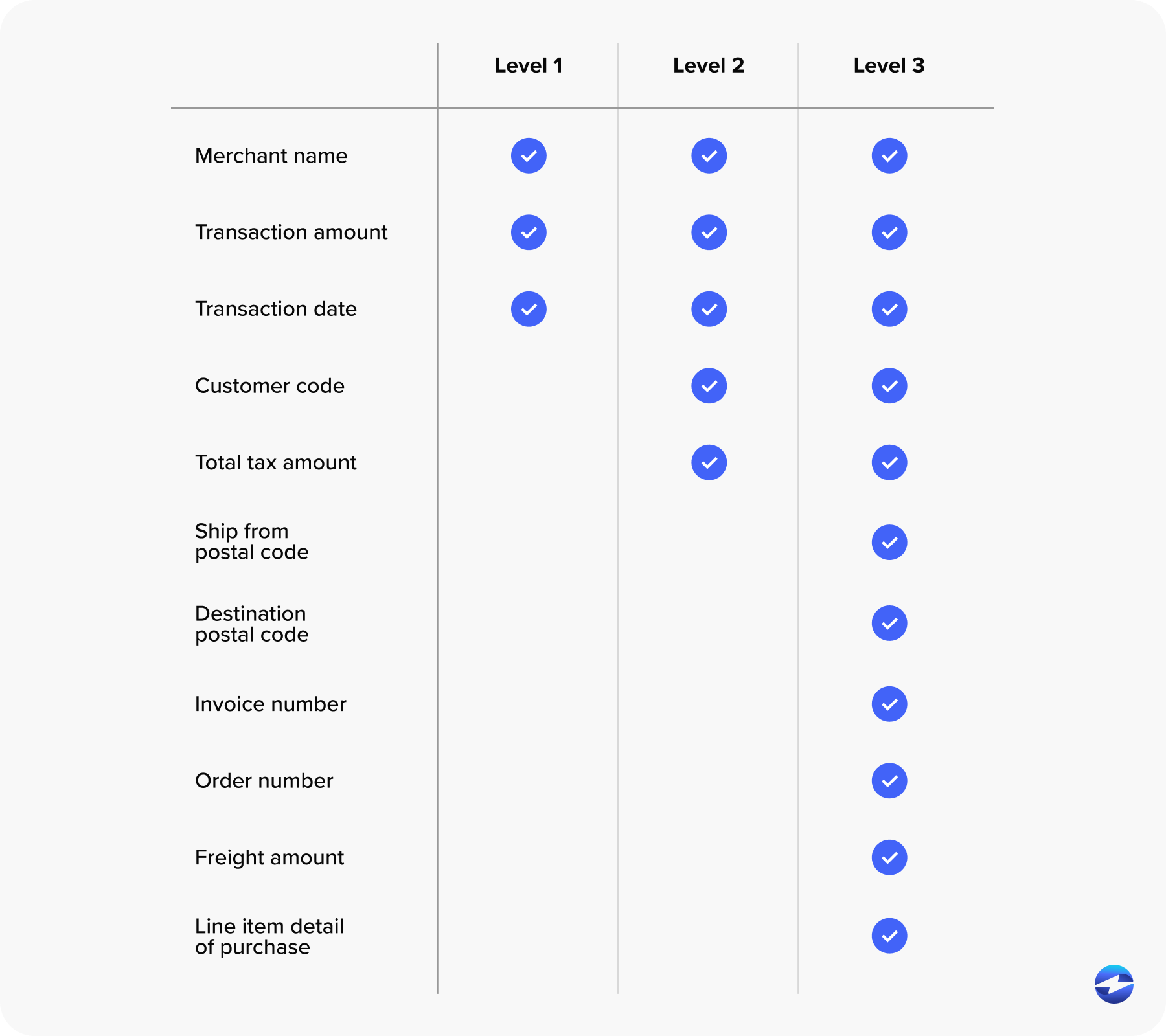

Level 1 is the baseline. It covers the essentials: cardholder name, transaction amount, and date. This is what most consumer purchases look like. Your interchange rate at this level is the highest of the three, and for a consumer swiping a card at a grocery store, that makes sense. There’s no expectation of detailed purchase data.

Level 2 adds a layer. Tax amount, merchant ZIP code, and a customer reference code get included. Many B2B processors handle Level 2 automatically, and it already brings interchange rates down compared to Level 1. But it still doesn’t capture the full picture of what was purchased.

Level 3 is where things get specific. Level 3 credit card processing requires line-item detail for every transaction. We’re talking product codes, item descriptions, quantity, unit of measure, freight amounts, duty amounts, ship-to ZIP code, tax indicators, and discount per line item. It’s the kind of data that already lives in your ERP or accounting system. The question is whether it’s making it to the transaction.

What Level 3 Processing Requirements Actually Look Like

The reason Visa and Mastercard offer lower rates for level 3 payment processing is that the additional data essentially proves the transaction is a legitimate B2B purchase. When a corporate purchasing card is used to buy 200 units of a specific component from a distributor, that looks very different from a consumer buying something online. The networks want to see that difference reflected in the data.

To meet level 3 processing requirements, each transaction needs to include specific line-item fields. The exact requirements vary slightly between Visa and Mastercard, but the general framework is consistent. You need item-level product codes, quantities, and unit prices. You need to capture freight and duty if applicable. Ship-to ZIP code and a tax indicator are required. And every line item needs to be broken out separately, not lumped together into a single amount.

For companies that process a high volume of B2B transactions, getting this data attached to each payment is where the operational challenge tends to show up. Manually keying in line-item detail for every invoice isn’t realistic at scale. This is exactly why the payment processing solution you’re using matters so much.

Who Actually Benefits from Level 3 Credit Card Processing for B2B Companies

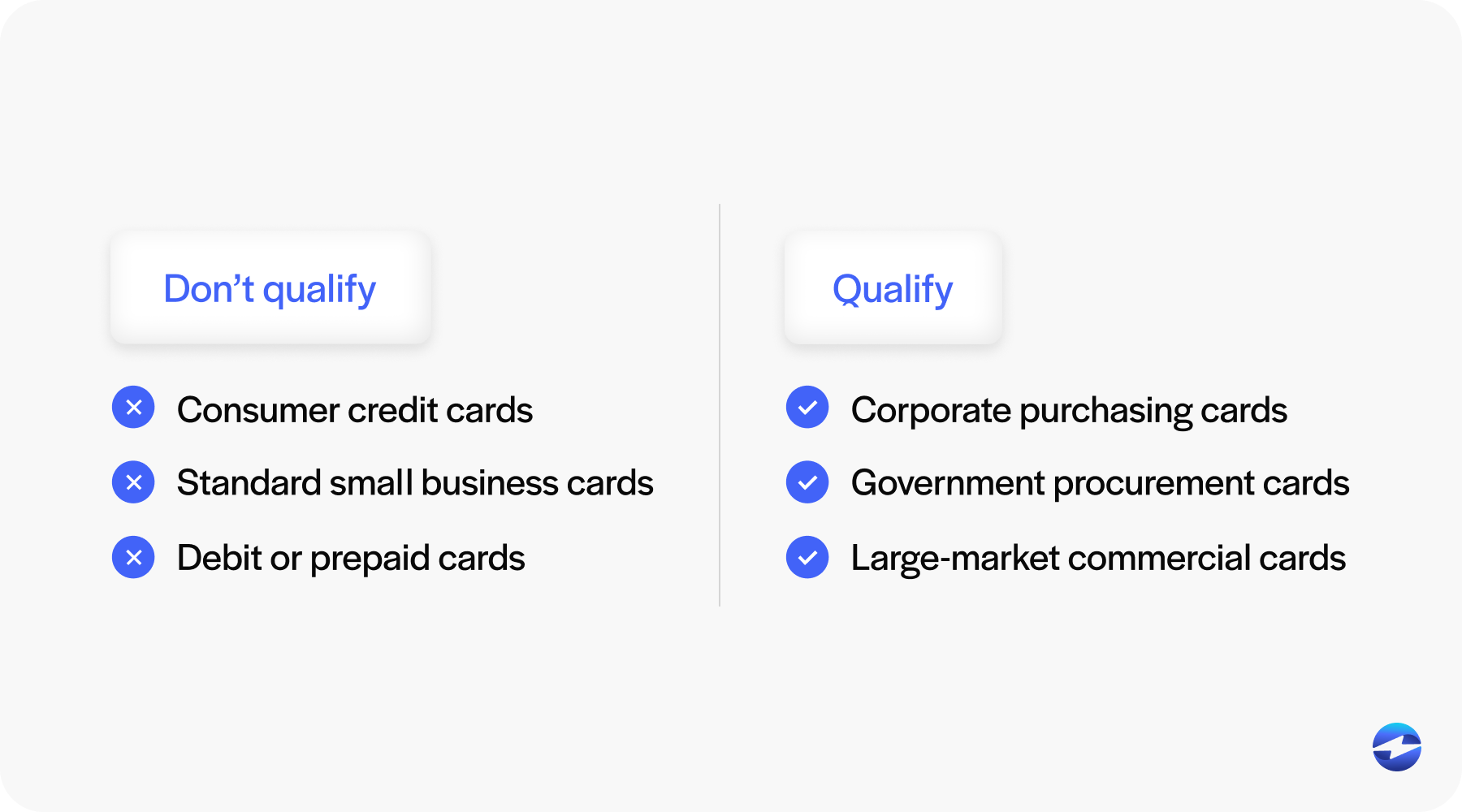

Not every transaction qualifies. Level 3 credit card processing for B2B companies only applies to commercial cards, purchasing cards, corporate cards, and certain government cards. If a customer pays with a standard consumer credit card, Level 3 data won’t change your interchange rate, because consumer cards don’t qualify for those programs.

For CFOs, AR managers, and billing teams processing significant monthly card volume from business customers, this distinction matters. If a meaningful portion of your card payments comes from corporate accounts paying with commercial cards, you’re likely sitting on real interchange savings that you’re not capturing.

Industries that see the biggest impact tend to be manufacturing, wholesale distribution, construction, and professional services. These are sectors with higher average transaction values and a customer base that regularly pays with purchasing cards or corporate accounts. Level 3 processing for B2B transactions with an average ticket of $5,000 saves dramatically more in real dollars than the same percentage savings on a $50 transaction.

What the Savings Actually Look Like

The difference between Level 1 and Level 3 interchange rates on a commercial card transaction can range anywhere from 0.30% to over 1.00%, depending on the card type and program. That might sound small in isolation, but it adds up quickly at volume.

Run $1 million in annual commercial card volume at Level 1 interchange. Now apply a conservative 0.50% rate reduction through level 3 processing rates. That’s $5,000 per year. On $5 million in volume, you’re looking at $25,000 or more. For businesses processing significant commercial card revenue, level 3 processing rates represent a meaningful reduction in one of their largest transaction costs.

The actual savings will depend on your card mix, average ticket size, and how your processor passes through interchange. Which brings up the next issue.

Why Most B2B Companies Aren’t Doing This Yet

Here’s the frustrating part. Many businesses qualify for Level 3 rates but aren’t getting them, either because their payment processor doesn’t support Level 3 submission, or because they technically support it but require manual data entry that nobody has time for.

The other common barrier is the disconnect between payment tools and the ERP. A business running NetSuite, Sage, Epicor, or any other major ERP system has all the line-item data they need sitting right there in the invoice. But if their payment processing solution operates outside the ERP, that data doesn’t automatically travel with the transaction. The invoice and the payment live in different systems and never communicate.

This is where businesses lose the benefit without realizing it. The data exists. It just never gets submitted.

How to Know If You’re Leaving Money on the Table

A few straightforward steps will help you figure out where you stand. Start by pulling a recent processing statement and look at the interchange categories your transactions are settling into. Most statements break this out by card type and qualification level, though the formatting varies by processor. If you’re seeing a lot of transactions settling at non-qualified or mid-qualified commercial card rates, that’s a signal.

Next, ask your current payment processor directly whether they support Level 3 data submission and whether it’s happening automatically on your account. Some processors support it in theory, but don’t enable it by default. Others don’t support it at all.

Finally, think about how your payment system connects to your ERP or accounting platform. If payments are processed through a separate gateway that doesn’t pull from your existing invoice data, the line-item detail required for level 3 credit card processing B2B companies need is probably getting left behind.

What to Look for in a Payment Processing Solution That Supports Level 3

If you’re evaluating options, a few criteria should be non-negotiable. The payment processing solution needs to have a native integration with your ERP, not a third-party connector that sits in between. Native means the line-item data from your invoices flows directly into the transaction without manual re-entry.

Level 3 data submission should happen automatically. You shouldn’t have to train your team to remember to add fields before processing a payment. The right system handles it in the background.

Pricing transparency matters too. Interchange-plus pricing means the savings from qualifying at Level 3 actually come back to you. Flat-rate pricing structures typically absorb that difference, and you never see the benefit.

Why EBizCharge Works for Level 3 Payment Processing

The EBizCharge payment processing solution is built specifically for B2B payment processing, and level 3 payment processing support is built into its design, not bolted on after the fact.

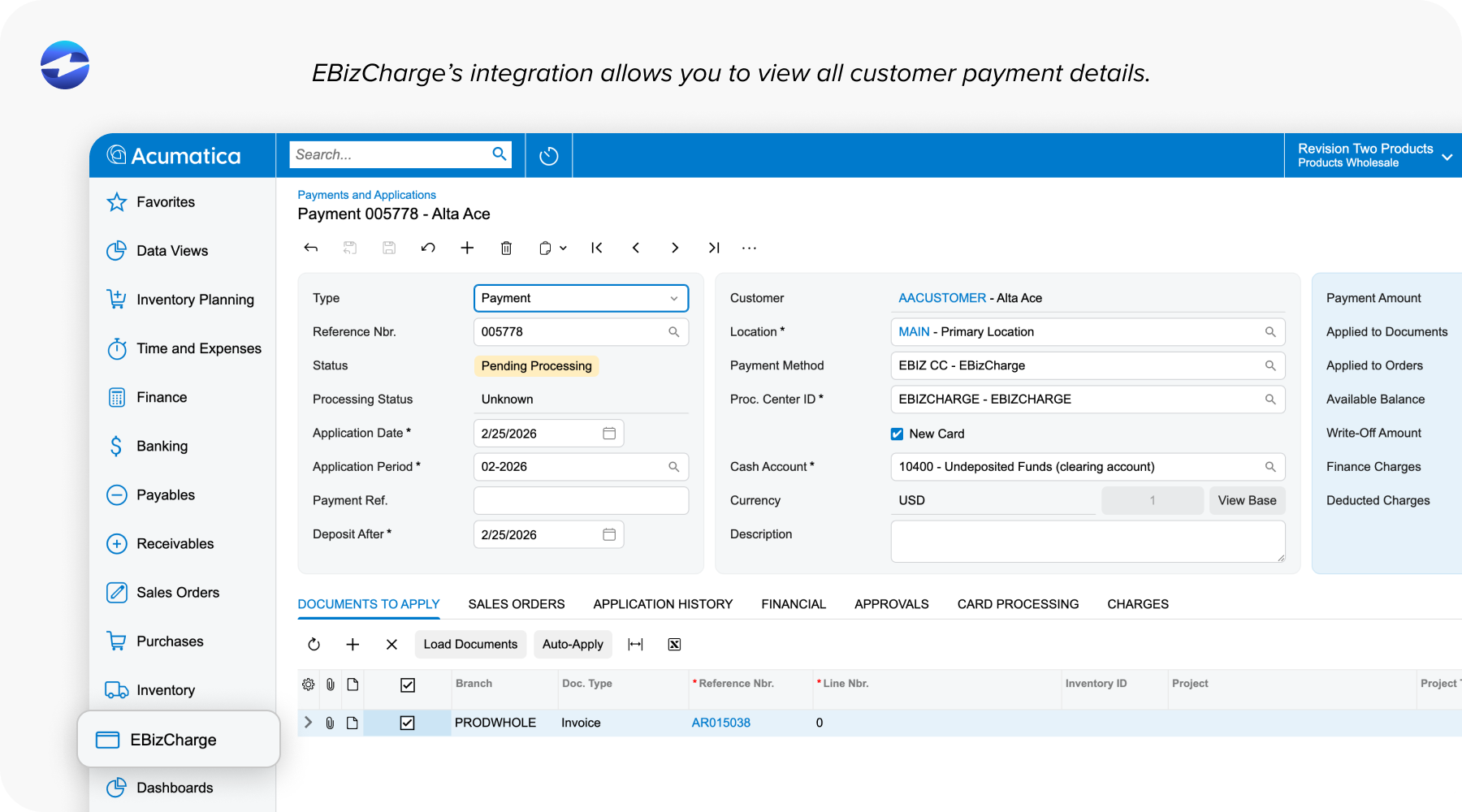

Because EBizCharge integrates natively with more than 100 ERP, CRM, and accounting platforms, including NetSuite, Sage, Epicor, QuickBooks, Microsoft Dynamics, and others, the line-item data required for level 3 processing for B2B transactions already exists inside the system where payments are processed. That data gets submitted automatically with each qualifying transaction. No manual entry. No missed qualifications.

EBizCharge uses interchange-plus pricing, which means when a transaction qualifies for lower Level 3 rates, those savings pass directly to the business. Twenty-plus years of B2B payment processing experience also means the company understands commercial card programs, qualification requirements, and how to ensure transactions settle at the correct rate.

If you’re not sure whether your current setup is actually submitting Level 3 data, that’s worth finding out. In many cases, the savings are already there. You just need the right system to capture them.