Blog > Low-Cost Credit Card Processing: How Much Merchants Can Cut Processing Fees

Low-Cost Credit Card Processing: How Much Merchants Can Cut Processing Fees

Most merchants know they’re paying credit card processing fees. Fewer know exactly what they’re paying, why they’re paying it, or how much of it is actually negotiable. That gap is expensive.

For CFOs and controllers managing high transaction volumes, credit card processing fees are one of those line items that tend to be accepted rather than examined. They show up on the statement, they get paid, and life moves on. But for mid-market B2B companies running meaningful volume, even a modest reduction in effective rate translates into real money. This guide breaks down where your fees actually come from, what low-cost credit card processing looks like in practice, and how to honestly evaluate whether you’re getting a fair deal.

What’s Actually Driving Your Processing Fees

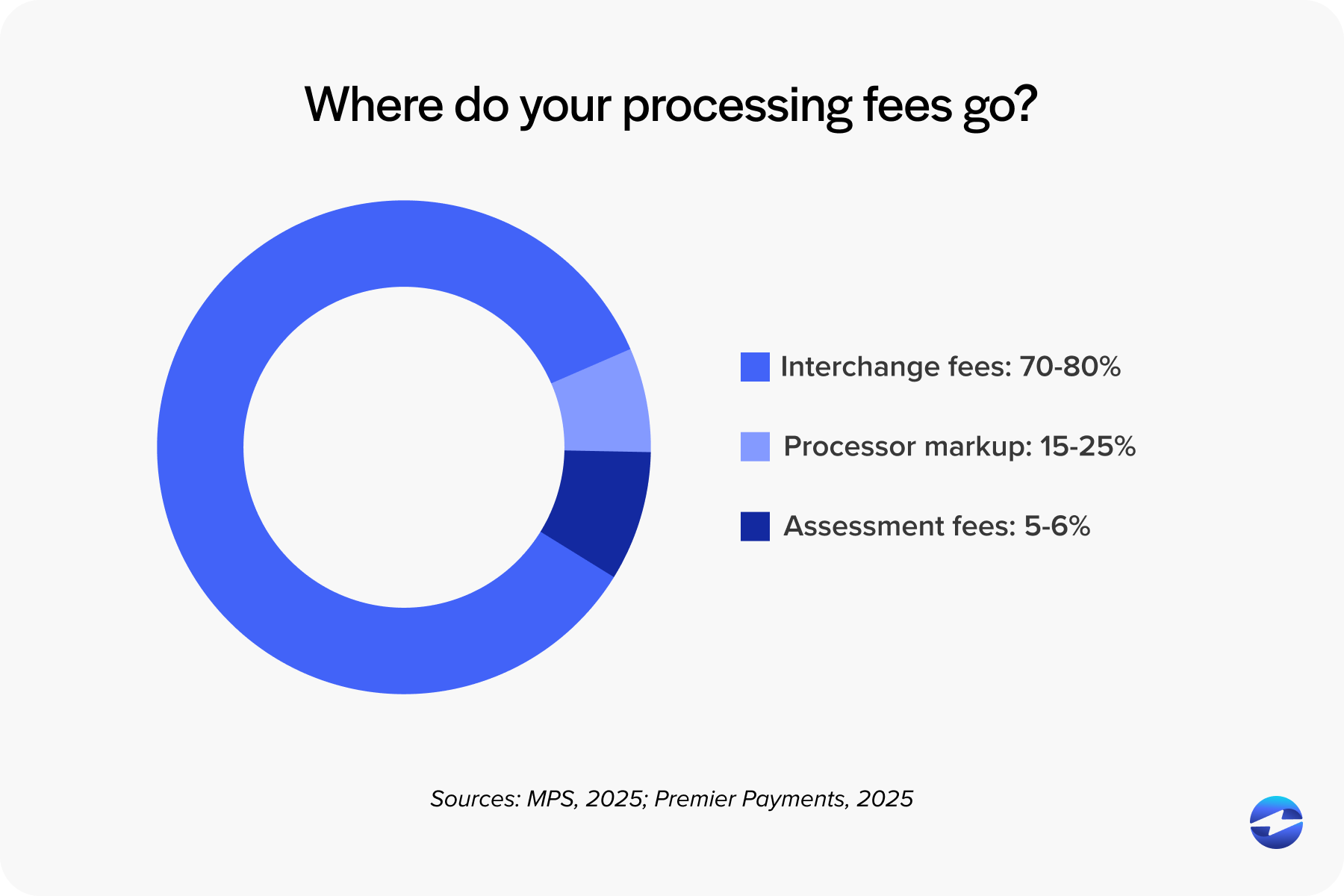

Before you can cut costs, you need to understand the structure. Credit card processing fees have three components, and they don’t all behave the same way.

Interchange is the largest piece. It’s the fee paid to the cardholder’s issuing bank on every transaction, and it’s set by the card networks (Visa, Mastercard, Amex). You can’t negotiate interchange. It varies based on card type, industry, and how the transaction is processed, but it’s not something your payment processor controls.

Assessment fees are charged by the card networks themselves. They’re small, typically a fraction of a percent, but they’re also non-negotiable.

The processor markup is the only part of your fee structure that’s actually negotiable. It’s what your payment processor charges on top of interchange and assessments for handling the transaction. This is where the real conversation happens when you’re shopping for low-fee credit card processing.

Beyond those three, merchants often carry a layer of fees they don’t pay close enough attention to: monthly minimums, PCI compliance fees, batch fees, gateway fees, statement fees, and chargeback fees. None of these are large on their own, but collectively they inflate your effective rate and represent costs that a better payment processing solution can often eliminate or reduce significantly.

Pricing Models: What You’re Actually Agreeing To

How your processor structures its pricing matters as much as the rates themselves.

Interchange-plus pricing is the most transparent model available. The processor passes interchange through at cost and adds a fixed markup on top, so you can see exactly what you’re paying for. This is the gold standard for merchants who want clarity.

Flat-rate pricing is simple and easy to understand, which makes it appealing for low-volume merchants. But at scale, it tends to be expensive. You’re paying one rate regardless of card type, which means you’re often overpaying on low-cost transactions.

Tiered pricing is the model to be most skeptical of. Processors bucket transactions into qualified, mid-qualified, and non-qualified categories, and a lot more transactions end up in the higher-cost buckets than you’d expect. This model benefits the processor far more than the merchant.

Subscription pricing charges a flat monthly fee plus interchange at cost. For high-volume merchants, it can be very competitive. It requires comparing your monthly fee to what you’d pay in markup under interchange-plus, but the math is usually worth doing.

If you’re currently on tiered pricing and haven’t looked closely at your statement in a while, that’s probably the first place to start.

Zero-Cost Processing: Appealing, But Not for Everyone

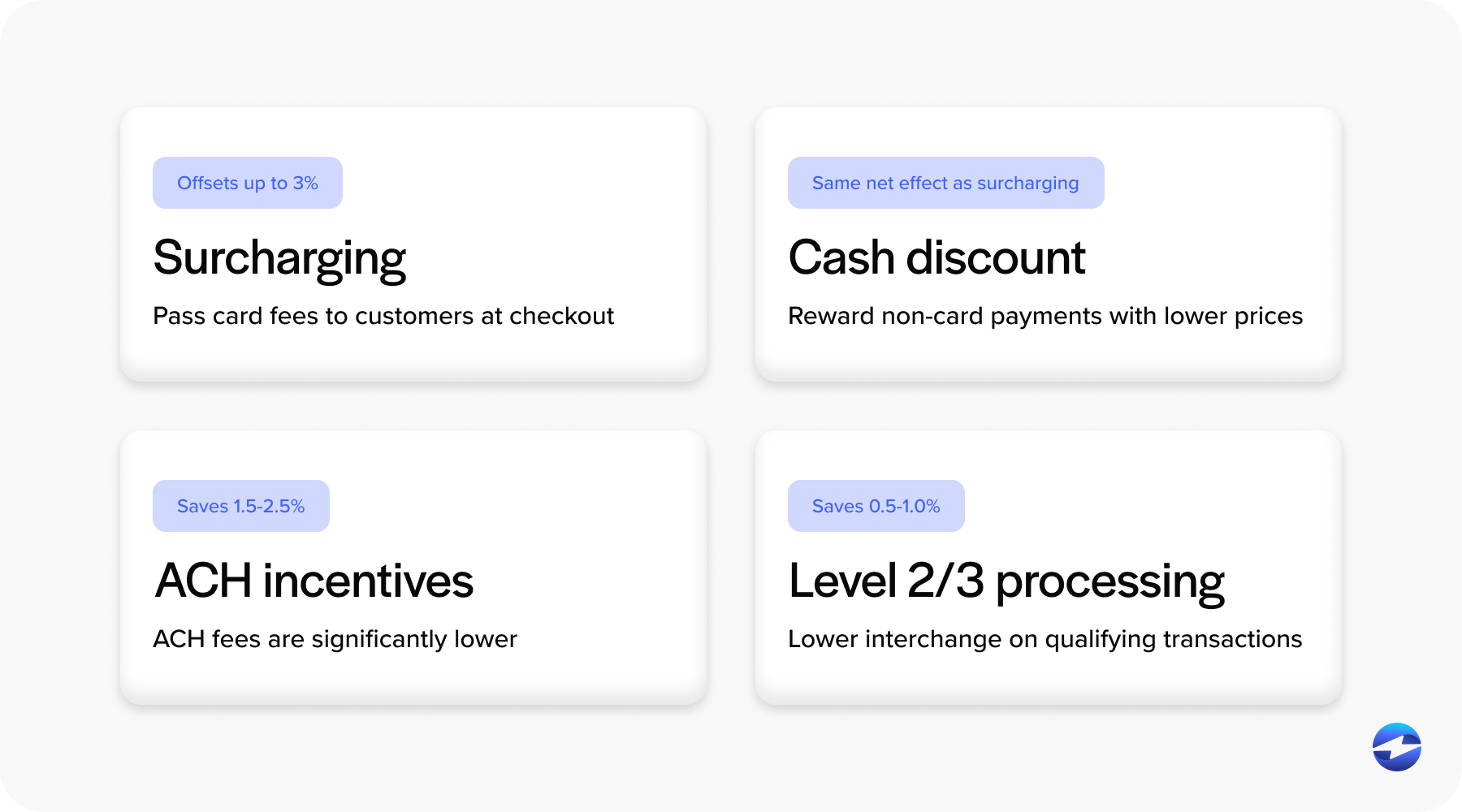

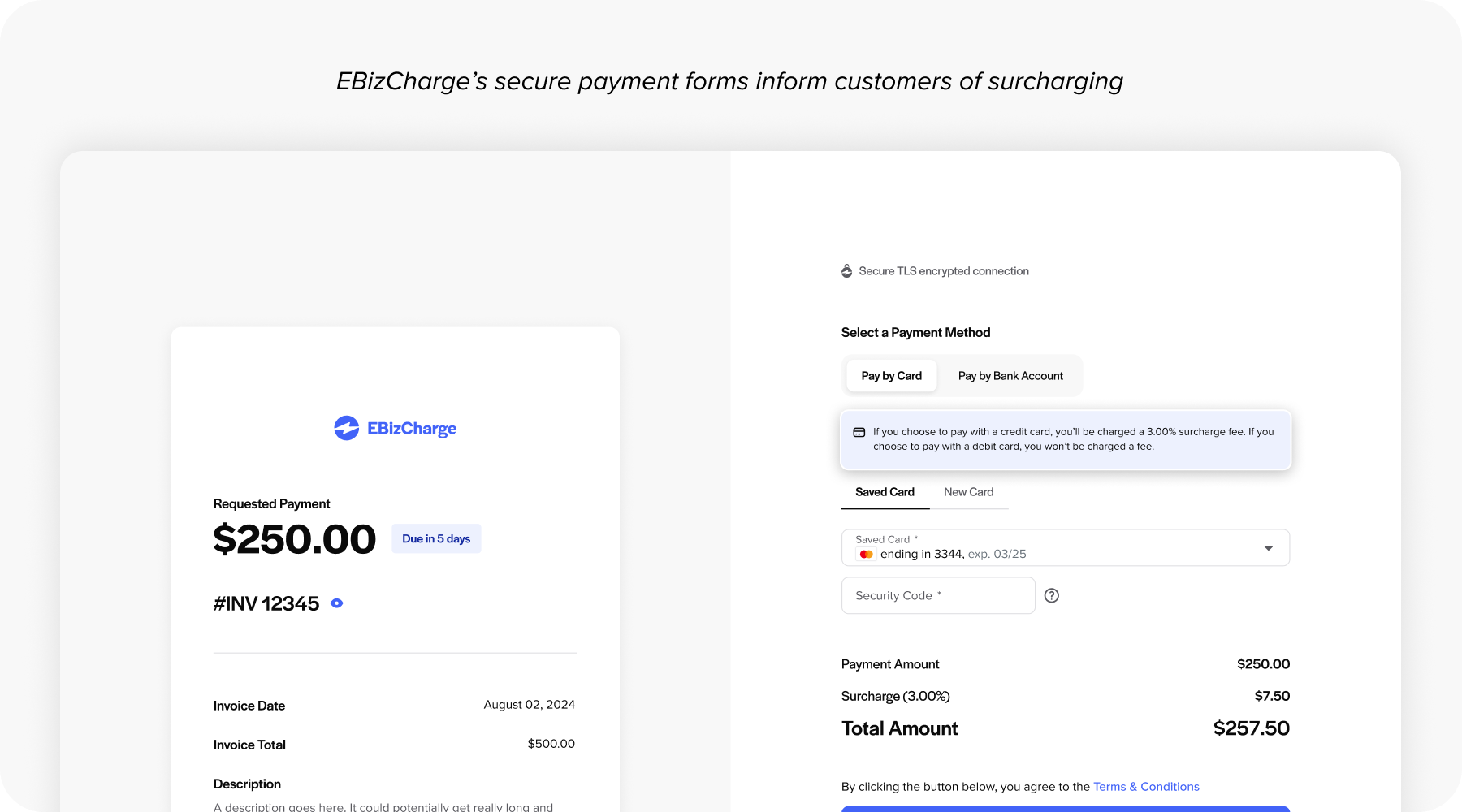

Zero-fee credit card processing, meaning the merchant pays nothing in processing fees, comes in two forms: surcharge programs, where credit card users pay a fee at checkout, and cash discount programs, where customers paying cash receive a lower price.

The appeal is obvious. No-cost credit card processing sounds like the best possible outcome, and for some merchants it genuinely is. B2B businesses with established customer relationships and lower price sensitivity tend to absorb surcharge programs without significant pushback. When your customer is a purchasing department rather than an individual consumer, a 3% surcharge on a $50,000 invoice lands differently than a surcharge at a coffee shop.

But zero cost isn’t a universal solution. Consumer-facing businesses in competitive markets often see customer friction that outweighs the savings, and the compliance requirements for surcharging, network registration, disclosure rules, signage requirements, and card-type restrictions are more detailed than most merchants expect. Getting them wrong creates real exposure.

0 credit card processing fees is a compelling idea, but the right question isn’t whether you can avoid fees entirely. It’s whether the tradeoffs make sense for your business specifically.

The B2B Cost Lever Most Merchants Aren’t Using

This one is worth its own section because it’s genuinely underutilized, particularly in B2B environments.

Level 2 and Level 3 processing refers to submitting additional transaction data fields when processing corporate card payments. Level 2 includes things like tax amount and customer code. Level 3 includes line-item detail, essentially invoice-level data attached to the transaction. When this data is submitted, card networks reward it with lower interchange rates because it reduces fraud risk and gives corporate card programs better visibility into spending.

The savings are worth noting as well. Level 3 transactions can qualify for rates that are 0.5% to 1.0% lower than standard B2B interchange. At $100,000 monthly volume, that’s $500 to $1,000 per month in reduced credit card processing fees without changing your processor, pricing model, or anything customer-facing.

The catch is that most standalone processors and third-party gateways don’t submit Level 2 and Level 3 data automatically. It requires either manual data entry from your billing team, which creates its own overhead, or a payment processor that handles it natively through your accounting or ERP system.

Embedded Payments vs. Standalone Processors: Where Hidden Costs Live

When people ask who has the lowest credit card processing fees, they’re usually comparing rates. But the more complete question is: what does payment processing actually cost your organization when you factor in everything?

Standalone processors require separate gateways, manual reconciliation, and duplicate data entry between your payment system and your ERP. AR teams spend time manually posting payments, matching transactions to invoices, chasing down errors, and generating reports that your accounting system didn’t automatically capture. That time has a cost.

Embedded payments mean the processor lives inside your ERP or accounting platform. Transactions are posted automatically. AR updates in real time. Level 2 and Level 3 data submits without anyone on your team doing anything extra. You’re not paying for a separate gateway because the integration is native.

When you compare the average credit card processing fees between an embedded and a standalone processor, the rate might look similar on paper. But once you account for gateway fees, operational overhead, reconciliation errors, and the staff time your AR team spends on manual tasks, the embedded approach almost always wins on total cost.

What to Ask Before Switching Processors

For CFOs and controllers actively evaluating options right now, here’s what to press on before signing anything.

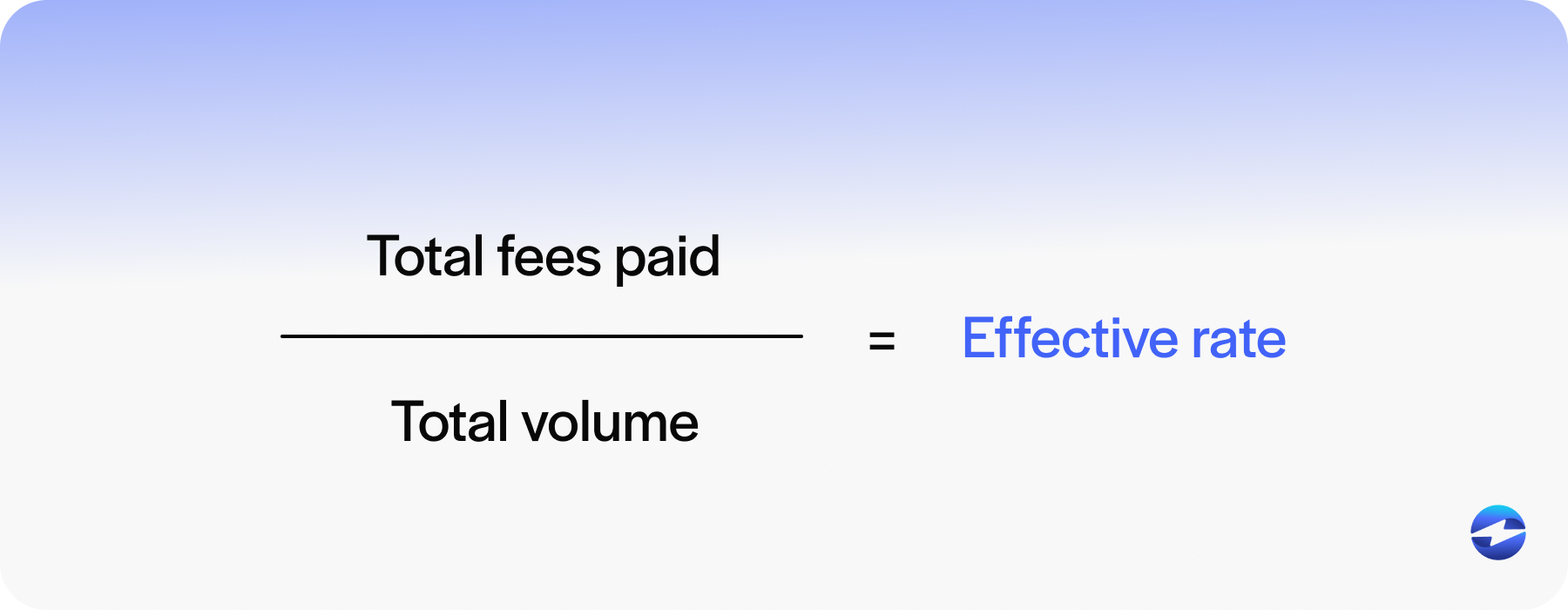

Ask for your effective rate, all-in. That means interchange plus assessments plus markup plus every fee on the statement divided by total volume. Some processors will give you a rate quote that doesn’t reflect the full picture.

Ask whether your pricing is interchange-plus or tiered. If it’s tiered, ask to see how your transactions have been qualifying over the past few months.

Ask whether Level 2 and Level 3 data is being submitted automatically on your B2B transactions. If your processor isn’t sure, it probably isn’t happening.

Ask what reconciliation looks like inside your accounting system. If the answer involves manual steps, that’s overhead worth quantifying.

Additionally, ask what fees you’re paying outside of interchange and markup. PCI fees, gateway fees, batch fees, and monthly minimums all add up.

How EBizCharge Approaches Low-Cost Processing

EBizCharge’s payment processing solution is a great option for low cost processing. Level 2 and Level 3 data is submitted automatically on eligible B2B transactions through the native ERP integration, so your team doesn’t manage it manually, and you capture the interchange savings without adding any process.

Because EBizCharge is embedded directly inside more than 100 ERP, accounting, and CRM platforms, there’s no standalone gateway fee. Payments post automatically, AR updates in real time, and reconciliation happens without your billing team spending hours on it each month.

Surcharge and cash discount programs are also supported with compliance enforcement built in, so merchants who want to pursue no-cost credit card processing have a path to do that without managing the compliance complexity manually.

The result is a payment processing solution that reduces both your processing rate and the operational overhead your team carries. That combination is where the real savings show up.

Processing Fees Are Not a Fixed Cost

Processing fees may feel like a fixed cost because most merchants treat them that way. But the rate you’re paying today reflects the processor you chose, the pricing model you agreed to, and the data you are or aren’t submitting on every transaction. All of those things can change.

CFOs and controllers who treat payment processing as a strategic line item rather than a utility bill consistently pay less. The gap between what merchants pay and what they could pay for low-cost credit card processing is usually wider than they expect.

- What’s Actually Driving Your Processing Fees

- Pricing Models: What You’re Actually Agreeing To

- Zero-Cost Processing: Appealing, But Not for Everyone

- The B2B Cost Lever Most Merchants Aren’t Using

- Embedded Payments vs. Standalone Processors: Where Hidden Costs Live

- What to Ask Before Switching Processors

- How EBizCharge Approaches Low-Cost Processing

- Processing Fees Are Not a Fixed Cost