Blog > Debit Card Surcharging: Is It Legal?

Debit Card Surcharging: Is It Legal?

If you’ve ever wondered whether it’s legal to add a surcharge when someone pays with a debit card, you’re not alone. It’s a common question – especially for business owners looking for ways to manage rising processing fees.

The short answer? No, debit card surcharging isn’t legal in the U.S. But that’s just the tip of the iceberg. The rules behind it come from a mix of card network policies, federal law, and state regulations.

What is a surcharge?

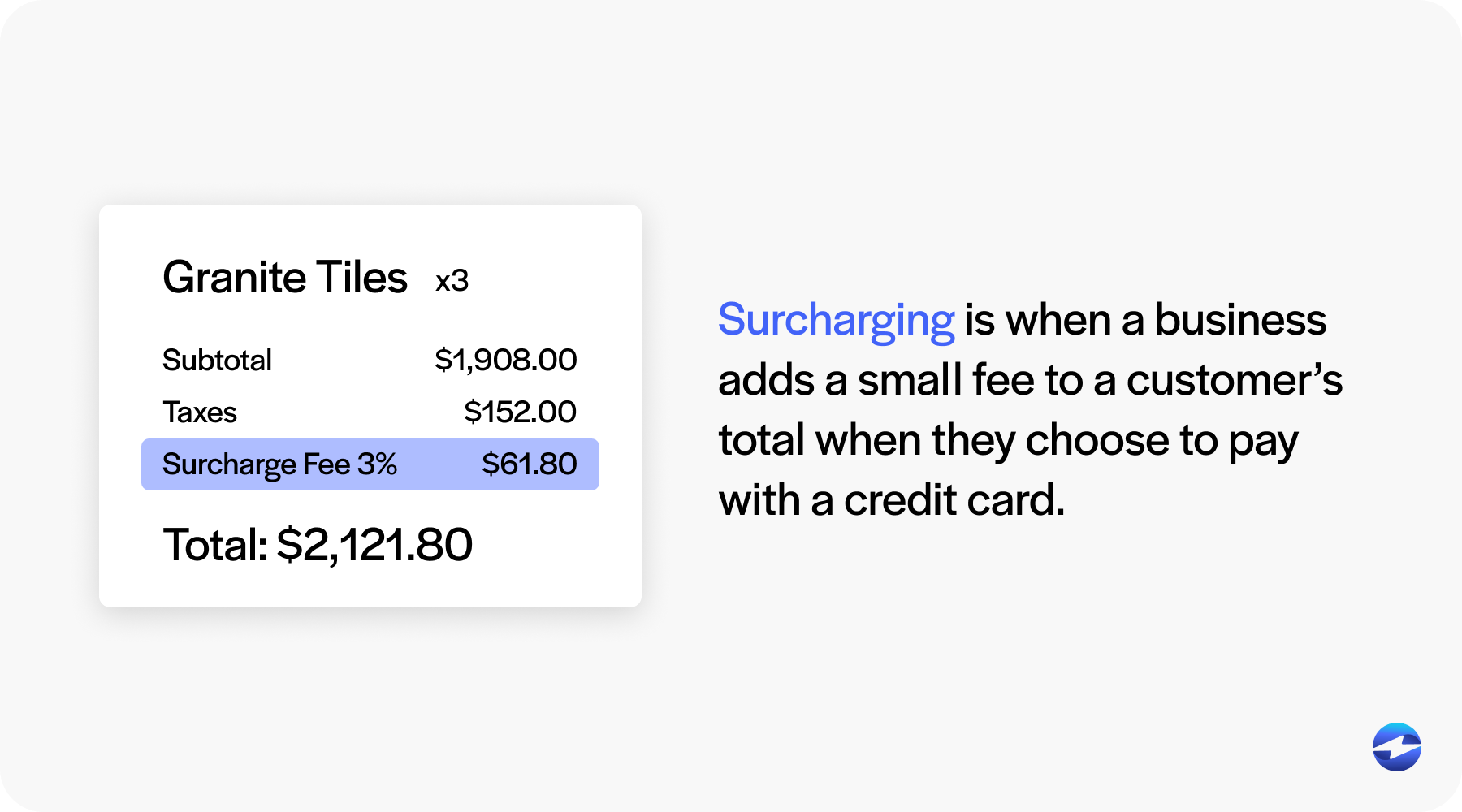

Surcharging is when a business adds a small fee to a customer’s total when they choose to pay with a credit card. It’s usually meant to cover the cost of credit card processing – the fees that businesses pay every time someone swipes, dips, or taps their card.

The idea is pretty straightforward: passing along the cost of accepting credit cards instead of absorbing it. For small businesses, especially those with tight margins, even a 2% or 3% fee per transaction can add up over time. Surcharging is one way to make those costs more visible – and to shift it, at least partially, to the person choosing the more expensive payment method.

Let’s say you buy a $50 item, and the store has a 3% surcharge for credit card use. You’d end up paying $51.50 if you used your credit card instead of cash or a check. That $1.50 goes toward offsetting what the business must pay the processor or card networks, like Visa or Mastercard.

Can you surcharge a debit card?

No, you cannot surcharge a debit card in the United States. All major card networks, including Visa, Mastercard, American Express, and Discover, prohibit merchants from adding surcharges to debit card transactions, even when the card is processed as credit. This restriction is reinforced by the Durbin Amendment, a federal law that regulates debit card fees. Credit card surcharging, however, is permitted in most states when disclosed properly.

If you run a business – or are someone who pays attention to the line items on your receipts – it helps to know how surcharging rules work. If you’re a merchant trying to stay compliant or a consumer just trying to make sense of what you’re being charged, it’s worth understanding where these rules come from and what they mean.

Is it illegal to charge a debit card fee?

It depends on the type of fee. Adding a surcharge to a debit card transaction is prohibited under card network rules and reinforced by federal law. Convenience fees, however, can legally apply to debit card transactions when structured correctly. The distinction comes down to what the fee is actually for and how your business collects payments.

Most merchants asking this question are looking for something broader: is there any legitimate way to recover debit card processing costs from the customer? The answer is yes, in certain situations.

How to to pass debit card fees on to customers

Convenience fees are one legitimate option, but whether they work for your business depends on how you typically collect payments. Here’s the basic structure: if your standard payment method is check, mail, or in person, and you also offer an online or phone payment option, you can charge a flat fee for that alternative channel. Debit card customers using that channel pay the fee just like everyone else. The fee has to be a flat dollar amount, not a percentage, and disclosed before the customer completes the transaction. That’s the catch though. The fee is tied to the channel, not the card type, so it only works if card payment is genuinely an alternative for your business rather than your primary method. Utilities, municipalities, property managers, and periodic billers tend to fit this model well. Retail stores and restaurants generally don’t, because card payments are already the everyday standard.

Minimum purchase requirements are another tool. The Durbin Amendment permits merchants to set a minimum transaction threshold of up to $10 for card payments, debit included. It doesn’t pass a fee to the customer directly, but it does limit card use on small transactions where processing costs hit hardest relative to the sale amount.

Government and public sector entities operate under a different set of rules than private merchants. Federal, state, and local agencies are often authorized to charge a card processing fee on debit transactions, as long as it reflects actual processing costs and is clearly disclosed. That’s why paying a tax bill or a DMV fee by card online typically carries a separate fee. This authorization doesn’t extend to private businesses.

For most merchants in retail, restaurants, or B2B services where card payment is the everyday norm, none of these options recover debit costs directly. The realistic alternatives are minimum purchase thresholds, cash discount programs, or building processing costs into your pricing. Credit card surcharging is also available in most states for credit transactions, with proper disclosure and within card network caps.

To reiterate, you can’t add a fee to a debit card transaction simply because the customer paid with debit. There are legitimate structures that allow cost recovery in specific contexts, but card networks and regulators look at the substance of the charge, not the label on the receipt. Understanding where those rules actually come from helps clarify what you’re working with.

Surcharging Card network rules

Most of the guidelines around surcharging don’t come from lawmakers – they come from the card networks themselves. These networks set the terms for how their cards can be used, and if you want to accept their payments, you agree to play by their rules.

Most networks do allow credit card surcharging – but they don’t leave it wide open. Usually, there’s a cap: you can’t charge more than 4% of the transaction amount. You must clearly disclose the surcharge before the customer pays. That means signage at the register, notices on receipts, and online alerts if you’re an eCommerce business.

Debit cards are a different story. Even if a debit card is run “as credit” – something customers often do to avoid entering a PIN – the networks still classify it as a debit transaction. And surcharges on debit cards are a no-go across all the major card brands.

Federal law

In addition to card network rules, there are federal laws that govern how surcharging works in the U.S. One of the most significant is the Durbin Amendment – part of the Dodd-Frank Act, which was passed after the 2008 financial crisis.

The Durbin Amendment mainly deals with debit card fees. It limits how much banks can charge businesses to process debit card transactions, especially when the bank has more than $10 billion in assets. This was intended to reduce costs for merchants – and in many cases, it did.

But here’s where it gets tricky: the law doesn’t say much about surcharges directly. It doesn’t ban them, but it doesn’t give businesses a free pass either. Instead, it creates a framework that requires businesses to follow card network rules and local laws. So federal law gives a foundation, but real enforcement power often lies elsewhere.

State-level laws

This is where things get complicated. Some states are totally fine with surcharges as long as you disclose them properly. Others, like California or New York, have had surcharging laws that either ban surcharging outright or impose strict conditions.

That means a business operating legally in one state might be breaking the rules just by doing the same thing across state lines. In places where surcharges are allowed, you might be required to display the cash price and card price side by side. In others, any extra charge could be considered deceptive – or even illegal.

These laws are also constantly evolving. Court challenges have overturned some of the older bans, and new legislation pops up regularly. Compliance with surcharge laws requires constant monitoring of relevant rules and regulations.

Why debit surcharging is generally prohibited

If you’re wondering why you rarely – if ever – see a debit card surcharge at checkout, there’s a reason for that. In most cases, adding a fee to a debit card transaction just isn’t allowed. It’s something that’s generally off the table for U.S. merchants.

This restriction primarily stems from the Durbin Amendment. But the law also led to a stricter line around debit card surcharges. Unlike credit cards, which can incur additional fees under certain conditions, debit cards fall into a different category. They’re typically cheaper to process, and they pull funds directly from a bank account. So, there’s no need for an extra charge.

Why is this rule in place?

There are a few reasons behind the restriction:

- Consumer protection comes first. Lawmakers didn’t want people to face extra costs just for using a debit card, which is often the most straightforward and debt-free way to pay.

- Debit is safer for the average person. It doesn’t rack up interest. It’s tied to money the customer already has. By keeping it surcharge-free, there’s an incentive to use it over credit.

- It keeps things simple across the board. While states can still make their own rules, this restriction from the federal level sets a basic, consistent standard. It helps avoid confusion for both merchants and customers.

If you’re unsure about how these rules apply to your business, it’s worth taking the time to research.

Debit Card Surcharge Laws by State (2026)

Card network rules from Visa, Mastercard, American Express, and Discover prohibit debit card surcharges everywhere in the United States. There is no state that overrides that. So regardless of where your business operates, adding a fee to a debit card transaction is off the table.

That said, state laws create a second layer of rules and the penalties for violating consumer protection statutes vary quite a bit from state to state. If you’re a merchant trying to understand your exposure, or a consumer who was charged a fee you shouldn’t have been, knowing your state’s posture matters.

Here’s a breakdown of how key states approach surcharging:

| State | Debit Surcharge Permitted? | Additional Context |

|---|---|---|

| California | No | Card network rules apply. State law (Cal. Civil Code §1748.1) historically banned credit card surcharges, though legal challenges have complicated enforcement. Civil penalties under consumer protection law apply for debit violations. |

| Flordia | No | Card network rules apply. State statute §501.0117 restricted surcharging broadly, though it has faced First Amendment challenges. Merchants can face class-action exposure under Florida’s consumer protection statutes. |

| New York | No | Card network rules apply. NY’s surcharging law was challenged in Expressions Hair Design v. Schneiderman (SCOTUS 2017) and later struck down for credit cards. Debit surcharges remain prohibited regardless. AG enforcement is active. |

| Pennsylvania | No | Card network rules apply. No specific surcharging statute, but the Unfair Trade Practices and Consumer Protection Law covers unauthorized fees broadly. Civil liability applies. |

| Texas | No | Card network rules apply. Texas is more merchant-friendly on credit card surcharges with disclosure. Debit surcharging is still prohibited under network rules regardless of disclosure. |

| All other states | No | Federal framework and network rules apply universally. Some states restrict credit card surcharges further; none permit debit surcharges. |

A few of these states come up frequently enough in billing disputes and compliance questions that they’re worth more context.

California gets a lot of attention because of its history with surcharging litigation. The state originally prohibited credit card surcharges under Civil Code §1748.1, but that law was effectively struck down after a federal court found it violated free speech protections on pricing disclosure. Credit card surcharging with proper disclosure is now generally permitted in California. Debit card surcharging is not — and California’s consumer protection enforcement tends to be aggressive. Customers who are charged a debit fee can report the merchant to the California Department of Consumer Affairs or the state Attorney General.

Florida is notable in the GSC data because it generates a high click-through rate on state-specific queries. Florida statute §501.0117 was another surcharging restriction that faced constitutional challenges, with the 11th Circuit striking it down in 2016. Merchants in Florida can now surcharge credit card transactions with disclosure. Debit surcharges remain prohibited. The Florida Deceptive and Unfair Trade Practices Act (FDUTPA) gives consumers and the AG grounds to pursue businesses that charge unauthorized fees, and class-action lawsuits are a documented risk.

Pennsylvania doesn’t have a dedicated surcharging statute, which sometimes creates confusion. The absence of a specific law doesn’t mean surcharging debit is allowed — card network rules still govern. What Pennsylvania does have is a broad consumer protection framework under the UTPCPL that covers deceptive business practices, including undisclosed fees.

These laws are also not static. Court rulings, legislative updates, and regulatory guidance can shift the picture in any given state. If surcharging compliance is material to your business operations, it’s worth reviewing with a payments attorney who tracks these developments.

Consequences of non-compliance

Non-compliance with surcharging rules and regulations can cause serious problems. If you apply a surcharge when you’re not supposed to – especially on a debit card – you could face fines, lawsuits, or even lose your ability to accept card payments. Unauthorized debit surcharges may be characterized as junk fees under federal consumer protection frameworks.

Breaking those rules can result in higher processing fees or having your merchant account shut down entirely. On top of that, there’s your reputation to think about. Customers notice extra fees, and if they feel they’ve been charged unfairly, they may not come back – or worse, they may spread the word.

Different states have different penalties. For example, California and New York can impose civil fines or even take legal action against businesses that surcharge illegally. In Florida, you might be exposed to class-action lawsuits. That’s why staying up to date on both local laws and network rules is important. It’s not just about compliance – it’s about protecting your business and maintaining trust with your customers.

Simplifying surcharging with EBizCharge

For businesses seeking a compliant and streamlined way to implement credit card surcharging, EBizCharge provides a reliable and effective solution. Designed to help merchants recover the cost of credit card processing, EBizCharge’s surcharging feature automates the process while ensuring adherence to card network rules and applicable state laws.

One of the key advantages of the EBizCharge payment processing solution is its intuitive interface, which allows merchants to easily configure surcharge settings and apply them automatically to qualifying credit card transactions. This automation not only reduces the risk of manual errors but also helps ensure that surcharges are applied consistently and within the bounds of legal and regulatory requirements.

Additionally, EBizCharge integrates seamlessly with a wide range of payment systems and ERP software, including QuickBooks payment processing, NetSuite credit card integration, and Acumatica payment gateway solutions. This makes it a practical option for businesses of all sizes that want compliant surcharging built directly into their existing workflows. Dedicated support is also available to assist with implementation, configuration, and ongoing use.

EBizCharge takes the guesswork out of surcharging by giving businesses in the U.S and Canada a simple, compliant way to manage costs without the headache.

Frequently Asked Questions

Is it illegal to charge a fee for using a debit card?

It depends on the fee type. Surcharging a debit card transaction is prohibited under card network rules and the Durbin Amendment. Convenience fees, however, can legally apply to debit transactions when structured as a flat amount, tied to a non-standard payment channel, and disclosed before payment.

Can businesses pass on debit card processing fees to customers?

Not through a direct surcharge. Convenience fees can apply in specific contexts where the payment channel qualifies. Minimum purchase thresholds up to $10 are also permitted under the Durbin Amendment. For most private merchants, the realistic alternatives are cash discount programs, credit card surcharging on credit transactions, or building costs into pricing.

What is the federal law on debit card surcharges?

The Durbin Amendment, part of the Dodd-Frank Act signed in 2010, is the primary federal law governing debit card transactions. It caps interchange fees large banks can charge merchants and establishes the regulatory framework around debit card costs. Card network rules from Visa and Mastercard independently prohibit debit surcharges on top of this.

Can a restaurant charge a fee for using a debit card?

No. Restaurants follow the same card network rules as any other merchant. Surcharging a debit card transaction is prohibited regardless of business type, and a convenience fee structure won’t apply either since card payments are the everyday standard for most restaurants.

What is the difference between a surcharge and a convenience fee on a debit card?

A surcharge is a percentage-based fee for paying by card. A convenience fee is a flat fee for using a specific, non-standard payment channel. Surcharges on debit are prohibited. Convenience fees can legally apply to debit transactions when the structure and channel requirements are met.

How do I report a business for charging a debit card fee?

Keep your receipt as documentation, then file a complaint with your card network, your state attorney general, or the Consumer Financial Protection Bureau at consumerfinance.gov. Your bank may also be able to initiate a chargeback if the fee was added without prior disclosure.

What happens if a business illegally charges a debit card surcharge?

Card networks can terminate the merchant’s ability to accept card payments. State attorneys general can pursue civil penalties, and depending on the state, the business may face private lawsuits or class-action exposure. Unauthorized debit fees may also be characterized as junk fees under federal consumer protection frameworks.

- What is a surcharge?

- Can you surcharge a debit card?

- Is it illegal to charge a debit card fee?

- Surcharging Card network rules

- Why debit surcharging is generally prohibited

- Debit Card Surcharge Laws by State (2026)

- Consequences of non-compliance

- Simplifying surcharging with EBizCharge

- Frequently Asked Questions