If you run a B2B company and you’re accepting commercial credit cards, there’s a good chance you’re overpaying on processing fees. Not because you negotiated a bad rate, and not because your processor is doing anything wrong. It’s because most businesses simply aren’t submitting the right data with their transactions.

That’s what level 3 processing is about. It’s a data tier that unlocks lower interchange rates on commercial and government purchasing cards, and the majority of businesses that qualify for it never actually see the savings. Here’s what it is, how it works, and what it takes to actually use it.

The Three Levels of Card Processing Data

Card networks like Visa and Mastercard set interchange rates based partly on risk. The more information a merchant submits with a transaction, the more confidently the network can verify the purchase, and the lower the rate. This is the logic behind the three-tier data system.

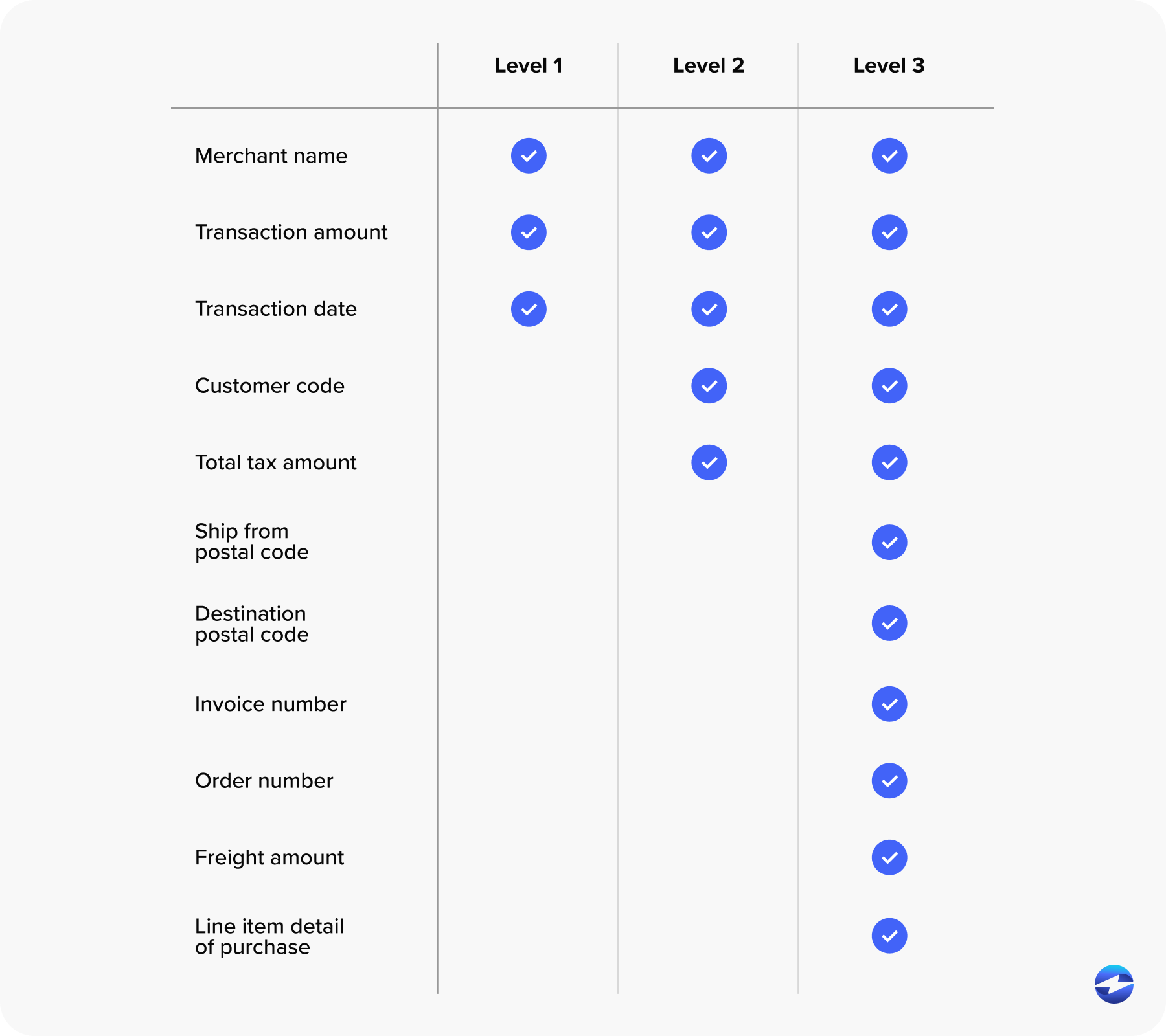

Level 1 is the baseline. It covers what you’d expect: the transaction amount, the merchant name, and the date. Most consumer retail transactions run at level 1.

Level 2 adds a layer of detail. Tax amount, customer code, and merchant postal code are the main additions. It’s enough to qualify for reduced rates on some business cards and is commonly used in B2B transactions.

Level 3 is the most detailed tier. It requires full line-item data for every transaction — product codes, item descriptions, quantities, unit prices, tax at the line level, shipping, and more. Understanding level 3 payment processing starts here: the more data you submit, the better your interchange rate on qualifying cards.

Level 2 vs. Level 3 Processing: What’s the Difference?

The simplest way to think about level 2 and level 3 credit card processing is this: level 2 describes the transaction, and level 3 describes what was in it.

Level 2 data tells the card network how much was charged, what the tax was, and who the buyer is. That’s useful, but it doesn’t say anything about the actual items purchased. Level 3 goes further and requires a full breakdown of the order: every line item, unit cost, quantity, product code, and applicable discount or freight charge. It’s the difference between submitting a receipt total and submitting the itemized receipt itself.

When comparing level 2 and level 3 processing side by side, the jump from level 2 to level 3 is the most significant in terms of both data volume and potential savings. Level 2 is a step up from the baseline, but level 3 is where B2B companies see the biggest rate impact.

For B2B companies, this distinction matters because the transactions you’re running often already have that line-item detail sitting in the invoice. The question is whether your payment processing solution is actually capturing and submitting it.

Level 3 Processing Rates: What You Actually Save

This is where things get concrete. Level 3 processing rates are lower than level 1 or level 2 because card networks treat detailed line-item data as a signal of a legitimate, well-documented commercial transaction. Lower risk means lower cost.

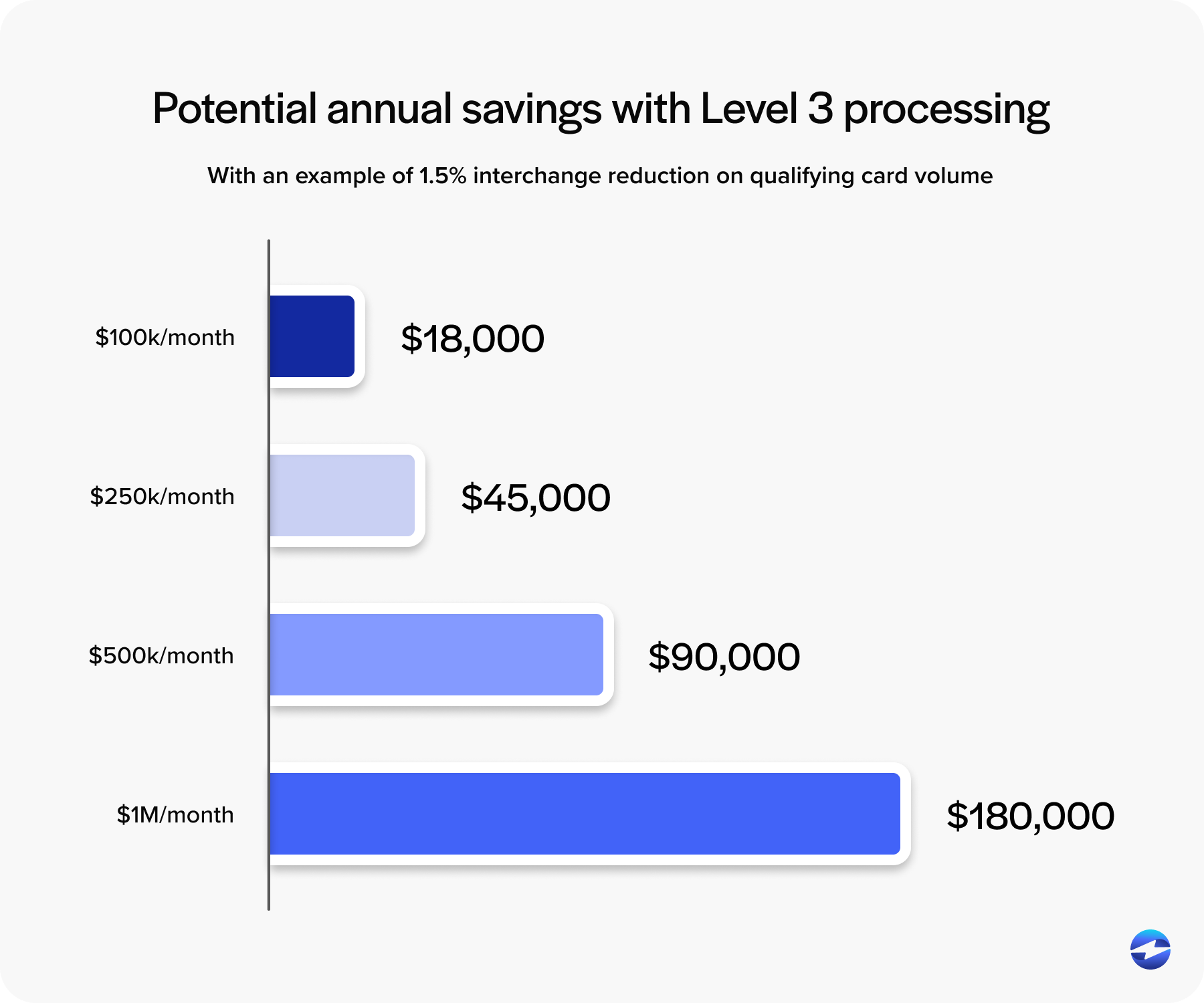

Level 2 typically saves somewhere in the range of 0.5% to 1% over level 1 rates. Level 3 can save an additional 0.5% to 1% on top of that, depending on the card type and network. Those numbers might sound small, but they add up fast.

A company processing $500,000 a month in commercial cards could realistically save tens of thousands of dollars per year by qualifying at level 3 instead of level 1. The difference between level 3 processing rates and standard consumer-tier rates is even more pronounced for companies dealing in government procurement, where purchasing card volume tends to be high, and transaction sizes are large.

One important caveat: the savings only apply to qualifying card types. Consumer credit cards and standard small business cards don’t benefit from level 3 data, regardless of what you submit. The rate reduction is specific to corporate purchasing cards, large-market commercial cards, and government cards.

Level 3 Processing Requirements: What Data You Need

To qualify for level 3 rates, your payment processor needs to submit a specific set of line-item data fields at the time of authorization and settlement. You can’t append this information after the fact — it has to go through with the transaction.

Here are the core level 3 data fields required per transaction:

- Item product code or commodity code

- Item description

- Quantity and unit of measure

- Unit price and line item total

- Discount per line item

- Tax amount at both the line and order level

- Freight and shipping amount

- Duty amount

- Ship-to ZIP or destination postal code

- Customer reference number or PO number

Meeting level 3 processing requirements isn’t just about having the right processor — it’s about making sure the data exists in your system in the first place. Most ERP platforms already capture all of this at the invoice level. The challenge is getting it to pass through to the card network automatically without anyone having to do extra work on each transaction.

This is exactly why so many B2B companies miss out on level 3 rates even when they’re eligible. Their payment processor either doesn’t support level 3 data submission at all, or it requires manual entry that simply doesn’t happen consistently in practice.

Who Actually Qualifies?

Level 3 processing is designed for B2B and B2G (business-to-government) transactions. If your customers are paying with corporate purchasing cards, government procurement cards, or large-market commercial cards issued under Visa or Mastercard’s commercial programs, you’re likely processing transactions that could qualify.

The industries that benefit most are wholesale distributors, manufacturers, government contractors, and professional services firms — basically any business that regularly invoices other businesses or government agencies at meaningful dollar amounts. Wholesale processing systems, billing software for manufacturing companies, and credit card processing for government agencies are important. If you’re a CFO, controller, or AR manager reading this and you process a significant volume of commercial card payments, it’s worth asking your current payment processor whether level 3 data is being submitted on eligible transactions.

Not All Processors Support Level 3

This is where many businesses run into a wall. Level 2 level 3 processing support is not universal. Many standard merchant accounts only process at level 1 by default, and some processors that claim to support level 3 actually require manual batch file submissions or separate data entry, which defeats the purpose entirely.

Knowing what separates genuine level 2 and level 3 credit card processing support from surface-level claims is important. Ask your processor directly: Is level 3 data submitted automatically for every eligible transaction, or does someone have to submit it manually? The answer will tell you a lot.

What you want is a payment processing solution that captures and submits level 3 data automatically as part of the normal payment workflow. No extra steps, no separate system to maintain, no room for human error.

ERP-integrated payment solutions are particularly well-suited for this. Every invoice in an ERP already has product codes, quantities, unit prices, tax amounts, and shipping details. The processor just needs to read that data and pass it through at settlement.

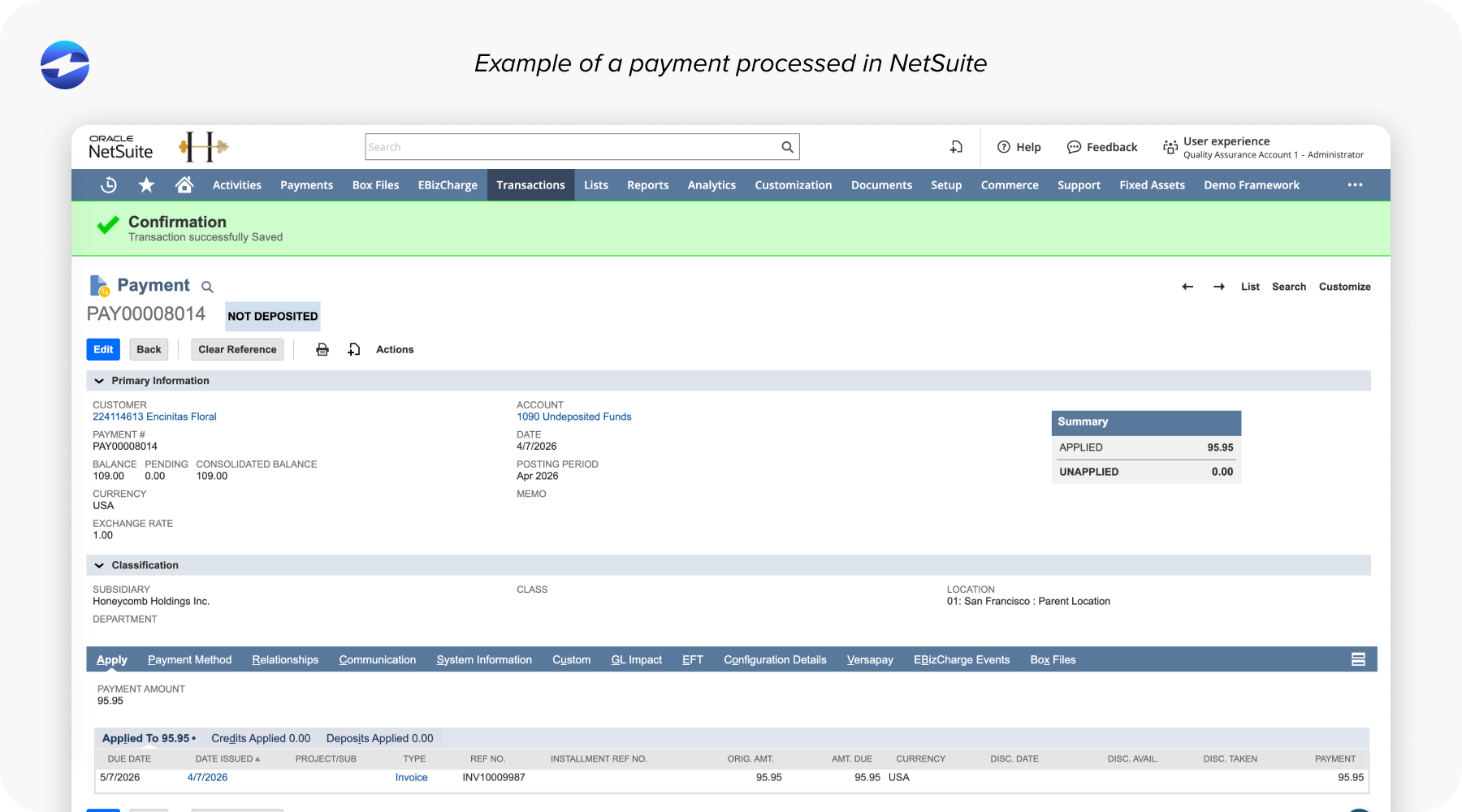

A Real-World Example: Level 3 Processing in NetSuite

Here’s how this plays out in practice. A wholesale distributor using NetSuite invoices a corporate customer for a large equipment order. The customer pays by purchasing card.

Without level 3 credit card processing, that transaction likely downgrades to a higher interchange rate. The distributor pays more than they should, and they probably don’t even know it because it’s buried in the processing statement.

With an EBizCharge integration in NetSuite, the payment is processed directly inside NetSuite, and the line-item data from the invoice — product codes, quantities, unit prices, tax, shipping — is automatically submitted with the transaction. No copying data between systems. No manual fields to fill out. The transaction qualifies at level 3 rates because the integration is built to pass that data through without any extra effort from the user.

The same logic applies across other ERP platforms. Level 3 payment processing works best when it’s embedded in the system where invoices originate, not bolted on afterward.

How to Get Started

Start by reviewing your processing statements to understand what share of your transactions are running on qualifying commercial or government cards. If it’s a meaningful portion of your volume, level 3 is worth pursuing. Then ask your current payment processor directly: Are you submitting level 3 data on eligible transactions automatically? If they can’t give you a clear answer, that’s a signal.

From there, check whether your invoicing or ERP system already collects the fields required for level 3 data submission. In most ERP environments, the data is already there — the question is whether your processor can access it.

If your current setup isn’t getting you to level 3, look for a payment processing solution built specifically for B2B. Processors embedded directly into ERP systems are the most reliable path to consistent level 3 qualification, because the data handoff happens automatically rather than depending on manual processes that can break down.

A Native Solution

Level 3 processing is one of the more straightforward ways B2B companies can reduce their payment processing costs, and most businesses that qualify for it aren’t taking advantage of it. The barrier usually isn’t eligibility. It’s that the processor isn’t submitting the right data, or the payment workflow isn’t connected to the system where that data lives.

The EBizCharge b2b payment solution is built to close that gap. Because it integrates natively into 100+ ERP, CRM, and accounting platforms — including NetSuite, Sage, Microsoft Dynamics, and Acumatica — it sits directly inside the system where invoices are created. That means the line-item details required for level 3 credit card processing are already there, and EBizCharge passes them through automatically with every eligible transaction. No manual data entry, no downgrade risk, no separate workflow to manage.

For B2B companies processing significant commercial card volume, that’s a meaningful difference. If you’re not sure whether your current setup qualifies for level 3 processing rates, that’s a conversation worth having with your payment processor today.