Blog > Does Your Payment Processor Support Level 3? (Stripe, Square, CardConnect, & More)

Does Your Payment Processor Support Level 3? (Stripe, Square, CardConnect, & More)

Here’s a situation that comes up more than you’d think. A B2B company figures out they’ve been eligible for level 3 processing rates the entire time, asks their payment processor about it, and gets one of two responses: either a vague confirmation that level 3 is “supported,” or a blank stare followed by a callback that never comes.

Both responses are a problem.

The phrase “level 3 support” gets used loosely in the payments industry. There’s a real difference between a processor that technically handles level 3 data under specific conditions and one that submits it automatically on every eligible transaction without any extra work from your team. For B2B companies processing significant commercial card volume, that difference shows up directly on the processing statement.

This article walks through how the most commonly used processors actually handle level 3 payment processing, where the gaps tend to appear, and what you should be asking before you commit to any platform.

A Quick Level 3 Recap

Level 3 credit card processing is the highest tier of interchange data submission. Card networks like Visa and Mastercard reduce interchange rates on transactions where detailed line-item data is submitted: product codes, quantities, unit prices, line-level tax, shipping amounts, and a customer PO number, among other fields. The more data submitted, the lower the rate on qualifying cards.

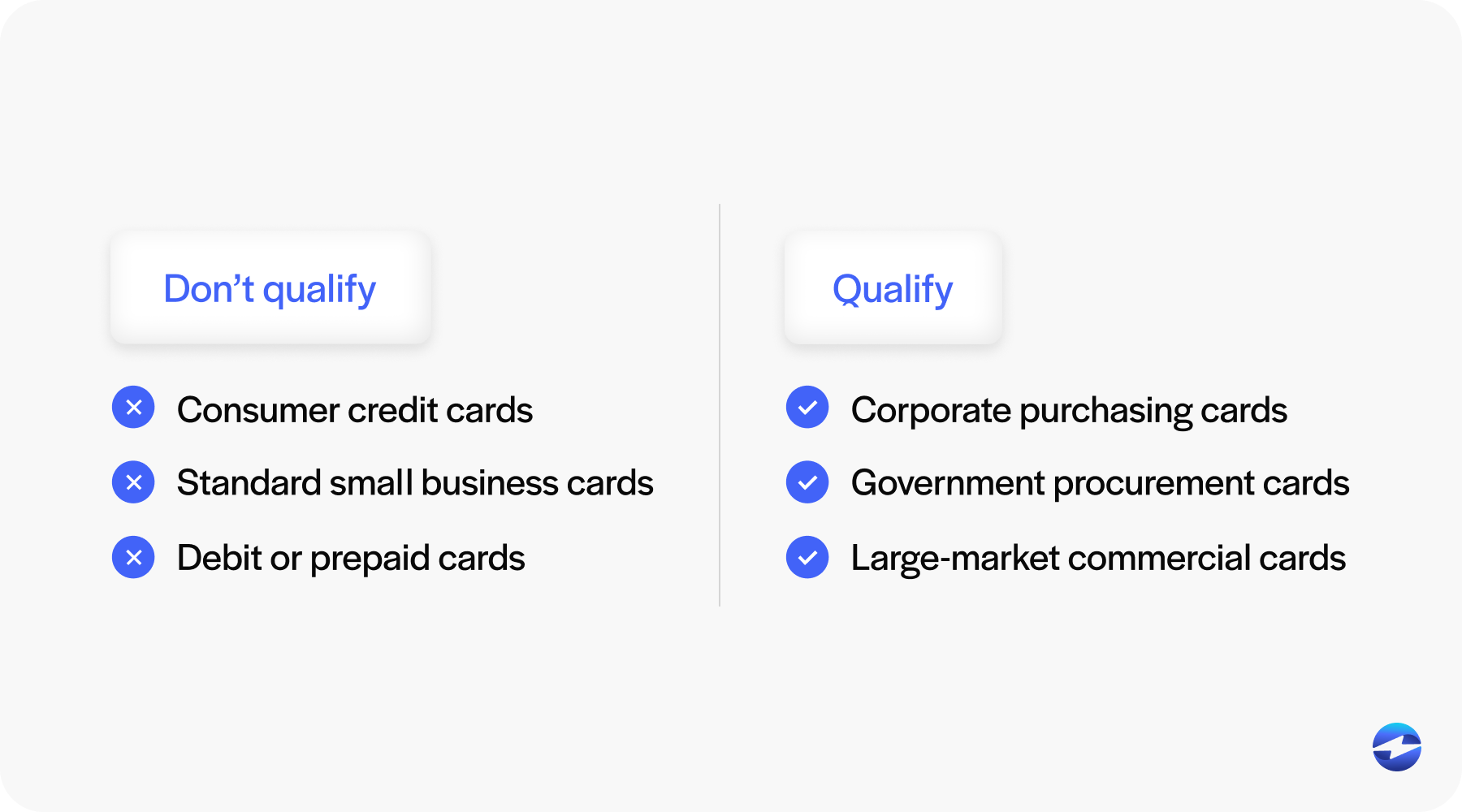

Level 3 only applies to specific card types: corporate purchasing cards, government procurement cards, and large-market commercial cards. Consumer cards don’t qualify regardless of what data you submit.

The savings at level 3 processing rates can be significant for companies with meaningful commercial card volume. The challenge is that actually qualifying for those rates depends entirely on whether your payment processor is set up to capture and submit the right data automatically.

What “Level 3 Support” Actually Means

Before getting into individual processors, it helps to define what genuine level 3 support looks like versus what it often is in practice.

Real level 3 support means the processor automatically captures and submits all required line-item data fields at the time of authorization and settlement, on every eligible transaction, without anyone on your team having to do anything beyond processing the payment normally. No manual data entry. No custom application programming interface (API) development. No separate workflow to maintain.

What passes for level 3 support in many cases is something different: the capability exists in the API documentation, but it requires a developer to build the implementation. Or it’s available as an add-on. Or it technically works, but requires the AR team to enter line-item fields by hand for every transaction, which doesn’t happen consistently at any real volume.

When level 3 data is missing or incomplete at settlement, the transaction quietly downgrades to level 1 or level 2 rates. No notification. No flag on the statement. Just a higher cost that most businesses absorb without realizing there was a better rate available.

With that framework in place, here’s how the major processors stack up.

Stripe

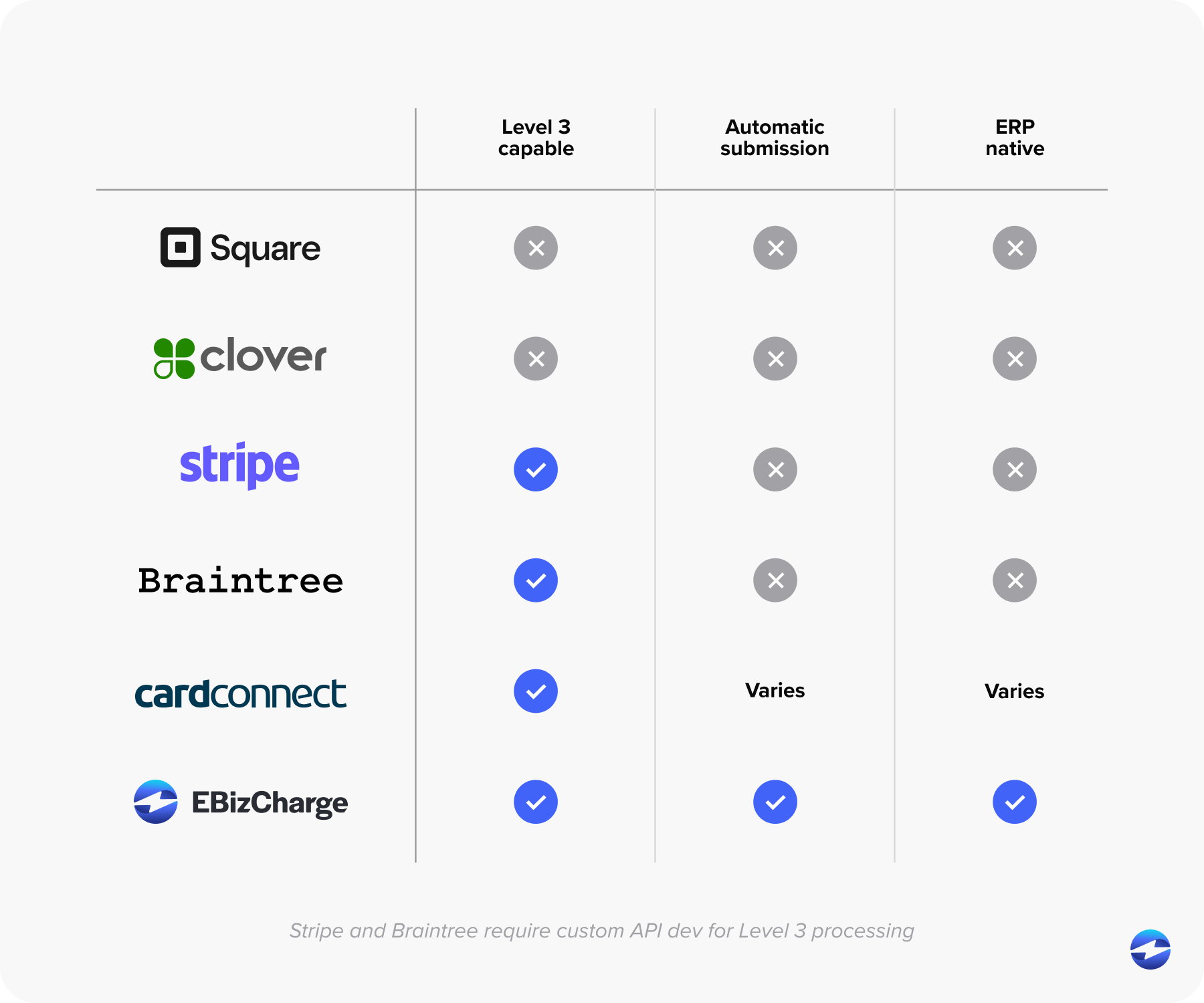

Stripe level 3 processing is technically available, but it’s built for developers, not for AR teams.

To submit level 3 data through Stripe, merchants need to pass line-item information programmatically through Stripe’s API at the time of charge creation. If you have an engineering team actively managing your payment integration, this is workable. If you’re a wholesale distributor or manufacturer with an AR department processing payments through an ERP, it’s not a realistic path to consistent level 3 qualification.

Stripe is a strong product for what it was designed for: developer-led, online, and consumer-facing payment flows. B2B companies processing invoices through an ERP are not the core use case, and Stripe level 3 processing reflects that. The capability is there in the documentation, but the workflow required to use it doesn’t match how most B2B businesses actually operate.

Square

Square level 3 processing doesn’t exist. Square is built for in-person retail, food service, and small consumer-facing businesses. Its interchange optimization features don’t extend to level 3 commercial card data, and there’s no path to level 3 qualification within the Square ecosystem.

For B2B companies running commercial card transactions through Square, every one of those transactions is defaulting to level 1 rates regardless of card type or volume. It’s built for a different market, and the B2B commercial card use case isn’t one it addresses.

CardConnect

CardConnect level 3 processing is more relevant than either Stripe or Square for B2B use cases. CardConnect is an acquiring processor with a stronger commercial card orientation, and its gateway does support level 3 data submission.

The nuance is that effective CardConnect level 3 processing depends on how it’s implemented. For businesses that have a working ERP integration with CardConnect and the technical setup to pass line-item data through consistently, it can be a solid option. For businesses running through the standalone gateway without an ERP connection, the same problem applies: someone has to manually enter line-item data for every transaction, and that doesn’t scale.

If CardConnect is your current payment processor and you’re not sure whether level 3 is being submitted automatically on eligible transactions, that’s worth a direct conversation with your account rep. Ask for documentation showing which transactions hit level 3 rates and which were downgraded. The answer will tell you a lot.

Braintree

Braintree level 3 processing follows a similar pattern to Stripe. Braintree, which is owned by PayPal, is a developer-facing gateway with level 3 capability available through its API. The platform can handle the data requirements, but the implementation depends on custom development work to pass line-item fields at the time of transaction.

For B2B companies, Braintree level 3 processing faces the same practical limitation as Stripe: the workflow required to qualify consistently doesn’t fit the way most ERP-based businesses process payments. It’s a gateway built for online commerce, and level 3 is available as a technical feature rather than a built-in default for commercial card transactions.

Clover

Clover level 3 processing is limited. Clover is primarily a point-of-sale platform oriented toward retail and restaurant environments. Like Square, it’s not built for B2B commercial card workflows, and its level 3 support is minimal at best.

B2B companies processing corporate purchasing card transactions through Clover level 3 processing will find the same gap: the platform isn’t designed for the transaction type that level 3 serves. If your business relies heavily on commercial card volume from corporate or government buyers, Clover is not the right payment processing solution for that use case.

The Pattern Across All of Them

Stepping back from the individual processors, a clear pattern emerges.

Consumer-facing platforms like Square and Clover don’t support level 3 in any practical sense. Developer-dependent platforms like Stripe and Braintree support it in principle but require custom engineering work that most B2B companies aren’t positioned to maintain. Mid-market processors like CardConnect support it more intentionally, but effectiveness still depends on whether the payment workflow is connected to the system where line-item data actually lives.

For CFOs, controllers, and AR managers evaluating their options, the conclusion is consistent: level 3 payment processing only works reliably when the payment processor is embedded in the system where invoices originate. That’s where the data is. The processor needs to be able to reach it automatically at settlement, without any manual steps in between.

Questions to Ask Any Processor Before You Commit

Regardless of which payment processor you’re evaluating, these questions will separate genuine level 3 support from surface-level claims.

Does your platform submit level 3 data automatically on eligible transactions, or does it require API development or manual entry? Does your payment processing solution integrate natively with my ERP and pull line-item data from existing invoices? How do you handle transactions where level 3 data is incomplete — do they downgrade, and will I know when they do? Can you show me on a recent statement which transactions qualified at level 3 rates and which didn’t?

A processor that genuinely supports level 3 credit card processing will answer those questions directly. Vague responses or redirects to technical documentation are signals worth taking seriously.

Why EBizCharge Is the Right Fit for Level 3

Most processors covered here have some version of level 3 capability. The practical reality is that for B2B companies on ERP platforms, capability in the documentation and automatic qualification on every eligible transaction are very different things.

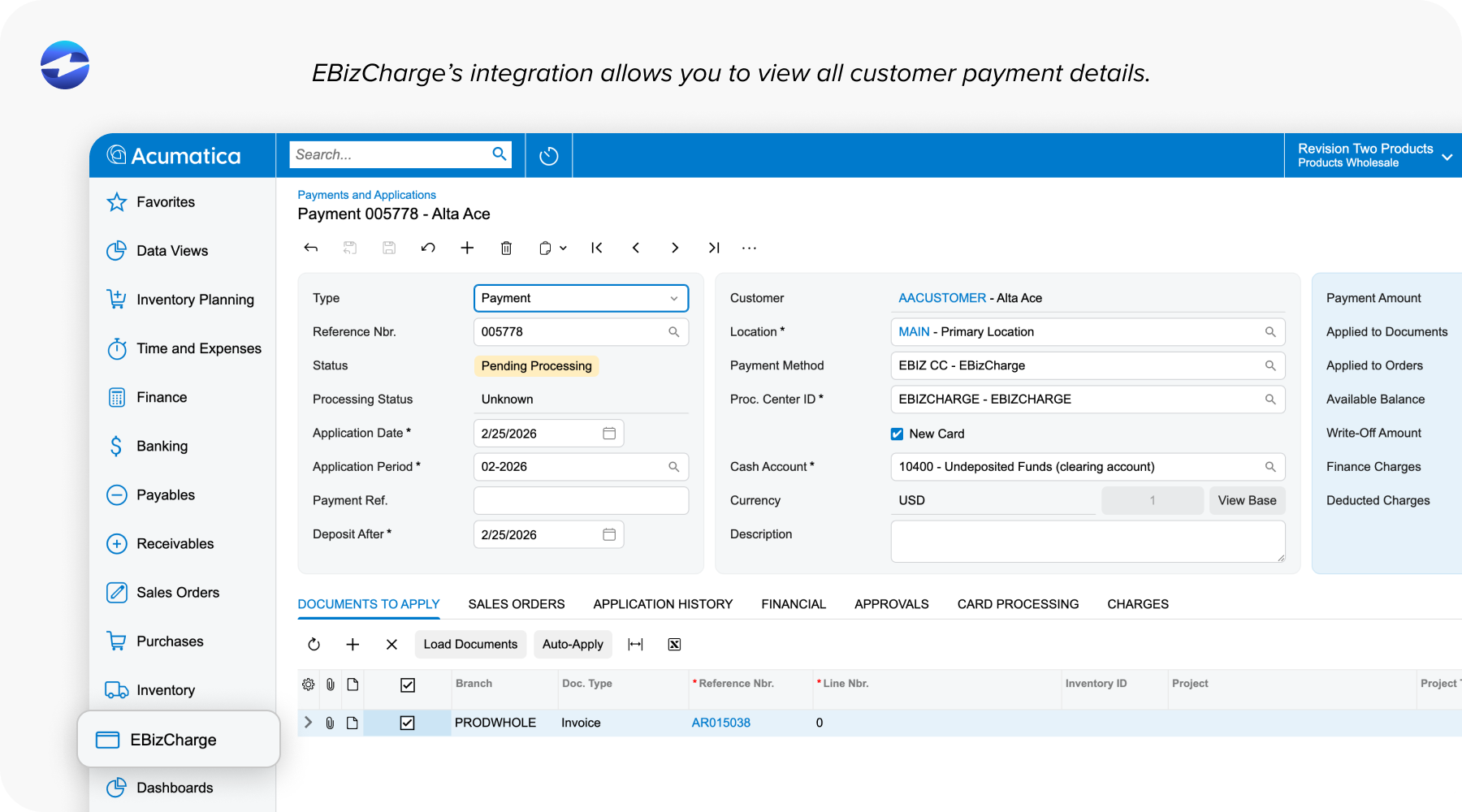

EBizCharge’s payment solution is built specifically for B2B payment environments. It integrates natively into 100+ ERP, CRM, and accounting platforms — including NetSuite, Sage, Microsoft Dynamics, Acumatica, and others — and sits directly inside the system where invoices are created. That means the line-item data required for level 3 payment processing is already there, and EBizCharge submits it automatically at settlement on every eligible transaction. No API development, no manual entry, no separate workflow.

With over 20 years in B2B payment processing, EBizCharge is designed for the transaction types and workflows that level 3 was built for. If you’re currently processing commercial card volume and aren’t certain you’re hitting level 3 processing rates on eligible transactions, the first step is pulling a recent statement and asking your current payment processor to show you exactly where those transactions landed. If they can’t show you clearly, that’s the answer.