Blog > Credit Card Surcharge Compliance: Rules, Limits, and Violation Risks

Credit Card Surcharge Compliance: Rules, Limits, and Violation Risks

Surcharging is appealing for obvious reasons. Processing fees add up fast, especially in B2B environments where transactions are high-volume and high-value. Adding a surcharge on credit card payments to offset those costs makes financial sense on the surface. But credit card surcharging comes with a compliance burden that many merchants underestimate, and the rules are detailed enough that getting them wrong can be surprisingly easy.

Getting it wrong isn’t just an inconvenience. It can result in card network fines, merchant account termination, chargebacks, and, in some states, real legal exposure. This guide covers what you need to know to run a compliant surcharge program: network rules, disclosure requirements, signage standards, and what happens when merchants cross the line.

What Is a Credit Card Surcharge?

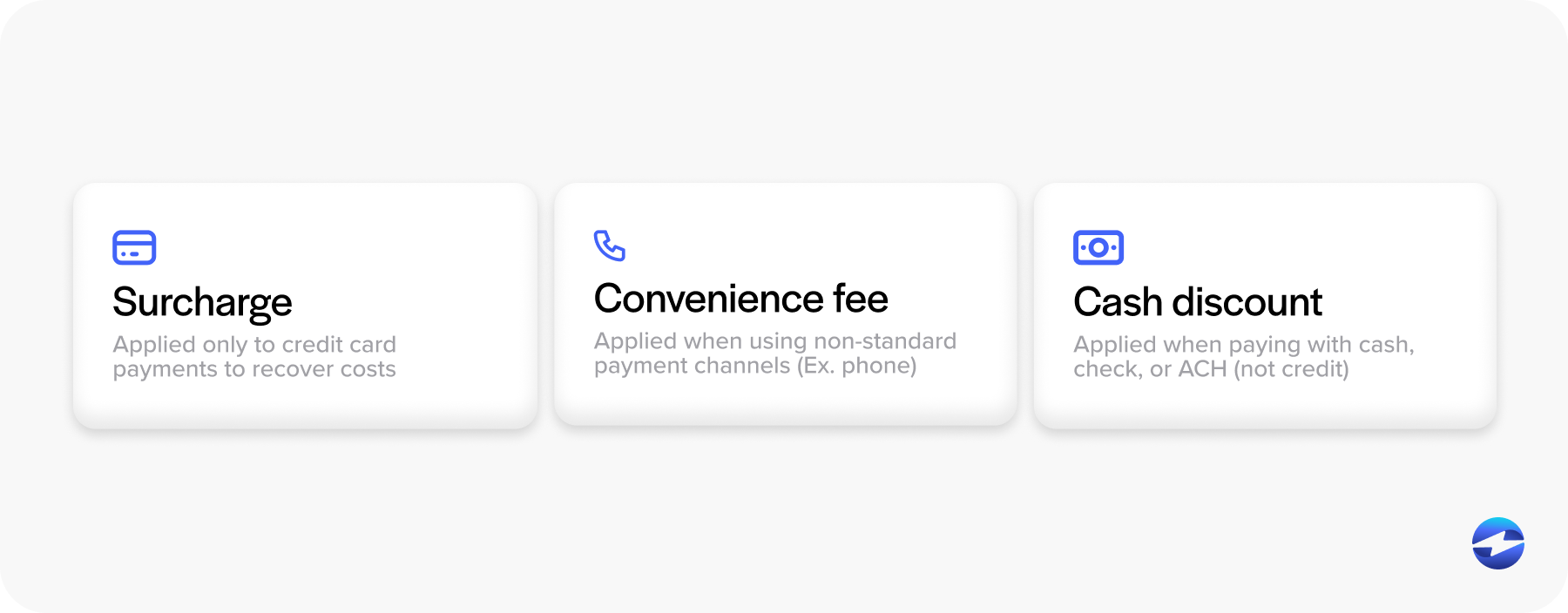

A surcharge on credit card transactions is an additional fee added at checkout when a customer pays by credit card. The purpose is to recover some or all of the merchant’s cost of accepting that card. But it’s important to separate surcharges from a few related concepts that often get confused.

A convenience fee is charged when a customer pays through a non-standard channel, like paying a utility bill by phone. Merchants will also charge a service fee to help cover operational expenses and administrative costs. A cash discount program works the opposite way: instead of adding a fee for card users, it offers a price reduction for customers who pay cash. Each of these operates under different rules, and mixing them up is a compliance problem waiting to happen.

One rule that applies universally: charging a surcharge for using credit card processing cannot extend to debit or prepaid cards. That’s a firm requirement across all major card networks, and violating it is one of the most common mistakes merchants make.

The Legal Landscape

Surcharging isn’t legal in every state. A handful of states prohibit credit card surcharging outright, or impose restrictions that go beyond what the card networks require. Before setting up any surcharge program, verify what’s permitted where you operate. This matters especially for e-commerce businesses serving customers across state lines.

The broader legal opening for surcharging came from a 2013 class-action settlement between merchants and Visa and Mastercard. Before that, network rules blocked merchants from surcharging entirely. Today, federal rules permit it, but state law still has the final say in certain jurisdictions.

Card Network Surcharge Rules

This is where most of the complexity lives. Each major card network has its own surcharge rules, and merchants have to follow all of them simultaneously.

Visa and Mastercard

Both networks require merchants to register their intent to surcharge at least 30 days in advance. You can’t decide to start surcharging tomorrow and flip a switch today. Both also require that surcharges be disclosed at the point of entry, itemized separately on receipts, and applied only to credit transactions. Current surcharge credit card processing caps sit at 3% for Visa, with Mastercard aligned similarly following recent updates.

One point that often gets overlooked: the surcharge cannot exceed your actual cost of acceptance. You can’t use surcharging as a revenue stream. The fee has to reflect what you’re actually paying to process the transaction, up to the network cap.

American Express

Amex updated its policies following the class action settlement and now allows surcharging under conditions that align with Visa and Mastercard. The central requirement is parity. If your Visa surcharge is 2%, your Amex surcharge can’t be 3%. You can’t charge Amex cardholders more than any other card brand.

The 4% Cap

You’ll see 4% referenced frequently in surcharging discussions. While individual network caps currently sit at 3%, the 4% figure appears in certain state regulations and older rule interpretations. The safest approach is to stay at or below 3% and confirm current limits with your payment processor directly, since these rules are updated periodically.

Disclosure and Signage Requirements

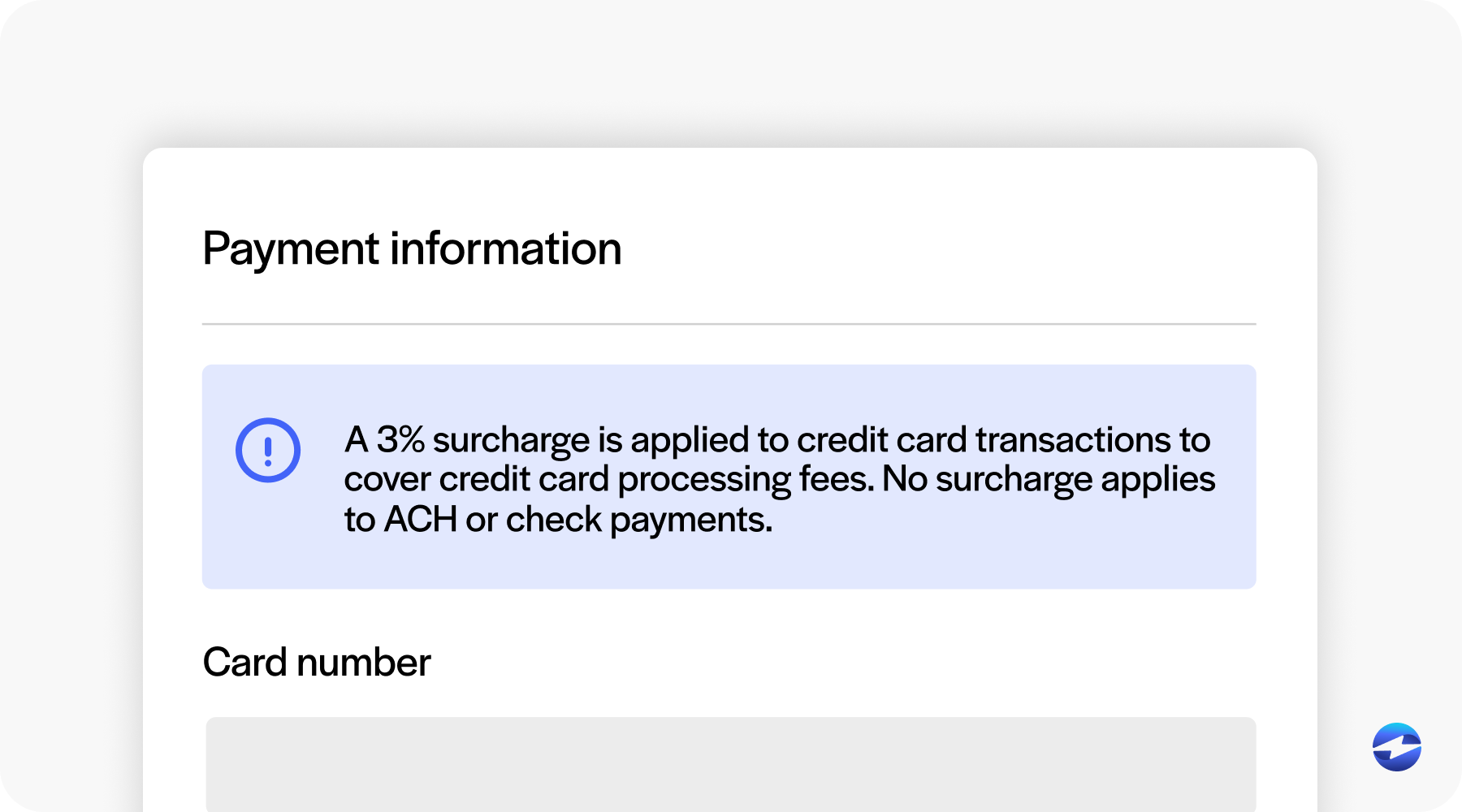

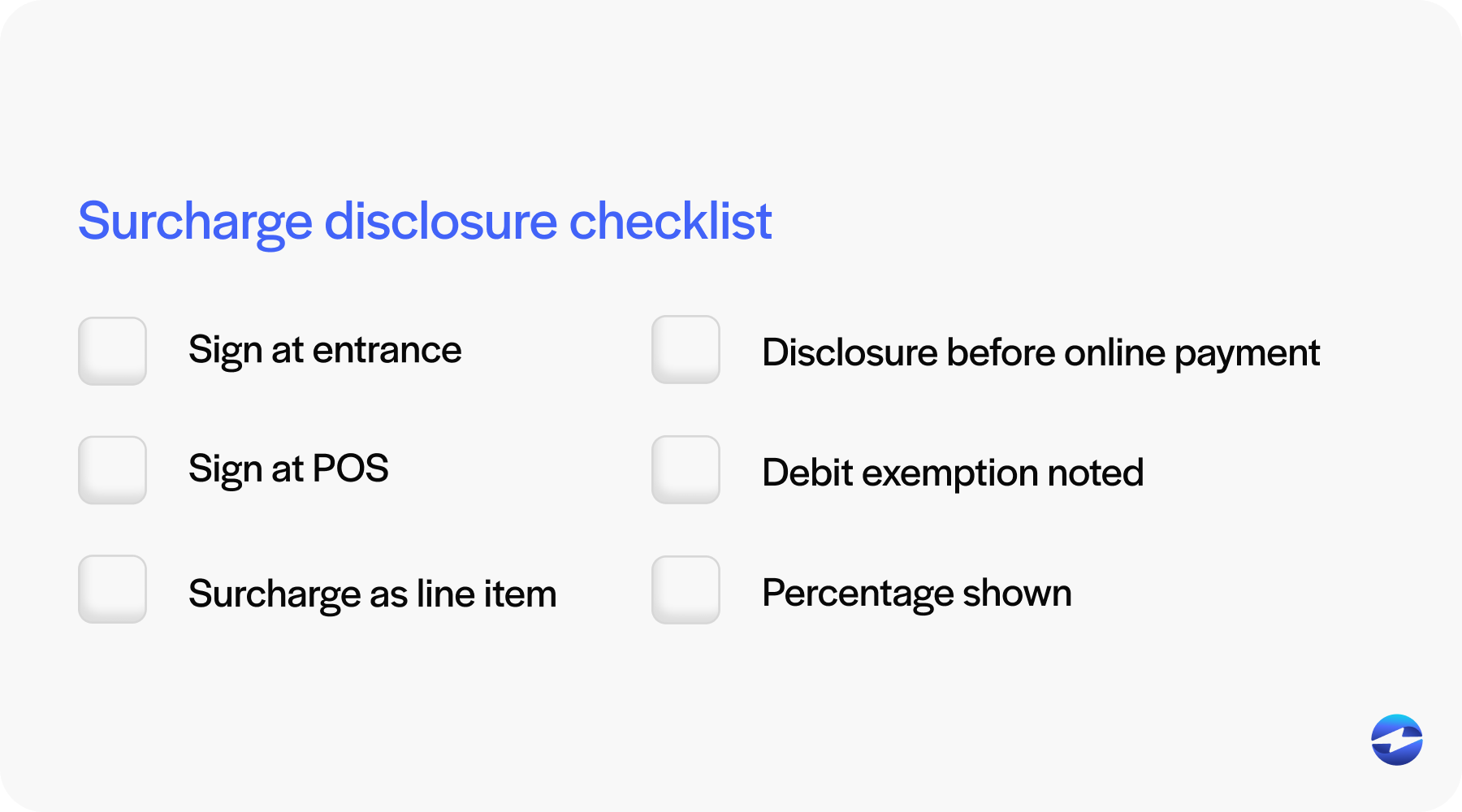

Disclosure isn’t optional, and it isn’t just good business etiquette. It’s a hard requirement under surcharge rules from every major card network. If you’re applying a surcharge for using credit card payments, customers need to know before the transaction happens, not after.

For brick-and-mortar merchants, that means signage at the store entrance and at the point-of-sale (POS) terminal. For e-commerce, the disclosure needs to appear on the checkout page before the customer submits payment. In both cases, it has to be specific: the percentage charged, confirmation that it applies only to credit cards, and a clear note that debit card transactions are exempt.

The receipt matters, too. The surcharge has to appear as its own line item. Rolling it into the total without labeling it separately is a violation.

A mistake merchants make frequently is disclosing the surcharge only on the receipt. That’s too late. The transaction is already complete, and the pre-transaction disclosure requirement has already been missed.

What Counts as a Surcharge Violation

For CFOs, controllers, AR managers, and billing teams who own payment operations, knowing exactly where the lines are is essential.

Network rule violations include failing to register before surcharging, exceeding the permitted cap, applying a surcharge on credit card transactions involving debit or prepaid cards, charging different rates across card brands, and surcharging in states where it’s prohibited.

Disclosure violations include missing pre-transaction notice, disclosures that only appear on the receipt, inadequate or missing signage, and checkout flows that don’t surface the fee before payment is submitted.

Calculation violations occur when the surcharge exceeds your actual cost of acceptance or goes above the applicable network cap.

Without a surcharge violation system in place to monitor and flag these issues automatically, merchants are relying on manual processes to stay within bounds. And manual processes have gaps, especially as transaction volume scales.

The Risks of Getting It Wrong

Card networks take surcharge violations seriously. Consequences can include per-transaction fines, suspension of your ability to accept specific card types, or full merchant account termination. Termination can land you on the Member Alert to Control High-Risk Merchants (MATCH) list, which significantly complicates opening a new account with another payment processor.

Customers also have recourse. A cardholder who believes they were improperly charged can dispute the transaction, and chargebacks accumulate quickly. In states with active enforcement around surcharge laws, civil liability is also a real possibility.

There’s also the reputational angle, which is easy to underestimate. A customer who feels blindsided by an undisclosed fee doesn’t usually give the merchant the benefit of the doubt. They dispute the charge, leave a negative review, and don’t come back.

How Compliant Payment Software Handles This Automatically

For finance and operations teams processing hundreds or thousands of transactions per month, manually tracking surcharge rules across card types, states, and network updates isn’t realistic. That’s where a purpose-built payment processing solution changes the equation.

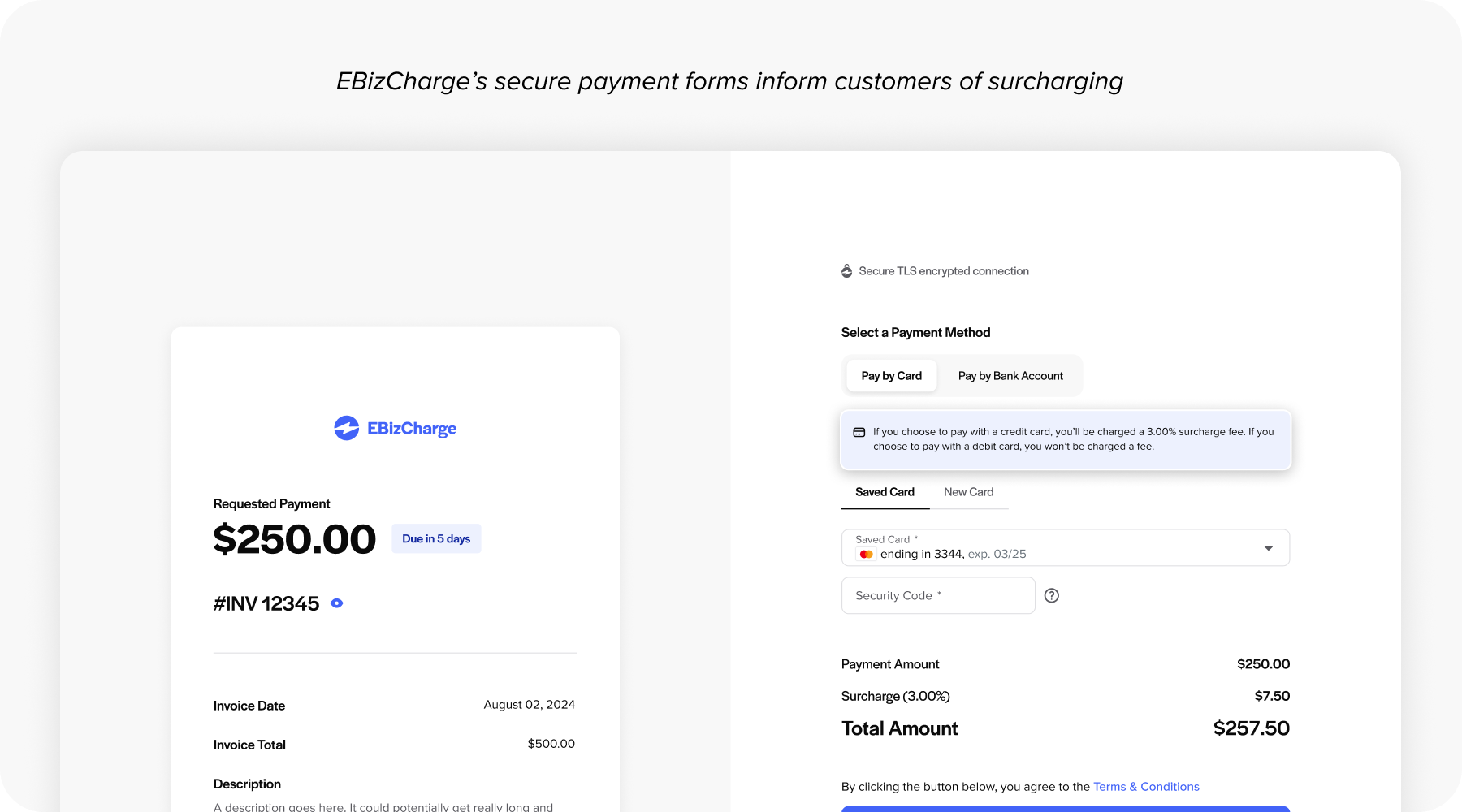

A compliant surcharge credit card processing platform handles the enforcement automatically. Card type detection runs on every transaction, so debit and prepaid cards are excluded without any manual review. Surcharge rates are tied to actual processing costs and checked against network caps in real time. State-level restrictions are built into the platform, not left to the merchant to monitor and update. A good payment processing solution also generates required disclosure language automatically and ensures the surcharge appears as a separate line item on every receipt.

Think of it as a built-in surcharge violation system: one that applies the rules consistently on every transaction, removes the manual compliance burden from your team, and keeps your program defensible if a network audit ever comes up.

How EBizCharge Keeps Merchants Surcharge-Compliant

Surcharge rules are layered, state-specific, and regularly updated. Merchants managing all of this manually are almost always carrying more risk than they realize. A single gap in disclosure, a wrong rate applied to a debit card, or a missed registration can trigger consequences that far outweigh whatever the surcharge program was meant to recover.

EBizCharge payment processing handles compliance at the transaction level. Card type detection runs automatically on every payment, so debit and prepaid cards are never incorrectly surcharged. Rates are tied to actual processing costs and hard-capped within network limits. State restrictions are built into the platform logic. Required disclosure language and itemized receipt line items are generated without any extra configuration on your end.

Because EBizCharge lives inside your ERP rather than sitting alongside it as a separate tool, the rules apply at the exact moment a transaction is initiated. There’s no gap between where billing happens and where compliance is enforced. When Visa, Mastercard, or Amex updates its policies around the surcharge for using credit card transactions, those changes are reflected in the platform. You’re not responsible for tracking them down yourself.

The result is a surcharge program that recovers your processing costs without putting your merchant account, your customer relationships, or your business at risk.