Blog > Level 3 Processing Requirements: What Data Do You Need?

Level 3 Processing Requirements: What Data Do You Need?

If you’re a B2B company accepting commercial credit cards, you’ve probably noticed that processing fees on certain transactions can run higher than expected. Maybe you asked your payment processor about it and got a vague answer about card types and interchange categories. The real explanation, in most cases, is simpler than it sounds: your transactions aren’t qualifying for the lower interchange rates they’re eligible for because the right data isn’t being submitted.

That’s what level 3 processing requirements are all about. There’s a specific set of data fields that card networks require before they’ll grant a reduced interchange rate on commercial and government purchasing card transactions. Most B2B companies already have that data sitting in their systems. The problem is that it’s not making it to the card network. This article walks through what’s required, why it matters, and where most businesses fall short.

A Quick Refresher on How the Tiers Work

Card networks like Visa and Mastercard don’t charge a flat interchange rate on every transaction. They use a tiered system where the rate you pay depends largely on how much data you submit.

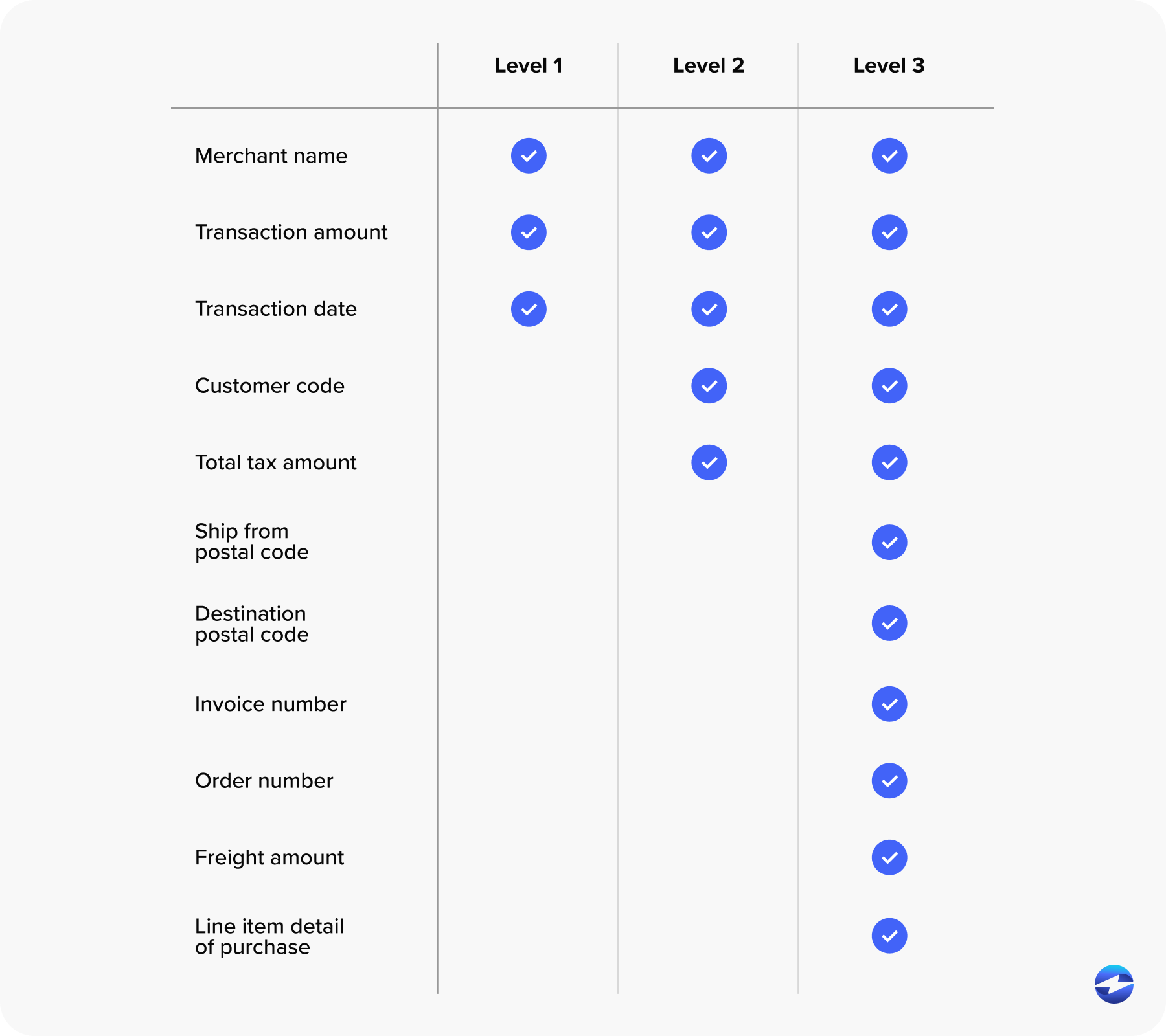

Level 1 is the baseline: transaction amount, merchant name, date. Level 2 adds tax amount, customer code, and merchant postal code. Level 3 goes all the way down to the line-item level, requiring a full breakdown of what was purchased, how many units were purchased, at what price, and which taxes and shipping costs applied.

Understanding level 2 and level 3 credit card processing as a progression helps here. Level 2 is a meaningful step up from level 1 and qualifies for modest rate reductions. Level 3 is the most detailed tier and unlocks the most significant savings, but it also comes with the most specific requirements. It’s designed for B2B and B2G transactions where corporate purchasing cards, large-market commercial cards, and government procurement cards are involved. Consumer cards and standard small business rewards cards don’t qualify for level 3 rates, regardless of what data you submit, so the first thing worth knowing is whether your card mix actually includes cards that can benefit.

Why Card Networks Require This Level of Detail

It’s worth understanding the logic before getting into the specifics.

Card networks require detailed level 3 transaction data because more information means less risk. A transaction that includes a PO number, a ship-to address, itemized product codes, and line-level tax amounts is much easier to verify than a transaction that just says “$4,200 charged at Acme Supply Co.” For corporate buyers managing procurement budgets or government agencies tracking expenditures, that line-item detail also supports their internal reporting and compliance processes.

The card network is essentially trading a lower interchange rate for better visibility into what the transaction actually represents. That’s the deal. And for B2B companies that are already generating that data as part of normal invoicing, it’s a trade worth making.

The Full Level 3 Data Requirements Breakdown

This is the part most people are looking for, so here it is clearly laid out. Level 3 credit card processing requirements apply at two levels: the overall order and each individual line item.

At the order level, you need to submit the customer reference number or PO number, the total tax amount, the ship-to ZIP or destination postal code, the freight and shipping amount, any applicable duty amount for international orders, and any order-level discount.

At the line-item level, every product or SKU in the transaction needs its own set of fields: item product code or commodity code, item description, quantity, unit of measure, unit price, line item total, any line-level discount, and the tax amount applied to that specific line.

All of this level 3 data must be submitted at the time of authorization and settlement. You can’t go back and append it after the transaction closes. If the data isn’t there when the transaction processes, the card network defaults to a lower tier, and you pay the higher rate.

The good news is that your ERP or invoicing platform almost certainly captures most of this already. Product codes, quantities, unit prices, tax breakdowns, and shipping charges are standard components of a B2B invoice. The question isn’t usually whether the data exists. It’s whether it’s getting to the card network.

Where Most Businesses Get This Wrong

There are a few common failure points worth naming directly.

The first is that the payment processor may simply not support Level 3. Many standard merchant accounts only process at level 1 by default. Businesses assume their eligible transactions are qualifying at the best available rate when they’re not. No one flags it. The higher fees just accumulate quietly.

The second issue is that the processor technically supports level 3 data credit card submission, but requires manual entry. Someone on the AR team would have to enter line-item fields for every transaction individually. At any real volume, that doesn’t happen consistently, which means qualification is sporadic at best.

The third failure point is on the data side. If the invoicing system or ERP isn’t recording commodity codes, unit of measure, or line-level tax in a way the processor can read, there’s nothing to submit even if the processor is fully capable. Meeting level 3 credit card processing requirements is a two-part problem: the data must exist, and the processor must use it.

The fourth issue is the one that causes the most damage over time: silent downgrades. When level 3 transaction data is incomplete or missing, the transaction downgrades to level 1 or level 2 rates automatically. There’s no notification. It doesn’t appear on the statement as a missed opportunity. It just shows up as a higher processing cost that most businesses attribute to card type variation and move on.

Which Card Types Actually Qualify?

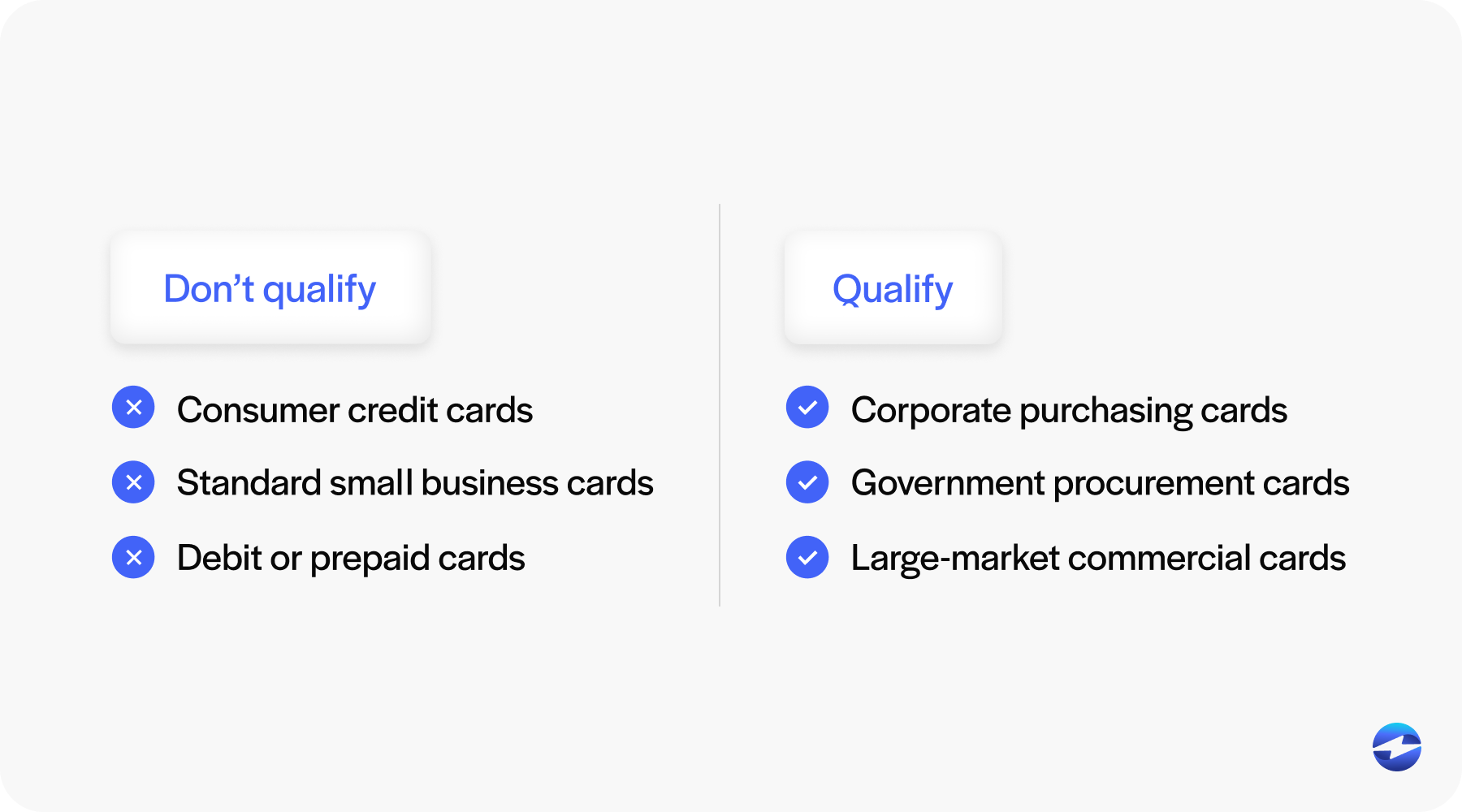

Level 3 processing only applies to specific card categories. Visa and Mastercard corporate purchasing cards, government procurement cards, including GSA SmartPay, and large-market commercial cards issued under specific commercial programs are the ones that qualify.

Standard consumer credit cards, debit cards, and typical small business cards do not qualify for level 3 processing rates, regardless of the data you submit. This is important because it means the savings opportunity varies depending on your customer base. A B2B company selling to large enterprises and government agencies will have a much higher share of qualifying card volume than one selling primarily to small businesses.

Ask your payment processor to break down your card mix by type if you haven’t already. If a meaningful share of your volume is corporate or government purchasing cards, the difference between level 2 and level 3 credit card processing rates is a real dollar amount worth calculating.

A Practical Checklist for Qualifying

Before making any system changes, it helps to work through a few quick assessments.

Start with your card mix. Confirm what percentage of your transaction volume runs on qualifying commercial or government cards. If it’s negligible, level 3 may not move the needle much. If it’s significant, keep going.

Next, audit your current data capture. Does your ERP or invoicing platform record product codes, unit of measure, line-level tax, freight, and PO numbers? Most do. If not, that’s a configuration issue worth addressing before anything else.

Then talk to your payment processor directly. Ask whether level 3 transaction data is being submitted automatically on eligible transactions. Not manually, not occasionally. Automatically, every time. If the answer is unclear or qualified, that tells you something.

If your system has the data but your processor isn’t submitting it, the solution is finding a payment processing solution that integrates with your existing platform and passes that data through natively at settlement.

Finally, once you’ve made changes, verify qualification on your first few statements. Confirm that transactions are hitting level 3 processing rates and are not being downgraded. Downgrade patterns are easy to miss unless you’re specifically looking for them.

Level 3 Requirements in an ERP Environment

ERP-integrated payment solutions are the most practical path to consistent level 3 qualification, and the reason is straightforward: all of the required data fields already exist in a well-configured ERP. Product codes, quantities, unit prices, line-level tax, shipping amounts — it’s all there on the invoice. The payment processing solution just needs to be able to read it and submit it at the time the card is charged.

Compare that to a standalone payment gateway with no ERP connection. For every transaction, someone would need to manually re-enter the line-item data from the invoice into the payment system. At low volume, that’s inconvenient. At high volume, it’s not realistic.

When the payment processor lives inside the ERP, the data handoff is automatic. The AR team processes the payment the same way they always have. The level 3 data goes with it. No extra steps, no manual entry, no risk of a transaction downgrading because someone forgot a commodity code.

The Easy Path to Level 3 Compliance

Level 3 processing requirements aren’t technically complicated. The data is specific, but if you’re running a B2B operation on an ERP platform, you almost certainly already have it. The gap for most companies isn’t the data itself. It’s the connection between where the data lives and where it needs to go.

The EBizCharge payment processing solution closes that gap. Because it integrates natively into 100+ ERP, CRM, and accounting platforms, it sits directly inside the system where invoices are created, and the line-item data already exists. Every eligible transaction automatically carries the required level 3 data credit card fields through to settlement — product codes, quantities, unit prices, tax, shipping, PO numbers — without any additional work from the AR team.

For B2B companies that have been unknowingly downgrading on commercial card transactions, an ERP-native payment processing solution like EBizCharge is often the fastest path to consistent level 3 qualification. And the savings tend to show up quickly. The data was already there. It just needed a better way to get where it was going.