Blog > Level 2 vs. Level 3 Processing: What’s the Difference?

Level 2 vs. Level 3 Processing: What’s the Difference?

Most finance teams know that credit card processing fees aren’t flat. They vary by card type, transaction size, and a handful of other factors that processors don’t always explain clearly. What fewer people know is that those fees also vary based on how much data gets submitted with each transaction — and that businesses often pay more than they should simply because they’re not sending enough of it.

That’s the foundation of level 2 level 3 processing. The card networks have a tiered data system, and the more information a merchant submits with a transaction, the lower the interchange rate on qualifying cards. Most businesses default to the lowest tier without realizing there’s a better rate available. Understanding where level 2 vs level 3 falls in that system is the first step toward doing something about it.

Why the Tiers Exist

Card networks like Visa and Mastercard price interchange rates partly based on transaction risk. A transaction with more detail attached to it is easier to verify, harder to dispute, and less likely to represent fraud. In exchange for that data, the card network offers a lower rate.

The logic is straightforward. A charge that says “$6,800 — Acme Industrial Supply” tells the network very little. A charge that includes a PO number, itemized product codes, quantities, unit prices, line-level tax, and a ship-to address tells the network a lot. The second transaction is lower risk, and the rate reflects that.

The tiered system is largely invisible to most businesses because standard payment workflows don’t flag which tier a transaction qualified for. The fees show up on the statement, and most companies don’t look closely enough at the interchange category breakdown to notice when transactions are defaulting to a higher rate than necessary.

Level 1

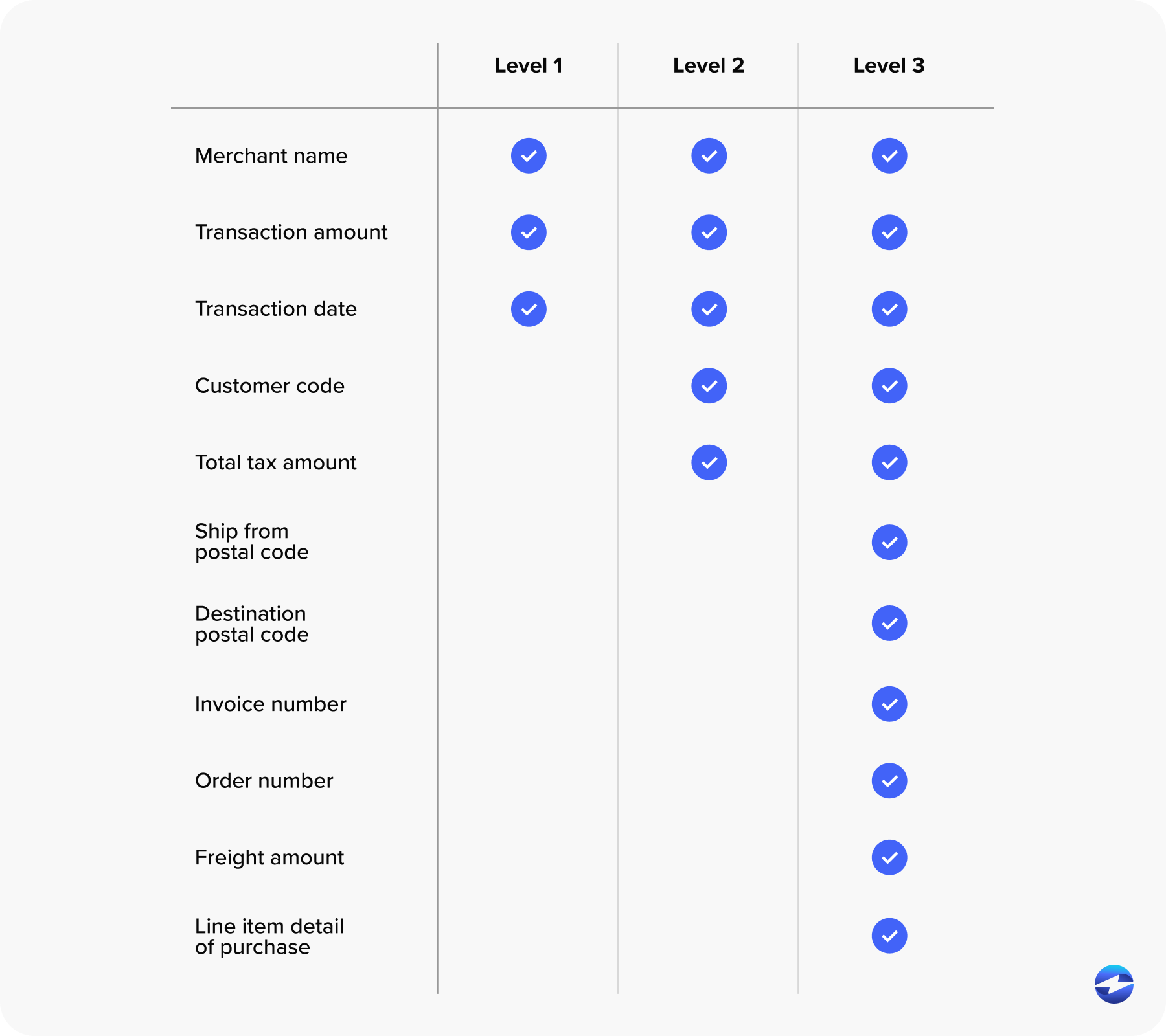

Level 1 is the minimum. It covers transaction amount, merchant name, and date. Every card transaction qualifies at level 1 by default.

For consumer-facing businesses — such as retail stores, restaurants, service businesses — level 1 is appropriate. The transaction type doesn’t call for detailed line-item data, and the interchange rates reflect that.

The problem for B2B companies is that commercial card transactions run at level 1 when additional data isn’t submitted, even when that data is readily available. That’s where the unnecessary cost creeps in.

Level 2 Processing

Level 2 adds a layer of detail on top of the level 1 baseline. The additional required fields are relatively straightforward: sales tax amount, customer code or purchase order number, and merchant postal code. Some processors also include invoice numbers depending on the card network and card type.

That’s it. For most B2B companies, this data already exists in the invoicing system. Tax amount and a customer reference number are standard components of a commercial invoice.

Level 2 and level 3 credit card processing both deliver interchange savings over level 1, but level 2 is the more accessible starting point. It typically saves somewhere in the 0.5% to 1% range on qualifying transactions. The qualifying card pool at level 2 is also broader — it covers a wider range of commercial and corporate card products than level 3 does.

Many small to mid-sized B2B companies should be running at level 2 and aren’t, simply because their payment processor isn’t submitting those additional fields by default. The data is there. It’s just not being used.

Level 3 Processing

Level 3 credit card processing goes significantly further. Instead of order-level summary data, it requires full line-item detail for every product in the transaction.

At the order level, you need the customer reference or PO number, total tax amount, ship-to ZIP code, freight and shipping amount, duty amount for international orders, and any order-level discount. At the line-item level, every product in the transaction needs its own set of fields: item product code or commodity code, item description, quantity, unit of measure, unit price, line item total, line-level discount, and line-level tax amount.

All of that data has to be submitted at the time of authorization and settlement. It can’t be added afterward. If any of it is missing when the transaction is processed, the transaction automatically downgrades to a lower tier.

Level 3 processing rates deliver additional savings on top of level 2 — typically another 0.5% to 1%, depending on card type and network. When you stack that on top of the level 2 savings over level 1, the cumulative difference is meaningful. For a company processing $400,000 per month in commercial card volume, the gap between consistent level 1 qualification and consistent level 3 qualification can reach $20,000 to $40,000 per year or more, depending on the card mix.

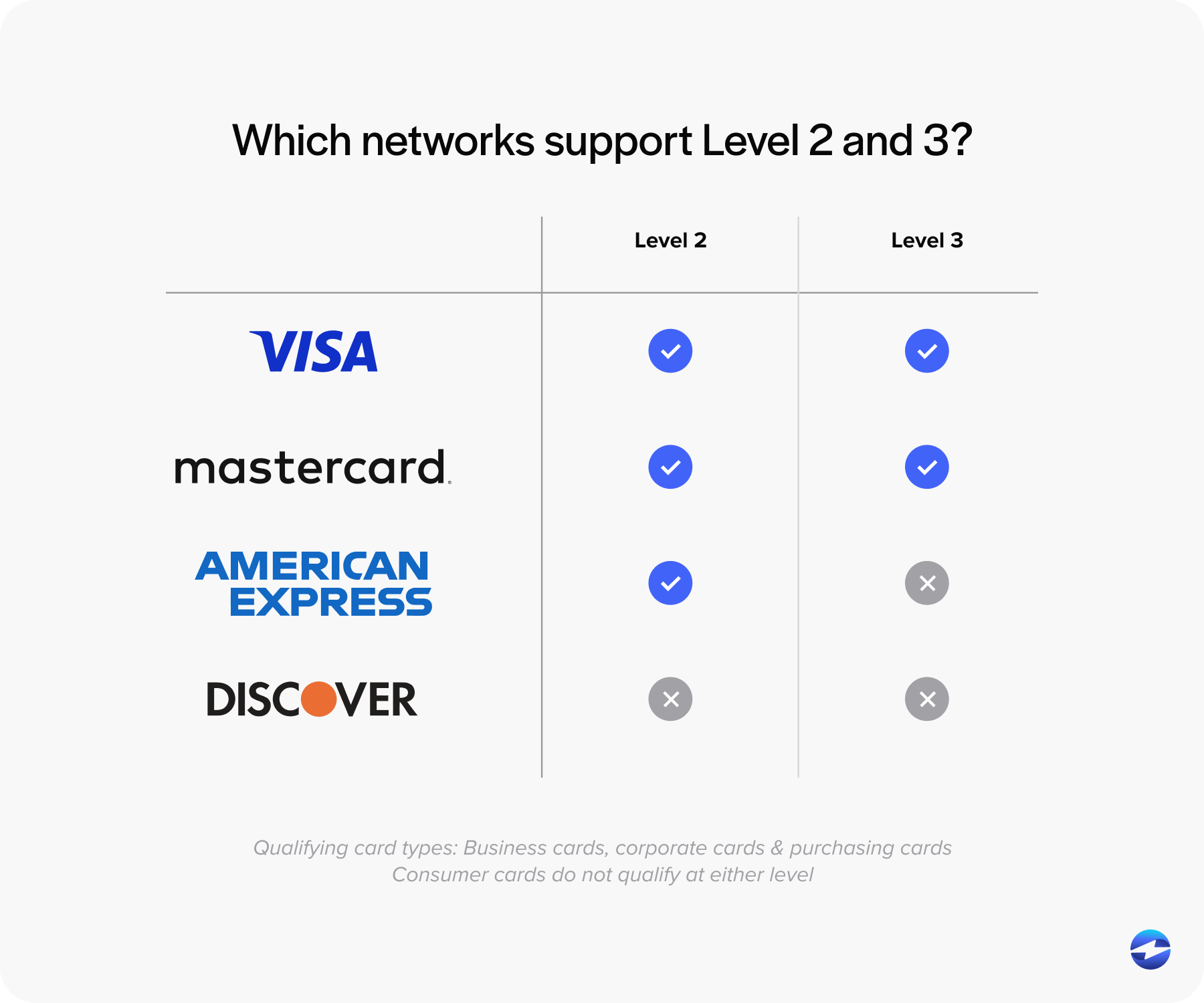

Level 3 applies to a more specific set of card types than level 2: corporate purchasing cards, government procurement cards like the GSA SmartPay program, and large-market commercial Visa and Mastercard cards. Consumer credit cards and standard small business cards don’t qualify, regardless of the data submitted.

Level 2 vs Level 3: The Practical Differences

For CFOs, controllers, and AR managers trying to figure out where to focus, here’s the clearest way to think about the comparison.

Level 2 and 3 credit card processing both exist to reduce interchange costs on commercial card transactions. They share the same underlying logic. But they differ in a few important ways.

The data requirements are different in kind, not just quantity. Level 2 is order-level. Level 3 is line-item. That’s a structural difference that affects which businesses can realistically implement each tier and what payment infrastructure they need.

The qualifying card types are different. Level 2 covers more commercial card products broadly. Level 3 is narrower and more specific to corporate purchasing and government cards. If your customers are primarily paying with those card types, level 3 matters a lot. If they’re mostly using standard commercial cards, level 2 may be the more relevant tier.

The implementation requirements are different. Getting to level 2 is usually achievable with minimal system changes for businesses already capturing tax and PO data. Getting to level 3 payment processing consistently requires a payment processing solution that can pull line-item data from the source system automatically at settlement. That’s where the ERP integration piece becomes critical.

The Downgrade Problem

Both tiers come with the same hidden risk: silent downgrades.

When a transaction that should qualify at level 2 or level 3 is missing required data fields, it falls back to a lower tier rate automatically. No alert. No notification on the statement. The business just pays the higher rate and moves on, usually unaware that anything went wrong.

Downgrade triggers are often small: a missing tax amount, an absent PO number, an incomplete commodity code. The fix for any individual transaction is trivial. But when it’s happening across hundreds or thousands of transactions per month because the payment processor isn’t submitting the right data by default, the cumulative cost is substantial.

This is why it’s worth asking your current payment processor to show you the interchange category breakdown on a recent statement. Specifically: what percentage of your commercial card transactions qualified at level 2 or level 3, and what percentage downgraded to level 1? If they can’t show you that clearly, that’s information in itself.

Which Tier Should Your Business Be Targeting?

The honest answer for most B2B companies is that level 3 is the right target if two conditions are true: your customers are paying with corporate purchasing or government cards at meaningful volume, and your invoicing system already captures line-item data at the product level.

Most ERP platforms already do. Product codes, quantities, unit prices, line-level tax, and shipping amounts are standard components of a B2B invoice. The data infrastructure for level 3 is usually already in place. The missing piece is a payment processing solution that can access that data and submit it automatically at settlement.

If your commercial card volume is low or your customer base skews toward standard small business cards rather than corporate purchasing cards, level 2 is the more practical and immediately achievable improvement. It’s not as dramatic as level 3, but it’s still real savings that most businesses aren’t capturing.

The Integration Factor

The tier a business actually qualifies for has as much to do with the payment processor and integration as it does with the business itself.

Level 2 and level 3 credit card processing both rely on the processor submitting the right data fields at the right time. When a payment solution is embedded directly in the ERP or accounting platform where invoices are created, that handoff happens automatically. The AR team processes the payment the same way they always have. The data goes with it. No manual entry, no separate workflow, no risk of a field being missed.

A standalone payment gateway with no ERP connection creates a data gap. The line-item information exists on the invoice, but it never reaches the transaction. The business qualifies at a lower tier as a result, often without realizing it.

Qualifying at the Right Tier Every Time

Level 2 and level 3 processing represent real, recurring savings for B2B companies processing commercial card volume. The difference between them is the depth of data required and the card types they apply to. Most businesses should be at one tier or the other, and many are at neither.

EBizCharge’s payment processing solution is built to close that gap. Because it integrates natively into 100+ ERP, CRM, and accounting platforms — including NetSuite, Sage, Microsoft Dynamics, and Acumatica — it sits inside the system where invoice data already lives. Level 2 fields, like tax amount and customer code, are submitted automatically. So is the full line-item detail required for level 3 payment processing. Every eligible transaction qualifies at the best available rate without anyone on the AR team having to do anything differently.

If you’re not sure which tier your transactions are currently hitting, pull a recent statement and ask your payment processor to walk you through the interchange category breakdown. That single conversation will tell you exactly where the opportunity is.