Templates | Surcharge Signage

Free Printable Credit Card Fee Sign (PDF Download)

Free Printable Credit Card Fee Sign (PDF Download)

Looking for a credit card surcharge sign you can print and post today?

Download our free PDF sign and start displaying your credit card processing fee clearly and compliantly.

Download your free printable credit card fee sign to clearly communicate surcharge policies while maintaining transparency and compliance.

Our free credit card processing fee sign gives you a clean, professional notice you can print and display right away. It keeps your customers informed and helps your business stay on the right side of card network rules.

Learn more

What Is a Credit Card Surcharge?

A credit card surcharge is an extra fee added to a transaction when a customer pays with a credit card. Businesses use this fee to offset the cost of credit card processing, which is charged by card networks like Visa, Mastercard, American Express, and Discover every time a card is swiped, tapped, or entered online.

If you’ve ever wondered why some businesses charge more for card payments, that’s usually the reason. Processing fees can eat into margins pretty quickly, especially for small and mid-sized businesses handling a high volume of transactions. A surcharge lets you recover some or all of that cost without raising your prices across the board.

| Overview | |

|---|---|

| Purpose | To offset credit card processing fees |

| Application | Applies to credit card transactions only, not debit or prepaid cards |

| Amount | Typically a percentage of the total purchase price |

| Presentation | Listed as a separate line item on the customer’s receipt |

| Legal Status | Permitted in most U.S. states, with a few exceptions |

Key U.S. Credit Card Surcharge Rules

Before you print a credit card fee sign and post it at your register, you need to understand the rules that govern surcharging. Getting this wrong can lead to fines, chargebacks, or losing your ability to surcharge altogether.

1. Legal in Most States

Surcharging is legal across most of the United States, but not everywhere. A handful of states ban the practice entirely based on consumer protection laws. As of 2025, Connecticut, Massachusetts, and Puerto Rico do not allow credit card surcharges.

If your business operates in one of those areas, you’ll need a different approach. Many businesses in restricted states use a cash discount program instead, which gives customers a lower price for paying with cash rather than adding a fee for using a card. The end result is similar, but the legal framework is different.

It’s worth keeping an eye on this list, too. Surcharge laws have shifted in recent years as more states have revisited their positions. What’s restricted today could change tomorrow, and vice versa.

2. Clear Disclosure Is Required

This is where your credit card surcharge sign comes in. Businesses are required to notify customers about the surcharge before the transaction is completed. Card networks are very specific about this, and failing to disclose properly is one of the fastest ways to run into trouble.

For brick-and-mortar businesses, that means posting signage at your entrance and at the point of sale. Your customers should know about the fee before they decide to pay with a credit card, not after.

For eCommerce businesses, the surcharge needs to be disclosed on your checkout page before the customer enters their payment details. Burying it in fine print or only mentioning it in your terms of service is not enough.

Your receipts also need to show the surcharge as a separate line item. It should be clear exactly how much the customer paid for the product and how much was added as a surcharge. Staff who handle payments should understand the policy too, so they can explain it to any customer who asks.

Failure to provide proper disclosure can trigger chargebacks, compliance violations from card networks, or penalties from your payment processor. Keep your credit card fee sign visible and up to date.

3. Credit Card Surcharge Fee Limits (3% and 4% Cap)

You can’t just pick a number and call it your surcharge. The fee is capped by card network rules, and you can never charge more than your actual processing cost.

Here’s how it breaks down:

- Visa transactions: The surcharge cannot exceed 3% of the total transaction amount.

- Other credit card transactions (Mastercard, Amex, Discover): The maximum surcharge is 4% of the total transaction, or your actual processing cost, whichever is lower.

So if your payment processor charges you 2.5% per transaction, your surcharge can only be 2.5%. You can’t round up to 3% just because Visa allows it. And if your processor charges 3.5%, you can apply that rate on non-Visa cards but you’re still capped at 3% for Visa transactions.

Going over these limits can result in penalties, loss of surcharging privileges, or compliance action from card networks. If you’re unsure about your exact rate, check with your payment processor before setting your surcharge percentage.

4. How to Register Your Surcharge with Card Networks

You can’t just start surcharging overnight. Before you begin, you need to register with the major card networks at least 30 days in advance. This applies to Visa, Mastercard, American Express, and Discover.

The registration process looks like this:

- Submit a surcharge registration form through Visa and Mastercard’s online portals.

- Notify your payment processor and acquiring bank that you plan to apply surcharges.

- Make sure your POS system or payment gateway can itemize surcharge fees separately on receipts.

Skipping registration can lead to disputes, penalties, or even losing your ability to accept certain card brands. It’s a straightforward process, but it’s not optional.

5. Debit and Prepaid Card Exemptions

This one catches a lot of businesses off guard. You cannot apply a surcharge to debit cards or prepaid cards, period. Even if the customer selects “credit” when running their debit card, the card is still classified as debit and is exempt from surcharging.

Federal regulations treat debit transactions differently from credit transactions, and adding a surcharge to a debit card can result in fines, customer disputes, or action from your payment network.

To avoid this, you should configure your payment terminal to automatically exempt debit and prepaid cards from any surcharge. Your staff should also know the difference, since not every customer will know which type of card they’re using. And your receipts should always reflect that the surcharge was only applied to eligible credit card transactions.

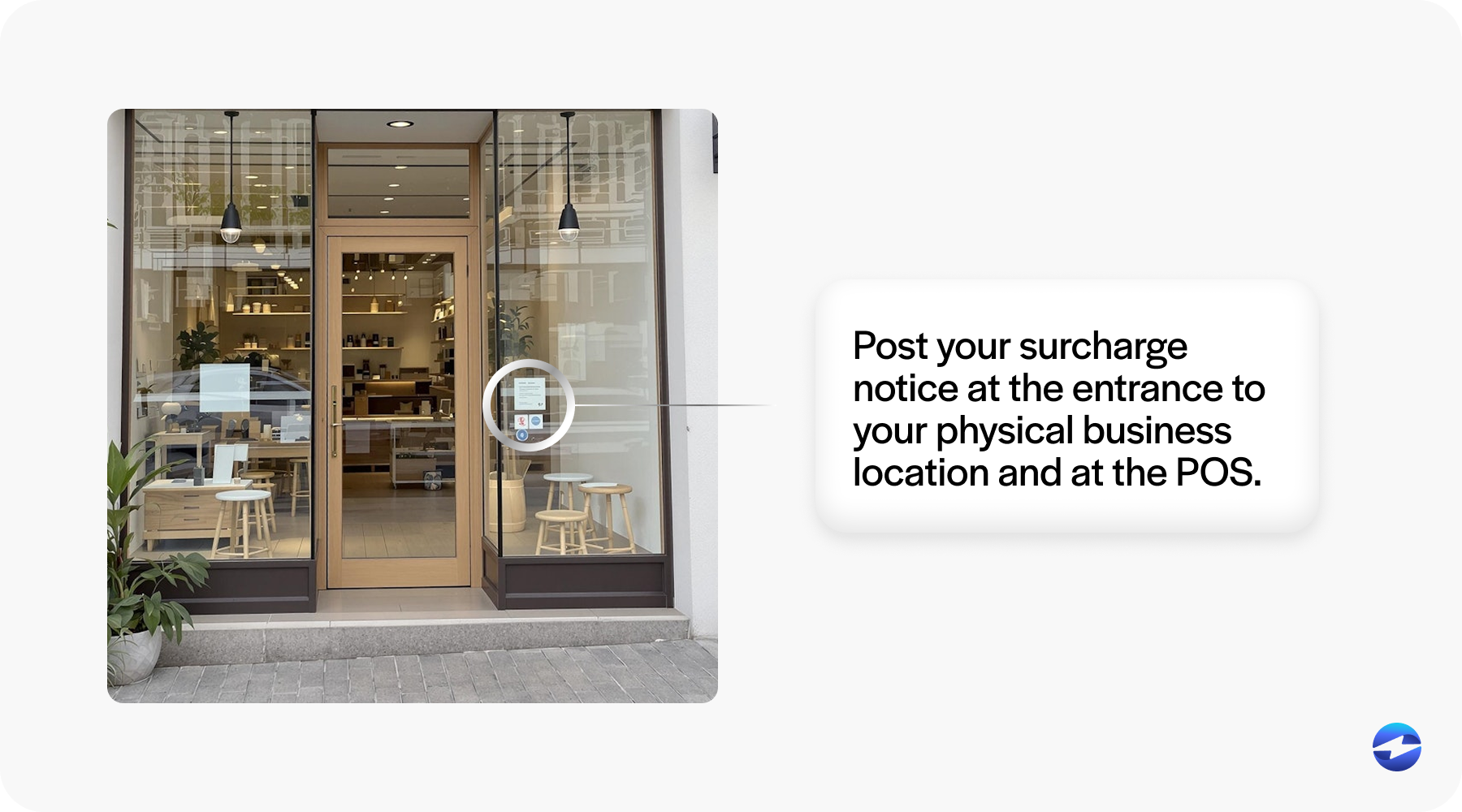

How to Display Your Credit Card Processing Fee Sign

Having a credit card surcharge sign is step one. Knowing where and how to display it is what actually keeps you compliant and avoids customer pushback.

Surcharge Signage Placement for Brick-and-Mortar Stores

If you have a physical location, plan on placing your credit card fee sign in at least two spots. The first should be at your entrance, where customers see it before they start browsing or placing an order. The second should be at the checkout counter, right where the payment happens.

Some businesses also add a smaller version near the card terminal itself, which is a good move if you have multiple checkout stations. The point is to make sure no customer is caught off guard at the moment they swipe. Visa and Mastercard both require that the surcharge is disclosed before the customer commits to paying with a credit card.

If you want to take it a step further, a brief verbal disclosure from your staff can go a long way in building trust. Something as simple as “Just so you know, we do apply a small surcharge on credit card payments” can prevent uncomfortable moments and reduce the chance of chargebacks.

Credit Card Fee Notice for eCommerce and Online Checkout

For online businesses, the disclosure requirements are a bit different but equally important. The surcharge needs to be visible on your checkout page before the customer enters their payment information. A common approach is to place a notice near the order summary or right above the payment fields.

Some businesses add a surcharge note to their FAQ page or terms of service as well. That’s fine as extra coverage, but it can’t be your only disclosure. The card networks want customers to see it at the exact point where they’re choosing how to pay.

If you’re using a payment gateway that supports automated surcharging, like EBizCharge, the surcharge calculation and disclosure can be built into the checkout flow automatically. The system handles the math, applies the correct rate, and displays the fee to the customer before they finalize the order. That takes one more compliance concern off your list.

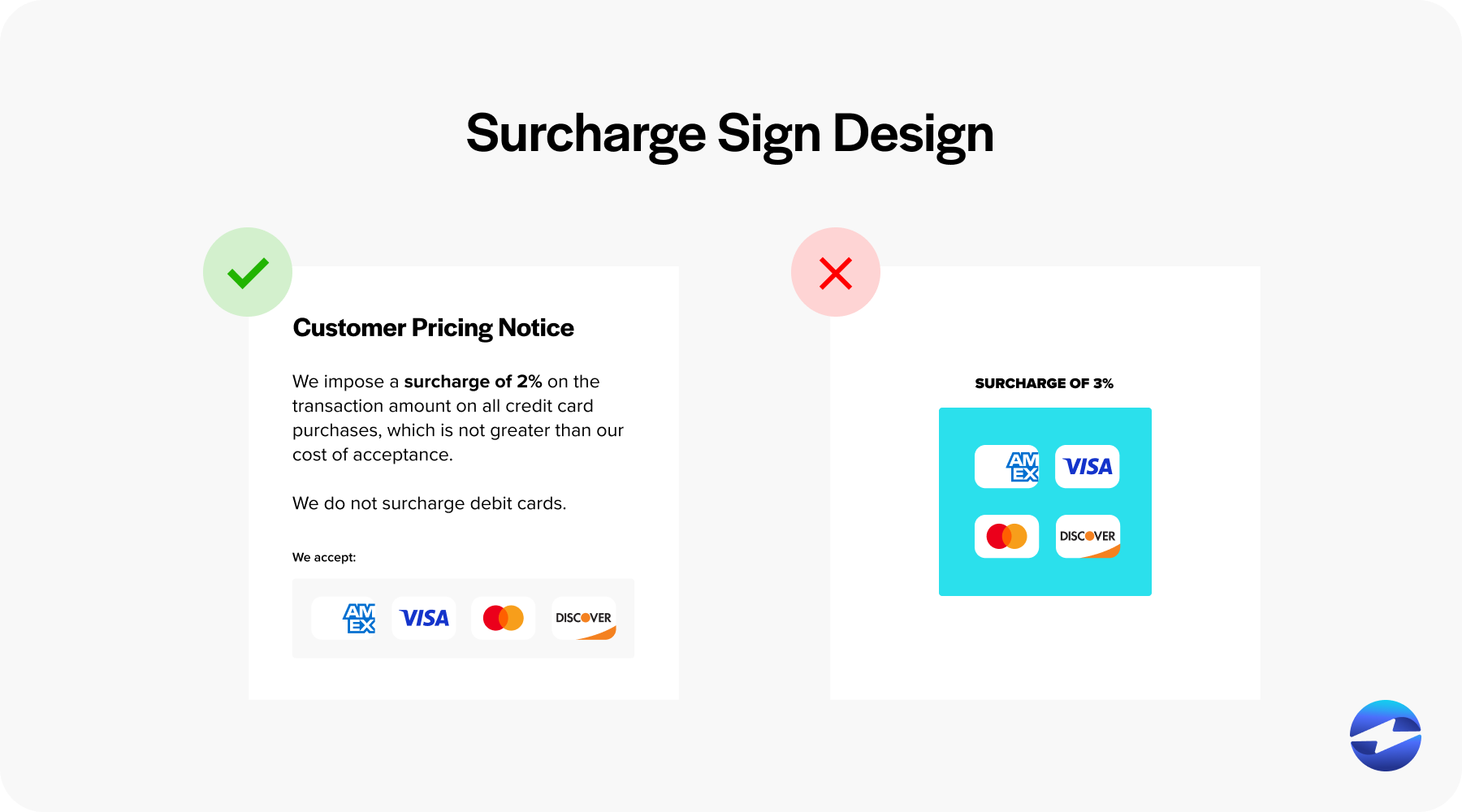

Credit Card Surcharge Sign Templates and Formats

Not every business charges the same surcharge percentage, so your signage needs to match your actual rate. Using the wrong number on your sign is a compliance issue, so accuracy matters here.

3% Credit Card Fee Sign

A 3% surcharge is the most common rate and the maximum Visa allows on any transaction. If your processing costs are at or near 3%, this is the version most businesses will need. Our free downloadable PDF includes a clean, professional 3% credit card fee sign you can print and post right away.

3.5% Credit Card Fee Sign

Some processors charge rates slightly above 3%. If that’s your situation, you may apply a surcharge up to 3.5% on non-Visa credit card transactions. Just keep in mind that Visa transactions are still capped at 3%, regardless of your actual processing cost. If you accept multiple card brands at different surcharge rates, your payment system should be configured to handle that distinction automatically.

4% Credit Card Fee Sign

A 4% surcharge is the absolute ceiling allowed by Mastercard, American Express, and Discover, and only if your actual processing costs justify it. Businesses with higher-risk merchant accounts or specialized industries sometimes fall into this range. Before posting a 4% fee sign, verify with your payment processor that your rate supports it, because charging above your actual cost is a compliance violation.

Custom Percentage Credit Card Surcharge Sign

If your processing rate doesn’t land on a round number, your sign should still reflect the exact percentage your customers are being charged. The most important thing is accuracy. Whether it’s 2.75% or 3.25%, your credit card surcharge sign needs to match the actual fee, down to the decimal point. Overstating the surcharge, even by a fraction of a percent, can put you out of compliance with card network rules.

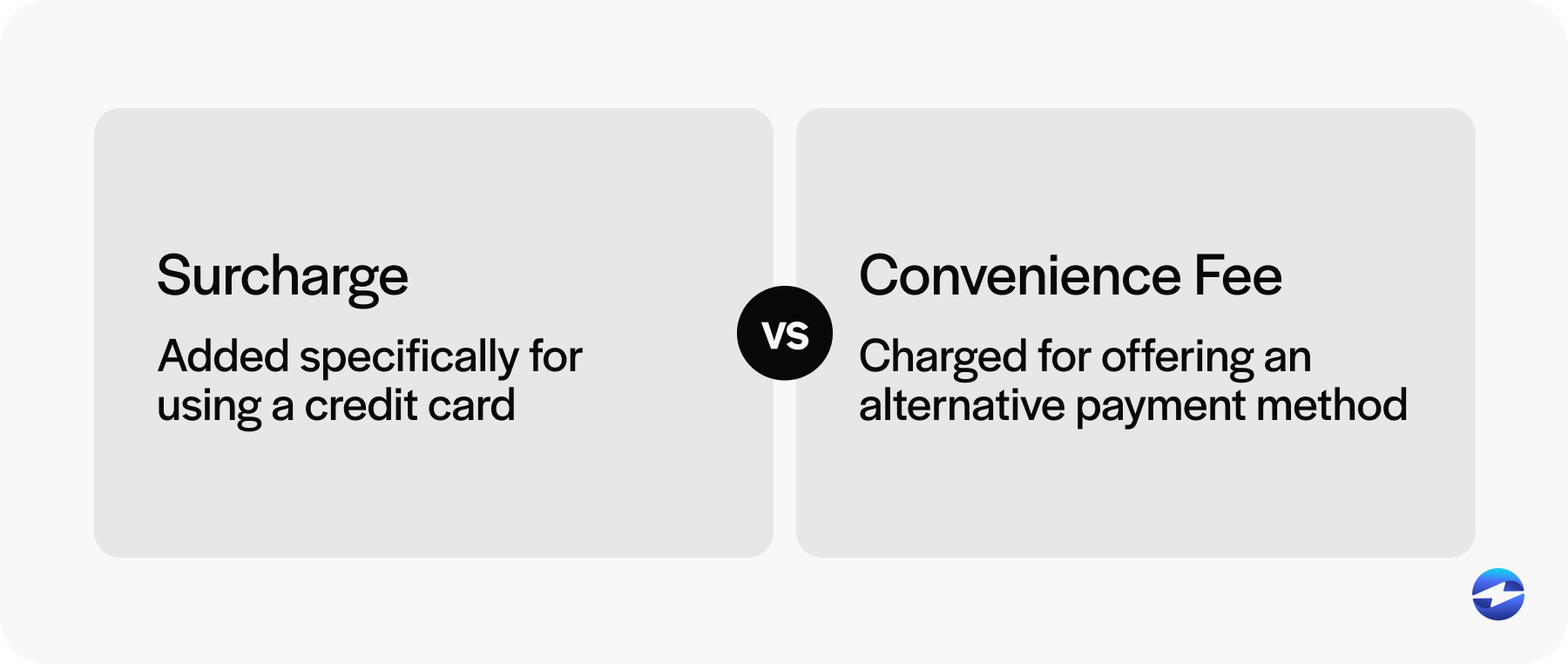

Credit Card Surcharge vs. Convenience Fee vs. Service Fee

These three terms get tossed around like they mean the same thing, but they don’t. If you’re posting a sign or disclosing a fee to customers, using the wrong label can create real problems.

A credit card surcharge is a fee added specifically to credit card transactions to help cover the cost of processing. It only applies to credit cards, and it’s regulated by the card networks. Visa, Mastercard, and the others each have their own rules about how much you can charge and how you have to disclose it. Surcharges cannot be applied to debit or prepaid cards.

A convenience fee is something different. It’s a charge for offering an alternative payment channel. For instance, if a utility company normally collects payments by mail but gives customers the option to pay by phone or online, they might add a convenience fee for that alternative method. The fee isn’t about the card type. It’s about the payment channel. Convenience fees tend to be regulated differently and are usually limited to card-not-present transactions.

A service fee is the broadest of the three. It’s a general charge a business adds for providing a service, and it doesn’t carry the same strict card network regulations as surcharges or convenience fees. That said, service fees still need to be disclosed upfront and can’t be misleading.

Here’s the practical takeaway for anyone printing a sign: make sure the language matches the type of fee you’re actually charging. Calling a surcharge a “convenience fee” or a “service fee” doesn’t just confuse your customers. It can trigger compliance issues with your payment processor or disputes from customers who know the difference.

| Credit Card Surcharge | Convenience Fee | Service Fee | |

|---|---|---|---|

| What it covers | Credit card processing costs | Alternative payment channel access | General service provision |

| Applies to | Credit cards only | Any payment via alternative channel | Varies by business |

| Regulated by | Visa, Mastercard, Amex, Discover | Card networks + state laws | General consumer protection laws |

| Debit cards included? | No | Depends on setup | Varies |

| Requires card network registration? | Yes | In some cases | No |

Credit Card Surcharge vs. Cash Discount Program

This is another comparison that comes up often, and it’s worth understanding the distinction before deciding which approach is right for your business.

A credit card surcharge adds a fee on top of the listed price when a customer pays with a credit card. The sticker price stays the same, and the surcharge appears as a separate line item at checkout.

A cash discount program works in the opposite direction. Your listed prices already include the cost of card processing, and customers who pay with cash receive a discount. The net effect on your margins is similar, but the framing is different, and so are the rules.

One of the biggest practical differences is legality. Surcharging is banned in a few states, but cash discount programs are generally legal everywhere because they’re structured as a discount rather than an additional fee. For businesses in Connecticut, Massachusetts, or Puerto Rico, a cash discount may be the only option for recovering processing costs.

The other difference is customer perception. Some businesses find that customers respond better to “save money by paying cash” than to “pay more for using a credit card.” It’s the same math, but framing matters.

If you’re unsure which route makes sense for your business, it’s worth talking to your payment processor. Solutions like EBizCharge support both surcharging and cash discount programs, so you can choose the approach that fits your market and your state’s regulations.

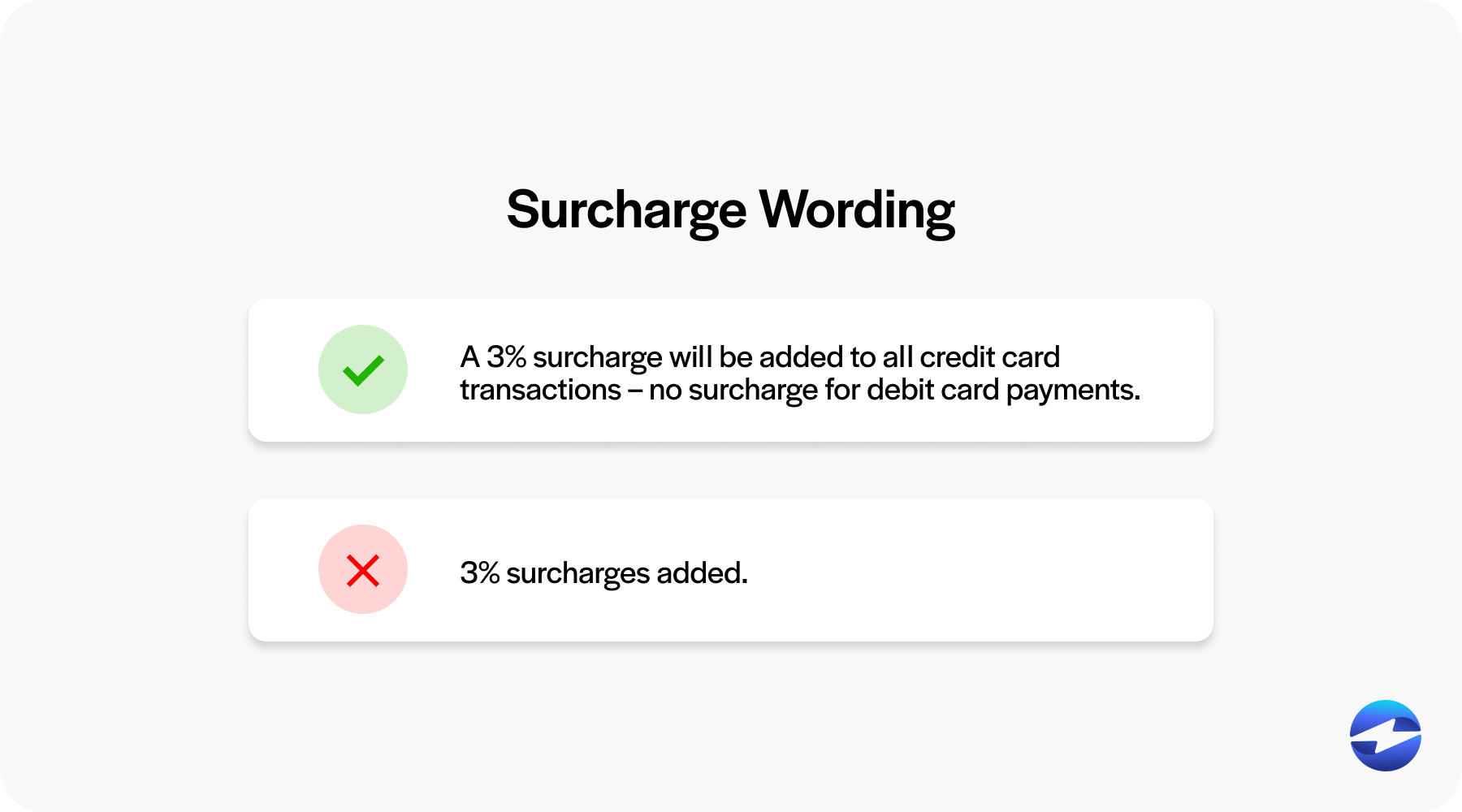

Sample Credit Card Surcharge Wording and Disclosure Language

Getting the wording right on your credit card fee notice matters more than you might expect. Vague or inaccurate language can lead to customer disputes, and card networks may flag your account if your disclosure doesn’t meet their standards.

Here are a few examples you can adapt for your business.

For in-store signage:

“A surcharge of [X]% is applied to all credit card transactions. This fee does not exceed our cost of acceptance and does not apply to debit or prepaid card payments.”

For online checkout pages:

“A surcharge of [X]% will be added to credit card payments at checkout. Debit and prepaid cards are not subject to this fee.”

For customer-facing emails or letters:

“Effective [date], a surcharge of [X]% will be applied to credit card transactions at [Business Name]. This fee helps offset credit card processing costs and will appear as a separate line item on your receipt. Debit and prepaid card payments are not affected.”

For receipts:

“Credit card surcharge ([X]%): $[amount]”

A few things to keep in mind when writing your disclosure. Always state the exact percentage. Always make it clear that debit and prepaid cards are exempt. And always present the surcharge as its own line item on the receipt. Rolling the surcharge into the product price or bundling it with other fees defeats the purpose of transparent disclosure and puts you at risk of non-compliance.

How to Set Up Credit Card Surcharging for Your Business

If you’ve decided to start surcharging, here’s a step-by-step overview of the process from start to finish.

- Check your state’s surcharge laws. Make sure surcharging is legal where you operate. If you’re in Connecticut, Massachusetts, or Puerto Rico, you’ll need to explore other options like a cash discount program.

- Review your processing rate. Contact your payment processor and confirm your exact credit card processing rate. Your surcharge cannot exceed this amount, and it also can’t exceed the card network caps (3% for Visa, 4% for others).

- Register with card networks. Submit your surcharge registration with Visa, Mastercard, American Express, and Discover at least 30 days before you plan to start surcharging. Also notify your acquiring bank and payment processor.

- Configure your payment system. Set up your POS terminal, payment gateway, or eCommerce checkout to automatically apply the surcharge to eligible credit card transactions. Make sure the system exempts debit and prepaid cards and displays the surcharge as a separate line item.

- Post your signage. Print and display your credit card surcharge sign at your entrance and checkout area. For online stores, add a clear disclosure on your checkout page. Use our free downloadable sign to get started.

- Train your staff. Make sure anyone who handles payments understands the surcharge policy, knows how to explain it to customers, and can distinguish between credit and debit transactions.

- Monitor and adjust. Review your surcharge settings periodically. Processing rates can change, and you’ll want to make sure your surcharge always matches your actual cost. If your rate drops, your surcharge should drop with it.

FAQs About Credit Card Surcharge Signs

Is it legal to charge a credit card fee?

Yes, credit card surcharging is legal in most U.S. states. As of 2025, the only places that prohibit it are Connecticut, Massachusetts, and Puerto Rico. Businesses in all other states can apply a surcharge as long as they follow card network rules around disclosure, registration, and fee limits.

What states don’t allow credit card surcharges?

Connecticut, Massachusetts, and Puerto Rico currently ban credit card surcharges. If you operate in one of these areas, a cash discount program is usually the alternative businesses use to offset processing costs.

Is a surcharge the same as a credit card fee?

They’re related but not the same thing. The credit card fee is what your business pays to the payment processor for handling the transaction. A surcharge is what you charge the customer to help cover that processing cost. The surcharge is the customer-facing version of the fee.

Can you surcharge a debit card?

No. Surcharges can only be applied to credit card transactions. Debit cards and prepaid cards are exempt, even if the customer selects “credit” at the terminal. Federal regulations prohibit surcharging debit transactions.

Do I need a separate sign for Visa surcharges?

You don’t necessarily need a separate sign, but you should be aware that Visa caps surcharges at 3%, while other card networks allow up to 4%. If you charge different rates by card brand, your payment system should handle that distinction automatically, and your signage should reflect the applicable rate.

Can I charge a credit card fee for online transactions?

Yes. Surcharges apply to both in-store and online transactions. For eCommerce, the surcharge must be disclosed on your checkout page before the customer enters their payment information. It can’t be buried in your terms of service or shown only after the purchase is complete.

What is the maximum credit card surcharge I can charge?

It depends on the card network. Visa limits surcharges to 3% of the transaction. Mastercard, American Express, and Discover allow up to 4%, or your actual processing cost, whichever is lower. You can never charge more than what your processor charges you.

How do I register my surcharge with card networks?

You need to submit a registration form to Visa and Mastercard through their online portals at least 30 days before you start surcharging. You also need to notify American Express, Discover, your payment processor, and your acquiring bank.

Can I use a convenience fee sign instead of a surcharge sign?

Only if you’re actually charging a convenience fee, which is a different type of charge with different rules. A convenience fee applies to alternative payment channels, not to the card type itself. Using the wrong label on your sign can lead to compliance issues and customer disputes.

Is a surcharge sign required by law?

Card networks like Visa and Mastercard require visible disclosure before the transaction takes place. While it may not be a specific state law in every jurisdiction, failing to post a surcharge sign can result in penalties from card networks, chargebacks from customers, and potential loss of your surcharging privileges. In practice, treating it as a requirement is the safest approach.

Can you surcharge American Express or Discover?

Yes, both American Express and Discover allow surcharging, but they have their own registration processes. You need to notify each network individually before you begin. The maximum surcharge for Amex and Discover follows the same general rule: 4% or your actual processing cost, whichever is lower.

Why do businesses charge a credit card fee?

Credit card processing isn’t free. Every time a customer pays with a card, the business pays a processing fee to the card network and payment processor. These fees typically range from 1.5% to 3.5% of the transaction amount. For businesses with tight margins, especially in retail, food service, or professional services, those costs add up fast. A surcharge lets the business recover that expense without raising prices for everyone, including cash-paying customers.

Does my surcharge sign need to show the exact percentage?

Yes. Your sign should display the exact surcharge percentage your customers will be charged. Vague language like “a small fee may apply” is not sufficient. Card networks require specific disclosure, and showing the actual rate builds trust with your customers.