6 Best Payment Processing Platforms for Convenience Stores

Convenience stores don’t have much margin for error. Customers expect to be in and out in under two minutes, and a payment system that fumbles a transaction creates real friction during the moments that matter most: the morning coffee rush, the midday fuel stop, the after-work snack run.

But speed isn’t the only thing that makes convenience store payment processing a distinct challenge. C-stores run a complex mix of product categories — tobacco, alcohol, lottery, food service, and sometimes fuel — each with its own compliance considerations and sales patterns, all at a transaction volume that makes credit card processing costs a number worth watching closely.

If you’re an independent c-store owner, a multi-site operator, or a store manager dealing with the payment side of the business, you already know most processors weren’t designed with your operation in mind. Many c-store operators end up with whatever payment processing software came bundled with their POS, and never evaluate whether it’s the right fit. This guide does that work.

Six Things a Convenience Store Needs from a Payment Processor

High transaction volume support comes first. A busy c-store may run 400 to 600 transactions per day — the payment processor needs to handle that without slowdowns or holds that back up the line.

Low per-transaction cost at scale is equally important. Thin margins mean that the difference between flat-rate and interchange-plus pricing across hundreds of daily transactions is real money by month-end. Payment processing fees that seem minor per transaction compound at c-store volume, and keeping those payment processing fees under control is one of the most direct ways to protect margin.

POS integration is non-negotiable. The payment processing platform needs to communicate with your POS natively — manual reconciliation wastes time and creates errors.

Chargeback management matters more than most operators think. High transaction volumes mean occasional disputes, and having documentation tools built into the payment processing solution protects revenue without requiring staff to become dispute experts.

For c-stores with an attached fuel operation, pump integration is also worth evaluating. Unified payment processing across inside sales and outdoor pumps beats running two separate systems.

The 6 Best Payment Processing Options for Convenience Stores

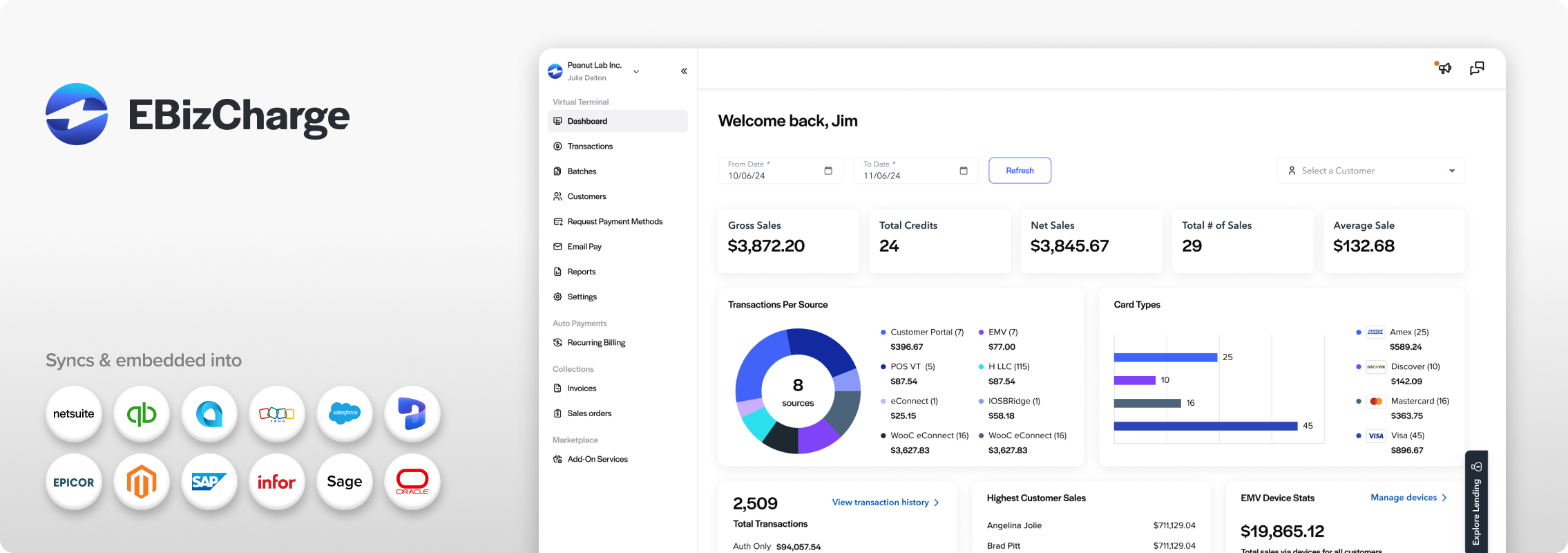

1. EBizCharge: Best Overall

EBizCharge is the strongest convenience store payment processing solution available for operators who want pricing transparency and back-office integration depth that most bundled or entry-level processors don’t offer.

The pricing model is where EBizCharge makes its most immediate impact. Running on interchange-plus pricing, the platform passes through the actual cost of each transaction rather than charging a flat rate. At the transaction volumes a busy c-store runs, the difference between interchange-plus and flat-rate credit card processing fees adds up to real money over a month and year.

The accounting integrations are deep and genuinely useful for c-store operators managing both inside sales and fuel revenue. EBizCharge connects natively with QuickBooks, Sage, and other platforms, so payment data posts automatically into financial records without manual reconciliation. For a business running on thin margins where every dollar of revenue needs to be tracked accurately, that automation matters.

The virtual terminal handles situations that don’t originate at the register — phone-in orders for c-stores with food service operations, catering invoices, or any other off-site transaction. It’s all handled from one platform without requiring separate tools.

The recurring billing engine handles corporate accounts and food service subscription programs automatically. The secure payment vault keeps commercial customers moving by storing payment details on file.

Chargeback management tools are built in. When a dispute comes up, EBizCharge provides the documentation and response capability to handle it without pulling staff off the floor. U.S.-based support is reachable when a payment issue disrupts a shift.

Verdict: EBizCharge covers the full billing picture of a convenience store operation without the hardware lock-in or opaque fee structures that come with some bundled alternatives.

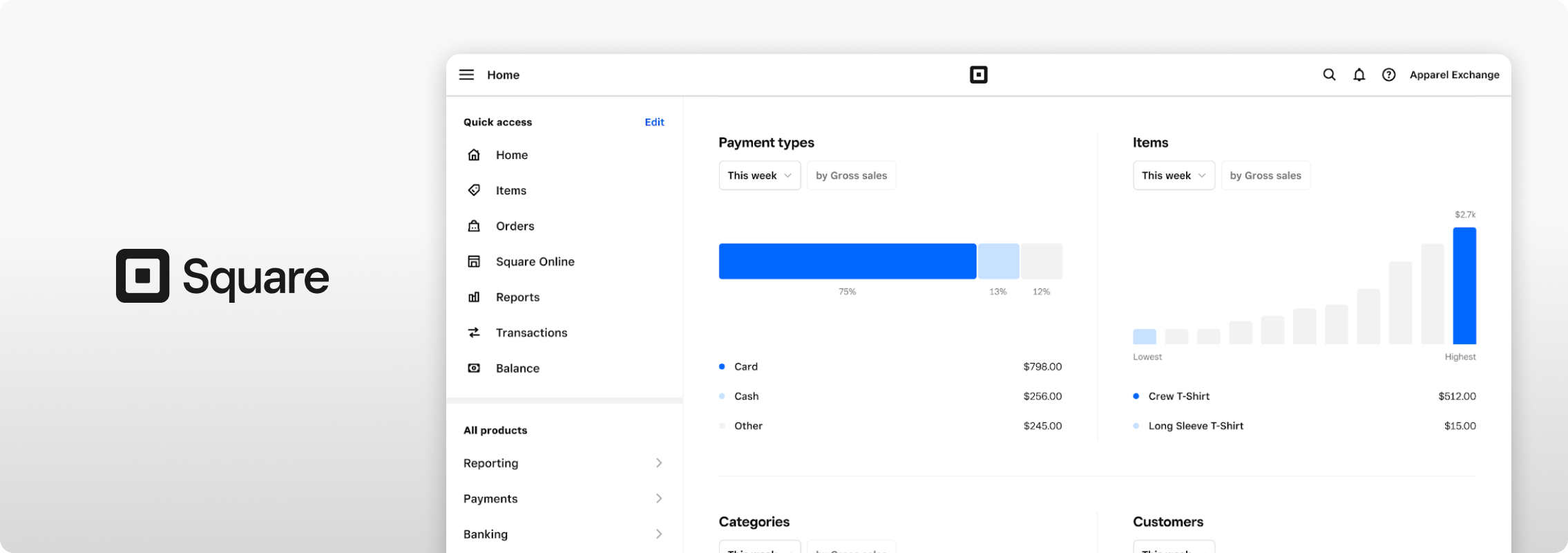

2. Square for Retail: Best for New or Smaller Operators

Square screen via squareup.com

Square has built a genuinely strong retail POS, and for a new or smaller c-store, it’s a legitimate starting point. The payment processing software covers inventory management, employee roles, and the interface itself well. Setup is fast, and the no-monthly-fee base plan keeps startup costs low.

The limitations become more visible as volume and complexity grow. Square’s flat-rate credit card processing means credit card processing fees don’t scale favorably at c-store transaction volumes. There’s no interchange-plus option. And while Square handles inside retail well, fuel pump integration is limited — not ideal for c-stores with an attached fuel operation.

Verdict: A reasonable entry point for small independent operators. Outgrown quickly as daily volume and billing complexity increase.

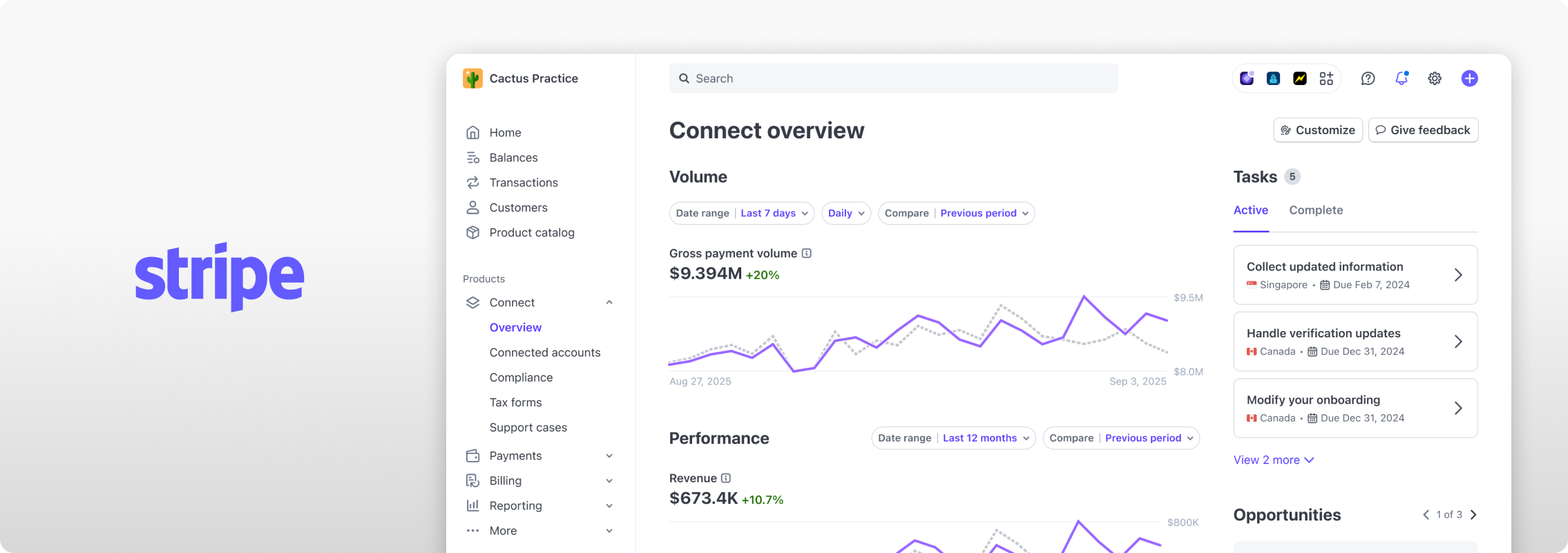

3. Stripe: Best for Multi-Site Brands Building Custom Platforms

Stripe screen via stripe.com

Stripe is a powerful payment processing platform for multi-site c-store brands building custom loyalty apps or order-ahead platforms. The API handles high transaction volumes and recurring billing well when configured.

The gap is that nothing works out of the box. No native c-store POS or fuel pump integrations exist, developer investment is required, and support is self-service.

Verdict: A strong payment processing system for tech-enabled brands with engineering resources. Not a practical option for most independent c-store operators.

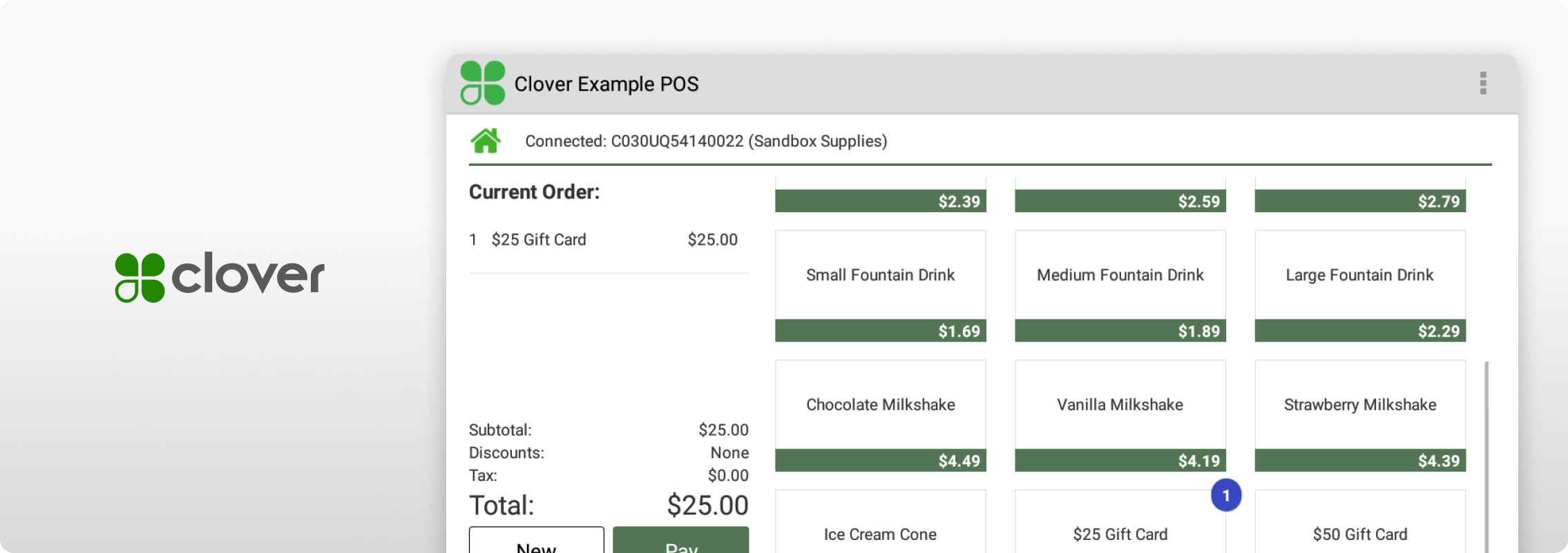

4. Clover: Best for Operators Who Want a Bundled Hardware-Software Solution

Clover screen via docs.clover.com

Clover is widely used in convenience retail. The hardware is purpose-built, the POS software is capable, and having payments, POS, and hardware from one provider simplifies vendor management.

The trade-offs are real. Clover devices are locked to Fiserv’s payment network, limiting your flexibility if costs or service become an issue. Monthly fees and hardware costs add up, and the pricing model deserves scrutiny before committing.

Verdict: A capable bundled option for operators who want simplicity and don’t mind the cost structure. Not the most cost-effective choice for high-volume operations.

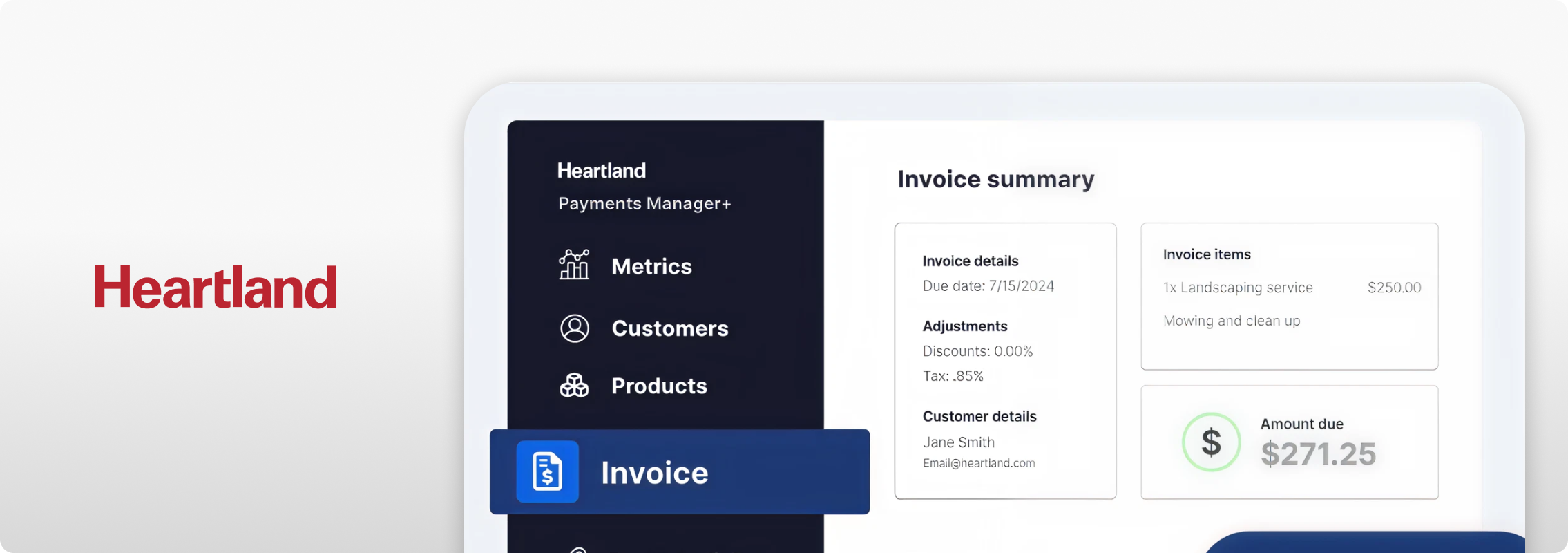

5. Heartland Payment Systems: A Traditional Processor Worth Comparing

Heartland screen via heartland.com

Heartland has real retail payment experience and integrates with several POS platforms used in convenience retail. Interchange-plus pricing is available to qualifying merchants, which is a meaningful differentiator.

Fee structure transparency and accounting software integration depth are where Heartland falls short relative to EBizCharge. Contract terms vary, and smaller operators may not receive consistent service.

Verdict: A legitimate payment processor to include in any comparison. EBizCharge edges it out on integration depth and pricing clarity for most c-store operators.

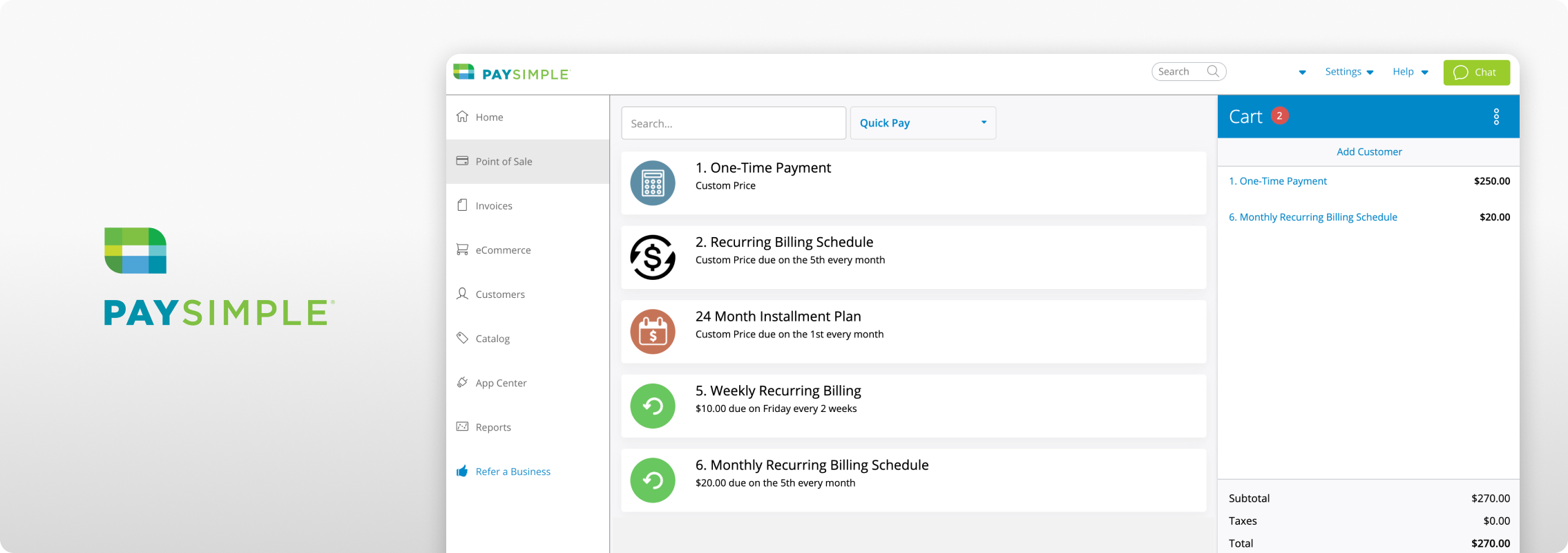

6. PaySimple: Best as a Supplemental Billing Tool

Paysimple screen via trustradius.com

PaySimple is built around recurring billing, and for c-stores running corporate accounts or food service subscriptions, those tools are solid. A self-service payment portal reduces billing-related back-office calls.

As a primary payment solution for daily in-store transactions, PaySimple doesn’t fit. It works as a supplemental payment solution for recurring billing, but no native POS integration, no fuel pump support, and chargeback tools are too basic for high-volume retail.

Verdict: A useful addition for c-stores with meaningful recurring account billing. Not a replacement for a primary payment processing solution that handles day-to-day retail volume.

Side-by-Side Comparison

| Feature |  |

|||||

|---|---|---|---|---|---|---|

| Pricing model | Interchange-plus | Flate rate | Flat rate | Hybrid | Interchange-plus if qualify | Flat rate |

| EMV compliance | ||||||

| Accounting integration | Extensive | Dev required | ||||

| Surcharging/cash discount | In beta | |||||

| Best for | All-around | Small/new stores | Custom platforms | Full-featured c-store POS | Multi-location operations | Service-oriented stores |

![]() = partial or varies

= partial or varies

Scroll to compare ![]()

The Right Payment Processor Is the One That Keeps Up with Your Store

Square is a solid starting point, but its payment processing system costs more per transaction at volume, and no payment processing system without interchange-plus can keep up with a busy c-store’s margin requirements. Clover is a capable bundle with a pricing model worth scrutinizing. Stripe is powerful for platform builders but impractical for most in-store operators. Heartland is a legitimate alternative but lacks EBizCharge’s integration depth. PaySimple fills a specific recurring billing niche.

EBizCharge is the only option that combines interchange-plus pricing at c-store volumes, deep accounting integration, virtual terminal capability, and chargeback management in one payment processing platform — without hardware lock-in or layered fees.

The cost case is concrete. A c-store running 500 transactions a day at an average of $12 is $6,000 in daily volume. The difference between flat-rate credit card processing fees and interchange-plus pricing on that volume across a full year can easily reach several thousand dollars. That money belongs in your operation.

Get paid faster with less work.

Get paid faster with less work.

3-minute product overview