Blog > ACH and ABA Routing Numbers: What’s the Difference?

ACH and ABA Routing Numbers: What’s the Difference?

ACH and ABA routing numbers are two critical pieces of information used in banking and financial transactions.

Therefore, it’s crucial to understand the differences between these two routing numbers to help you decide which is the best to use for your business.

What is a routing number?

Routing numbers, or ABA routing numbers, are nine-digit codes that identify financial institutions within the U.S. that conduct transactions. This number is essential for directing funds to the correct bank during a transfer.

The American Bankers Association (ABA) developed ABA routing numbers in 1910 to streamline the process of sorting, bundling, and shipping paper checks to the check writer’s bank to debit to the check writer’s account.

What is an ABA routing number?

Bank ABA routing numbers are unique nine-digit numbers that identify financial institutions participating in the ABA system. ABA stands for American Bankers Association which is a trade organization that represents banks in the United States.

ABA routing numbers work by routing funds from one bank account to another through the ABA network. This system is used for traditional check processing, wire transfers, and other transactions. Unlike ACH routing numbers, ABA routing numbers are used for both electronic and paper transactions.

Similar to ACH routing numbers, the purpose of ABA routing numbers is to ensure funds are accurately and efficiently transferred between financial institutions. ABA routing numbers are used for various transactions such as check processing, wire transfers, etc.

Is an ABA number the same as a routing number?

Yes, an ABA number and a routing number are essentially the same thing. The term “ABA number” comes from the American Bankers Association, which originally developed this 9-digit identification system for banks. Today, most people call it a “routing number,” but both terms refer to the same code that identifies your specific financial institution for processing transactions like checks, direct deposits, and electronic transfers.

However, there’s an important distinction about ACH routing numbers. While people often use “ACH number” and “routing number” interchangeably, an ACH routing number is technically a specific routing number designated exclusively for electronic ACH transactions. Many banks use the same 9-digit number for all transaction types, but some larger financial institutions assign different routing numbers for different purposes. One is for ACH transfers, another is for wire transfers, and sometimes a separate one is for check processing. This is why it’s always best to confirm which routing number to use for specific transaction types with your bank.

What is an ACH routing number?

ACH stands for Automated Clearing House which is a system that facilitates electronic payments and direct deposits between financial institutions. Therefore, ACH routing numbers are unique nine-digit numbers that identify financial institutions participating in the ACH network.

ACH numbers were developed in the 1970s when there was a significantly large amount of checks which threatened to slow down the banking system. This started an even larger industry-wide shift toward electronic banking.

ACH routing numbers work by routing funds from one bank account to another through the ACH network. This system is used to process direct deposits, bill payments, and other types of electronic payments. ACH routing numbers differ from ABA routing numbers because they’re used specifically for electronic transactions. The first two digits of ACH routing numbers typically range from 61 to 72, whereas the first two digits of ABA routing numbers range between 00 and 12.

The purpose of ACH routing numbers is to ensure funds are accurately and efficiently transferred between financial institutions. ACH routing numbers are used for various transactions such as direct deposit of payroll, government benefits, and tax refunds.

ACH routing numbers can be found on personal checks, bank statements, or by contacting your financial institution. Some financial institutions provide this information on their websites.

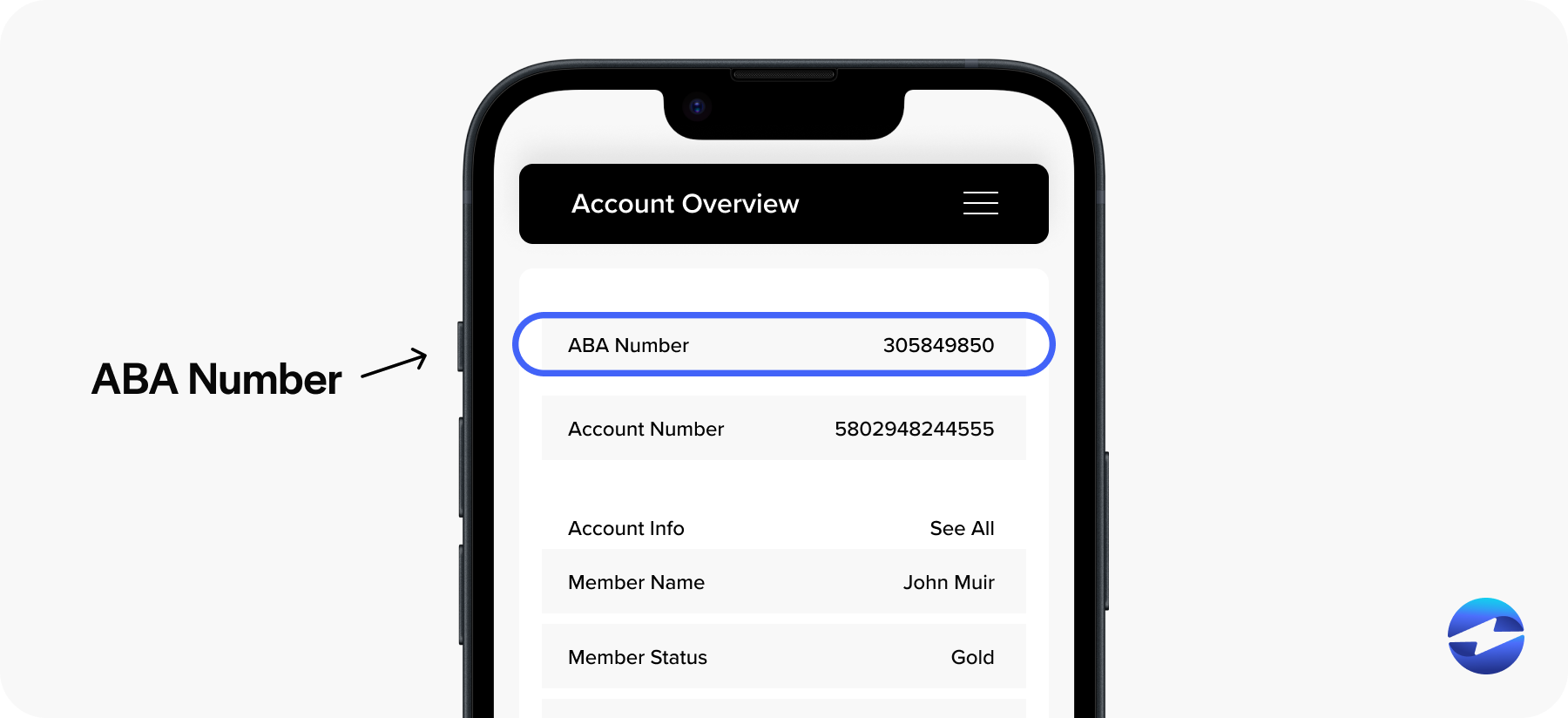

Where to find your ABA routing number

Knowing where to locate your ABA routing number is essential when setting up direct deposits, initiating wire transfers, or making electronic payments. Here are the three most reliable places to find it:

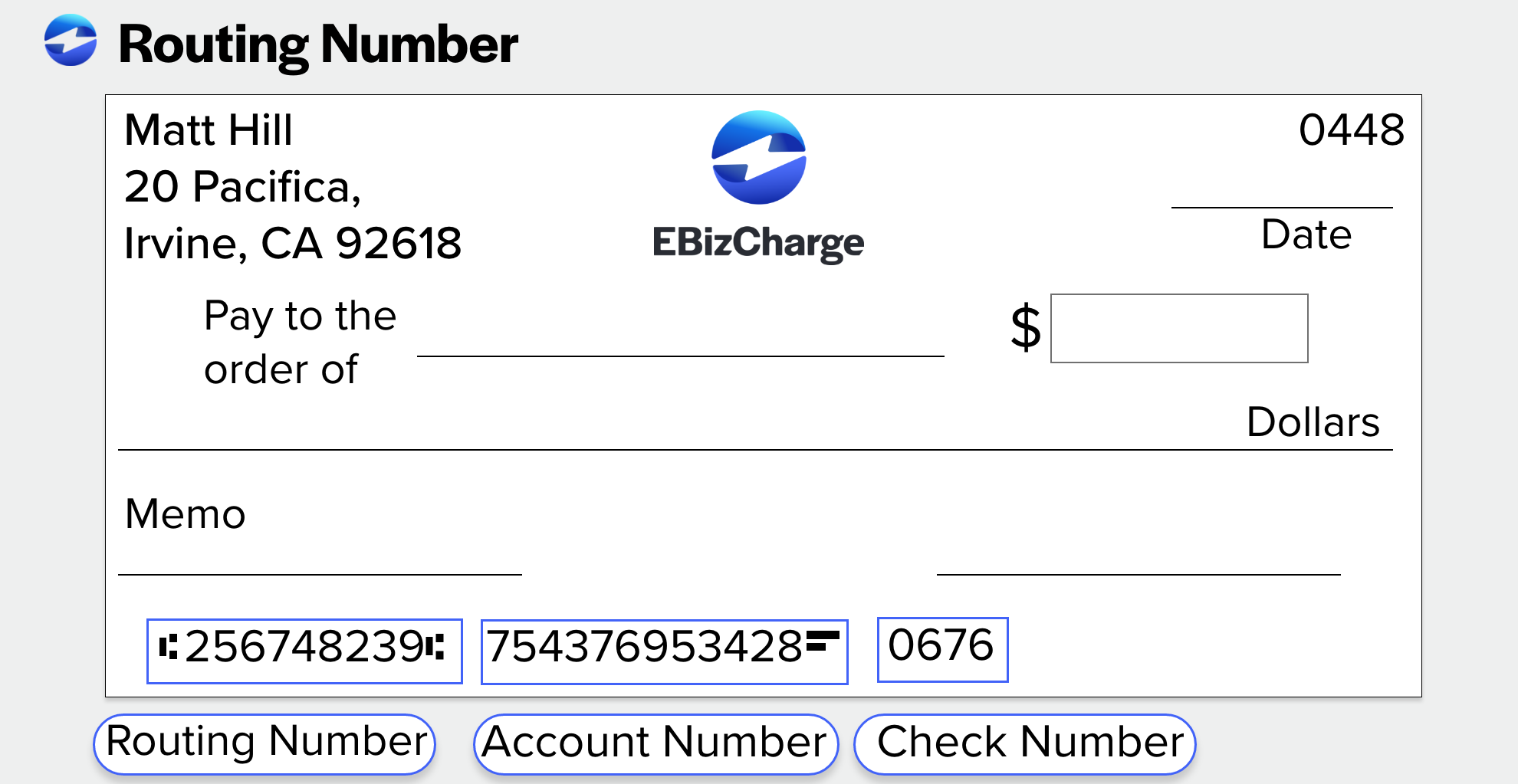

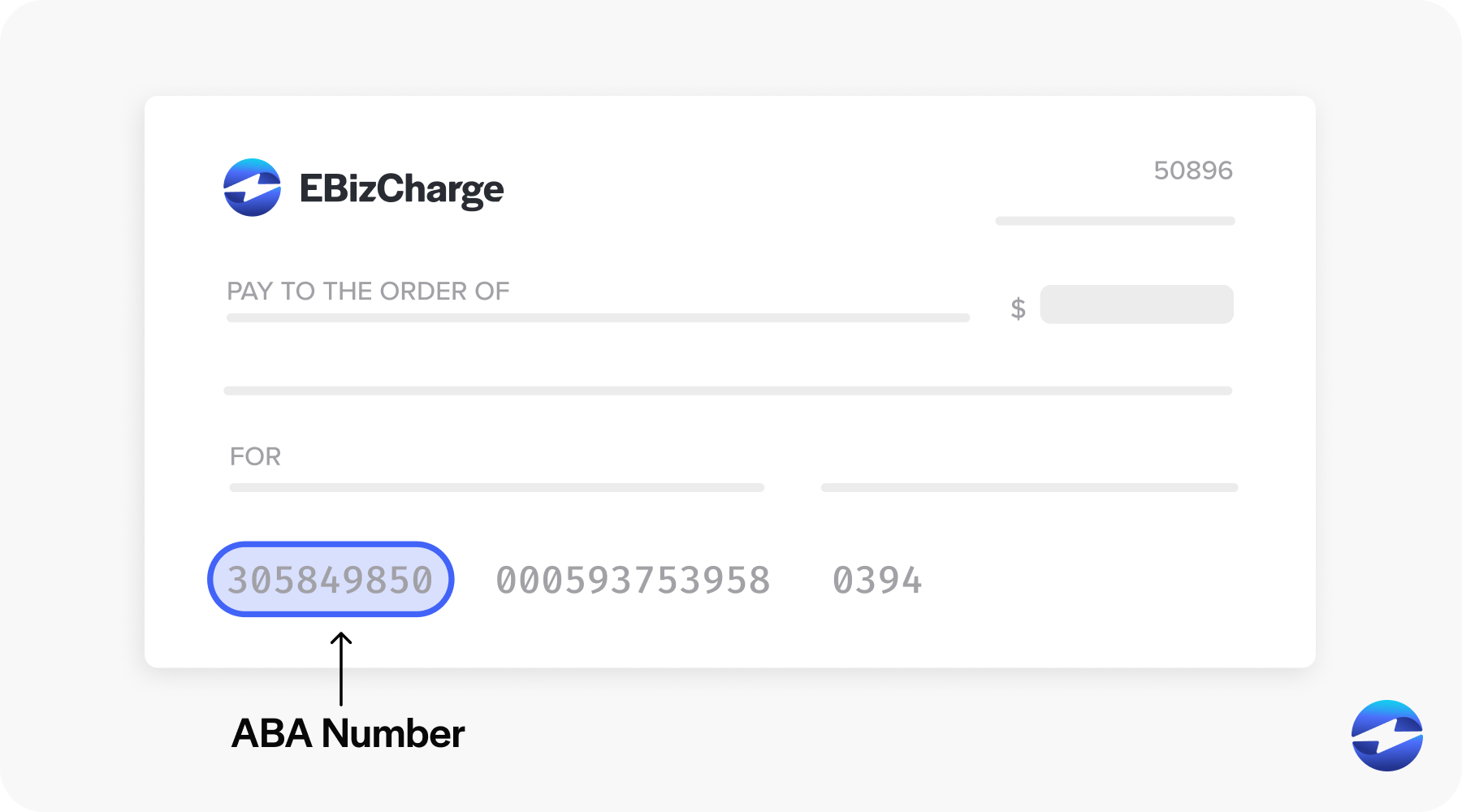

- On a check. The ABA routing number is printed at the bottom left corner of a personal check, encoded in magnetic ink using a system called magnetic ink character recognition (MICR). It is the first nine-digit sequence in that lower left area, preceded by a symbol that resembles a colon, followed by your account number and check number.

- On a bank statement. Financial institutions typically list the ABA routing number on monthly statements, usually on the first pages summarizing account information.

- Through online banking. Most financial institutions make routing numbers available through their online banking portals under Account Details or Account Information, accessible through both the mobile app and web browser.

Since entering the wrong ABA number can result in failed or misrouted transactions, always verify the number before initiating any payment.

How to verify a routing number

Knowing where to find your routing number is only half the equation. Before initiating any payment, verifying the number is correct can prevent failed transactions and misrouted funds. Four reliable ways to verify:

- Check your bank’s website or app. Most banks list their routing numbers on their official website and mobile banking apps. Make sure you select the correct number for your specific transaction type, as some larger banks assign different routing numbers for ACH transfers, wire transfers, and check processing.

- Contact your bank directly. Calling your bank’s customer service line is the most reliable way to confirm the routing number for your account and transaction type. This is especially important during bank mergers or operational updates when routing numbers can change.

- Use an online routing number verification tool. Several websites allow you to look up routing numbers to verify their validity and confirm the corresponding financial institution. The ABA maintains an official routing number lookup tool at aba.com.

- Test with a small transaction. Before proceeding with a large or important transfer, testing the routing number with a small transaction first is a simple precaution that can confirm the number is correct and avoid costly delays.

If you realize you have entered the wrong routing number, contact your bank or the institution involved immediately to correct the error before the transaction is processed.

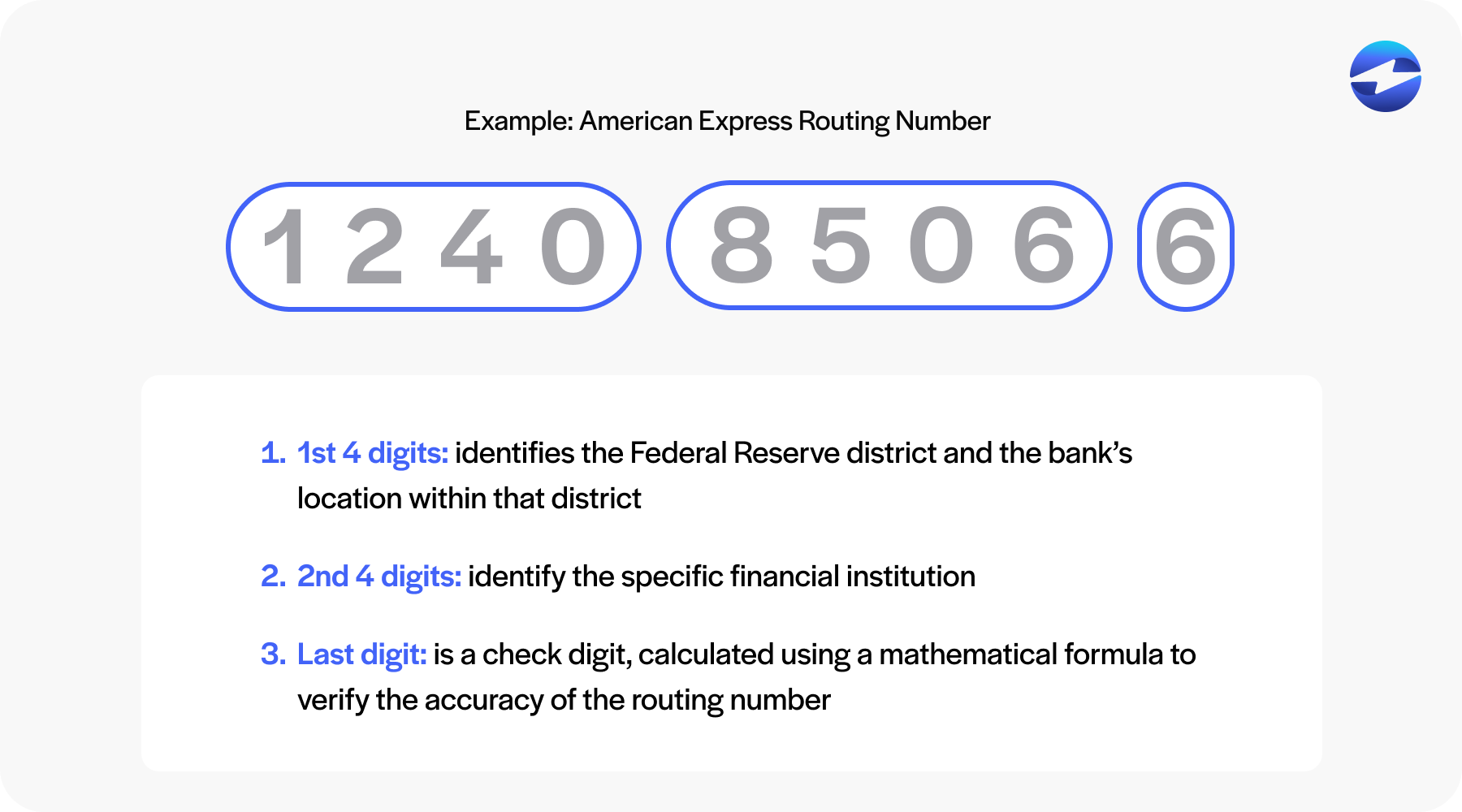

How routing numbers work

Routing numbers are not random nine-digit sequences. Each section of the number carries specific information that tells the banking system exactly where to send funds:

Digits 1 through 4 represent the Federal Reserve routing symbol, which identifies the Federal Reserve district where the bank is located and the specific processing center assigned to it. This is why ABA numbers starting with 00-12 indicate U.S. banks while ACH numbers starting with 61-72 indicate electronic-only transactions.

Digits 5 through 8 identify the specific financial institution within that Federal Reserve district, ensuring the transaction reaches the correct bank rather than another institution in the same region.

Digit 9 is a check digit calculated using a mathematical formula based on the first eight digits. If the result does not match, the system flags the transaction for manual review. This built-in error detection prevents simple typing mistakes from sending funds to the wrong institution.

Understanding this structure explains why entering even one wrong digit can cause a failed or misrouted transaction.

Routing numbers in practice

Understanding what a routing number is becomes more useful when you see how it functions across different transaction types. Here is how routing numbers are used in everyday banking:

- Check processing. When you write or deposit a check, the routing number directs the check through the banking system to ensure funds are drawn from the correct institution and account. It acts as the bank’s address in the paper check clearing process.

- Direct deposits. For payroll, government benefits, and tax refunds, routing numbers allow employers and agencies to send funds directly to the recipient’s bank account. This is one of the most common reasons individuals are asked for their routing number.

- Bill payments. When setting up automatic bill payments, providing your routing number alongside your account number allows your bank to send payments electronically to the biller’s financial institution on the scheduled date.

- ACH transactions. Utility payments, account-to-account transfers, and other automated transactions use routing numbers to identify both the origin and destination of funds through the ACH network.

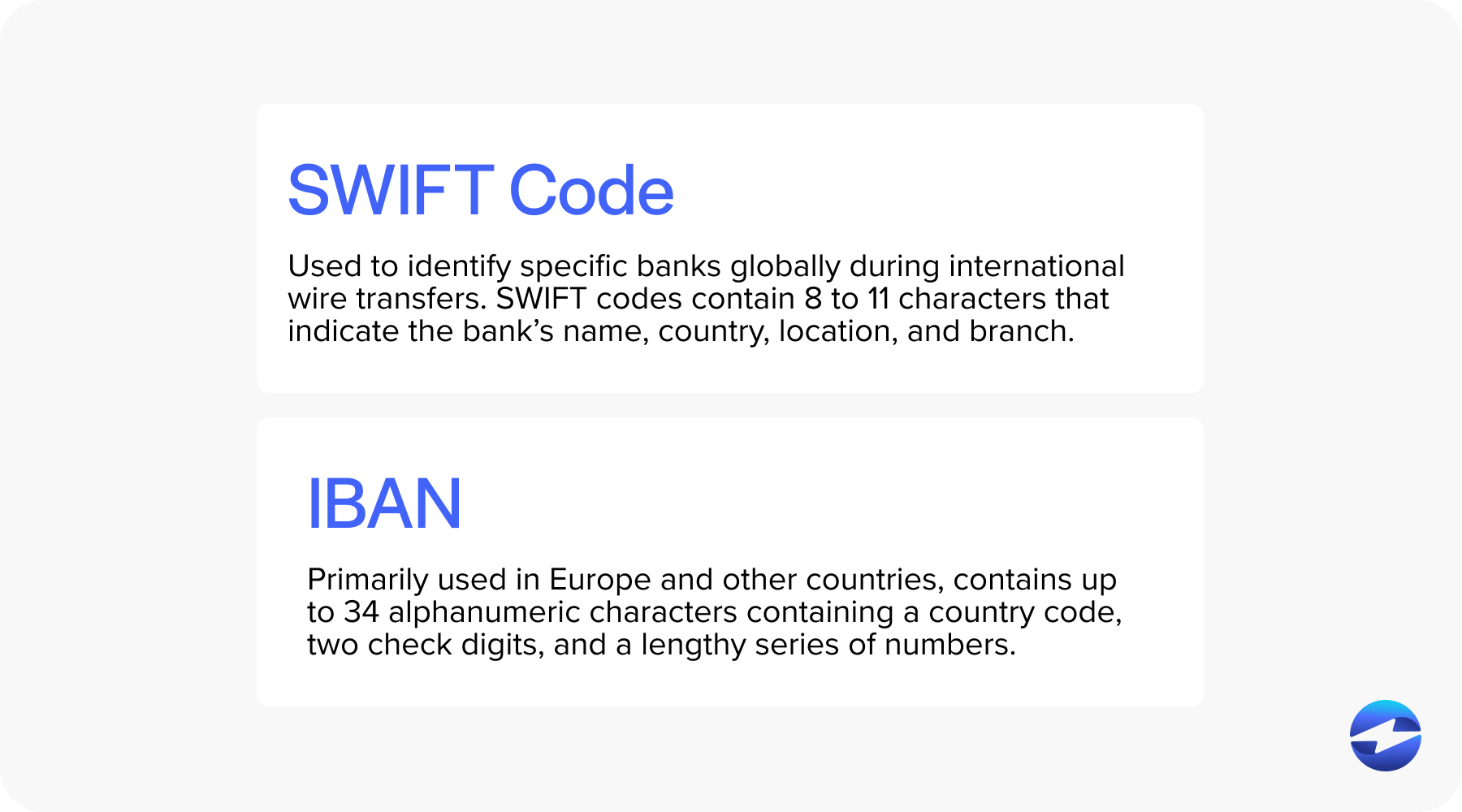

- Wire transfers. Domestic wire transfers use routing numbers to identify the receiving bank. For international wire transfers, SWIFT codes or IBANs are required instead of or in addition to a routing number, depending on the destination country.

Differences between ACH and ABA routing numbers

While there are several similarities between ACH and ABA routing numbers, there are also key differences when comparing the two.

Quick Reference: When to Use Each Number

| Use ACH Routing Numbers For: | Use ABA Routing Numbers For: |

|---|---|

| Direct deposit setup | Writing or depositing checks |

| Automatic bill payments | Wire transfers (domestic and international) |

| Electronic fund transfers | Setting up new bank accounts |

| Online banking transfers | General banking transactions |

| Payroll processing | When unsure which type is needed |

The main differences between ACH and ABA routing numbers are:

-

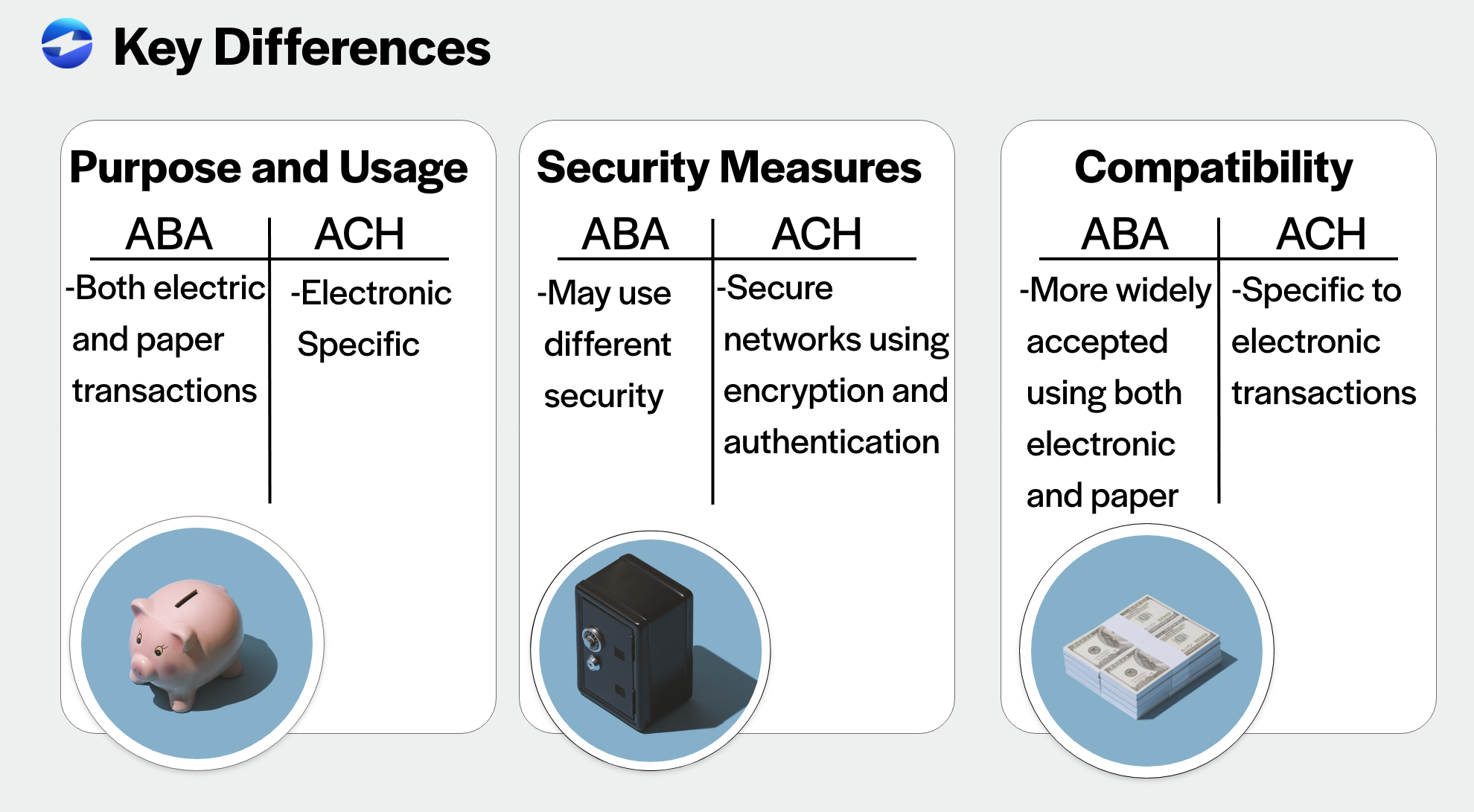

Purpose and usage:

ACH routing numbers are used specifically for electronic transactions, whereas ABA routing numbers are used for both electronic and paper transactions.

-

Security measures:

ACH transactions are typically processed through secure networks and subject to security measures such as encryption and authentication, while ABA transactions may be subject to different security measures depending on the financial institution and type of transaction.

-

Compatibility with different payment systems:

ACH routing numbers are used specifically for electronic transactions, so they may not be compatible with all payment systems. On the other hand, ABA routing numbers are used for both electronic and paper transactions and are more widely accepted.

ACH number vs routing number

While both ACH and ABA routing numbers are 9-digit codes that identify financial institutions, they serve different purposes in banking transactions.

ACH routing numbers are designed specifically for electronic transactions through the Automated Clearing House network, such as direct deposits and automatic bill payments, and typically begin with digits 61-72.

ABA routing numbers, developed by the American Bankers Association, handle a broader range of transactions including both electronic and paper-based transfers like checks and wire transfers, with numbers typically starting with digits 00-12. The key distinction is that ACH numbers work exclusively within electronic payment systems and often include enhanced security measures like encryption, while ABA numbers are more universally accepted across different payment methods but may have varying security protocols depending on the transaction type. Many banks use the same 9-digit number for both purposes, but larger institutions often assign separate routing numbers for different transaction types to optimize processing efficiency.

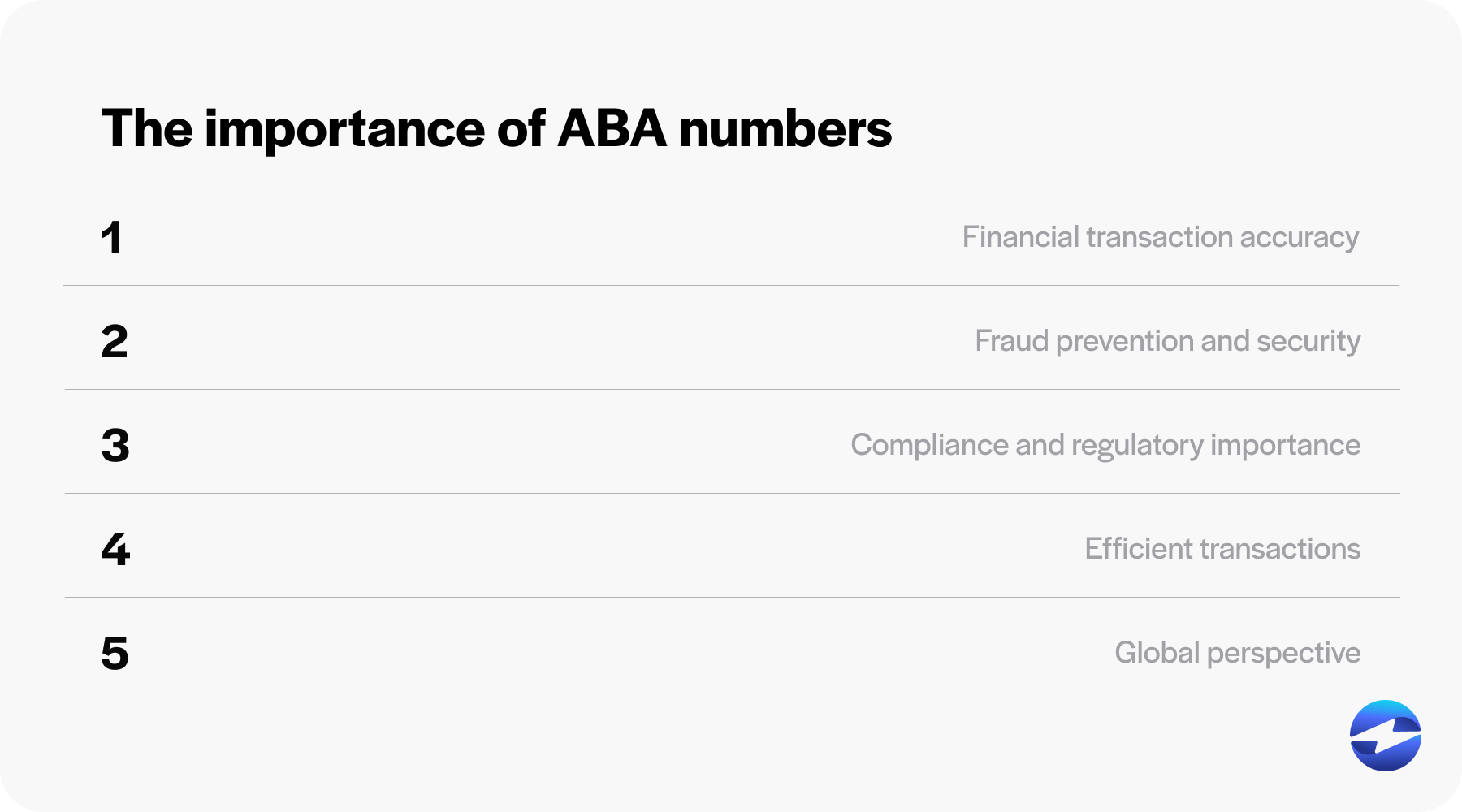

Why ABA routing numbers matter

ABA routing numbers do more than identify a bank. They serve several critical functions that keep the U.S. financial system running accurately and securely:

Financial transaction accuracy. ABA routing numbers act as an essential checkpoint in verifying where funds should be directed. When combined with an account number, the routing number pinpoints the exact institution and account, eliminating the risk of misrouting funds to a bank with a similar name.

Fraud prevention and security. Because each financial institution is assigned a unique ABA number, ACH and wire transfers can be more easily traced to their origin. This makes it significantly harder for fraudulent transactions to go undetected.

Compliance and regulatory requirements. The Federal Reserve uses ABA numbers to process Fedwire funds transfers, and banks are required to use them to reconcile accounts and maintain compliance with financial regulations. The standardized format established by the American Bankers Association promotes transparency and consistency for regulatory reporting and auditing.

Efficient transaction processing. ABA numbers allow financial networks to quickly identify the appropriate institution, enabling both traditional and electronic transactions to be processed with minimal errors and reduced delays.

International context. While ABA numbers are specific to the U.S., equivalent systems exist globally. SWIFT codes facilitate international wire transfers and messages between banks, while International Bank Account Numbers (IBANs) provide a structured account format across countries. Understanding how ABA numbers fit into this global picture helps businesses managing cross-border payments navigate the right identifier for each transaction type.

What are other types of routing numbers?

ABA and ACH are not the only types of routing numbers you may encounter. There are different types of routing numbers, each serving a specific purpose. Here are the main types of routing numbers, including the previously discussed ABA and ACH numbers:

ABA Routing Numbers:

These are 9-digit codes assigned by the American Bankers Association (ABA) to identify banks in the United States. They are used for various transactions, including paper or check transfers, direct deposits, and wire transfers.

ACH Routing Numbers:

These are routing numbers used specifically for electronic transfers through the Automated Clearing House network. They are used for electronic transactions such as direct deposits, electronic bill payments, and other automated transfers.

Wire Transfer Routing Numbers:

Financial institutions may have separate routing numbers specifically designated for wire transfers, which are used for sending and receiving funds electronically between banks domestically or internationally. These routing numbers are distinct from ABA routing numbers and are typically used for high-value or time-sensitive transactions.

International Routing Numbers:

For international transactions, banks use different codes, such as SWIFT (Society for Worldwide Interbank Financial Telecommunication) codes or IBANs (International Bank Account Numbers) instead of traditional routing numbers. These codes help identify specific banks and branches internationally to facilitate cross-border transactions.

Fedwire Routing Numbers:

These are used specifically for processing large-value, time-critical payments and transfers between financial institutions within the country. Fedwire is a real-time gross settlement system operated by the Federal Reserve Banks in the United States.

These are the main types of routing numbers that are essential for the smooth movement of funds between financial institutions, both domestically and internationally.

Utilizing the benefits of ACH and ABA routing numbers

ACH and ABA routing numbers serve distinct purposes in the world of banking and finance, whether it be electronic transfers such as direct deposits and bill payments or traditional paper transactions such as check processing.

Understanding how these routing numbers work helps businesses process payments more efficiently. Having the right ACH processing solution in place means your team doesn’t have to worry about manually entering routing numbers or chasing down failed transactions. Solutions like EBizCharge simplify ACH transactions by automating the entire process. With NetSuite payment processing and Sage Intacct payment processing integration, every ACH payment posts directly to your accounting software so your records stay accurate without manual entry.

Best practices for using routing numbers

Following a few simple best practices when handling routing numbers keeps transactions accurate and your financial data secure:

Always obtain routing numbers from official sources. Verify routing numbers directly from your bank’s website, a personal check, or by calling your bank. Avoid relying on third-party sources that may be outdated.

Monitor for changes during bank mergers. Banks that merge or undergo operational updates sometimes change their routing numbers. Banks typically notify customers, but proactively checking your bank’s communications can prevent unexpected transaction failures.

Test before large transfers. Before initiating a significant wire transfer or setting up recurring payments, run a small test transaction first to confirm the routing number is correct and the funds reach the right institution.

Store routing information securely. If your business stores routing numbers for recurring transactions, use encrypted storage solutions or secure payment platforms that handle routing data in compliance with financial data security standards. Solutions like EBizCharge store and route payment information automatically within your existing accounting or ERP system, so routing numbers and account details are handled securely without manual management.

Frequently Asked Questions

Is an ABA number the same as a routing number?

Yes, an ABA number and a routing number are essentially the same thing. The term “ABA number” comes from the American Bankers Association, which originally developed the nine-digit identification system for banks in the United States. Today most people simply call it a routing number, but both terms refer to the same code used to identify your financial institution for transactions like checks, direct deposits, ACH transfers, and wire transfers. The distinction worth knowing is that some larger banks assign different routing numbers for different transaction types, so it is always worth confirming which number applies to your specific transaction.

What is the difference between a routing number and an account number?

A routing number identifies the financial institution where your account is held — it tells the banking system which bank to send funds to or receive them from. An account number identifies your specific account within that institution. Both are required to complete transactions like direct deposits, wire transfers, and ACH payments. Think of the routing number as the bank’s address and the account number as your specific mailbox within it.

Is my ABA number the same for all transaction types?

Not always. Some banks use different routing numbers for different types of transactions. You may have one ABA number for paper checks and a separate one for wire transfers or ACH transactions. Always verify the appropriate routing number for your specific transaction type, especially when setting up direct deposits or initiating wire transfers.

What happens if I enter the wrong ABA number?

Entering the wrong ABA routing number can result in funds being sent to the wrong bank or returned to you. In some cases this delays the transaction and requires you to resubmit the payment. Always double-check the routing number before initiating any transaction, particularly for important payments like payroll or large wire transfers. If you realize you have entered the wrong number, contact your bank immediately to correct the error before the transaction processes.

Can ABA routing numbers change?

Although rare, ABA routing numbers can change. This typically happens during bank mergers or when a financial institution changes its operational structure. If your bank’s routing number changes, the bank will notify you and you may need to update any automatic payments or direct deposit instructions to reflect the new number. Proactively monitoring your bank’s communications is the best way to stay ahead of any changes.

Are ACH routing numbers the same as wire transfer routing numbers?

Not always. Some banks maintain separate routing numbers for ACH electronic payments and wire transfers. ACH routing numbers are used for transactions like direct deposits and bill payments processed through the Automated Clearing House network. Wire transfer routing numbers are used for high-value or time-sensitive transfers between banks. Always confirm which routing number your bank uses for each transaction type before initiating a payment.

Do credit cards have routing numbers?

No, credit cards do not have routing numbers. Routing numbers are specific to bank accounts like checking and savings accounts and are used for transactions like direct deposits and bill payments. Credit cards use a different system based on the card number and issuer information to process transactions.

- What is a routing number?

- What is an ABA routing number?

- What is an ACH routing number?

- Where to find your ABA routing number

- How to verify a routing number

- How routing numbers work

- Differences between ACH and ABA routing numbers

- ACH number vs routing number

- Why ABA routing numbers matter

- What are other types of routing numbers?

- Utilizing the benefits of ACH and ABA routing numbers

- Frequently Asked Questions