Blog > Who Pays Credit Card Processing Fees? A Merchant’s Guide

Who Pays Credit Card Processing Fees? A Merchant’s Guide

Most businesses don’t think carefully about credit card processing fees until someone in finance finally adds them up. Then the number lands on a spreadsheet, and suddenly it’s a conversation worth having. A business processing a million dollars a year in credit card payments at a 2.5% average rate is quietly writing a $25,000 check to its payment processor every year. That’s not a rounding error. That’s a real cost that deserves a real strategy.

The question of who pays credit card transaction fees is more nuanced than it might seem. The default answer is the merchant. But the default isn’t the only option, and understanding what’s actually available can change how your business approaches processing costs entirely. This guide covers how fees work, who absorbs them by default, how surcharging and discount programs redistribute the cost, and how the right payment processing solution handles all of it automatically.

How Credit Card Fees Are Structured

Before getting into who pays, it helps to understand what’s actually being paid and where it goes.

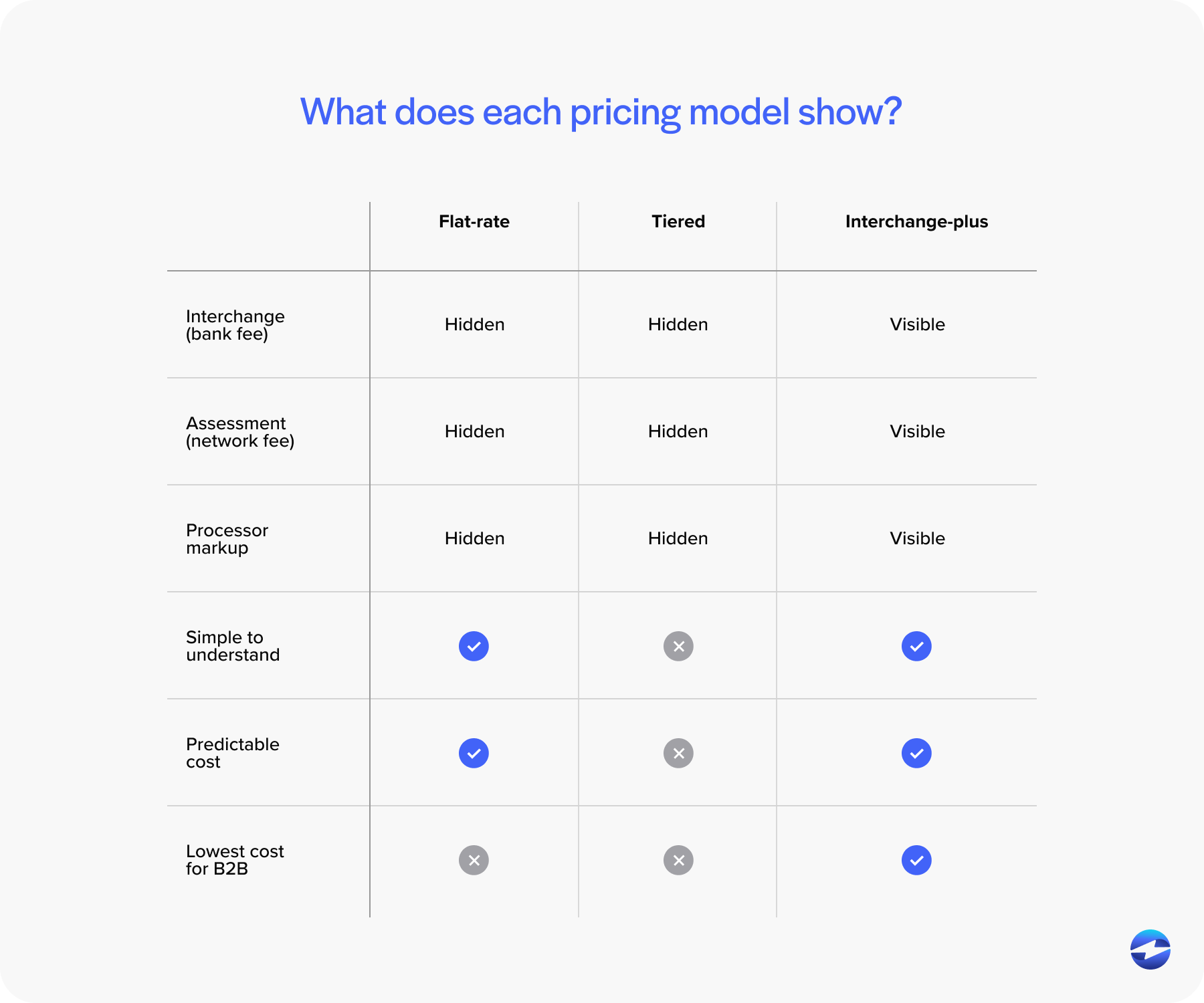

Every credit card transaction involves three separate fee components. The largest piece is the interchange fee, which goes to the bank that issued the customer’s card. Interchange rates vary by card type, transaction type, and industry, but for B2B merchants accepting corporate or rewards cards, these rates can be meaningfully higher than average. The second component is the assessment fee, which goes to the card network itself, meaning Visa, Mastercard, American Express, or Discover. Assessment fees are relatively small and fairly consistent. The third component is the processor’s markup, which is what your payment processor charges on top of interchange and assessments for handling the transaction.

The combination of all three is what shows up as your effective processing rate. Flat-rate pricing bundles everything into one number. Interchange-plus pricing separates the processor markup from interchange and assessments, which gives merchants more visibility into what they’re actually paying. Tiered pricing groups transactions into buckets that often obscure the real cost. Merchants who want to know who has the lowest credit card processing fees are usually asking the wrong question. The better question is which pricing model gives you the most transparency, because a low headline rate with hidden fees often costs more than a slightly higher rate with clean, predictable pricing.

For B2B merchants specifically, the card mix matters. Corporate cards, purchasing cards, and high-reward consumer cards all carry higher interchange rates than a standard debit card. If a significant portion of your customers pay by corporate card, your effective rate is probably higher than you realize.

Who Bears the Cost by Default

The default answer to who pays credit card fees for merchants is straightforward: the merchant. The processor deducts fees from each transaction before depositing the net amount into the merchant’s bank account. There’s no invoice, no separate line item, and no moment where the cost feels particularly visible. It just happens quietly on every transaction, every day.

That invisibility is part of why so many businesses accept processing fees as a fixed cost of doing business without ever questioning it. The fees don’t arrive as a bill. They arrive as a slightly smaller deposit.

The real cost compounds beyond the per-transaction rate, though. Chargebacks carry their own fees regardless of outcome. Refunds often still incur the original processing cost. Monthly minimum fees apply when volume dips. Taken together, credit card fees for merchants add up to more than the headline rate suggests, and the businesses that never examine them closely are the ones paying the most over time.

Absorbing fees entirely makes sense in some contexts. If you’re in a highly competitive consumer market where adding any cost to the customer experience would hurt conversion, passing fees along may not be practical. But for B2B businesses billing other companies, the calculation looks very different.

How Surcharging Shifts Fees to the Customer

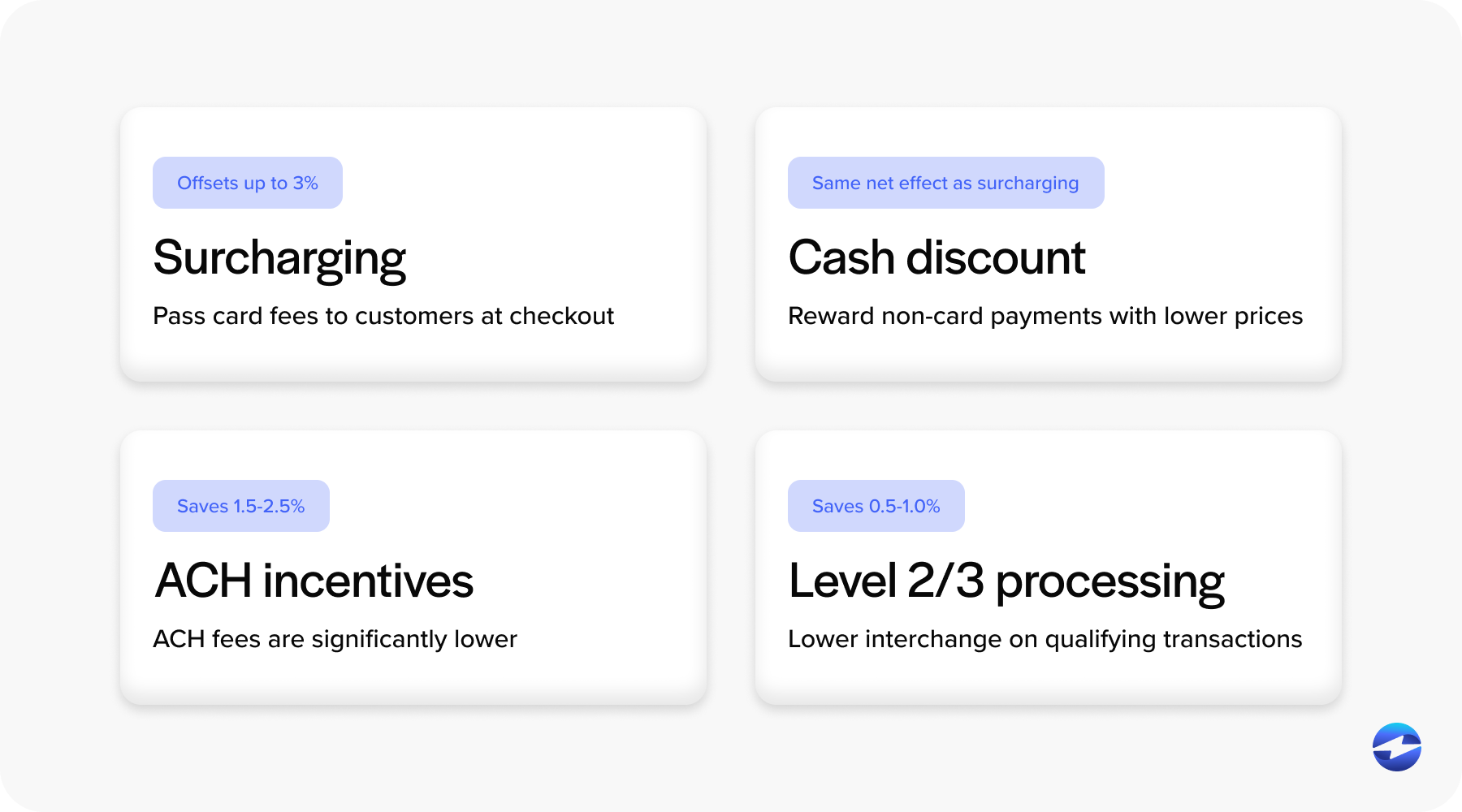

Surcharging is the practice of adding a fee to credit card transactions to offset the merchant’s processing cost. When configured correctly, a credit card surcharge is passed directly to the customer at the time of payment, which means the merchant nets the full invoice amount without absorbing the processing cost.

Credit card surcharging is legal in most U.S. states, though a small number of states still have restrictions worth verifying before implementing a program. Card networks also have rules that merchants must follow. Visa and Mastercard both require advance disclosure to customers before a surcharge is applied. There are cap limits on how much can be charged, currently 3% for Visa transactions, and surcharges cannot be applied to debit card transactions under any circumstances. Merchants are also required to register with the card networks before beginning a surcharging program.

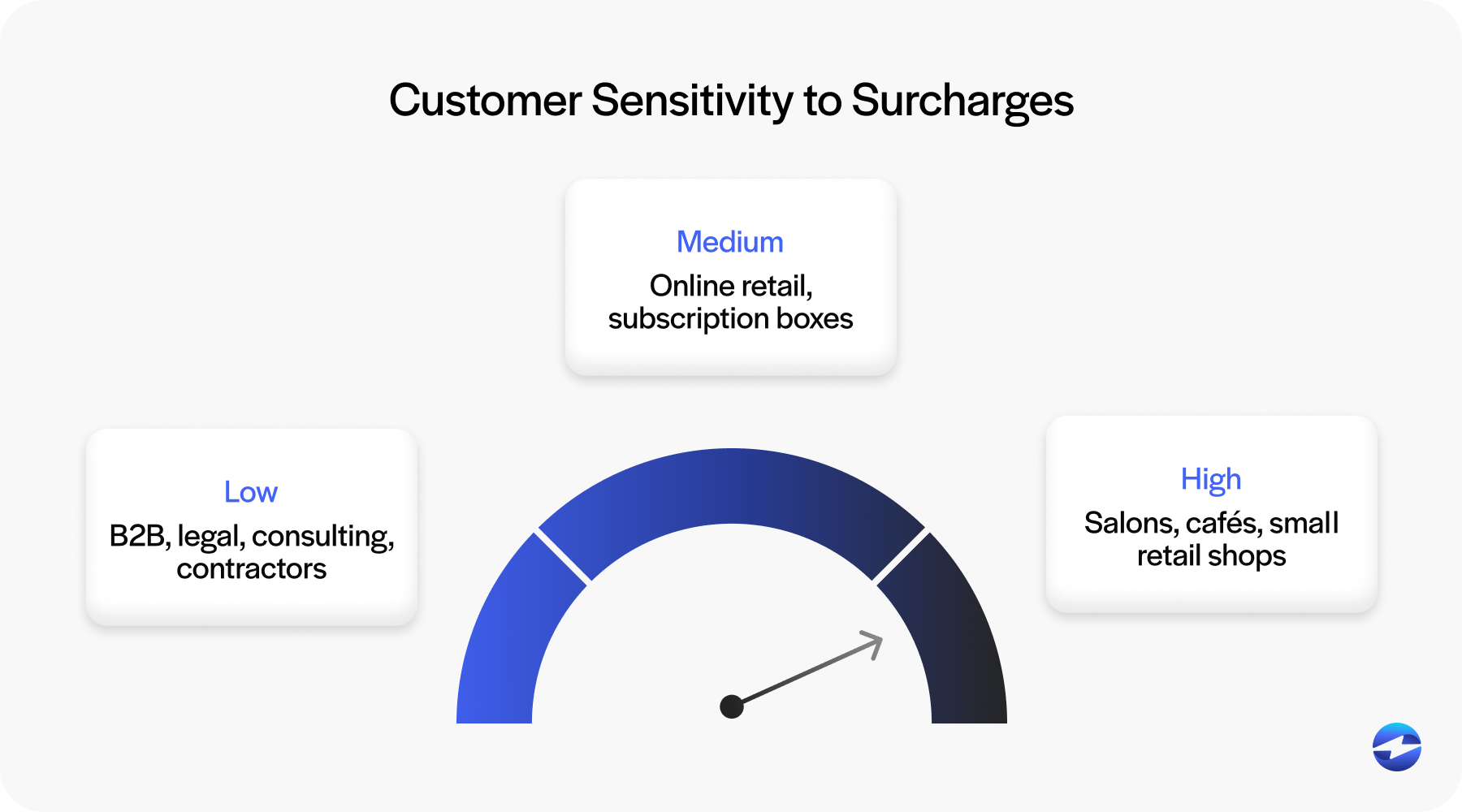

A surcharge on credit card transactions is generally more accepted in B2B environments than in consumer-facing ones. When a business is paying another business, a clearly disclosed processing fee is a routine part of the transaction. The discomfort surcharging sometimes creates in retail settings rarely shows up in B2B billing relationships.

The compliance piece is where merchants get tripped up most often. Applying a surcharge for using a credit card inconsistently across customers, exceeding the fee cap, failing to disclose before the transaction, or accidentally applying a surcharge to a debit card are all violations that carry real consequences. This is one of the reasons that manual surcharging programs are risky, and automated solutions are worth taking seriously.

How Discount Programs Work

Cash discount programs take a different approach to the same problem. Rather than adding a fee for card payments, the merchant builds the processing cost into the standard price and then offers a discount to customers who pay by cash, check, or ACH. The result is similar to surcharging in terms of who ultimately absorbs the cost, but the mechanics are different, and the card network rules are less restrictive.

Some businesses find cash discount programs easier to communicate to customers because the framing is a reward rather than a penalty. Others find surcharging more straightforward because the pricing doesn’t change for the majority of transactions.

ACH is worth calling out specifically here. For B2B merchants with large invoice amounts, ACH processing fees are significantly lower than credit card rates, typically a fraction of a percent, with a small transaction cap. Encouraging customers to pay by ACH through a discount or incentive program can reduce processing costs meaningfully without the compliance complexity of credit card surcharging.

Level 2 and Level 3 processing is another cost-reduction lever that often gets overlooked entirely. B2B card transactions can qualify for lower interchange rates when enhanced data is passed at the time of the sale. Level 2 includes information like the tax amount and a customer code. Level 3 adds full line-item detail. Corporate purchasing cards and government cards are particularly likely to qualify for lower rates with this data. The savings per transaction are modest, but across high-volume B2B processing, they compound quickly.

How Embedded Payment Software Handles Fee Allocation Automatically

Managing surcharging, cash discounts, and Level 2/3 data manually is where compliance risks and reconciliation errors tend to pile up. Tracking which cards are credit versus debit, applying the correct surcharge rate consistently, passing Level 2/3 data on qualifying transactions, handling disclosure requirements, and then posting it all correctly to the right GL accounts is a lot to manage by hand.

Embedded payment software handles all of it automatically. When a payment processor is built natively into your accounting or ERP system, it can identify card types at the time of the transaction, apply a surcharge on credit card transactions only where appropriate, pass Level 2/3 data automatically on qualifying B2B purchases, and post the fee allocation to the correct accounts in your general ledger without any manual adjustment.

The reconciliation benefit is also worth noting. When the payment processing solution is embedded in the system your AR team already works in, surcharges and discounts appear correctly on every transaction record from the moment the payment is processed. Month-end close doesn’t require a separate reconciliation pass to account for fee allocations because the software has already handled it.

Real-time reporting gives finance leadership visibility into exactly what was paid in fees, what was passed to customers through surcharging, what was offset through ACH, and what the net cost of processing actually was for any given period. That visibility is difficult to achieve when payment data lives in a disconnected processor and has to be imported or reconciled manually.

How EBizCharge Manages Processing Fees

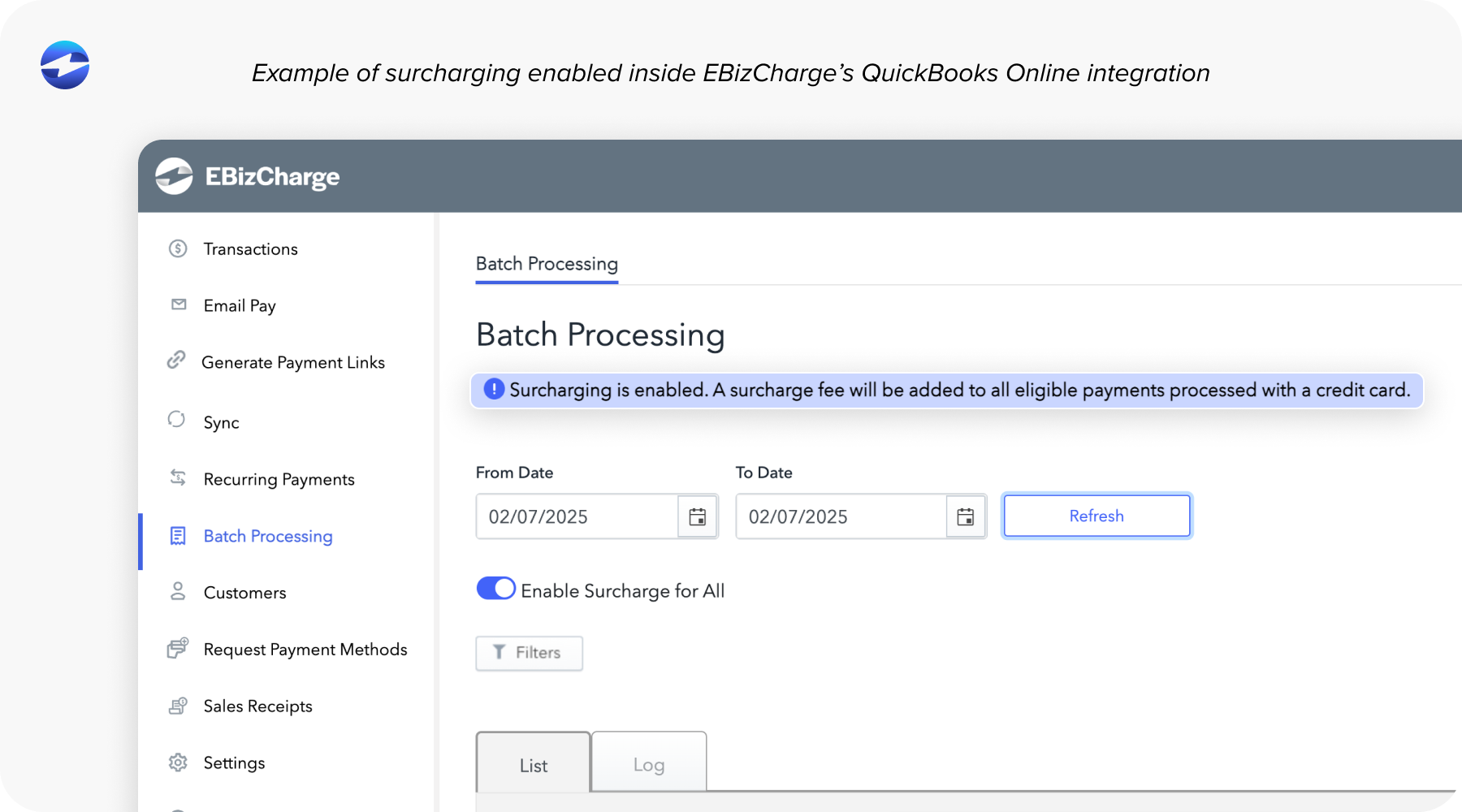

EBizCharge includes built-in credit card surcharging that is automatically applied, compliant with card network rules, and consistent across every transaction type. The platform identifies card types at the point of sale, applies surcharges only where appropriate, enforces cap limits, and handles the registration and disclosure requirements that merchants are responsible for meeting.

Level 2 and Level 3 data passes automatically on qualifying B2B transactions, which means interchange savings happen without anyone on your team having to think about it. ACH processing is fully supported for businesses that want to incentivize lower-cost payment methods.

Because EBizCharge integrates natively with over 100 ERP, CRM, and accounting platforms, fee allocations post directly to the correct GL accounts in real time. There’s no manual entry, no separate reconciliation process, and no gap between what the payment processor recorded and what your accounting system shows.

For business owners, controllers, and AR managers who are serious about understanding and managing credit card fees, the right payment processor makes the difference between a cost that runs on autopilot and one that actually works in your favor.